Drug Delivery White Paper: Thriving Against the Capital Winter, Raising RMB 44.3 Billion in Three Years – Is 'Everything Conjugatable' the Ultimate Frontier?

Since the inception of modern pharmaceutical R&D, drug delivery has remained a consistent and central focus, with research in this field having been honored with the Nobel Prize on multiple occasions. In recent years, particularly with the advancement of emerging sectors such as nucleic acid therapeutics and gene-editing therapies, delivery systems have played an increasingly critical role in the druggability and development of new medicines.

The carrier itself is no longer merely a delivery tool; it has the potential to catalyze the emergence of innovative therapies. Companies with a profound understanding of delivery technologies are positioned to identify promising drug development opportunities early on and secure significant first-mover advantages.

The focus of drug delivery technologies in the modern pharmaceutical industry has shifted from conjugates to viral vectors and nucleic acid nanocarriers, and further to more cutting-edge yet highly promising areas such as exosomes and microneedle-based drug delivery.Even during the industry-wide downturn in recent years, it has remained highly active and even gained mainstream attention.According to incomplete statistics from VCBeat, a total of 42 financing and investment events occurred in China’s hot drug delivery sector in 2023, with the total amount reaching RMB 6.3 billion and an average financing amount of RMB 150 million.

This has sparked our keen curiosity about the currently popular drug delivery technologies. Why is the field of drug delivery experiencing robust growth against the prevailing trend? Is there an optimal drug delivery technology? Which drug delivery technologies hold the greatest development potential and deserve the most market attention at present? Which technological advancements and breakthroughs will profoundly shape the future development of drug delivery technologies?

Guided by these questions, VCBeat Research Institute has endeavored to seek answers from the industry. Regrettably, there is currently no industry research report that comprehensively presents the current state of research and provides a cross-sectional analysis of the entire drug delivery field—a gap that is undoubtedly significant for the industry as a whole. With this objective as its starting point, VCBeat Research Institute has authored the industry’s first white paper covering currently popular drug delivery technologies.A detailed study and exposition of current hot delivery technologies was conducted, along with a comprehensive review and summary of the technological pathways adopted by relevant domestic enterprises.for the benefit of readers.

Conjugation Technology

Bioconjugation is the process of linking two or more molecules or biomacromolecules via chemical covalent bonds. Common conjugation technologies include Antibody-Drug Conjugates (ADCs), Peptide-Drug Conjugates (PDCs), Radionuclide Drug Conjugates (RDCs), and GalNAc conjugation. Among these, the success of ADCs and the breakthrough role of GalNAc conjugation in advancing small nucleic acid therapeutics have been particularly notable, making conjugated drugs a focal point of the industry.

1ADC: Largely based on “micro-innovations” of leading foreign technologies, yet holding the potential to surpass their origins.

ADC (Antibody-Drug Conjugates) is currently the most prominent and mature conjugated targeted therapy technology.

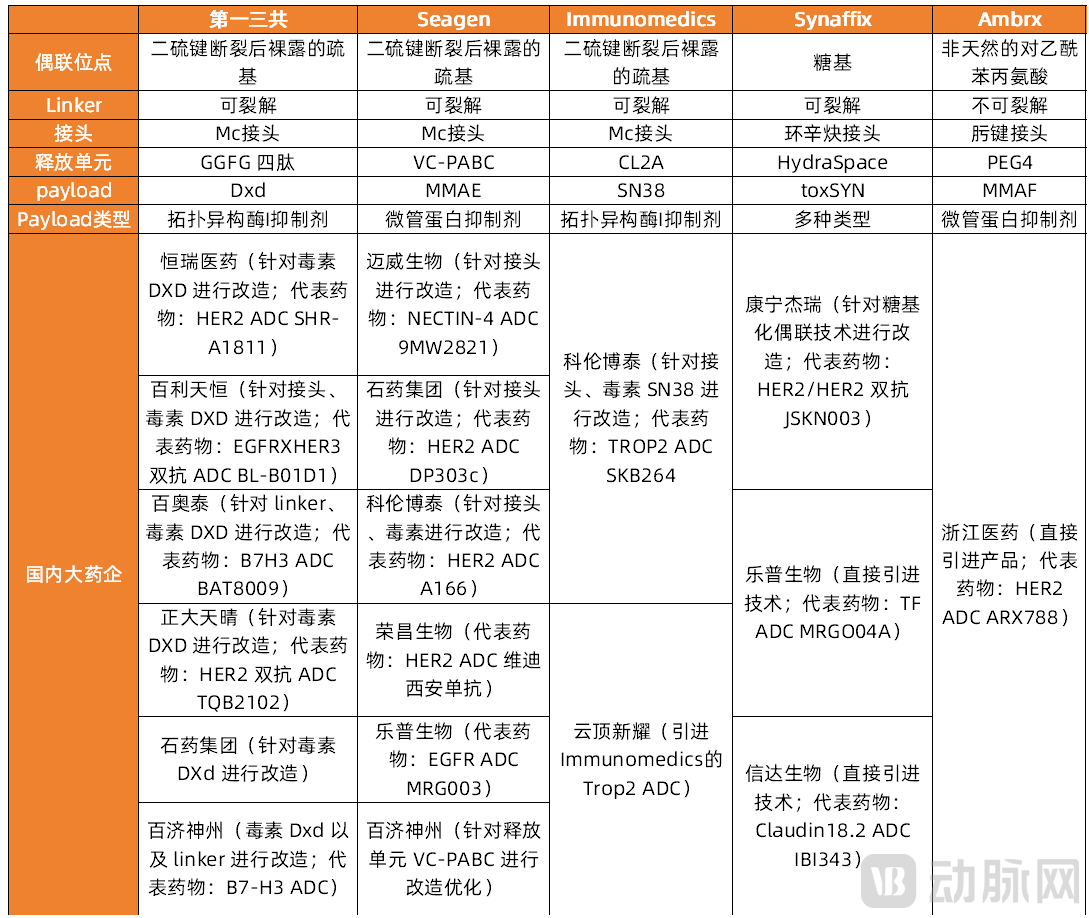

Given the optimistic outlook on the development potential of antibody-drug conjugate (ADC) therapies, numerous pharmaceutical companies worldwide have strategically positioned themselves in ADC research and development.Companies including Daiichi Sankyo, Seagen, Immunomedics, Ambrx, Synaffix, ImmunoGen, Mersana, NBE Therapeutics, Zymeworks, and Alteogen each possess unique strengths in the field of antibody-drug conjugate (ADC) technology. Among them, Daiichi Sankyo and Seagen stand out as the most prominent and representative players; accordingly, this report provides a detailed analysis and introduction using these two companies as case studies.

Foreign Companies with Proprietary ADC Technologies

Data sources: Official websites of respective companies, YaoYanNet, VCBeat

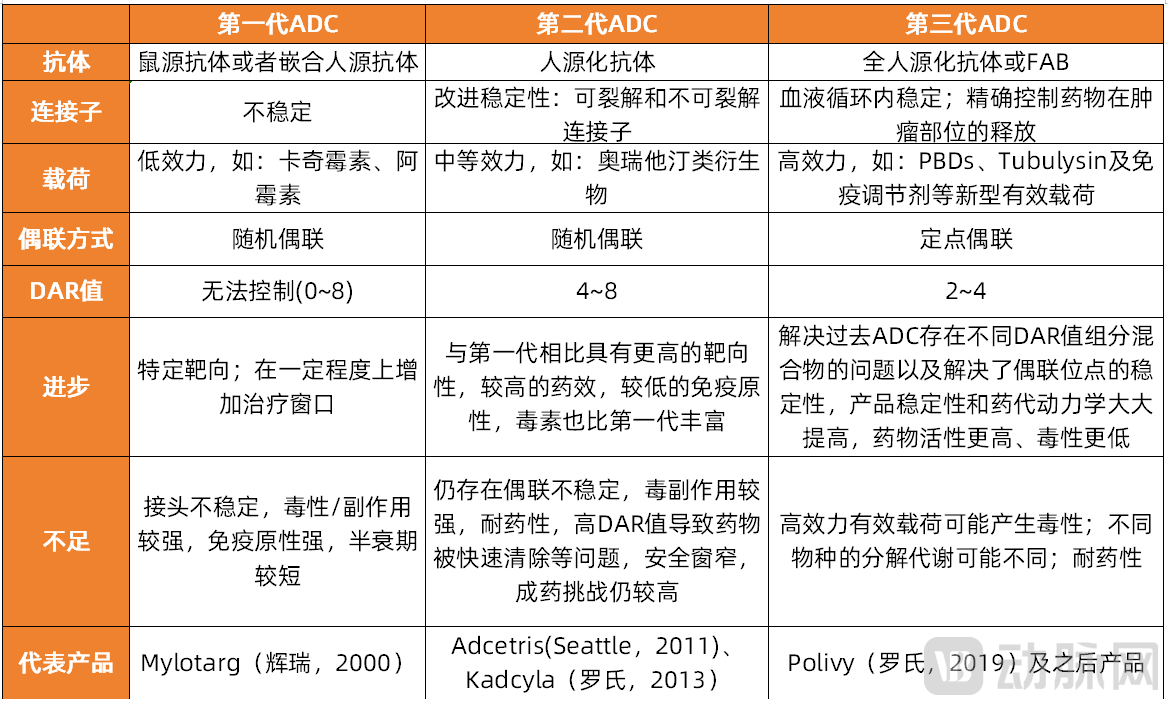

ADC research has a history spanning over a century, and while it has evolved to third-generation technology, there remains significant room for optimization.As early as the early 20th century, Paul Ehrlich first proposed the concept of the “magic bullet.” However, in the early stages of antibody-drug conjugate (ADC) development, progress was slow and fraught with challenges due to high technical barriers in synthesis, long-standing issues of off-target effects, and difficulties in identifying specific antigens. It was not until 2000, when the U.S. Food and Drug Administration (FDA) approved the first ADC drug, Mylotarg®, for the treatment of adult acute myeloid leukemia (AML), that the era of ADC-targeted cancer therapy officially began. Although ADC technology has now advanced to its third generation, significant room for optimization remains, such as reducing drug toxicity and addressing drug resistance.

ADC Technology Has Now Evolved to the Third Generation

Data source: Compiled from public information; chart by VCBeat.

Furthermore, antibody-drug conjugates (ADCs) are a class of products with a high degree of system integration. Their research and development require extensive proprietary expertise and capabilities in biology, chemistry, and manufacturing, posing numerous challenges in design and development.Future directions for improvement and innovation include: low toxicity, high efficacy, reduced production costs, increased patient accessibility, clinical combination with other drugs, and pan-cancer applications.

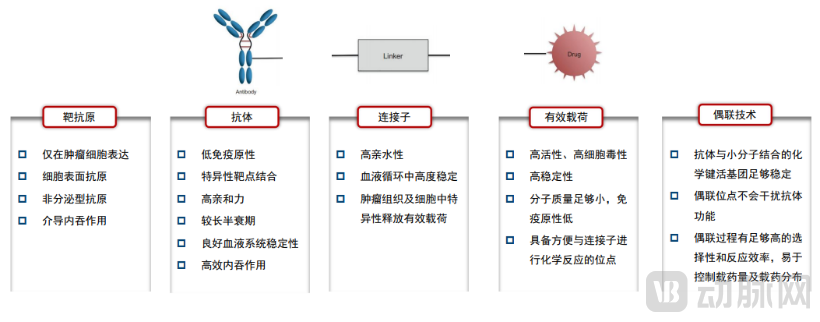

Structurally, antibody-drug conjugates (ADCs) primarily consist of three structural modules: the antibody (targeting moiety), the linker, and the small-molecule toxin (payload). Innovations in ADC drugs are mainly driven by advancements in these components, as well as by the identification of novel target antigens and the adoption of different conjugation strategies.

Five Key Elements to Consider in ADC Drug Design and Their Ideal Development Scenarios

Image source: Huajin Securities

In the search for new target antigens,Identifying highly specific tumor targets, targeting the tumor microenvironment (TME), and seeking non-internalizing antigens as targets are current hotspots in ADC development.In the selection and innovation of antibodies (targeting moieties),In addition to the development of monoclonal antibody-based ADCs, research into related modalities such as bispecific antibody-drug conjugates (BsADCs) and probody-drug conjugates is emerging as a focal point in the industry.

In terms of connexins,The development of cleavable or non-cleavable linkers with enhanced efficiency (enabling the release of small-molecule toxins at the target site), high stability in systemic circulation, and improved aqueous solubility (to prevent the formation of ADC aggregates) through chemical modification represents a key direction for innovation in antibody-drug conjugates.

High DAR Values Combined with Low-to-Medium Toxicity Technological Approaches’s success has injected new vitality and greater imaginative potential into global ADC drug development. ADC drugsInnovation Directions Based on PayloadIt also includes the development of dual payloads, non-internalizing payloads, and others.

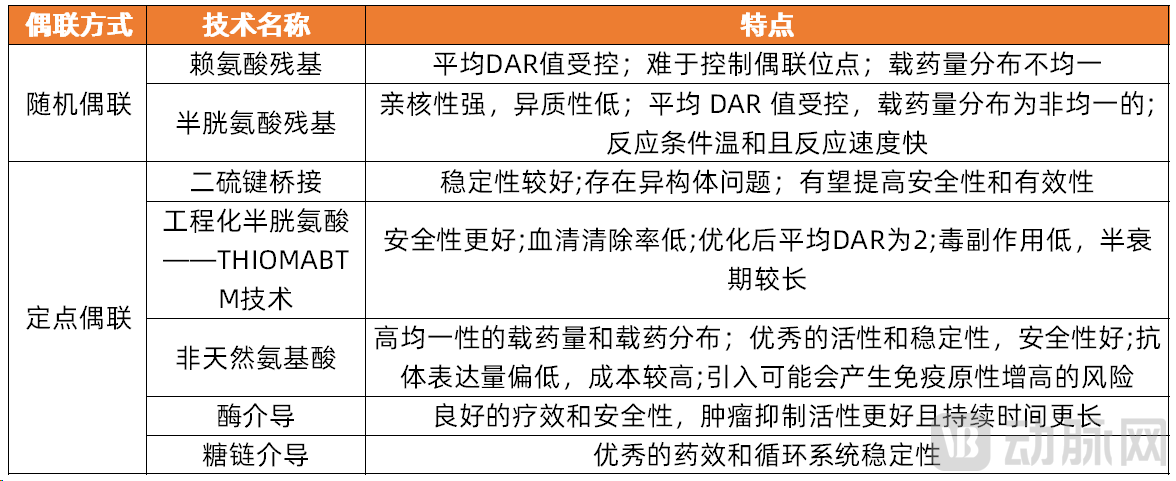

Site-Specific Conjugation TechnologyA more uniform DAR and drug-loading method, along with improved stability, are expected to yield ADC drugs with superior safety and efficacy, thereby widening the therapeutic window.

Characteristics of Random Conjugation and Site-Specific Conjugation Technologies

Source: Public information; graphic by VCBeat

In addition to innovating proprietary structural modifications of ADCs, exploring combination therapies and other approachesIt is also an important strategy and research direction for achieving better efficacy of ADCs and overcoming drug resistance.

Domestic ADC Industry Development: Widespread Adoption of "Micro-Innovation" to Circumvent Patent Barriers.As foreign entities took the lead in deploying antibody-drug conjugate (ADC) technology, they currently hold over 72% of ADC-related patents, leaving China’s ADC development relatively lagging. The deep expertise cultivated by industry leaders such as Daiichi Sankyo, Seagen, and ImmunoGen in the ADC field has formed formidable barriers for Chinese pharmaceutical companies.

To circumvent patent barriers,Most ADC companies in China have optimized and modified the technological platforms of firms such as Daiichi Sankyo, Seagen, Immunomedics, Synaffix, and Ambrx through “micro-innovations” to circumvent patent barriers, or have directly licensed related products or platform technologies.

Listed pharmaceutical companies in China are pursuing micro-innovations in ADC technology or directly licensing technologies/products for their ADC drug development pipelines.

Data sources: Company websites, company patents, Essence Securities Research Center; graphic by VCBeat.

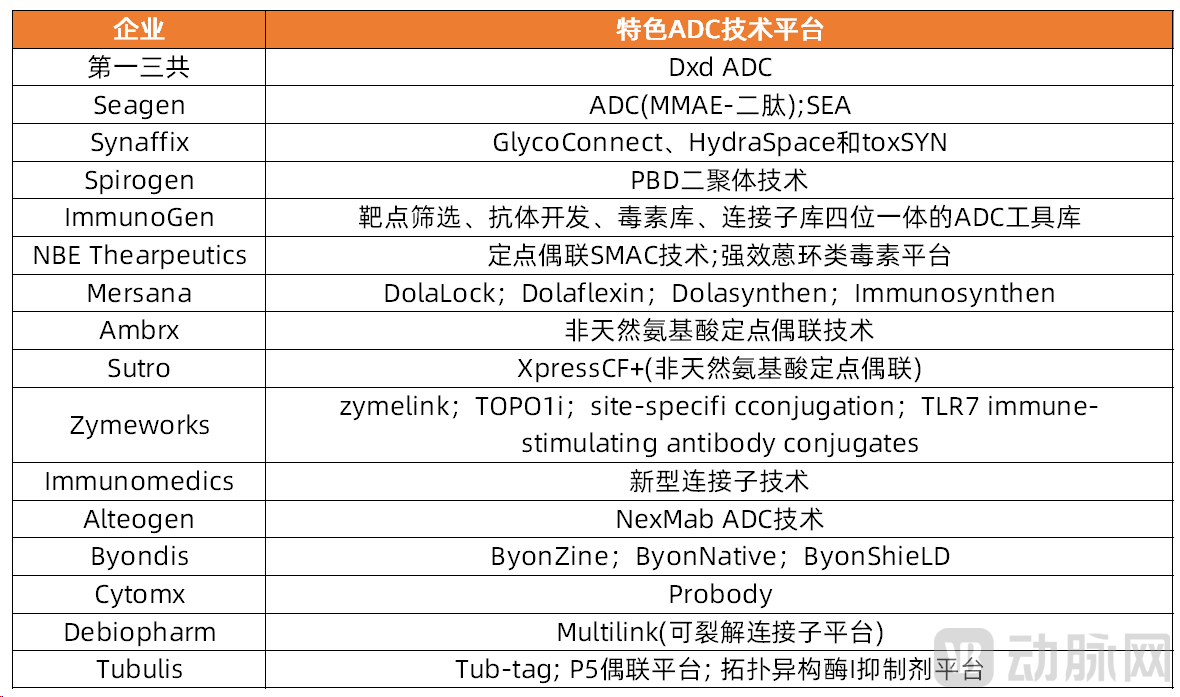

Distinctive ADC Technology Platforms of Selected Listed Pharmaceutical Companies in China

Image source: Official websites/annual reports/semi-annual reports of respective companies, Huajin Securities Research Institute

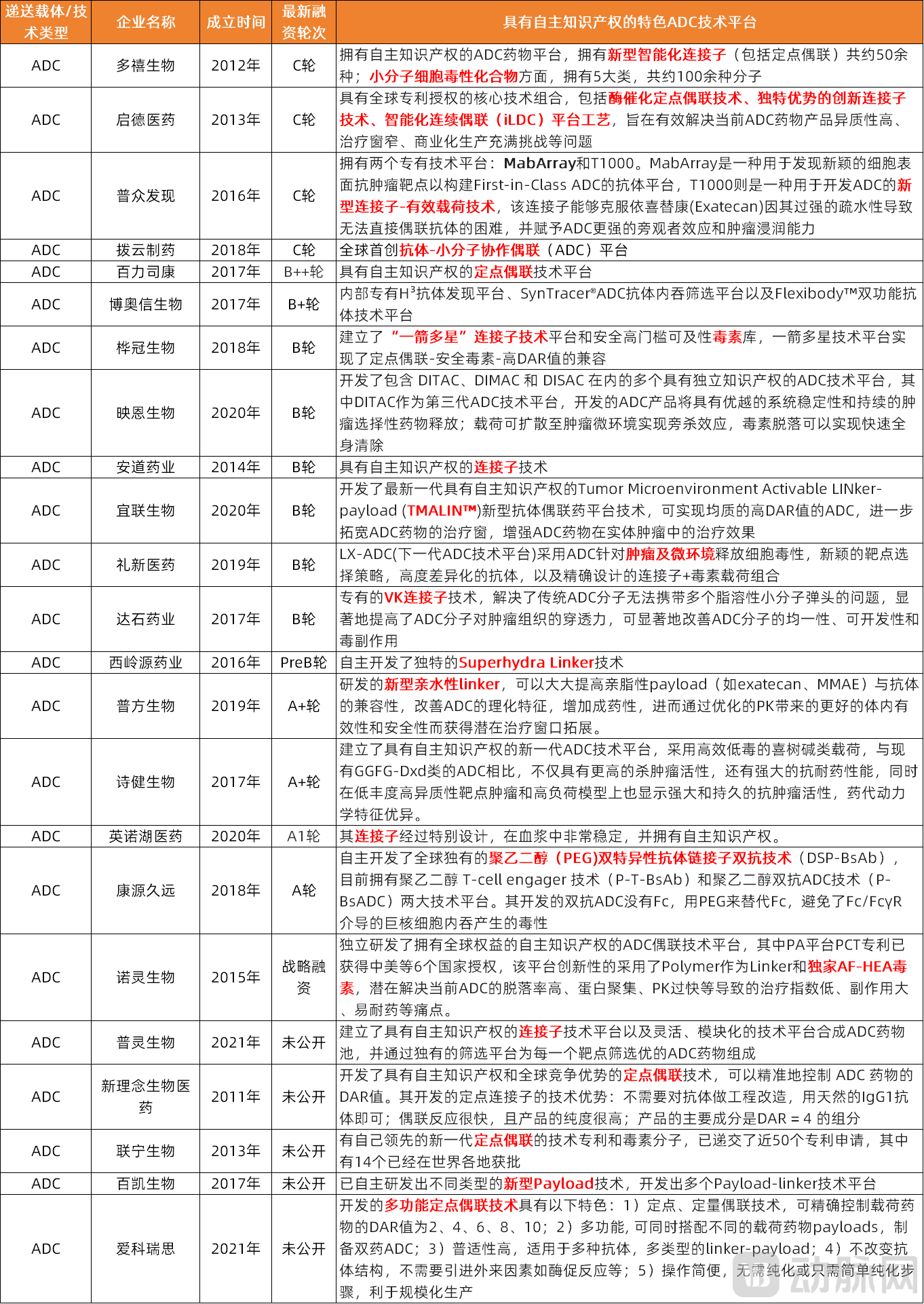

In addition to listed pharmaceutical companies,In response to the limitations of existing ADC drugs, several emerging startup ADC companies have also rapidly developed, establishing ADC technology platforms with independent intellectual property rights,VCBeat has conducted a comprehensive review and analysis of the technological pathways adopted by relevant startups.

Startups with Proprietary ADC Technology Platforms and Their Distinctive Technologies

Source: Company websites and public reports; chart by VCBeat

It can be observed that,Numerous domestic startups are driving innovation across the dimensions of targeting moieties, payloads, and linkers.Established an ADC technology platform with independent intellectual property rights, and throughIn-house R&D, Collaborative DevelopmentADC drugs orEmpowermentIndustry enterprises are developing ADC drugs.

Although most ADC drugs in China are categorized as incremental innovations and optimized modifications,ADC drugs developed by some pharmaceutical companies are undoubtedly beginning to demonstrate the potential to “surpass their predecessors.”

asMabwell BiosciencesAlthough the first-generation ADC technology was developed based on Seagen’s ADC platform, it diverged from the traditional maleimidocaproyl (MC) linker. Instead, it employed a design capable of simultaneously conjugating to the two exposed sulfhydryl groups following disulfide bond cleavage, thereby achieving site-specific conjugation. In Phase II clinical trials, 9MW2821 demonstrated an objective response rate (ORR) of 50% and a disease control rate (DCR) of 100% among 12 patients with urothelial carcinoma. Among 6 patients with cervical cancer, the ORR was 50% and the DCR was 100%. In non-head-to-head comparisons with agents such as enfortumab vedotin and sacituzumab govitecan in these patient populations, 9MW2821 showed certain advantages in terms of ORR.

For example,RemeGenRC48, the first domestically developed ADC drug, was also created based on Seagen’s ADC technology platform and has earned recognition from Seagen: in June 2021, Seagen acquired the rights to this drug for a total consideration of $2.6 billion.

“Standing on the Shoulders of Overseas Giants”: Domestic ADC Players Are Venturing Further.

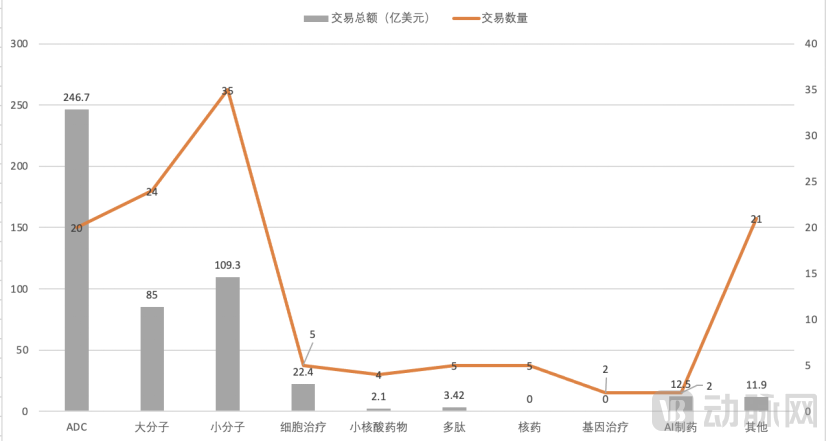

In 2023, ADCs emerged as the most prominent area of breakthrough in business development (BD) transactions in China.—In 2023, a total of 20 BD deals were concluded in the ADC field, with a total value reaching $24.67 billion.

2023 Statistics on BD Deals Across All Sectors of the Biopharmaceutical Industry

Data source: VBNewMed, VCBeat

2023 Overview of ADC Business Development and Licensing Deals Among Chinese Pharmaceutical Companies

Data Source: VCBeat New Medicine, VCBeat Research Institute

On the other hand, as technology and product imports become increasingly prevalent, market competition has further intensified.Domestic ADC R&D is entering a more challenging phase, driving genuine innovation and optimized design, ultimately translating into clinically superior drugs. These products are poised to capture larger market shares through license-out deals or simultaneous development in China and the United States.

2GalNAc: Domestic startups raise nearly RMB 1.5 billion in the past three years, driving innovations in delivery efficiency and drug durability

GalNAc (N-acetylgalactosamine) conjugation is another well-known hotspot conjugation technology in the industry, primarily used for the delivery of small nucleic acid drugs. It addresses the historical challenges encountered in the development of small nucleic acid drugs.Poor targeting, severe off-target effects, and poor stability...and other pain points, bringing significant progress to the field of liver-targeted therapies and representing a major breakthrough in the development of oligonucleotide drugs.

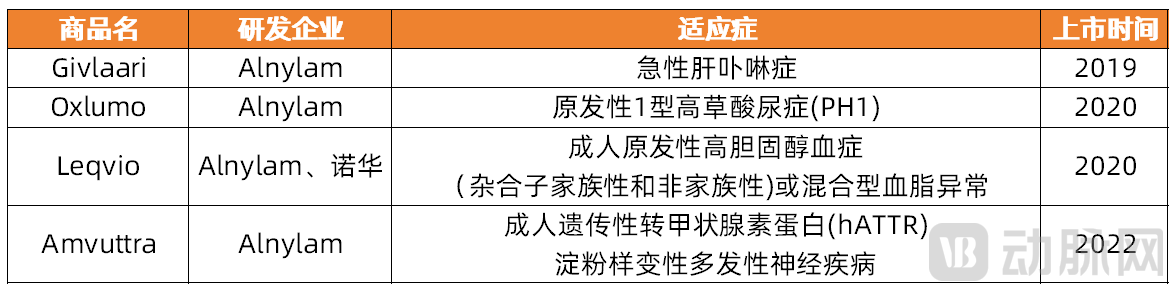

Following the 2018 market launch of ONPATTRO, the first siRNA drug (which utilizes an LNP delivery system), the subsequent four siRNA drugs were all developed based on the GalNAc delivery system, including Givlaari, Leqvio, Oxlumo, and Amvuttra.

GalNAc-Based Delivery Systems for Marketed Oligonucleotide Drugs

Source: Public information; chart by VCBeat.

As a delivery technology that also drives the breakthrough development of oligonucleotide drugs,Both GalNAc and LNPs exhibit robust hepatic accumulation and uptake; however, GalNAc offers distinct advantages over LNPs:Clinically, GalNAc-conjugated oligonucleotide drugs administered via subcutaneous injection (as intravenous administration leads to rapid renal clearance) achieve favorable drug distribution, prolong circulation time, and sustain therapeutic effects for several months up to half a year. Furthermore, the subcutaneous route is more convenient and easier to administer, thereby reducing the treatment burden on patients. Due to the high-efficiency hepatic targeting of GalNAc, lower drug doses are required, resulting in fewer side effects, a lower incidence of related local adverse events, and improved safety and tolerability.

AlnylamPossession of key patents covering GalNAc delivery technology, including GalNAc ligands, linkers, and GalNAc-oligonucleotide conjugates, has hindered numerous domestic and international companies from entering the small nucleic acid drug sector. However,In addition to Alnylam, other GalNAc-based technology platforms include Dicerna’s GalXC, Arrowhead’s TRiM, and Ionis’ LICA.

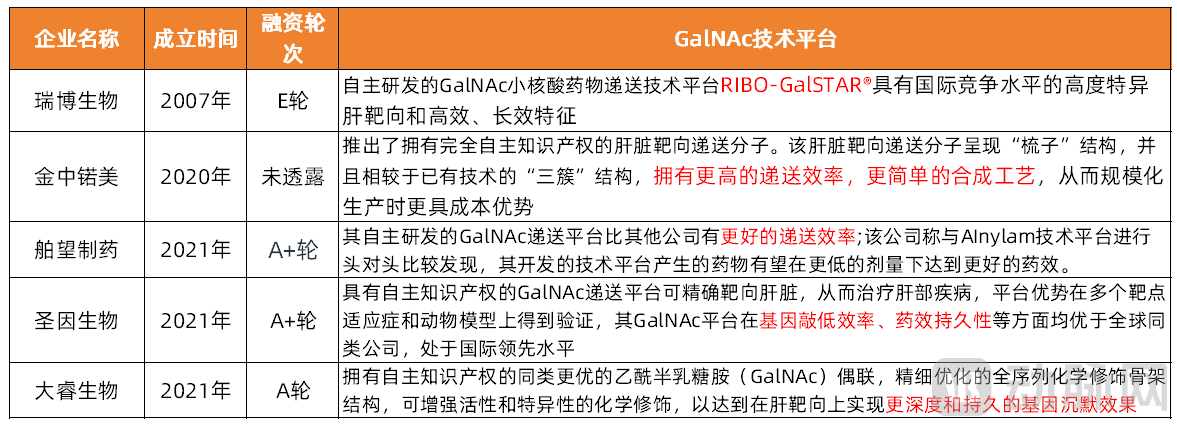

Currently in China, includingStarnovo, Ribo Life Science, Bowang Pharma, Shengyin Biopharma, etc.Companies, among others, have also mastered GalNAc delivery system technology and achieved a certain degree of innovation, possessing independently owned intellectual property rights for their GalNAc delivery technology platforms.

Introduction to Domestic Startups with Independent Intellectual Property Rights in GalNAc Delivery Technology Platforms and Their Technical Platforms

Data source: Company websites and public reports; chart by VCBeat

GalNAc delivery technology offers significant advantages, but it also has limitations, such as being able to target only hepatocytes and being restricted to applications in the field of small nucleic acid drugs. CurrentlyIn China, the primary directions for improving GalNAc-conjugated delivery technology itself include enhancing its delivery efficiency and prolonging the duration of drug action in vivo.

For extrahepatic delivery, it is generally necessary to identify GalNAc-like ligands.(GalNAc-like ligand)or conjugation modification with other novel ligandsFor example, O-hexadecyl (C16)-modified siRNA can penetrate the central nervous system (CNS), eyes, or lungs. Alnylam’s extrahepatic delivery ligand discovery platform is developing various ligands, including small molecules/lipids (such as C16 for CNS delivery), peptides, and antibodies. DTx’s FALCON™ platform, based on fatty acid modification, can target diverse extrahepatic tissues, such as Schwann cells in the peripheral nervous system.

3Innovations in Targeting Moieties and Payloads Enable “Universal Conjugation,” with Novel Technologies Such as PDCs and RDCs Unlocking Significant Potential

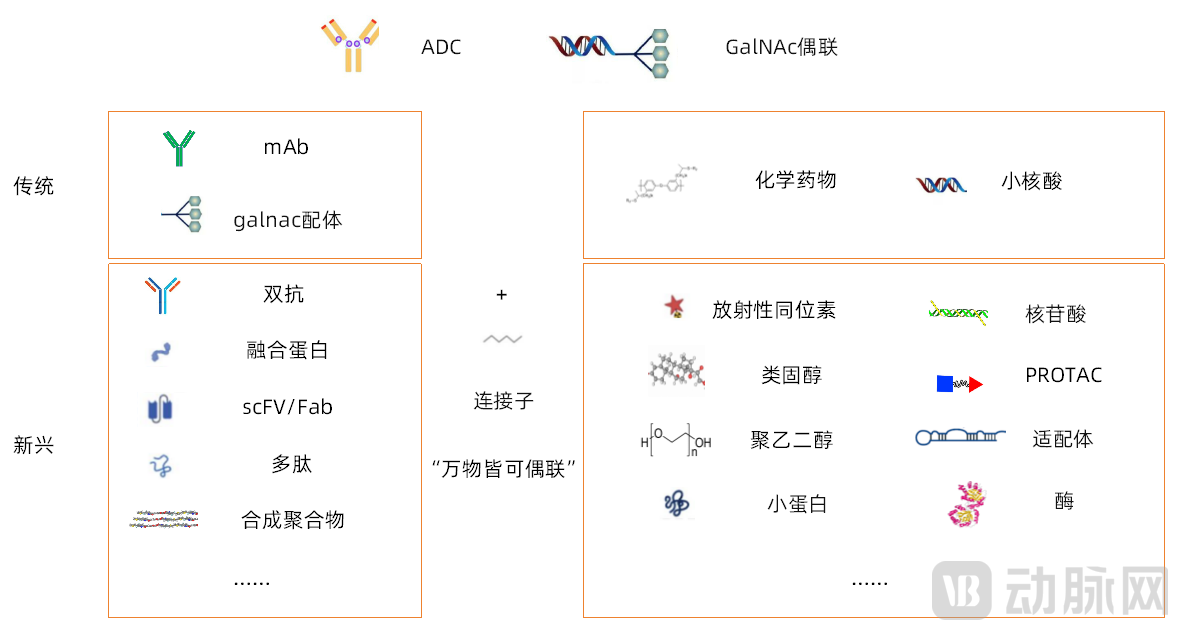

With the in-depth development of ADC and GalNAc technologies, the concept of “selectively delivering therapeutic agents to disease sites via targeting ligands to exert therapeutic effects”The design concept is further expanded and extended, leading to the development of additional conjugation formats and technologies by varying the types of targeting moieties and payloads.Expand the indications of conjugated drugs from oncology to cardiovascular diseases, diabetes, autoimmune disorders, and other fields, while extending the target sites from tumors and hepatocytes to other tissues.

Bioconjugation is expanding beyond traditional conjugation modalities, exhibiting a development trend where “everything can be conjugated.”

Image source: VCBeat

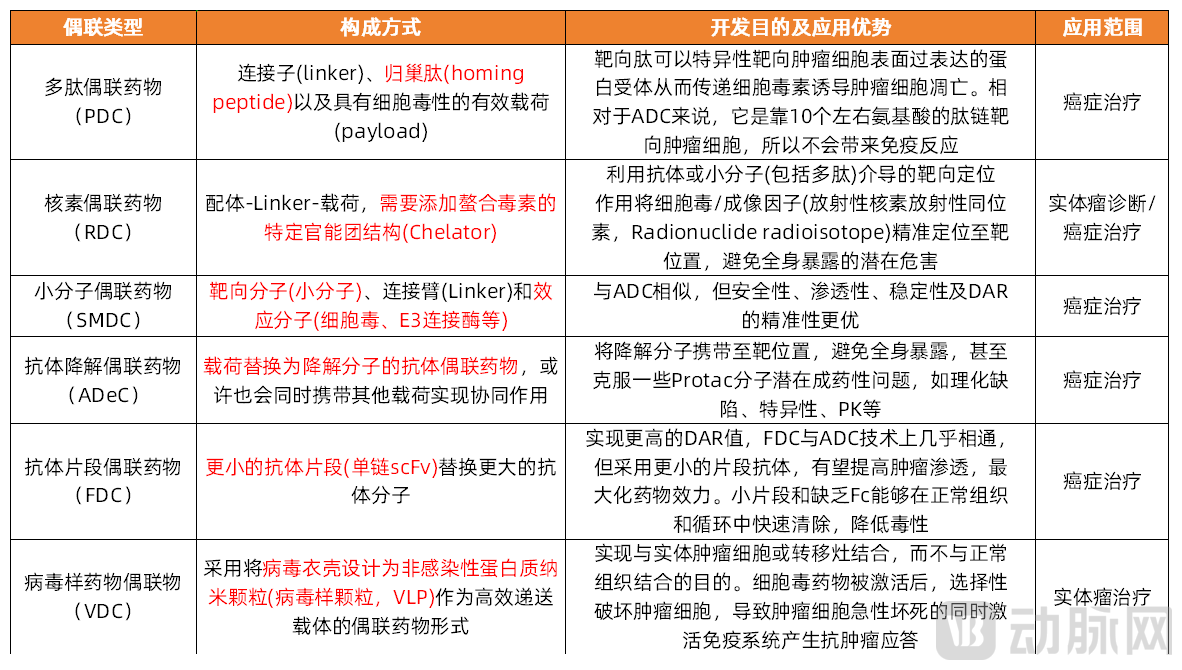

Besides ADCs and GalNAc, Several Common Types of Emerging Conjugate Drugs

Data Source: Patsnap, VCBeat

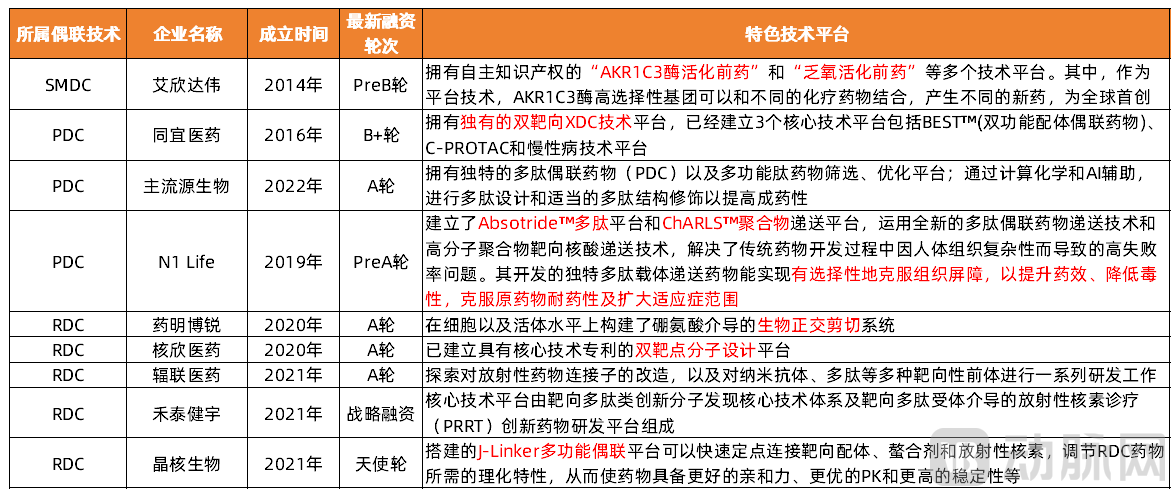

Among them,PDCs, RDCs, and SMDCs are areas, apart from ADCs and GalNAc-based therapies, where Chinese companies have made significant inroads and achieved rapid development.VCBeat has conducted a comprehensive review of domestic startups and the development trajectories of their distinctive technologies.

Proprietary Conjugation Technology Platform with Distinctive Features

Data source: Official company websites and public reports; chart by VCBeat.

Mainstream Viral Vectors

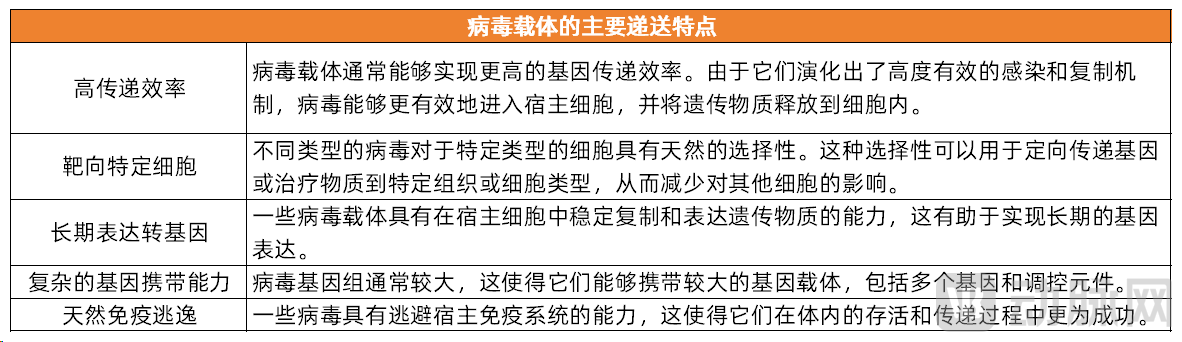

Viruses have an evolutionary history far exceeding that of humans,Possesses the ability to efficiently penetrate cell membranes,Characterized by high transduction efficiency, specific cell targeting, long-term transgene expression, the capacity to carry large gene fragments, and natural immune evasion, as well as scalability for mass production, it is widely applied in vaccines, gene therapy, and cell therapy.

Among the COVID-19 vaccines approved globally, four vaccines—those developed by Johnson & Johnson, AstraZeneca, CanSino Biologics, and Russia’s Gamaleya Research Institute—are all viral vector vaccines; additionally, according to data from the ASGCT,89% of cell and gene therapy pipelines in development utilize viral vectors as delivery systems.

Key Delivery Characteristics of Viral Vectors

Data source: Public information; chart by VCBeat.

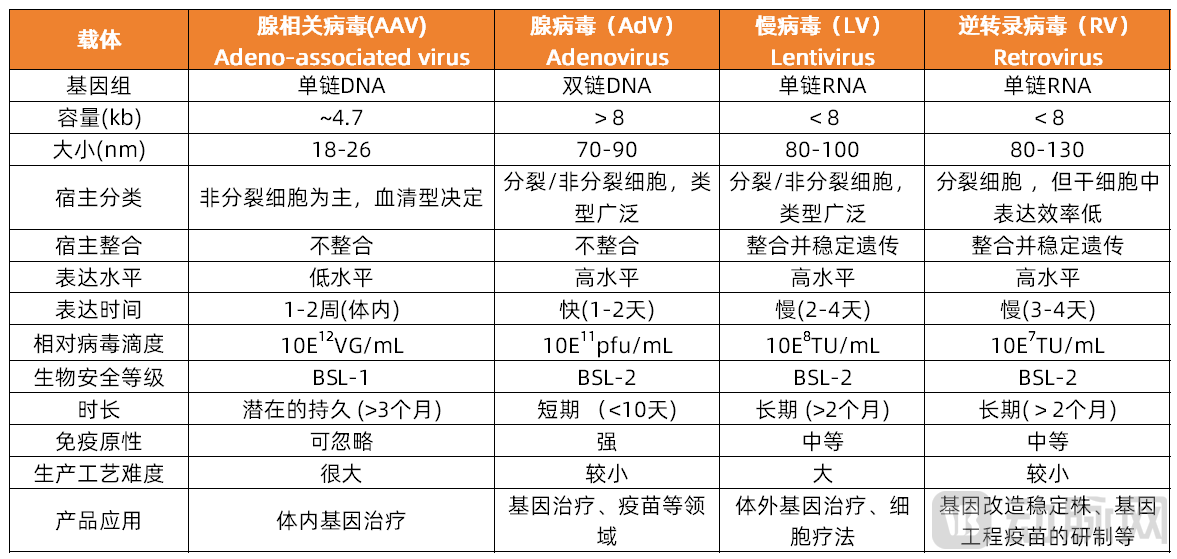

Currently, common viral vectors include adenovirus (Adenovirus, AdV), adeno-associated virus (Adeno-associated virus, AAV), lentivirus (Lentivirus, LV), and retrovirus (Retrovirus, RV).

Mainstream Viral Vectors

Image source: Public information

The four commonly used viral vectors each have their own advantages and disadvantages, making them suitable for different scenarios.

Distinct Characteristics of Mainstream Viral Vectors

Source: Compiled from public information; chart by VCBeat.

The white paper provides a detailed introduction to the unique advantages, primary application scenarios, and developmental iterations of the four mainstream viral vectors. Due to space constraints, this section offers only a partial discussion on AAV, which is currently the most widely used vector in industrial applications.

AAVThey are a class of naturally occurring, non-pathogenic viruses whose genome consists of a single-stranded DNA molecule approximately 4.7 kb in length.As the most widely used in vivo gene therapy delivery vector currently, AAV features high safety, a broad range of host cells, and long-term expression in vivo.It is currently the only viral vector with an NIH risk group 1 (RG1) rating, and no pathogenicity associated with wild-type AAV has been reported to date. Several AAV-based gene therapy products have already received regulatory approval for market launch, and hundreds of AAV therapies are currently undergoing clinical trials.

AAV does not integrate into the genome, thereby lacking oncogenic potential; furthermore, its low intrinsic immunogenicity minimizes immune rejection, offering significant advantages over other viral vectors. However, AAV is typically replication-defective and can only replicate in the presence of helper viruses (such as adenovirus, herpes simplex virus, or vaccinia virus). Recombinant AAV (rAAV) has 96% of the wild-type AAV genome removed, further ensuring its safety.

AAV Applications Offer Significant Advantages, but Also Have Notable Drawbacks:If the packaging capacity is too small (approximately 4.7 kb), challenges related to neutralizing antibodies make repeat dosing difficult, thereby limiting application scenarios. Furthermore, given the prolonged timeline from AAV infection to transgene expression, reducing production costs has become a key focus for all stakeholders.

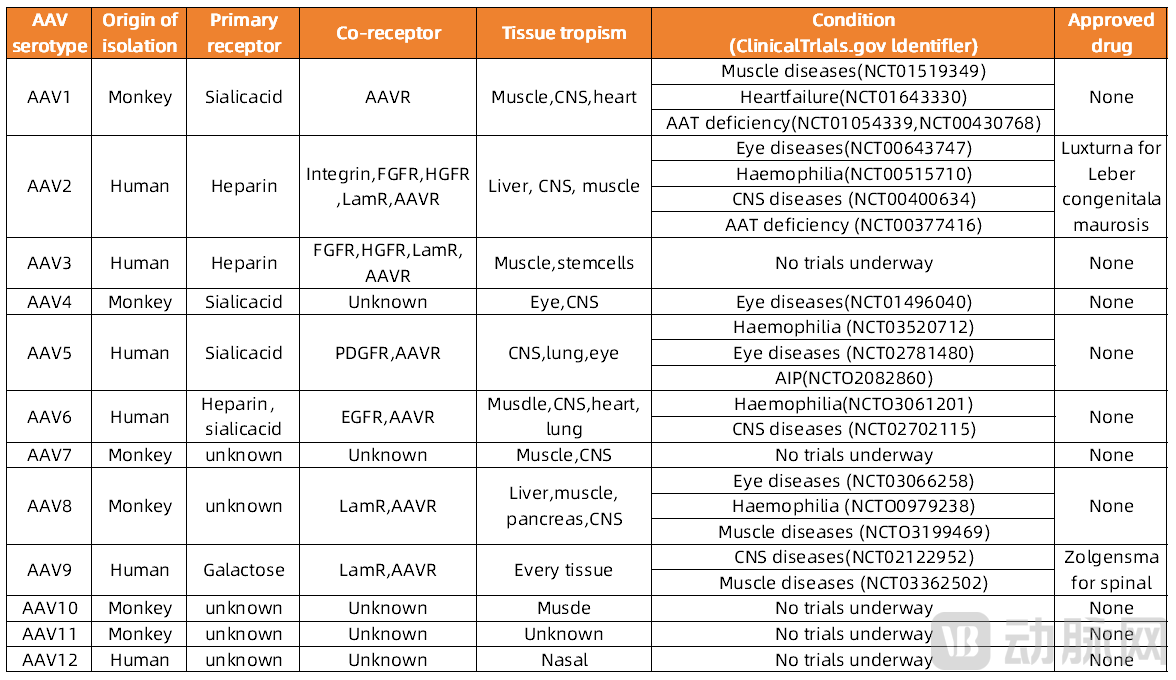

The process of AAV entry into cells depends on the recognition of AAV capsid proteins by cell-surface glycosylated receptors; therefore, AAV capsid proteins determine its tissue-targeting specificity.Precise delivery to different tissues and organs can be achieved by selecting appropriate AAV vector serotypes.New AAV serotypes with novel tissue tropism can be generated by modifying or mutating the AAV capsid protein sequences.

Tissue Tropism of Different AAV Serotypes and Their Clinical Applications

Data source: Public literature; chart by VCBeat.

Current optimization technologies for AAV vectors are primarily focused on the capsid and immunogenicity,AsCross-species Screening or DesignAAV capsids with robust delivery capabilities to enable lower AAV vector doses, leveraging existing knowledge of capsid biology and host cell targetsRationally design capsids to specifically recognize tissue-specific or cell-specific extracellular markers or evade immune surveillance, reducing the immunogenicity of AAV vectors, andReduce patients' immune response after administrationetc.

NowadaysThe focus of industry development has shifted to third-generation AAV capsids., such as Dyno (CapsidMap platform), 4DMT (Therapeutic Vector Evolution platform), and StrideBio (structure-inspired AAV capsid engineering, STRIVE platform), have all engaged in collaborations related to targets for next-generation AAV capsid platforms.

Computational algorithms enable the design of AAV capsid structures that do not exist in nature, without requiring a comprehensive understanding of the underlying biological principles of AAV capsids.For instance, DynoTherapeutics’ AI-driven CapsidMap™ platform leverages in vivo experimental data and machine learning to design and create novel AAV capsids with enhanced tissue targeting and immune evasion capabilities. These capsids enable simultaneous delivery across multiple organs, facilitating more effective systemic treatment for various diseases, while also offering improved gene packaging capacity and manufacturability. The scientific community is also working to develop AAV vectors with larger gene cargo capacities.

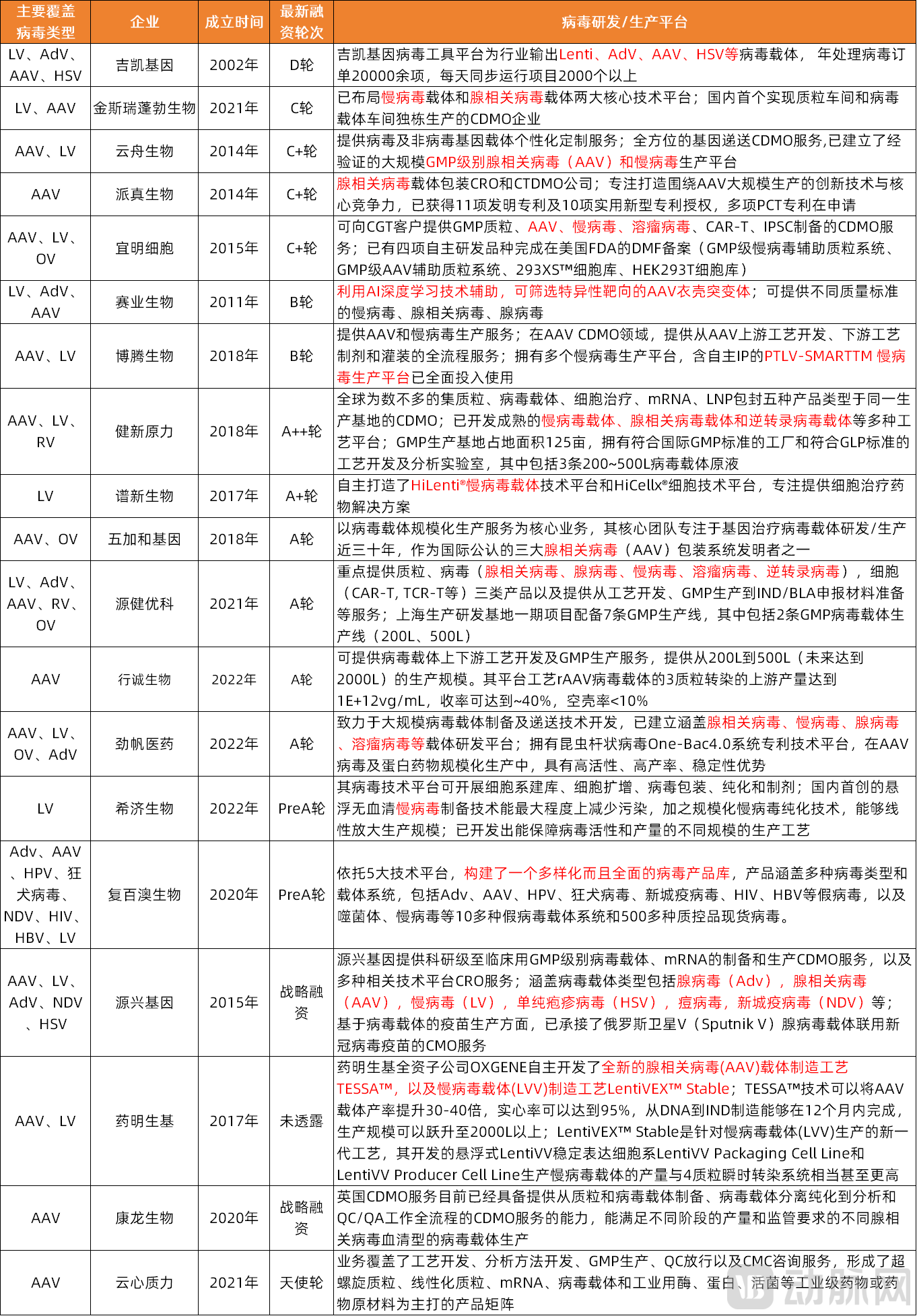

Among domestic gene therapy drug developers with proprietary, distinctive viral vector platforms, the majority have opted for the AAV technology route, which offers a higher safety profile.To enhance vector delivery efficiency, and to design or optimize the screening or directed evolution for target sites and tissue tropism, we conduct vector screening, design, and optimization to address the existing limitations of AAV.

Chinese Startups with Independently Developed Viral Vectors

Source: Official websites of respective companies and public reports; compiled and charted by VBInsight and VCBeat.

AlsoA Few Enterprises Lead the Frontier of Innovation, such as Bendao Gene, which has developed a vector that lies between viral and non-viral vectorsVirus-like vectors(virus-like particle, VLP) delivery technology. These virus-like particles can be degraded within a short period after fulfilling their function, unlike DNA delivery, where prolonged persistence increases the risk of off-target effects.

The AAV vector development capabilities of certain enterprises have gained recognition from multinational corporations (MNCs),Kerui Gene has currently entered into a development collaboration with Boehringer Ingelheim (BI) on delivery vectors for gene therapies targeting liver diseases.

High barriers and stringent requirements for viral vector production lead many CGT companies to adopt outsourcing.The R&D and manufacturing of viral vectors have consistently attracted significant attention from the capital market, accounting for a relatively high proportion of investment and financing within the overall cell and gene therapy (CGT) CDMO sector in recent years. For instance, in 2022, the total investment and financing amount in China’s viral vector production sector reached24.38100 million yuan, accounting for of the total investment and financing amount (RMB 2.747 billion) in the CGT CDMO sector in the same year88.77%。

Amid a challenging overall financing environment,In 2023, 15 companies in China’s virus production sector secured a total of RMB 3.01 billion in financing, surpassing the overall funding level of 2022. New entrants continue to emerge and establish their presence in this field.

Startups in China with Layouts in Viral Vector R&D/Production

Sources: Company websites and public reports; VBInsight and VCBeat Research compiled and charted.

Commonly Used Nucleic Acid Nanocarriers

The ultimate clinical translation and commercialization of nucleic acid therapeutics rely critically on advances in chemical modification technologies, including GalNAc conjugation, and the development of nanoscale nucleic acid delivery vectors, such as lipid nanoparticles (LNPs).Although viral vectors have been explored in the field of nucleic acid therapeutics, non-viral vectors remain the primary focus of development due to considerations such as safety and the need for repeated dosing.

The success of mRNA COVID-19 vaccines has propelled lipid nanoparticle (LNP) delivery systems into the spotlight, butDue to factors such as the LNP patent barriers faced both domestically and internationally, the field of potential nucleic acid nanocarriers beyond LNPs has also garnered significant industry attention.

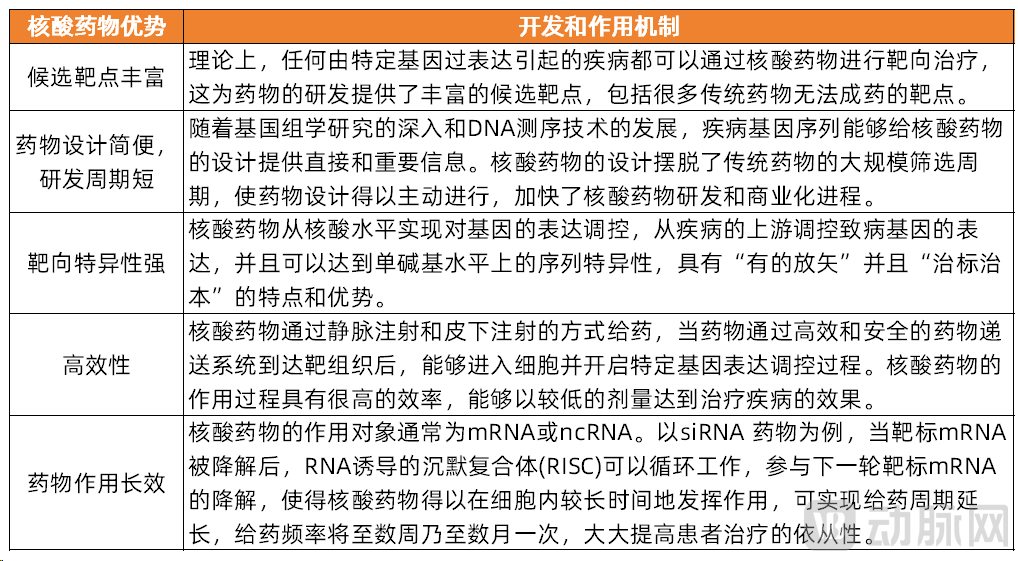

Advantages and Characteristics of Nucleic Acid Drugs and Their Mechanisms of Action in Development

Source: Public information; Chart by VCBeat.

5Lipid Nanoparticles: Innovations Break Through Patent Barriers and Extrahepatic Delivery Bottlenecks, Attracting Nearly RMB 13 Billion in the Past Three Years

As the most widely used nucleic acid nanocarrier currently, LNP has its unique advantages. Compared to viral vectors,LNP-mediated delivery of gene-editing therapeutics enables transient expression, thereby minimizing the risk of off-target editing. Furthermore, LNPs exhibit significantly lower immunogenicity than viral vectors, allowing for repeated dosing in certain cases and demonstrating favorable safety and biocompatibility profiles. In contrast to the complex manufacturing processes associated with viral vectors, LNP production benefits from mature large-scale manufacturing technologies, laying the foundation for clinical trials of gene therapies delivered via LNPs.Compared with traditional liposomes,LNPs exhibit superior kinetic stability and a more rigid morphology.

Patent barriers have become the primary bottleneck for domestic nucleic acid drug companies in applying LNP technology.Arbutus is a global leader in the lipid nanoparticle (LNP) field, with comprehensive patent coverage for its LNP technology. Its intellectual property protection remains robust and difficult to challenge until the patents expire in 2030. The three major mRNA companies—Moderna, BioNTech, and CureVac—have all sought LNP patent licenses from Arbutus, yet patent disputes over the use of LNP technology persist.

If Chinese manufacturers wish to use commercialized LNPs, they can either obtain licensing from Arbutus or focus on developing proprietary LNP structures to establish their own patent barriers.If companies are unwilling to incur substantial costs to obtain licensing yet wish to utilize existing LNP platform technologies, they must circumvent patent barriers by modifying the specific structures of cationic lipids covered in the patents or adjusting the ratios of various lipids.

Synthesizing a series of molecules with structures similar to the cationic lipids in existing patents has become the primary choice for most companies to circumvent patent barriers.Modifying lipid ratios is challenging, as the proportions protected by existing patents cover a broad range; deviating entirely from this range would inevitably compromise safety and efficacy. Given the substantial time and financial investment required to discover novel ionizable lipids and scale up their production, synthesizing a series of molecules with structures similar to the cationic lipids covered by existing patents has become the primary strategy for most companies to circumvent patent barriers. This approach currently represents the main innovation pathway for numerous domestic enterprises developing LNP technology.

In addition to the technical application challenges at the industry level, LNP technology itself also faces certain limitations, especiallyLiver Targeting. Due to the cytotoxicity of cationic liposomes and their tendency to accumulate in the liver, there are significant restrictions on dosage, making repeated administration difficult. Additionally, issues such as the need for improved delivery efficiency and short duration of action persist. To overcome this major application bottleneck—the limited organ targeting capability of LNPs—many companies in the industry are racing to develop novel LNP delivery systems capable of targeting non-hepatic tissues.

Therefore, most companies in China applying LNP delivery technologyOn one hand, innovative design of cationic lipid analogs or adjustment of the ratios of different lipids in LNPs is being pursued to circumvent patent barriers; on the other hand, efforts are focused on overcoming the current limitations of LNPs to enhance delivery efficiency, reduce toxicity, and develop LNPs capable of targeting extrahepatic tissues.VCBeat has conducted a comprehensive review of domestic startups with independently developed LNP technology platforms.

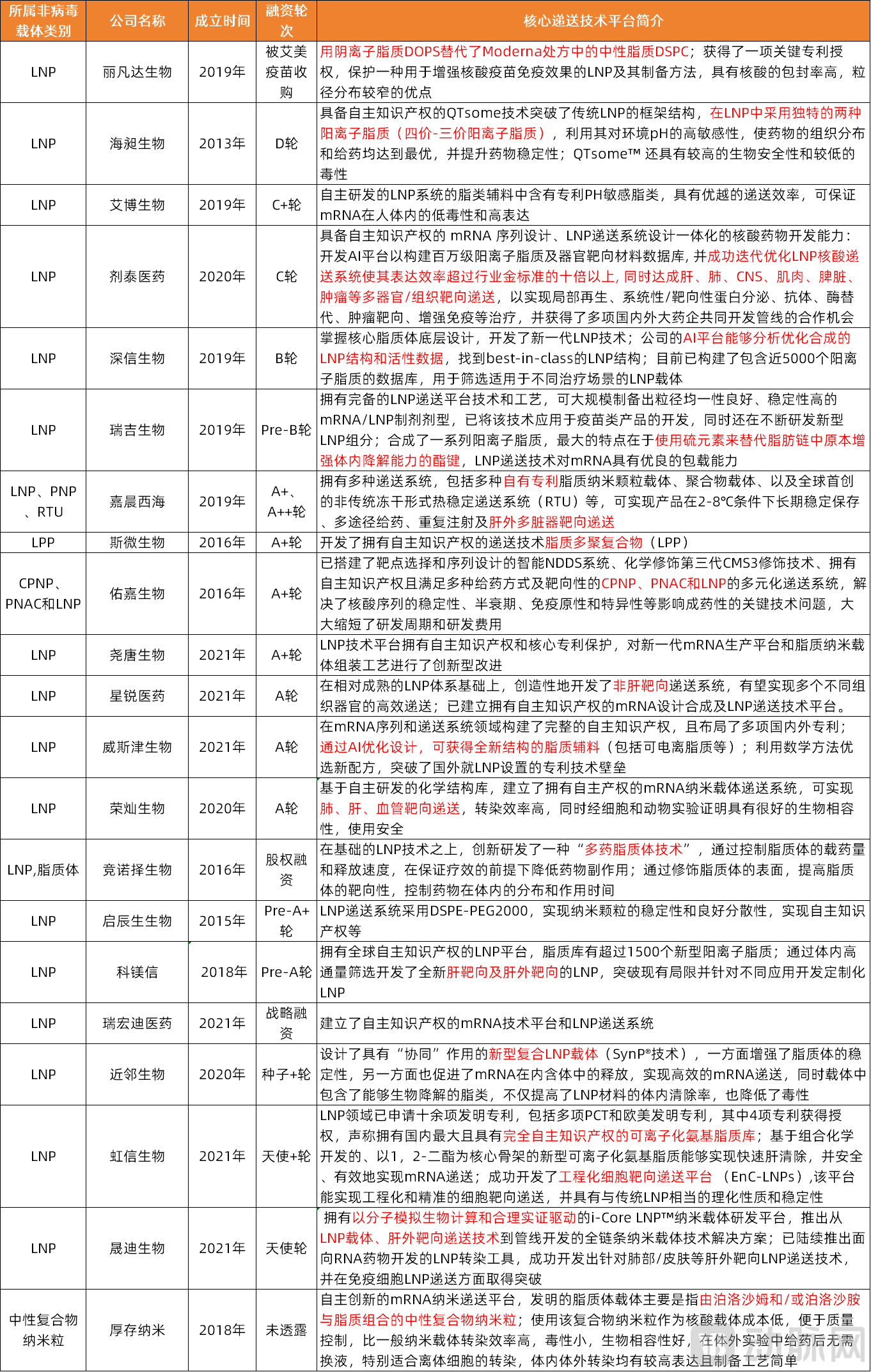

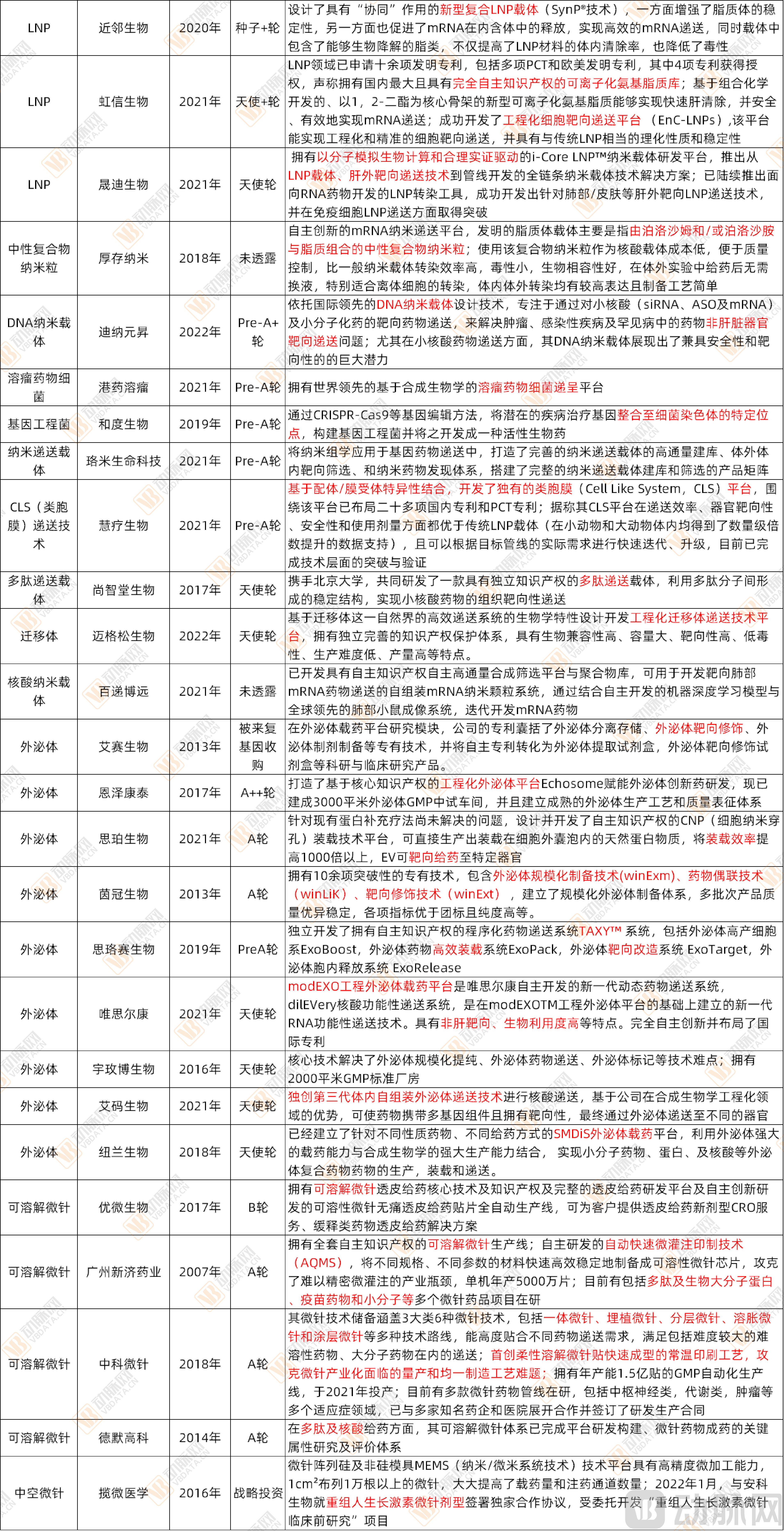

Domestic Startups with Proprietary LNP Technology Platforms and Their Innovations

Source: Company websites and public reports; compiled and charted by VCBeat.

Certain companies with distinctive features and excellent performance in the development of LNP delivery systems deserve attention.such as Abogen Biosciences, Rongcan Biotech, and Jinlin Biotech. There are also other companiesMore Boldly Innovative Designs Based on Existing LNP Structures, such as Haichang Bio (whose QTsome™ technology has broken through the structural framework of traditional LNPs).

Furthermore,Of particular note is the significant role and development potential of AI in the design and development of lipid nanoparticles (LNPs).Several Chinese startups excelling in the development of LNP delivery systems, such as Shenshen Biology, Metagenomi (Jitai Medicine), and WisGene Bio, have all leveraged AI technology to optimize the design of LNPs.

Dr. Lai Caida, Co-founder and CEO of Metagenomi, pointed out that AI-driven development of drugs and delivery systems features high predictability, high efficiency, rapid iteration, and strong scalability.By integrating AI algorithms with high-throughput iterative cycles of dry and wet lab experiments, the design space for delivery chemistry can be effectively expanded by several orders of magnitude, thereby pushing beyond the boundaries of current industry knowledge. This approach enables algorithms to design innovative delivery systems and makes the experimental development process more targeted and predictive. Compared with traditional methods, the design efficiency of delivery systems has increased by nearly 100-fold.

Faced with the patent barriers of LNPs and the challenge of liver targeting, some domestic companies opting for non-viral vectors have offered alternative solutions for the delivery of nucleic acid drugs and other categories of gene therapy.Developed a unique delivery technology.such as Huiliao Biotech (its proprietary cell-membrane-like platform) and Maigesong Biotech (its unique engineered migrasome delivery technology platform).

Domestic Startups and Technical Pathways for Non-Viral Vector Gene Drug Delivery Beyond LNPs

Source: Official company websites and public reports; compiled and charted by VCBeat.

In addition to LNPs, the currently mainstream nucleic acid nanocarriers also includePolymer Nanoparticles(PNP) andInorganic Nanoparticles(INP), etc. Although their use is still in the clinical validation process, they hold significant development potential. The report also provides a detailed introduction and elaboration on these two types of nucleic acid nanocarriers; due to space limitations, further details are not expanded upon here.

Potential Frontier Drug Delivery Technologies

In addition to clinically validated delivery technologies such as conjugation, viral vectors, and nucleic acid nanocarriers, which are in high demand within the industry, emerging frontier delivery technologies still undergoing clinical validation—such as extracellular vesicles (EVs) and microneedle (MNs) delivery—are also garnering significant industrial attention.

6Exosome Delivery: The Ideal Delivery Vector, Drug Development Bottlenecks Await Breakthroughs, and Nucleic Acid Delivery Layout Is Heating Up

As natural endogenous transport carriers, exosomes possess multiple inherent advantages, primarily including:

1) Low toxicity, low immunogenicity, and high stability:Composed of natural human proteins and lipids, native exosomes exhibit negligible immunogenicity and toxicity; even engineered exosomes with modifications demonstrate minimal immunogenicity and toxicity. Therefore, exosome-based delivery can avoid the recognition and clearance by the immune system that often occurs when exogenous protein- or nucleic acid-based therapeutics enter the body. Due to their endogenous origin, exosomes possess high stability in vivo. Although similar to liposomes, exosomes feature higher membrane curvature and asymmetry, which have been shown to facilitate interactions with cell membranes.

2) Large spatial capacity, enabling the delivery of a wider variety of active ingredients:As natural carriers of intercellular communication, exosomes are enriched with diverse bioactive substances, including nucleic acids, proteins, and lipids. They possess a substantial loading capacity, can accommodate various drug molecular structures, exhibit distinct molecular transport characteristics, and demonstrate good biocompatibility, enabling the encapsulation of many different types of molecules and cargo.

3) Can circulate to all body compartments, possesses favorable tissue selectivity, and enables targeted delivery:Exosomes secreted by different tissues exhibit a natural, homing-like tropism toward their tissue of origin. Leveraging this intrinsic property, exosomes derived from specific tissues can serve as carriers with natural targeting capabilities for those same tissues. For instance, exosomes derived from the central nervous system (CNS) can cross the blood-brain barrier (BBB). This characteristic can be exploited to overcome the limitation of conventional drugs in penetrating the BBB, thereby facilitating the development of therapeutics for brain disorders. Furthermore, the abundant protein components on the exosome surface confer excellent target cell recognition capabilities. By modifying surface molecules to endow exosomes with specific cellular and tissue targeting specificity, it is possible to deliver cargo—such as proteins, RNA, or small-molecule agents—encapsulated within exosomes to specific pathological tissues and organs.

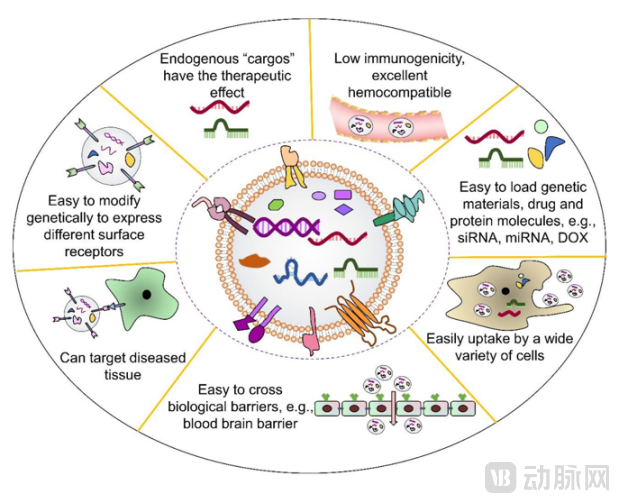

Advantages of Exosomes as a Novel Drug Delivery Carrier

Data Source: Public Information

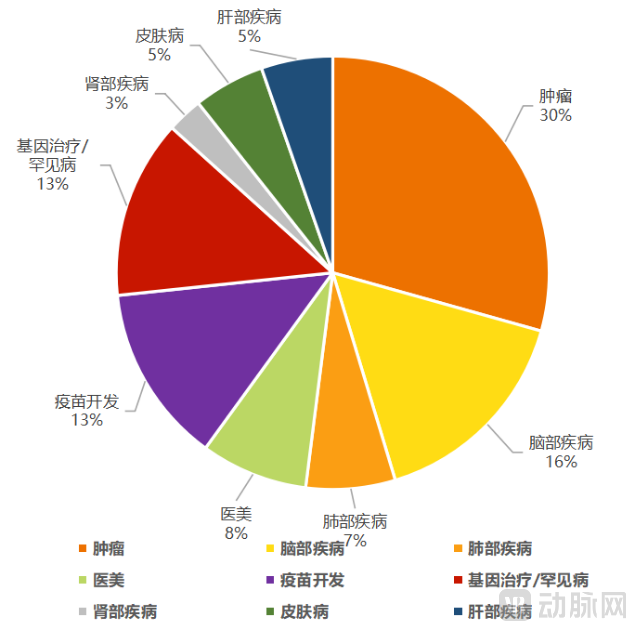

Due to their significant delivery advantages, exosomes are currently being extensively studied as a popular drug delivery system for therapeutic applications.Drug and Vaccine Development for Cancer, Brain Disorders, and Genetic DiseasesIn China.

Major Disease Areas Targeted by Nearly 50 Exosome Companies Worldwide

Data Source: VCBeat, VCBeat Research Institute

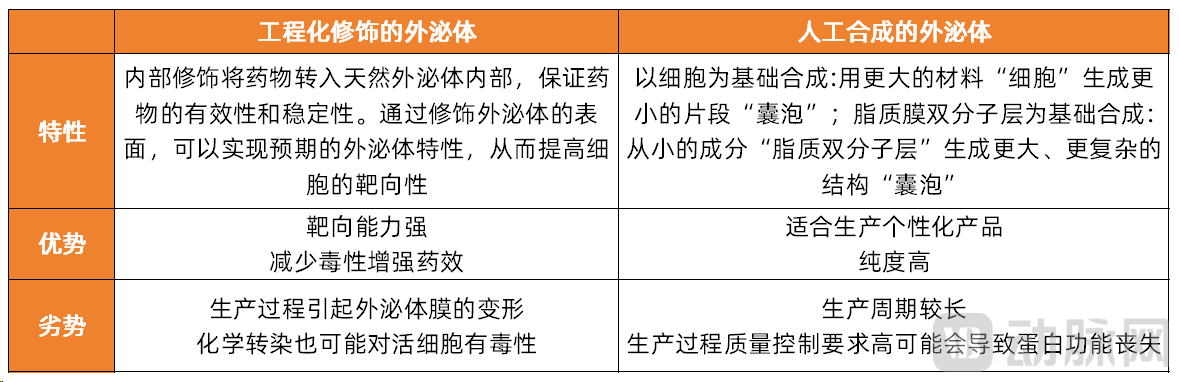

Exosomes in Various Forms for Drug Delivery Have Been Developed Based on Different Drug-Loading Methods and Design Pathways, mainly including two categories: engineered exosomes and synthetic exosomes.

Two Common Types of Exosomes Currently Used in Drug Delivery and Their Corresponding Characteristics

Source: Compiled from public data; chart by VCBeat.

Although exosomes offer numerous advantages in the field of drug delivery, no therapies utilizing exosomes as a delivery system have been approved for market launch to date. This is because the clinical translation of exosomes still faces many challenges, among whichThe major factors limiting the clinical application of exosomes include the technical challenges in isolation and purification, difficulties in achieving scalable manufacturing, and the lack of standardized production and quality control protocols.Other issues pending optimization and improvement includeTargeted Delivery, Drug Loading Efficiency, and Effective Drug Release of Exosomesetc.

In response to the current limitations in exosome development, companies both domestically and internationally have made significant efforts, with some achieving notable exploratory results. For instance, leading enterprises in the field of exosome-based therapeuticsCodiak has resolved the challenges associated with exosome isolation, purification, and production scale-up.(Its production system has been recognized by the FDA, and it has advanced three drugs to Phase I clinical trials),and identify high-secretion protein scaffolds(Extracellular PTGFRN and intracellular BASP1)Drug loading was performed, demonstrating the efficacy of exosome delivery.

ButAlternatively, this may be because the exosome industry remains in its early stages of research and development, presenting numerous unpredictable risks and challenges, as well as due to the company’s own strategic missteps in management and pipeline project initiation., In March 2023, Codiak filed for bankruptcy, with only its exo-STAT6 pipeline retained to continue advancing into Phase I clinical trials.

The domestic and international exosome industry is still in its early stages of development. However, some notable startups are making significant headway in the exploration of exosome-based drug delivery, including Siluocai Biotech, Enze Kangtai, Weisierkang, and Yinguan Biotech.

Startups in China with Independently Developed Intellectual Property Rights for Exosome Drug-Loading Technology Platforms and Their Technical Features

Source: Company websites and public reports, VBInsight; compiled and charted by VCBeat.

Currently, given the promising Phase 1 clinical data from Codiak’s exo-STAT6 pipeline, most domestic companies developing exosome-based drug delivery systems alsoRapidly expanding their presence in the field of exosome-based delivery for nucleic acid therapeutics,such as Viscocon and iMab Biopharma.

7Microneedle Delivery: Heated Exploration in Vaccines and Chronic Diseases Holds Great Potential, with Dissolvable Microneedles Being Promising

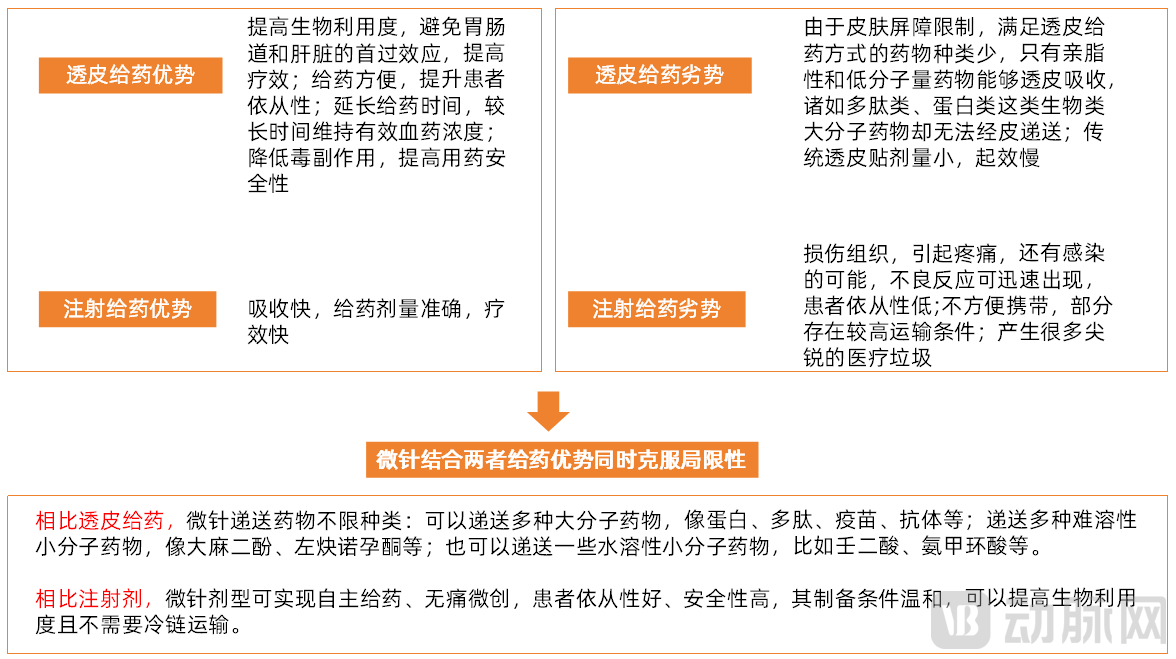

Microneedle delivery combines the dual advantages of transdermal and injectable drug administration while overcoming the limitations of both.It features painless minimally invasive administration, safety and convenience, avoidance of the first-pass effect, significant reduction in dosage, and decreased drug-related toxic side effects.

Microneedle Delivery Combines the Dual Advantages of Transdermal and Injectable Administration While Overcoming the Limitations of Both

Data source: public information, research interviews; chart by VCBeat.

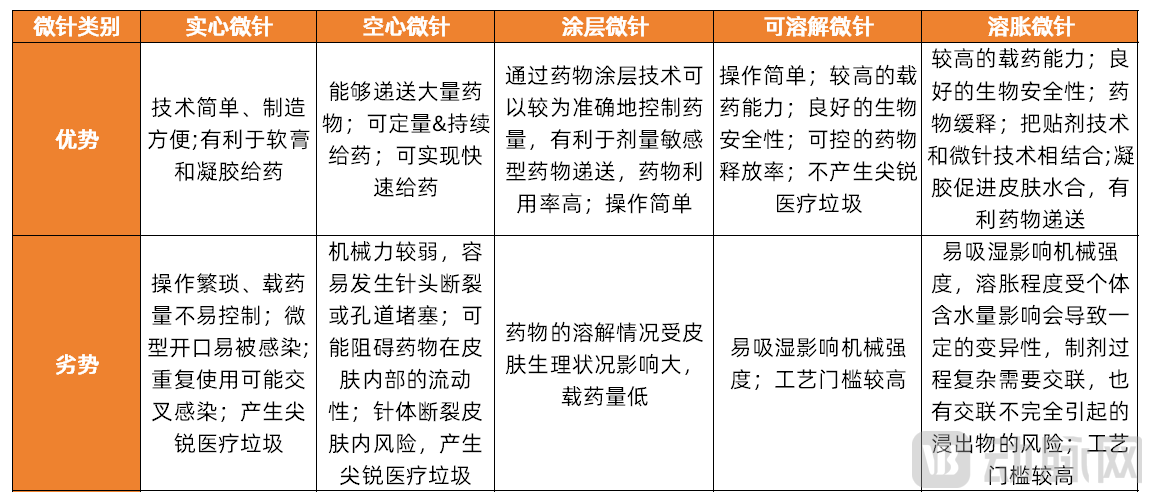

Based on the principles of drug release within the skin and their constituent materials, microneedles can be classified into five types: solid microneedles, coated microneedles, dissolving microneedles, hollow microneedles, and swelling microneedles.Different types of microneedles offer distinct functions and respective advantages,This section is elaborated in detail in the report; due to space constraints, it will not be further expanded here.

A Comparative Analysis of the Advantages and Disadvantages of Various Microneedles

Data sources: Public information, research interviews; chart by VCBeat

In terms of technological maturity, solid and hollow microneedles are more established, having been developed earlier, while emerging technologies such as dissolving microneedles are advancing rapidly and hold significant potential.

Solid Microneedles, Hollow MicroneedlesIt has been developed earlier, with the most related clinical studies conducted, and products have already been launched on the market.

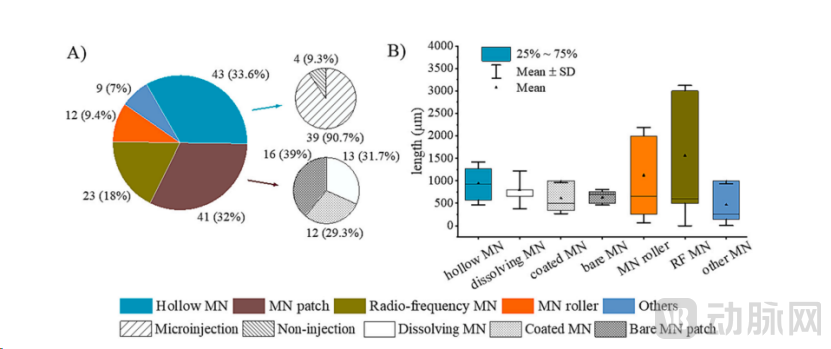

In terms of clinical research, according to relevant literature statistics, there are currently 43 clinical trials related to hollow microneedles, accounting for 33.6% of the total number of microneedle clinical trials. The number of clinical trials related to microneedle array patches (including solid microneedles, dissolving microneedles, and coated microneedles) is 41, among which 16 involve solid microneedles, accounting for 39% of the clinical trials related to microneedle patches. The number of clinical trials currently conducted for dissolving microneedles and coated microneedles is similar, with 13 and 12 trials, respectively.

Types of Microneedles Used in Clinical Trials

Data source: Zhang J, et al. J Control Release, 2023.

On the commercialization front,Approved microneedle products on the market include MicronJet 600 single-crystal silicon microneedles and the hollow microneedle-based influenza vaccine Fluzone® Intradermal (which had limited sales and was discontinued in 2016). Currently, there are no drug-loaded microneedle products commercially available in the mainstream market.

An examination of the current global landscape in the development of clinical indications for various microneedle-based drugs reveals that, as "micro-injectors,"Hollow microneedles have a wide range of clinical indications,From various vaccines to indications including anesthesia, tuberculosis, and ocular diseases.Coated microneedles have relatively limited potential for conducting related product clinical trials due to their low drug-loading capacity.Its clinical applications are primarily focused on peptides, zolmitriptan, and antibiotics.

Current Global Development of Clinical Indications Targeted by Various Microneedle Drug Delivery Systems

Data source: Zhang J, et al. J Control Release, 2023.

Dissolvable microneedles, as an emerging microneedle technology, are demonstrating a significantly faster growth momentum.Dissolvable microneedles emerged later than solid and hollow microneedles but have demonstrated a faster growth trajectory. Currently, the number of clinical trials involving dissolvable microneedles (14) has already surpassed that of solid microneedles (13), with a broader range of drug indications being explored in clinical settings.

Lu Di, Dean of the Institute of Microneedle Drug Research at Zhongke Micro-Needle, pointed out that dissolving microneedles, as an innovative formulation, have a wide range of developmental possibilities. Essentially, any indication treatable with coated microneedles can be addressed using dissolving microneedles instead. By adjusting the formulation of dissolving microneedles, the delivery of various types of drugs can be achieved.

Currently, the dissolvable microneedle influenza vaccine developed by Micron Biomedical has entered clinical trials.2In Phase I studies, its dissolvable microneedle measles vaccine has also entered clinical trials, making it the company with the most advanced progress in the international development of dissolvable microneedle drugs.

In China, the development of microneedles in medical aesthetics has taken the lead. As some companies break through the bottlenecks in the industrialization of microneedle drugs, they are beginning to venture into the field of serious medical applications, such as drug-loaded microneedles.In 2015, Europe and the United States began applying microneedles to the field of drug delivery, while Japan and South Korea focused predominantly on developing microneedle technology for medical aesthetics. China’s microneedle industry started later; its early development mirrored that of the Japanese and South Korean markets, with medical aesthetics leading the way. However, in the past two years, as industrialization technologies for microneedles have further matured, select companies have broken through bottlenecks in the mass production of microneedle-based drugs, gradually shifting their research focus toward the more promising field of drug delivery.

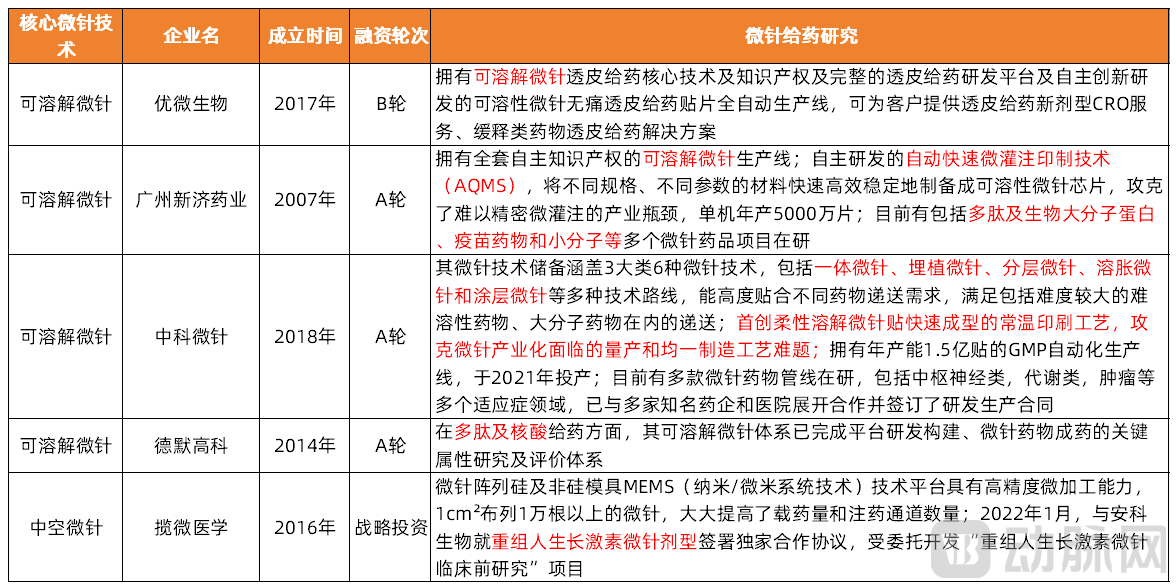

Microneedle companies, including Zhongke Microneedle and U-Microbe, have gradually overcome industrialization bottlenecks by accumulating experience in the mass production of medical aesthetic microneedle products, and are successively expanding into the field of microneedle-based drug delivery.

Startups in China Focused on Microneedle Drug Delivery

Data sources: Official websites of respective companies and public reports; chart compiled by VCBeat.

Among them,Zhongke MicroneedleThe medical aesthetics microneedle business achieved a breakthrough in industrialization as a pioneer, introducing the industry’s first room-temperature printing process for the rapid formation of flexible dissolving microneedle patches. It has gradually overcome challenges in mass production and manufacturing consistency of microneedles, and operates a GMP-compliant automated production line with an annual capacity of 150 million patches, which commenced operations in 2021. Currently, the company has multiple microneedle-based drug pipelines under development, covering various therapeutic areas including central nervous system disorders, metabolic diseases, and oncology. It has established collaborations with several renowned pharmaceutical companies and hospitals, signing research, development, and manufacturing contracts.

The mature experience and production capacity advantages previously accumulated in the development of dissolvable microneedle products for medical aesthetics will serve as a crucial foundation for domestic dissolvable microneedle companies to expand into the drug delivery sector.Lu Di, Dean of the Chinese Academy of Microneedle Drug Research, pointed out that although Europe and the United States started earlier in the research of microneedle drug delivery, Chinese microneedle pharmaceutical companies have the potential to achieve overtaking on a bend in the development of dissolvable microneedle drugs. The reason is that the production processes and steps for both medical aesthetic microneedles and microneedle drugs are actually similar, and China’s progress in the industrialization of dissolvable microneedle technology is no less than that of foreign countries. Currently, it is an excellent time to lay out microneedle drugs, with the opportunity to achieve head-to-head competition between China and the United States in this niche sector of the pharmaceutical industry.

Based on the characteristics of microneedle drug delivery, currently under developmentMicroneedle Vaccines and Exploring Microneedle Drug Delivery in the Field of Chronic DiseasesPossesses significant market potential.

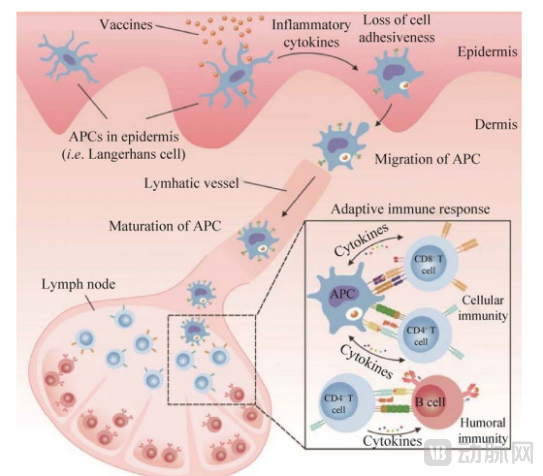

Basic Process of Transcutaneous Immunization

Image source: Public information

BecauseMicroneedle VaccineIt avoids the first-pass effect, is effective, convenient, and minimally invasive, while reducing pain for vaccine recipients and improving compliance. It also alleviates the workload of healthcare workers and offers advantages such as reduced dosage requirements, lower production costs, improved vaccine stability, and a simplified supply chain. This approach holds significant potential for addressing challenges such as the mismatch between high vaccine demand and limited production capacity in some developing countries, as well as the stringent cold-chain requirements during vaccine transportation.

For patients requiring long-term, high-frequency drug administrationChronic Disease Sector, microneedles are also a particularly promising drug delivery method. Currently, microneedle companies including Zhongke Microneedle and Demer High-Tech are allGLP-1 DrugsHas established a presence in the microneedle field.

Currently, several companies in the field of dissolvable microneedle drug delivery, including Zhongke Microneedles, have overcome industrial bottlenecks related to mass production and the development of uniform, stable manufacturing processes. These enterprises are also actively collaborating with relevant authorities to advance the establishment of standards for microneedle-based drug registration, evaluation, and approval. Given the promising prospects of microneedles in vaccine development and chronic disease management, and as domestic understanding, technology, and policy frameworks continue to mature and improve, the development of China’s microneedle industry holds significant promise.

Bucking the Trend Amidst the Capital Winter: Advances in Biology and Detection Technologies as the Key Turning Point

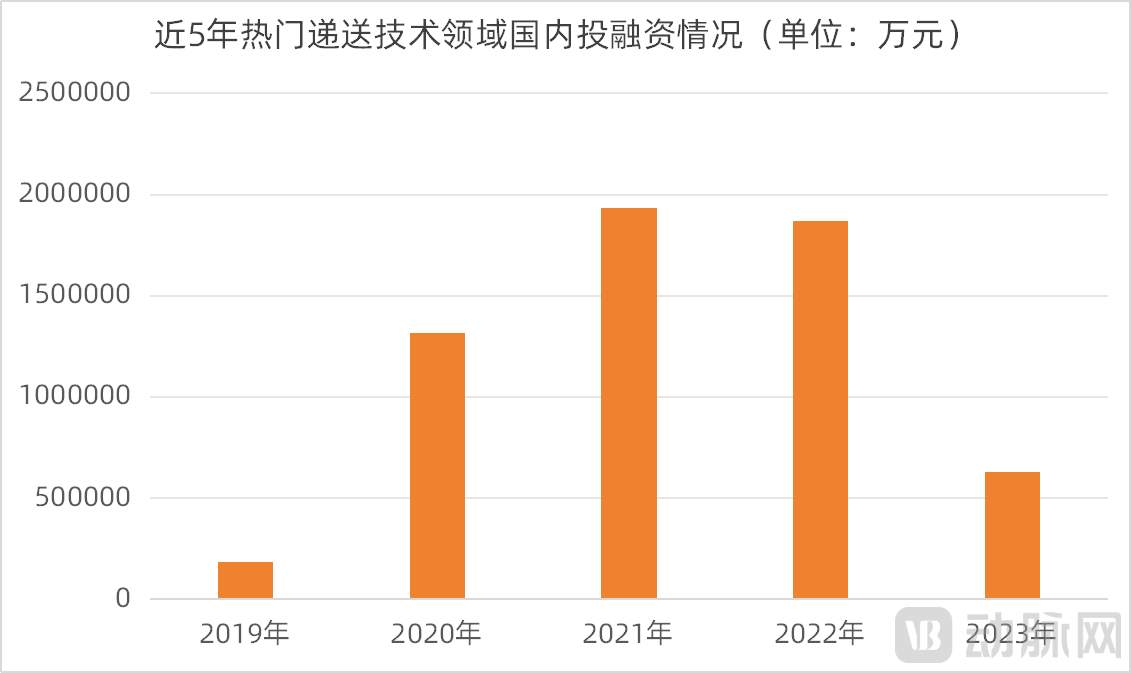

Domestic Investment and Financing Trends in Popular Drug Delivery Technology Fields Over the Past Five Years

Data Source: VBInsight; Chart by VCBeat.

Even during the broader downturn in the biopharmaceutical industry, drug delivery remains a focal point of capital market attention.From 2019 to 2022, capital market attention toward drug delivery continued to rise.Even in 2021 and 2022, when the capital winter had already set in, the rapid growth did not slow down. In 2021 and 2022, the total investment and financing amounts in the hot field of drug delivery in China reached as high as RMB 19.34 billion and RMB 18.69 billion, respectively.In 2023, according to incomplete statistics from VCBeat, the total value of financing and investment transactions in China’s drug delivery sector reached RMB 6.3 billion. Although this figure represents a significant decline from the rapid growth seen in the previous two years, it remains remarkably resilient for the biopharmaceutical industry, which has long endured a capital winter.

Investors have pointed out the underlying reasons for this phenomenon,With the advancement of emerging fields such as nucleic acid therapeutics and gene therapy, delivery systems are playing an increasingly critical role in the drug development process. Once delivery challenges are resolved, novel technologies—including mRNA, siRNA, and CRISPR—exhibit strong druggability. Companies with a deep understanding of delivery technologies can rapidly identify promising opportunities for drug development. The carrier itself is no longer merely a delivery tool; it has the potential to catalyze the emergence of innovative therapies.

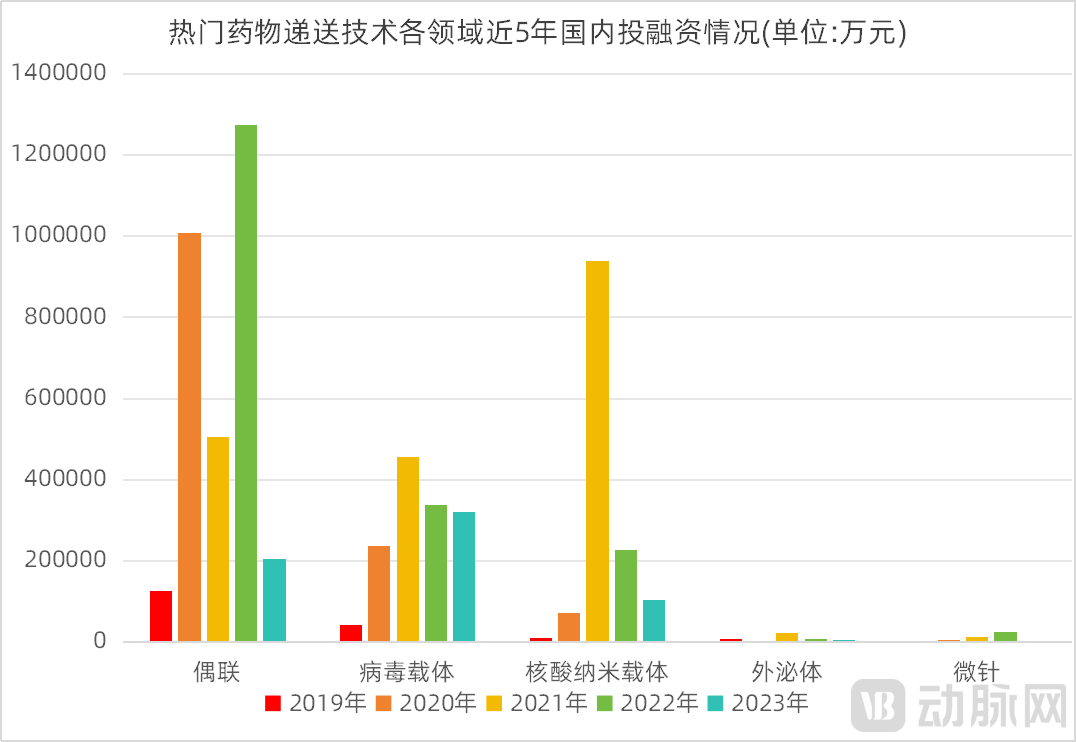

Investment and Financing Trends in China Over the Past Five Years Across Various Fields of Popular Drug Delivery Technologies

Data Source: VBInsight; Chart by VCBeat

VCBeat Research Institute onPast 5 YearsAn analysis of investment and financing data across various popular delivery technologies reveals that conjugation-based approaches have attracted the highest level of capital interest, followed byOver the past three years, the conjugation sector has attracted the highest volume of financing, totaling RMB 19.85 billion, followed by nucleic acid nanocarriers, which have raised RMB 13 billion in the same period.

While conjugation technology has reached a relatively mature stage of development, industrial enthusiasm remains high due to its vast potential for future applications.

Although conjugation technologies, represented by antibody-drug conjugates (ADCs), have reached a relatively mature stage of development, they continue to attract significant industry interest due to the substantial room for innovation. Investors have pointed out that while numerous ADC products have already received marketing approval—making ADCs the most mature among all currently popular drug delivery technologies—the future development potential of ADC therapeutics remains considerable.

On the one hand,Different combinations of antibodies, linkers, and small-molecule toxins all affect the clinical efficacy of ADC drugs.Even for ADCs targeting the same antigen, there is substantial room for improvement through optimizations in the antibody, payload, and conjugation strategy.

On the other hand, the technical approach of combining low-to-moderate toxicity compounds with high drug-to-antibody ratio (DAR) values has injected new vitality and greater potential into global ADC drug development.In recent years, Enhertu, developed by Daiichi Sankyo, and Trodelvy, developed by Immunomedics, have provided new insights into ADC drug design. The key distinction between these two products and previous ADC designs lies in their use of compounds with low to moderate toxicity. In contrast, traditional ADC drugs have predominantly relied on highly toxic compounds, a strategy that has resulted in numerous failures.

Industry investors have pointed out that while scientists initially lacked robust strategies for the research and development of antibody-drug conjugates (ADCs), they have gradually mastered the intricacies of the field. This progress has enabled the batch development of high-quality ADC products and the gradual formation of sound design strategies and conceptual frameworks for ADC drugs.

Other emerging conjugation technologies, such as PDCs and RDCs, are also unleashing significant development potential.“The concept of ‘everything can be conjugated’ has directly ignited strong market enthusiasm for conjugation technology.”

Since the outbreak of the COVID-19 pandemic, nucleic acid nanocarriers, represented by lipid nanoparticles (LNPs), have been gaining significant traction in the industry.

Regarding why nucleic acid nanocarriers have garnered such significant attention from the industry, industry experts point out that this is primarily driven by the development of mRNA vaccines during the COVID-19 pandemic.The safety and efficacy of LNPs as novel delivery vectors have been extensively validated.Furthermore,The rapid development of nucleic acid drugs and their heavy reliance on innovations in delivery systems for successful drug development constitute another major reason for the surge in interest in nucleic acid nanocarriers.

However, the currently most mainstream nucleic acid nanocarrier, LNP, still has limitations such as liver targeting, and there is considerable room for improving delivery performance and innovation, includingPNP、INPThe future development of other nucleic acid nanocarriers is also promising.

Various delivery technologies cannot be directly compared across the board; an optimal delivery method exists only in the context of specific application scenarios.

For example,Viral VectorIt features efficient cell membrane penetration, high transduction efficiency, specific cell targeting, long-term transgene expression, the capacity to carry large gene fragments, and natural immune evasion. However, it exhibits high immunogenicity, which hinders repeat dosing, and faces challenges such as sustained expression of gene-editing therapeutics, off-target gene editing, potential genomic integration, high manufacturing costs, and dose-limiting toxicity.

LNPThe safety and efficacy have been clinically validated, and issues related to large-scale production are gradually being resolved. However, challenges such as the limitations of organ targeting and restrictions on dosage due to the cytotoxicity of cationic liposomes—which preclude repeated administration—still require further research and innovation to address.

GalNacAlthough it demonstrates excellent delivery efficacy, its clinical scalability is limited by its liver-specific targeting and applicability only to small nucleic acid drugs;ExosomesandMicroneedleDespite its prominent delivery advantages, development has been relatively slow due to druggability bottlenecks encountered in manufacturing processes; it may take some time before its advantages in drug development can be fully realized.

Furthermore, some emerging delivery vectors such asVirus-like vectors, engineered bacteria, and intelligent delivery systems based on physiological signals or disease biomarkersThese are promising, but most are still in the early stages of development and require further clinical data for validation.

Advances in biology and detection technologies will profoundly influence the development of delivery technologies.Academician Chen Hongmin, Co-founder and Chief R&D Officer of Metagenomi Biopharma, pointed out that as a critical component of drug development, the ultimate goal of drug delivery is to provide patients with therapeutics offering superior efficacy. Therefore, the industry’s understanding and comprehension of disease mechanisms, disease targets, and target signaling pathways will profoundly influence the advancement of delivery technologies.

On the one hand, advances in biology enable the industry to gain a better understanding of disease mechanisms, therapeutic targets, and target signaling pathways; on the other hand, analytical techniques that further interpret various biological signals within the human body can deepen the industry’s understanding of biology.

The above is an excerpt of the main content of the report. To obtain the full report, please scan the QR code to add our assistant and initiate a conversation after adding.

Appendix 1: 105 Domestic Startups with Independent Intellectual Property Technology Platforms in Hot Delivery Fields and Their Technical Pathways

Appendix Table 2: Latest Financing Status of 103 Domestic Startups with Independent Intellectual Property Technology Platforms in Hot Delivery Fields

References

1、J Control Release. 2017 Sep 28;262:247-258.

2、BARIYA S HGOHEL M C,MEHTA T A et al.Microneedles: an emerging transdermal drug delivery system[J] .Pharm Pharmacol, 2012, 64(1): 11-29.

3、Sheng T, Luo BW, Zhang WT, et al. Microneedle-mediated vaccination: innovation and translation. Adv Drug Deliv Rev, 2021, 179: 113919. DOI:10.1016/j.addr.2021.113919

4、https://www.zjujournals.com/med/CN/10.3724/zdxbyxb-2023-0101

5、Springer AD, Dowdy SF. GalNAc-siRNA Conjugates:Leading the Way for Delivery of RNAi Therapeutics. Nucleic Acid Ther. 2018Jun;28(3):109-118.

6. [Industry In-Depth] The ADC Framework for Innovative Drug Research: A Review of Domestic ADC Technologies, Surpassing the Master

7. Dr. Xie Yuli: Drug Delivery—The “Chokehold” Technology for the Future of Biomedicine. PharmaEra

8. Drug Delivery - Basic Research on Viral Vector Drugs. Maibo Capital | PatSnap

9. Core Vectors for CGT: Research on Lentiviral Vector Series [1] Overview of Viral Vectors. Zhihu

10. [Industry Research] Nanoparticle Carriers—Another Option for Nucleic Acid Delivery. Asymchem

11. Roche, Takeda, and Eli Lilly Enter the Fray as Nearly 50 Companies Race Ahead: A Comprehensive Review of the Exosome Industry | VCBeat

12. “Small” Microneedles, “Big” Prospects: Novel Transdermal Drug Delivery Methods Are Igniting a New Track. VCBeat

Report Data Disclaimer

1. The data in this report is current as of the end of November 2023; any data released after that date is excluded from the statistical scope of this report;

2. All transaction amounts are converted into RMB, using a unified exchange rate standard: 1 USD = 7.14 RMB, 1 HKD = 0.91 RMB;

3. Transaction amounts in the millions, tens of millions, or hundreds of millions are uniformly categorized as 1 million, 10 million, or 100 million, respectively;

4. The data may be incomplete; corrections and feedback are welcome in case of any errors or omissions.

5. Editor Zhou Qiuhan also contributed to the organization of the report data.