Nearly $60 Billion and Over 3,000 Deals: The Hottest Transactions in a Cold Market – 2023 Global Healthcare Investment & Financing Analysis Report

In 2023, the winter chill in the global healthcare investment and financing market persisted, albeit with subtle shifts in its manifestations.

In this report, VCBeat has compiled and analyzed over 3,000 investment and financing transactions in the global healthcare sector in 2023. By integrating global investment and financing data from the past decade, the report provides a detailed characterization of the current landscape and subtle shifts in global medical innovation funding in 2023, examining dimensions such as sub-sectors, transaction size, frequency, funding rounds, investing institutions, and geographic regions.

We found that rather than being a continuation of the global capital winter in 2023, it more objectively served as a regular link in an upward trend within a longer historical cycle, and even more so as a new starting point for global medical innovation to enter deeper waters.

Core Viewpoints

1. In 2023, the global healthcare industry’s ability to attract capital further contracted, with total financing volume retreating to 2019 levels.

2. The focus remains on small- and medium-sized financing rounds with individual amounts below US$100 million, while the proportion of deals exceeding US$100 million has dropped to below 5%.

3. Over a longer horizon, market trading activity remains at historically high levels, driving average transaction sizes close to historic lows, as investment institutions favor an investment approach characterized by small, rapid steps.

4. The deep integration of information technology and biotechnology is driving mainstream venture capital in healthcare toward innovative biomedical projects.

5. Venture capital is also beginning to prioritize certainty, with innovative companies that strengthen their product lines through asset acquisitions and industry mergers and acquisitions being more favored by capital.

6. Healthcare IPOs Shrink Again; Some U.S. Biotech Innovators Turn to the Pink Sheets for Financing, Highlighting the Need for More Diversified Funding Channels

7. While many regions across China are intensifying efforts to cultivate the biopharmaceutical industry, the Yangtze River Delta still maintains a distinct locational advantage as the primary source of medical innovation in the country.

I. Overall Trend: Volume Increases While Prices Decline; Valuations for Innovative Projects Struggle to Grow, or Even Correct

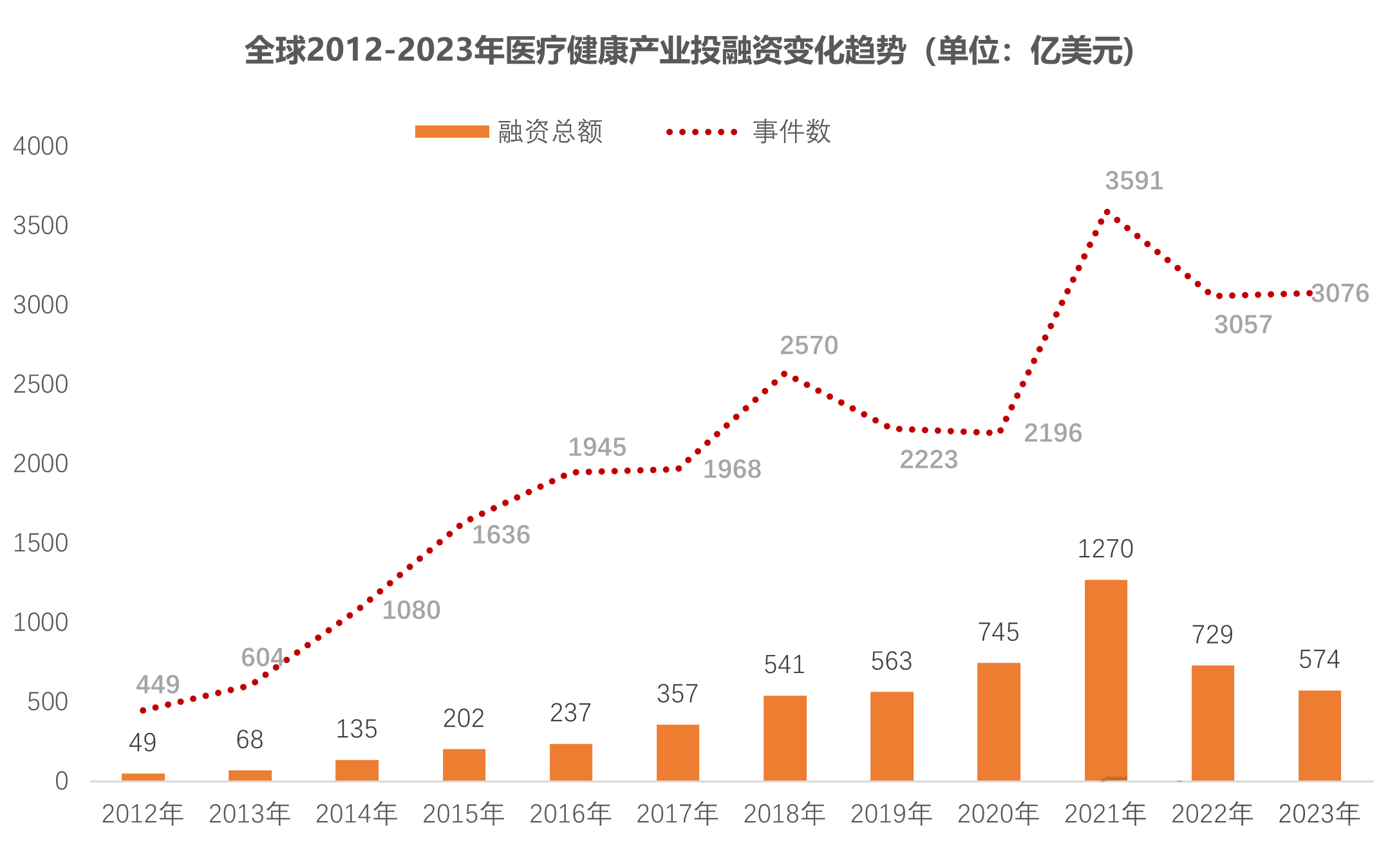

1. Global Healthcare Financing Drops to $57.4 Billion

Global Healthcare Investment and Financing Completes Its Third Year of Phased Downturn. In 2023, a total of 3,076 primary market investment deals were completed in the global healthcare sector, with cumulative financing reaching $57.4 billion. The total financing amount contracted by more than 20% compared to 2022. The capital winter of 2023 was undoubtedly colder than that of 2022.

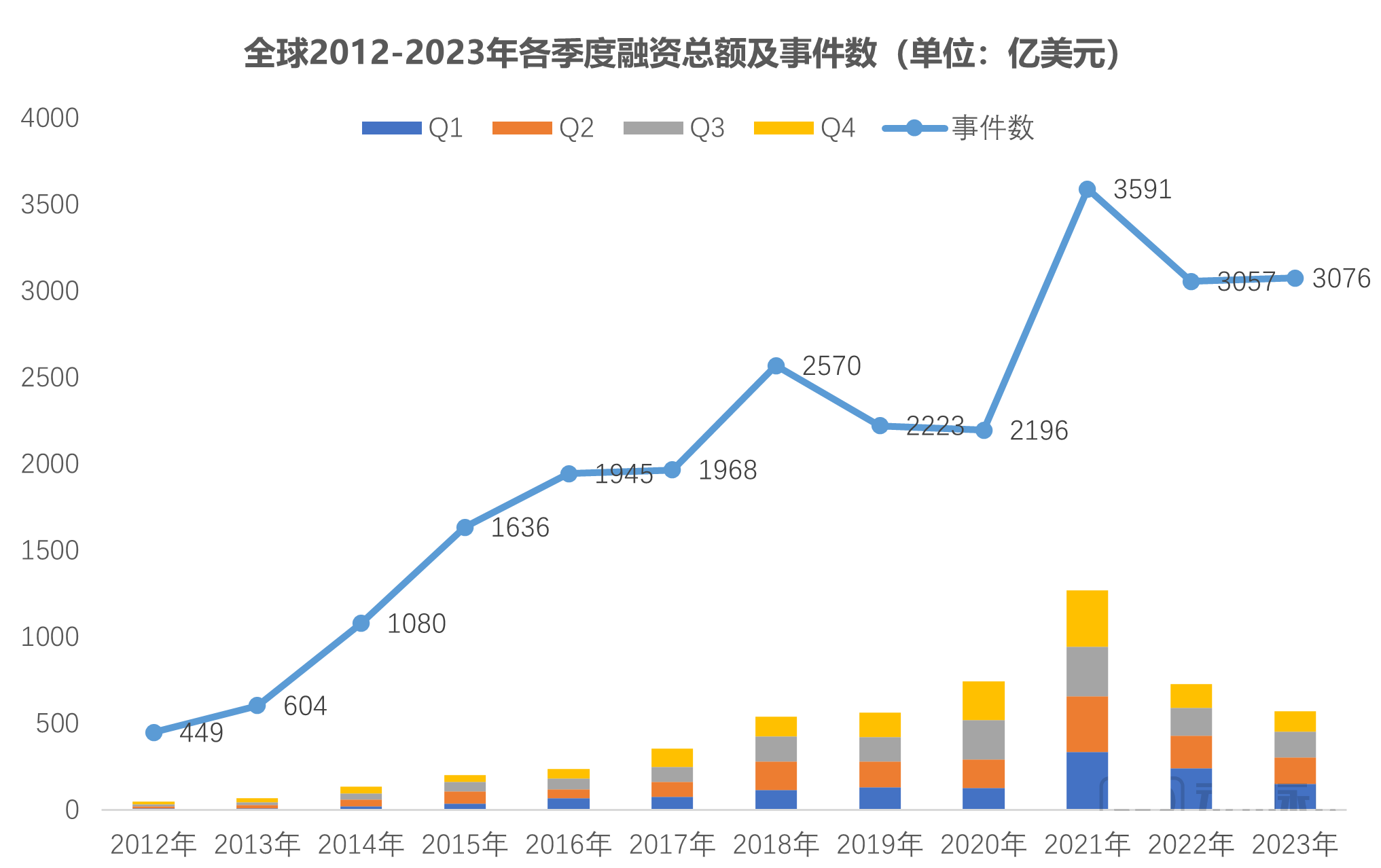

By quarter, the seasonal disparities in global healthcare investment and financing were further smoothed out in 2023. Since 2012, primary market investments and financings in the global healthcare sector have tended to be more concentrated in specific quarters. For instance, major events in industries such as biopharmaceuticals and medical devices are often clustered in the first and third quarters, coinciding with relatively more frequent primary market investment and financing activities in the global healthcare sector. However, by 2023, the correlation between these major events and financing transactions had weakened.

The likely reason behind this is that, amid the capital winter, investment firms have reduced their investments in unfamiliar projects encountered through industry events, shifting their focus instead to projects within their existing networks or making follow-on investments in their current portfolio companies.

Rapid growth interrupted.In the decade leading up to 2021, global primary market investment and financing in healthcare experienced a prolonged period of rapid growth, characterized by simultaneous increases in both deal volume and valuation. In 2021, global primary market investment and financing in healthcare reached a cyclical peak, with 3,591 deals completed and total capital raised amounting to $127 billion. Compared to 2012, when the sector was just gaining momentum, the total financing amount increased nearly 25-fold, while the number of financing transactions grew almost sevenfold. Although the $57.4 billion in global financing completed in 2023 remained at a relatively high level since 2012 and was significantly above the 10-year average of $45.583 billion, the industry expansion driven by disruptive innovations in healthcare has clearly lost momentum.

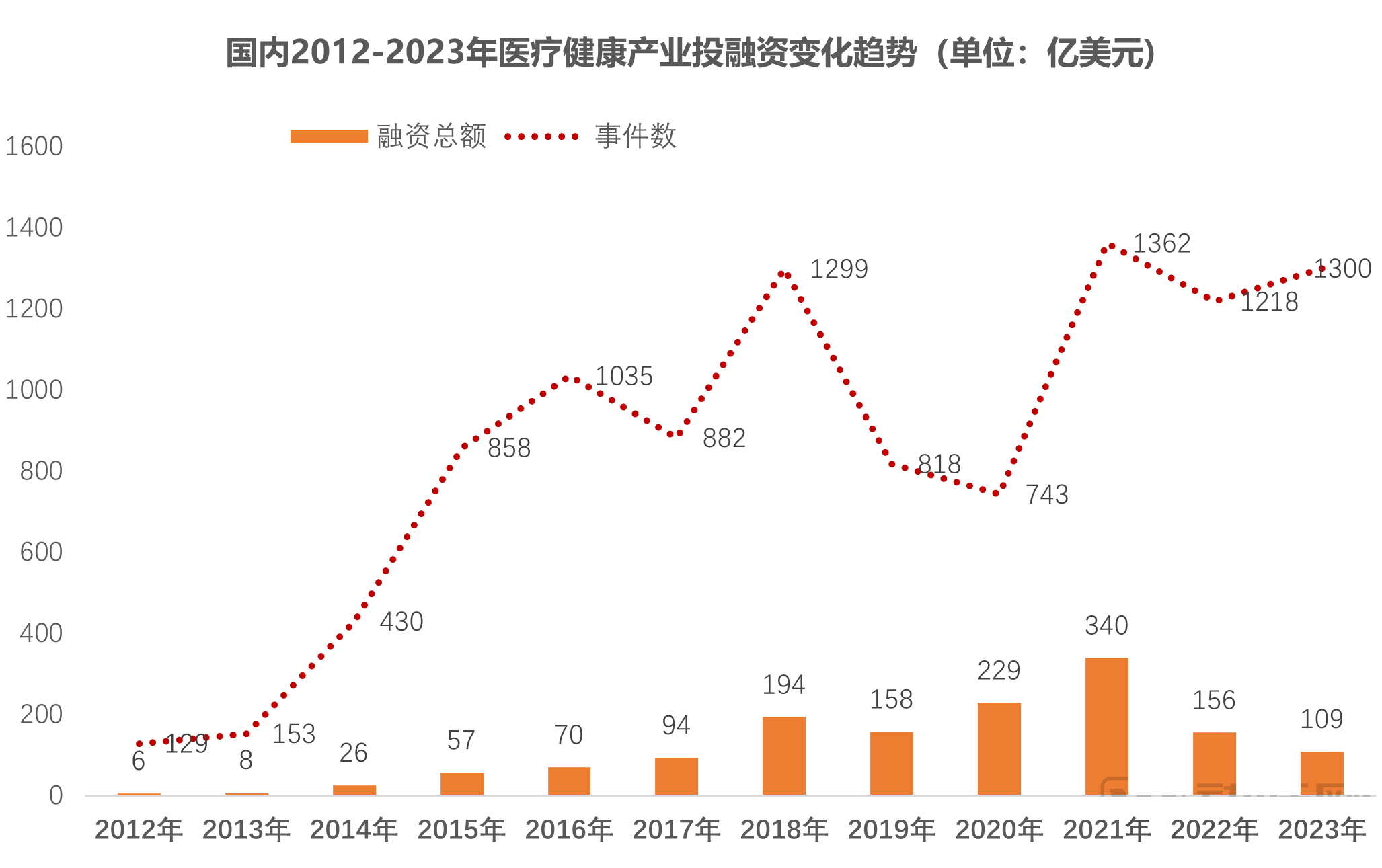

2. Total domestic healthcare financing in China declined again, with a 30.1% drop

Domestically, a total of 1,300 primary market financing deals were completed in the healthcare industry in 2023, with a cumulative $10.9 billion in early- and mid-stage capital flowing into innovative healthcare ventures.

Unlike the global healthcare primary market, which has maintained steady growth in investment and financing under normal conditions, China’s healthcare primary market has entered a cycle of volatile decline in terms of total financing volume, with transaction scales reverting to levels seen between 2017 and 2018. However, compared to 2022, when the total transaction value halved directly from the 2021 level, the year 2023 saw the impact of the COVID-19 pandemic gradually dissipate, and the decline in total financing within China’s healthcare primary market narrowed to 30.1%.

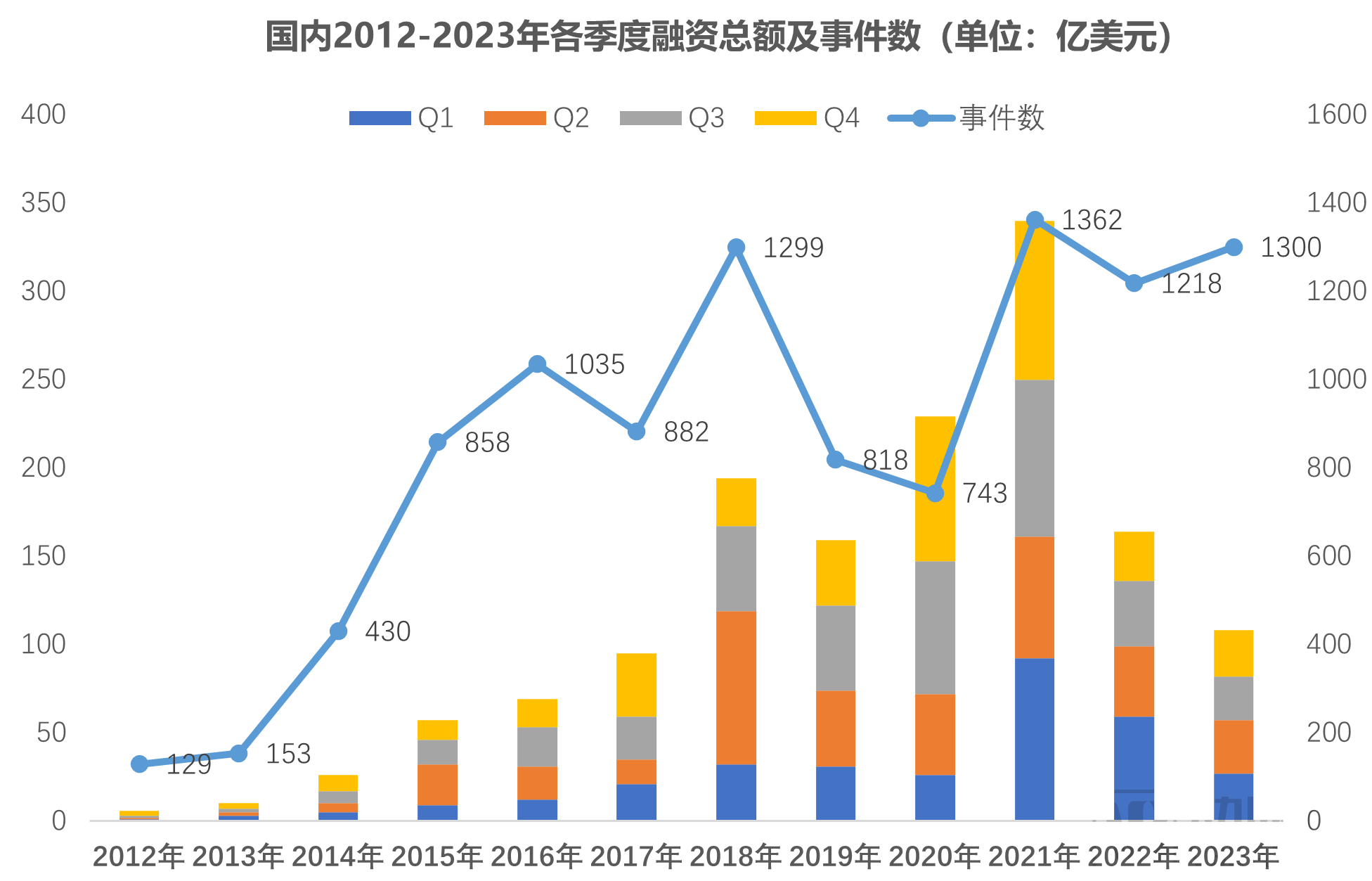

In terms of seasonal characteristics, investment and financing activities in China’s primary healthcare market have similarly seen a weakening of seasonal variations, likely due to shifts in how investment institutions screen potential targets.

An analysis of global and domestic investment and financing data reveals that, on the surface, the 2023 capital winter in healthcare uniformly impacted medical innovation projects worldwide. At a deeper level, however, it has quietly shifted global healthcare venture capital investment strategies—from backing ideas, innovation, and potential to prioritizing maturity and stability.

Total financing amounts shrank by 20% to 30%, while the frequency of financing rounds increased slightly, leading to a significant decline in the average financing amount and indicating difficulties in valuation growth for global healthcare projects. Data shows that in 2023, the average financing amount for global healthcare innovation projects even returned to levels seen around 2018, far below those of 2021.

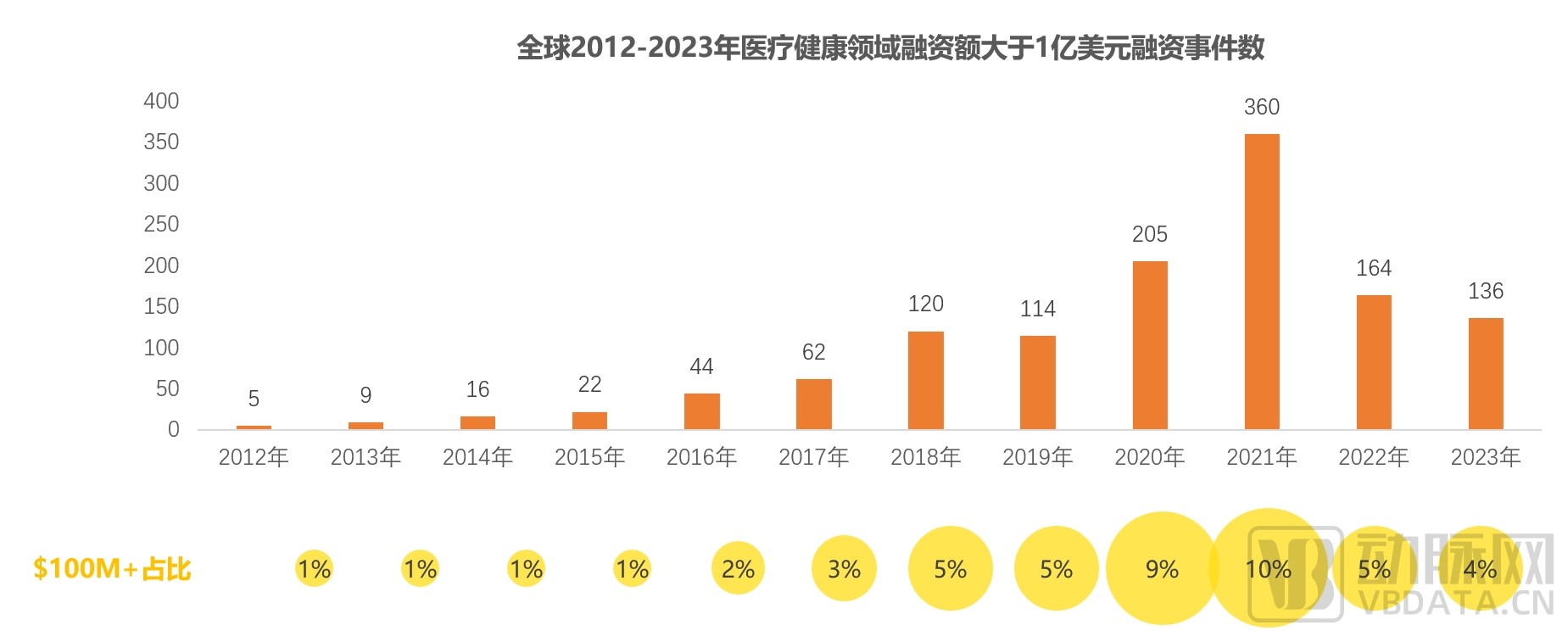

Significant Drop in Transactions Over $310 Million, While Trading Activity Remains High

In 2023, the number of large transactions exceeding $100 million decreased by 17.6%.Throughout the year, there were 136 financing deals exceeding $100 million in the global primary healthcare market, accounting for 4% of all financings. In 2021, this proportion reached 10%. For a period both before and after that year, the share of large-ticket transactions remained in the single digits. In fact, during typical years since 2018, the proportion of large-scale financings in the global healthcare industry has remained stable at around 5%.

Notably, despite a contraction in overall capital-raising capacity, the global primary market for healthcare and life sciences has maintained robust investment and financing activity.2023 was a relatively active year for such transactions over the past 11 years, with the total number of deals showing a significant increase compared to the approximately 2,000 transactions recorded before the 2020s. Furthermore, if data from 2020 to 2022—the period marked by the global outbreak of COVID-19—are excluded, a direct comparison between 2019 and 2023 reveals that global primary market financing and investment in healthcare continued to demonstrate a sustained and stable growth trend in 2023.

Similar to the global healthcare primary market, financing and investment activity in China’s healthcare primary market remained at historically high levels from 2021 to 2023.Interestingly, between 2022 and 2023, a divergence emerged in the frequency and scale of financing and investment activities within China’s primary healthcare market. On one hand, as China’s medical innovation landscape and venture capital ecosystem have matured, an increasing number of institutional investors have become active in the equity market, demonstrating strong willingness to invest. On the other hand, faced with the commercialization and capitalization challenges that innovative enterprises encounter during the mid-to-late stages of their growth, institutional investors have adopted a more prudent approach in their decision-making, preferring a strategy of “small steps and quick iterations” to mitigate risks.

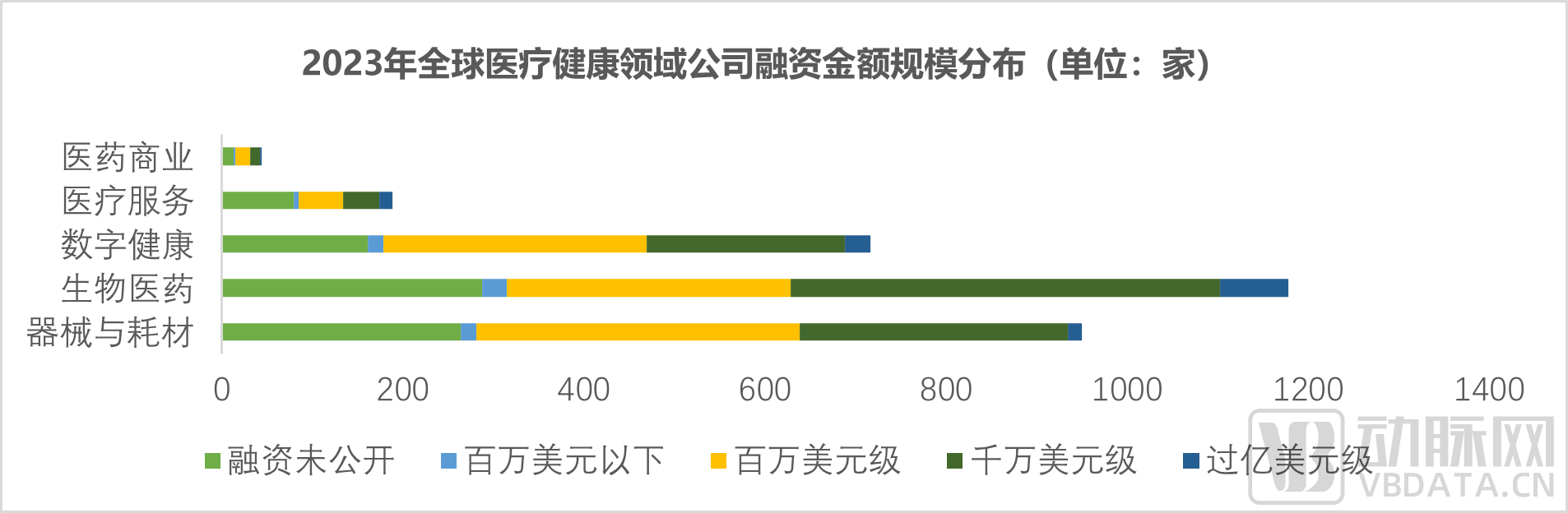

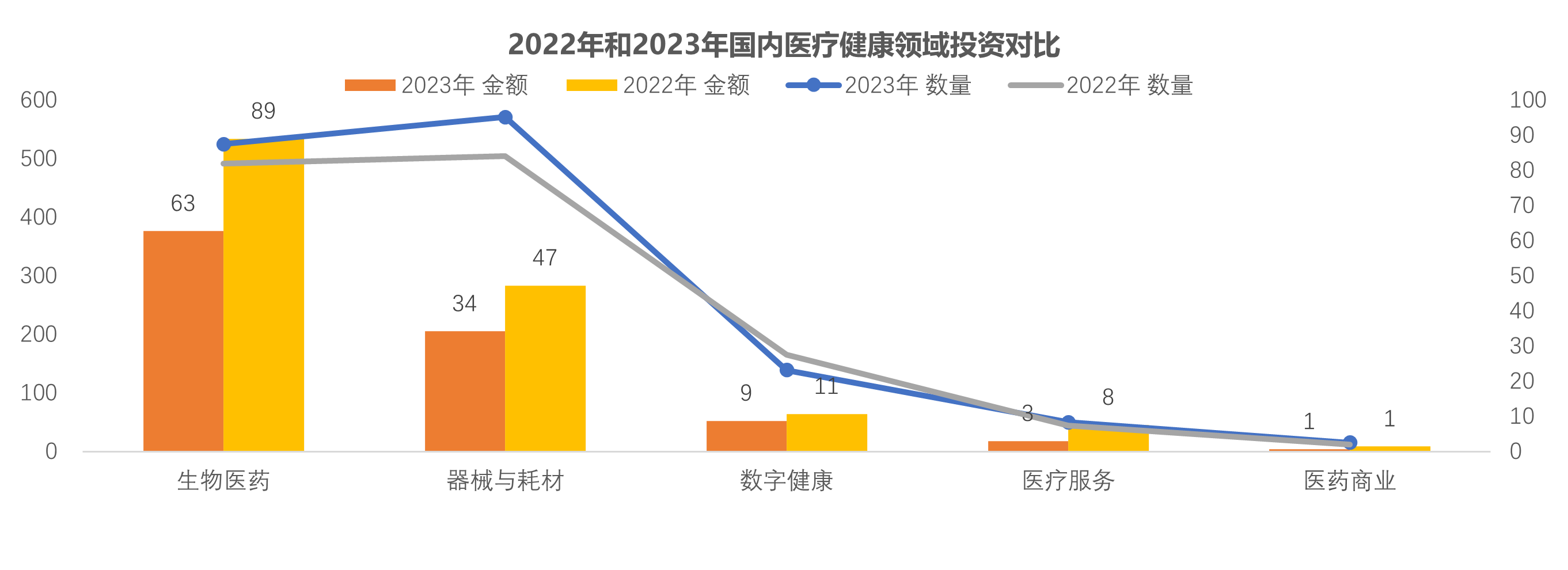

Breaking down by subsectors, in the global primary healthcare market in 2023, biopharmaceutical projects ranked first in both financing scale and activity level, followed by medical device and consumable projects. Although the pharmaceutical commercialization sector saw the single largest transaction of the year, its overall capital attraction and transaction activity were the lowest among all subsectors.

Furthermore, when distinguishing by the amount of individual transactions, excluding events for which transaction amounts were not disclosed,In 2023, global primary market investment and financing in healthcare focused on early-to-mid-stage projects with funding amounts in the tens of millions of US dollars., followed by projects in the initial stage with deal sizes in the millions of dollars; transactions with exceptionally large deal sizes (i.e., over $100 million) or exceptionally small deal sizes (i.e., under $1 million) account for a very low proportion.

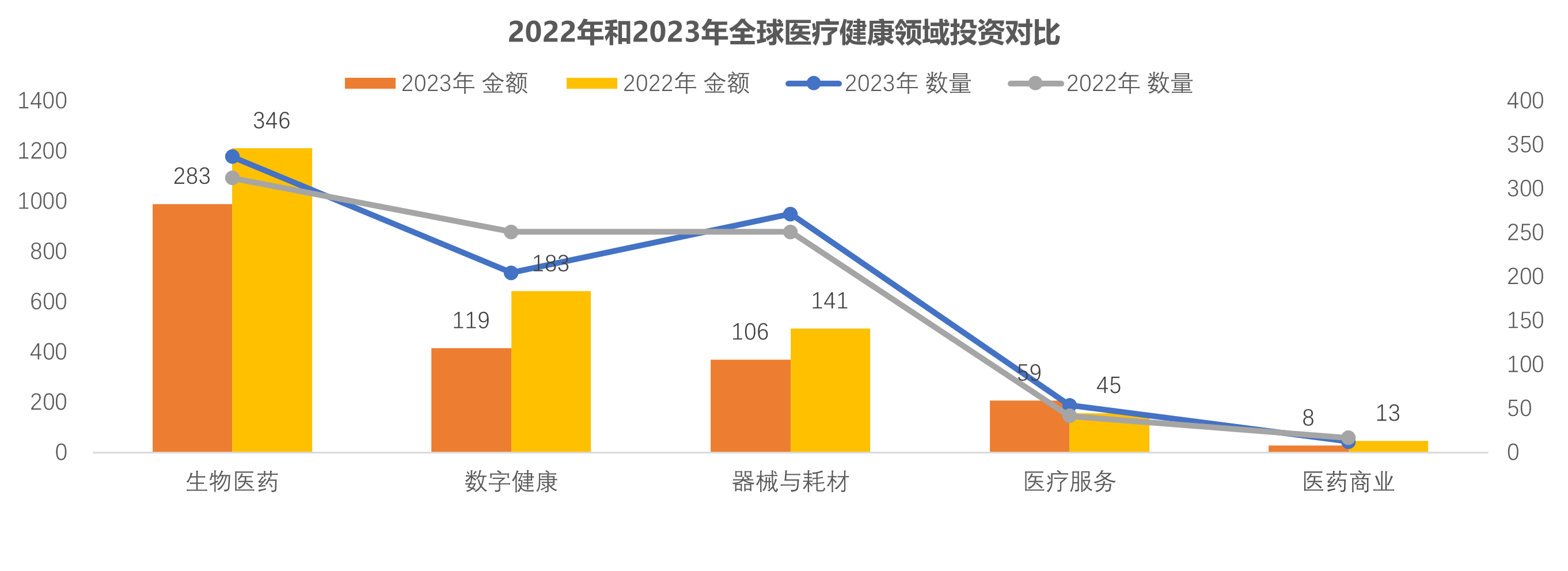

4. Volume increases and prices decrease for pharmaceutical and medical device projects; institutions bet on mature projects, with domestic institutions becoming more cautious

Compared with 2022, the total financing amount for biopharmaceutical, medical device, and consumable projects decreased in 2023, while the number of transactions increased, leading to a further reduction in the average transaction size. This reflects that venture capital funds have maintained their strategy of investing early and in smaller deals within these sub-sectors. Meanwhile, the average transaction size for digital health projects remained relatively stable. In light of the case studies and hotspot analysis presented later, global investment in digital health has begun to cool down after the frenzy between 2021 and 2022. Many early-stage projects are facing financing difficulties, and institutional investors are more inclined to bet on mid-to-late stage projects with relatively mature commercialization.

In China, the total investment and financing amounts and transaction frequencies across various sub-sectors in 2023 generally followed trends synchronized with the global market, differing only in the magnitude of change. Notably, for biopharmaceutical, medical device, and consumable projects, the average deal size in the domestic investment and financing market declined more significantly than in the global market, reflecting greater caution among Chinese institutions when investing in such projects.

5. Transactions are concentrated in Series A projects, making it difficult to increase project valuations, and the penetration rate of domestic technology transfer remains low.

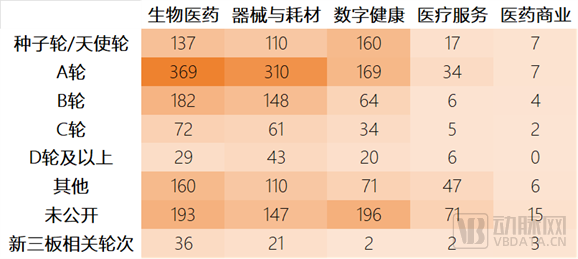

By transaction round, in 2023, apart from deals with undisclosed rounds, the primary focus of transactions in the global primary healthcare market was on Series A projects. Furthermore, a significant proportion of financing events across various sub-sectors had undisclosed rounds. Among the financing completed in 2023 by global companies in the biopharmaceutical, medical device, digital health, healthcare services, and healthcare commerce sectors, 16.3%, 15.4%, 27.3%, 37.7%, and 34.1% of the financing events, respectively, did not disclose the round.

Upon closer examination, although most innovative enterprises have secured a new round of financing, their valuations have failed to reach the levels expected for the next funding stage.In China, a growing number of innovative startups have adopted financing round designations such as “+,” “++,” and even “+++.” The underlying rationale is similarly rooted in the difficulty of achieving valuation growth. Analytical firms have pointed out that undisclosed financing rounds often signal tight cash flow for the companies involved, indicating they may soon need to raise additional capital to sustain operations. For companies using “+,” “++,” and similar notations to mark new financing, their financial situations are likely comparable.

Distribution of Financing Rounds Across Global Healthcare Sectors in 2023 Data Source: VCBeat Orange Database

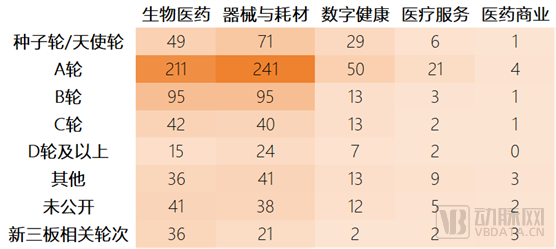

In China, the distribution of investment rounds in the primary healthcare market in 2023 was largely consistent with global trends. The key difference lay in the extremely low frequency of seed-stage transactions. Among the 525 deals in biopharmaceutical projects, only 49 were seed/angel rounds; among the 505 deals in medical devices and consumables, only 71 were seed/angel rounds; and for medical services and pharmaceutical commerce projects, seed/angel financing events numbered in the single digits. This indicates that for domestic investors, incubating seed-stage projects remains a rare occurrence, even as the commercialization of scientific research achievements has become a popular concept.

Distribution of Financing Rounds Across Domestic Healthcare Sectors in 2023 Data Source: VCBeat Orange Database

II. Hotspot Analysis: Medical Innovation Continues to Move into Deep Waters

The Further Integration of Information Technology and Biotechnology Constitutes the Core Theme of Global Healthcare Venture Capital Investment in 2023.

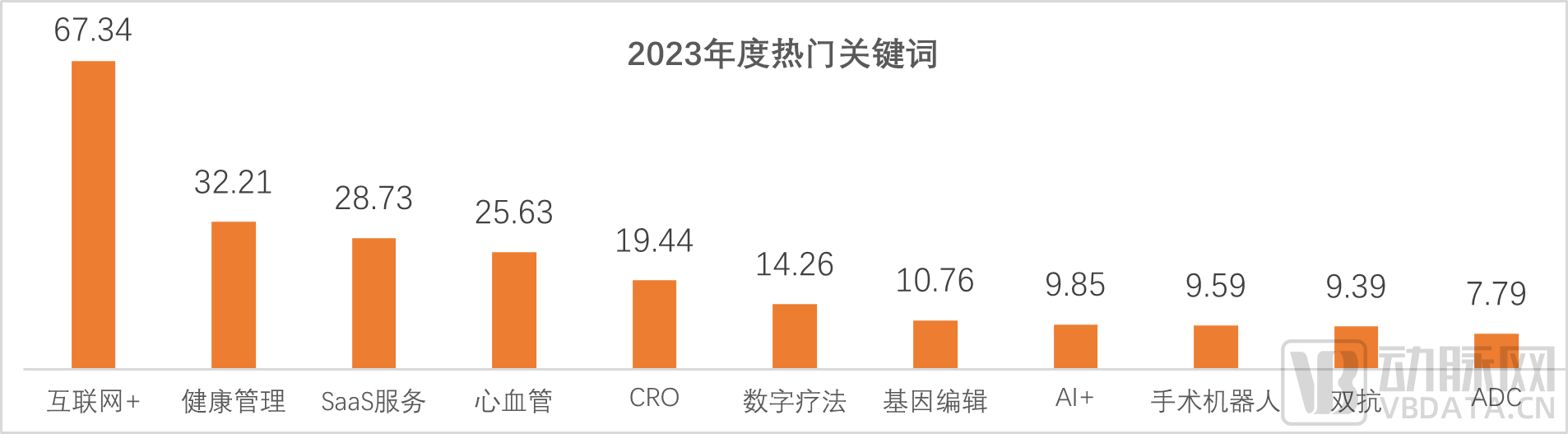

1. "Internet+" remains a hot topic, with bispecific antibodies and ADCs newly entering the rankings; only two biopharmaceutical companies made it into the TOP 100

Through a comprehensive analysis of tens of thousands of keywords in the global healthcare primary market in 2023, we have identified the top 10 annual buzzwords with the highest frequency and the largest financing transaction amounts, ranked by the cumulative total amount of related financing events. Traditional hot terms in global healthcare innovation, such as “Internet+,” health management, and SaaS services, continue to dominate the top rankings. Niche sectors that have garnered significant attention since 2021, including CROs, digital therapeutics, and surgical robots, have also maintained high levels of interest. Notably, frequent technological iterations in the global biopharmaceutical sector have propelled newer drug modalities, such as bispecific antibodies and antibody-drug conjugates (ADCs), to prominence as emerging buzzwords in the investment and financing market.

In terms of single-transaction value, the top 10 global healthcare primary market financing deals in 2023 were primarily from the healthcare services and digital health sectors. Among them, Smile Doctors, a dental service provider headquartered in Texas, USA, raised $550 million in a single round of financing, becoming the most well-funded healthcare innovation project globally in 2023. In addition to online and offline healthcare service projects, only two biopharmaceutical companies made it into the global top 10 financing list, originating from the fields of cell therapy and precision medicine services.

Top 10 Companies in Global Healthcare Primary Market Financing in 2023 Data Source: VCBeat Orange Database

In China, the top 10 annual financing list is dominated by biopharmaceutical and medical device projects. Haisen Biotech, ranked first, is headquartered in Hefei, Anhui Province. Despite being established for less than three years, it has already launched seven products. However, all of Haisen Biotech’s products have been acquired or licensed-in. Behind this success lies the strategic and operational support from Qiaokang Capital, along with industrial incentives provided by the Hefei Industrial Investment Group and Feidong County. This case exemplifies how pharmaceutical innovation models are increasingly aligning with clinical needs and practical applications.

Top 10 Companies in China’s Healthcare Primary Market Financing in 2023 Data Source: Artery Orange Database

2. Biopharmaceutical and Medical Device Projects Dominate the Rankings, with State-Owned Capital and Industrial Funds Taking the Lead

Among the top 10 global biopharmaceutical financing deals, innovative drugs for respiratory diseases, radiopharmaceuticals, and RNA-based therapeutics have demonstrated strong performance. Projects in cell and gene therapy (CGT) and antibody-drug conjugate (ADC)-related fields have also attracted significant capital interest. Notably, ElevateBio has completed four rounds of funding since its inception, each representing a major financing event at the time, bringing its total cumulative funding to $1.246 billion. It is worth noting that while strengthening its internal capabilities, ElevateBio has also pursued industrial mergers and acquisitions to expand its scale and competitiveness. For instance, in October 2021, ElevateBio acquired the biotechnology startup Life Edit Therapeutics, thereby gaining access to a complementary technology platform that integrates with its existing cell and gene therapy capabilities to achieve rapid advancement.

Top 10 Global Biopharmaceutical Companies by Financing in 2023 Data Source: VCBeat Orange Database

In China, professional outsourcing service platforms played a significant role in the biopharmaceutical financing deals of 2023. WuXi XDC (ranked second), Bio-Genius Biotech (ranked third), and Pharmaron (ranked eighth) all provide CDMO services to external clients. Although skepticism toward the CDMO sector persisted throughout the year, China’s biologics CDMO field attracted over $650 million in financing. Notably, these funds primarily flowed to CDMOs supporting currently hot biotechnologies such as antibody-drug conjugates (ADCs) and cell and gene therapies.

Top 10 Biopharmaceutical Companies in China by Financing in 2023 Data Source: VBData

In the medical device sector, the total funding volume of the global top 10 deals in 2023 was approximately half that of the top 10 biopharmaceutical deals globally, and was comparable to the figure for China’s top 10 biopharmaceutical deals. Among these, the most heavily funded global medical device project in 2023 was Neuralink, Elon Musk’s brain–computer interface (BCI) company. In August 2023, Neuralink closed a $280 million Series D financing round, bringing its cumulative fundraising to $653 million over the eight years since its inception, positioning it as a pioneer in the clinical application and development of BCI technology worldwide. Less than two months after the Series D closing, Neuralink announced the formal recruitment of participants for its first-in-human clinical trials, primarily targeting patients with quadriplegia caused by amyotrophic lateral sclerosis (ALS).

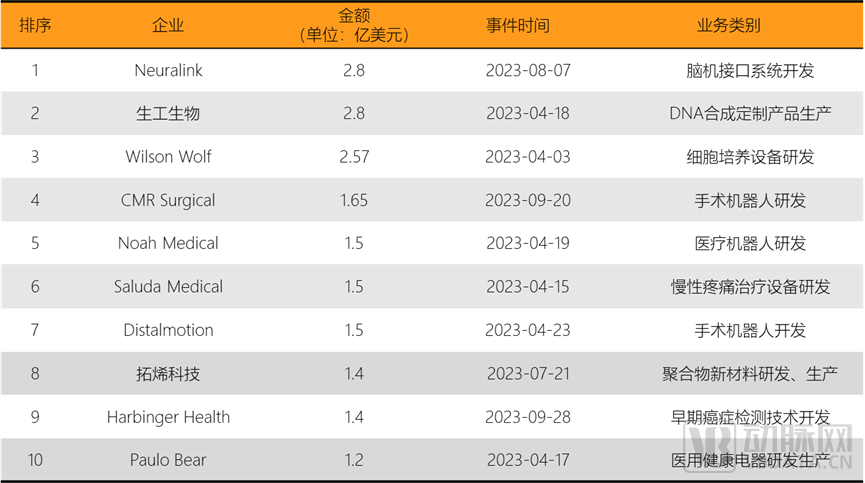

Furthermore, medical/surgical robots are a hot investment area in the global medical device industry.CMR Surgical, Noah Medical, and Distalmotion, ranked fourth, fifth, and seventh respectively, are all dedicated to developing robotic products that fill clinical gaps.

Top 10 Global Medical Device Companies by Financing in 2023 Data Source: VBData

In China, the largest single financing round in 2023 was secured by Sangon Biotech, a company primarily engaged in the custom production of DNA synthesis products. With nearly 30 years of history, Sangon Biotech is a key domestic supplier of upstream raw materials for scientific research and industrial applications, including primers, probes, enzymes, proteins, and antibodies. In April 2023, Sangon Biotech completed its first round of strategic financing, with participation from Defu Capital, CPE Yuanfeng, Jinglin Investment, the Capital Health Industry Fund managed by Huagai Capital, and Guokai Kechuang, among others, propelling the company’s expansion from the domestic market to the global stage. Furthermore, top-tier medical device financings in China mainly focused on high-end consumables and cardiovascular devices, achieving breakthroughs in the localization of multi-category medical devices. Ranking second, Tuoxi Technology completed a Series B financing round equivalent to USD 140 million in July 2023. Its main product, special cyclic olefin copolymers (SOOC® Tuomeite®), represents one of the critical “chokepoint” high-end materials in China. Meanwhile, Yongrenxin and Yixin Medical, which each secured financing equivalent to USD 100 million in March and September respectively, are developing artificial hearts and transcatheter heart valve devices.

Top 10 Domestic Medical Device Companies by Financing in 2023 Data Source: VCBeat Database

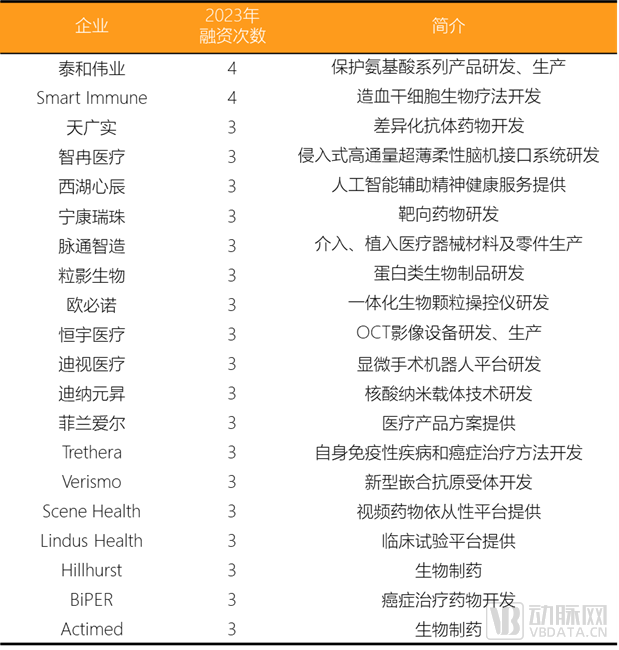

3. 238 global companies completed two or more rounds of financing, with capital flowing toward familiar leading projects

Notably, in 2023, numerous global projects completed two or more rounds of financing, with substantial capital converging on leading projects across various niche sectors.

In 2023, 238 global companies completed two or more rounds of financing, accounting for 8.4% of the total. Among them, Taihe Weiye, a Chengdu, Sichuan-based developer and manufacturer of protected amino acid series products, and Smart Immune, an overseas developer of hematopoietic stem cell biotherapies, each completed four rounds of financing in 2023, making them the most active companies globally in terms of investment and financing activity for the year.

Global Companies That Completed Three or More Rounds of Financing in 2023 | Data Source: VCBeat Orange Database

In addition, 18 companies completed three rounds of financing in 2023, primarily from the fields of active pharmaceutical ingredients (APIs), surgical robots, bispecific antibodies, and antibody-drug conjugates (ADCs). Amid the capital winter, innovative projects that continue to attract investment either address clear and growing market demands, possess translatable breakthrough technological advantages, or have achieved impressive data. The niche sectors in which these companies operate may see a new competitive landscape emerge within the next two to three years.

III. IPO Analysis: Cooling Capital Markets, Healthcare Innovation Enterprises Need More Diversified External Funding

1. IPO Pace Slows Further, with U.S. Companies and Capital Markets Taking the LeadStrength

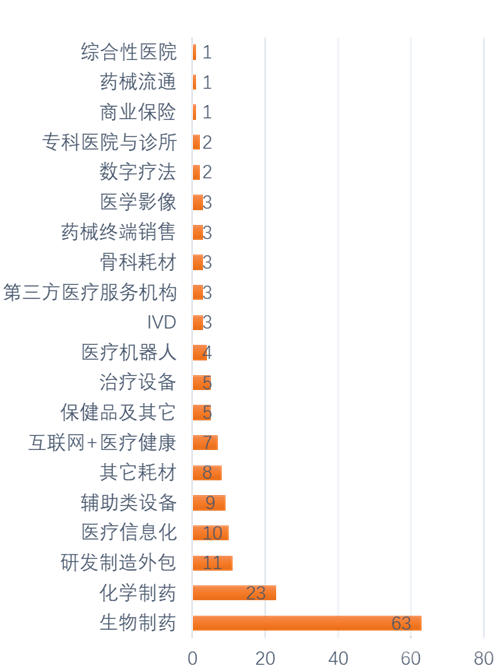

In 2023, the pace of global healthcare companies going public slowed further, with only 175 firms completing initial public offerings (IPOs) throughout the year. Among them, biopharmaceutical companies accounted for the largest number of IPOs, reaching 63, followed by chemical pharmaceutical companies with 23 IPOs; together, these two sectors represented nearly 50% of all healthcare IPOs.

Breakdown of Global Healthcare IPOs by Sector in 2023 | Data Source: VBInsight Database

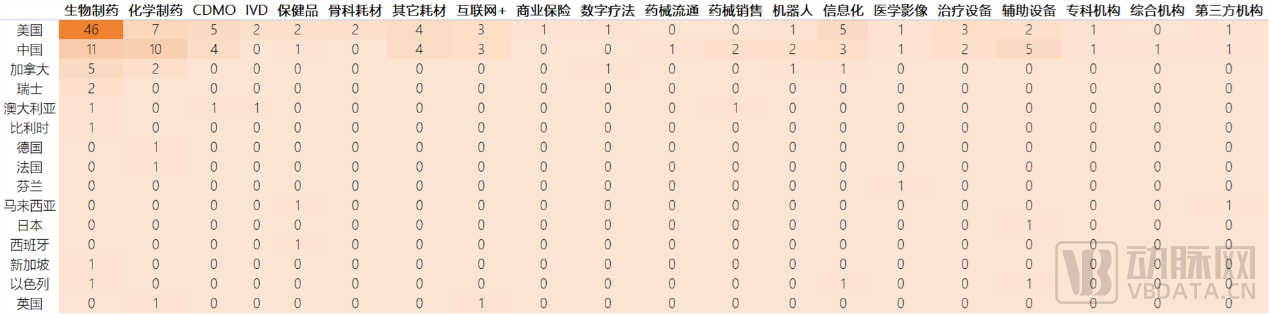

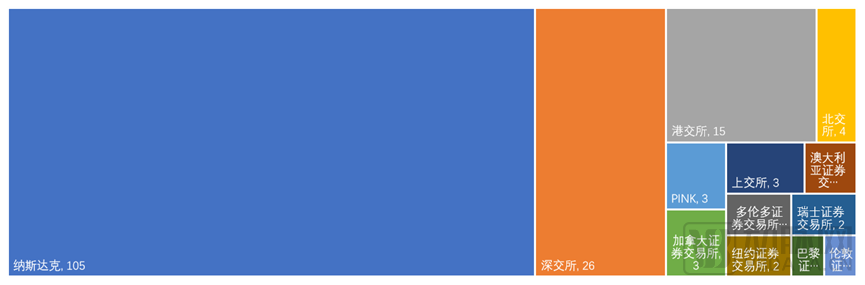

Among the 175 healthcare companies that went public, 87 were from the United States, accounting for nearly half, while 52 were from China, ranking second. Overall, in the secondary market, companies from North America and Asia were relatively more active. A total of 153 companies came from the United States, China, Canada, Malaysia, Japan, and Singapore, representing 87.2% of the total, whereas companies from Europe were relatively fewer.

2023 Global Distribution of IPOs Across Healthcare Sectors by Country Data Source: Arterial Orange Database

2. Global IPOs: Johnson & Johnson’s Spin-off Leads, Four Chinese Companies Make the List

In 2023, the company that raised the most capital through an initial public offering (IPO) globally was Kenvue, the consumer health business spun off from Johnson & Johnson. Kenvue owns multiple mainstream personal care brands, including Neutrogena, Band-Aid, Tylenol, Listerine, and Dabao. After more than a year of independent operations, Kenvue listed on the New York Stock Exchange in May 2023. Its stock price continued to rise after the opening bell on its IPO day, closing with a full-day gain of 22.27% and achieving a market capitalization exceeding $50.2 billion. Additionally, in October 2023, Sandoz, the Swiss giant in generic drugs and biosimilars, listed on the SIX Swiss Exchange, with an IPO market capitalization of CHF 10.3 billion (approximately $11.2 billion). As the IPO share placement ratio for Sandoz was not available in public records, we estimated it at the conventional 25%, implying that Sandoz raised approximately $2.9 billion in its initial offering, making it the second-largest healthcare IPO globally in 2023 by fundraising scale.

Top 10 Global Healthcare IPOs in 2023 Data Source: VBInsight Database

Notably, four Chinese companies—ZhiXiang JinTai, WuXi XDC, Hongyuan Pharmaceutical, and FuErJia—all operating in the biopharmaceutical sector, were among the global healthcare IPOs in 2023.

In terms of capital market selection, the U.S. stock market has re-emerged as the predominant venue for initial public offerings (IPOs) by global healthcare companies. In 2023, more than half of the healthcare enterprises that went public chose the U.S. market, followed by China’s domestic capital markets. This trend is driven by two main factors: first, under the macroeconomic conditions of global liquidity tightening, trading volumes on the Hong Kong Stock Exchange, as an offshore financial center, declined significantly, leading to a marked decrease in the number of healthcare companies listing in Hong Kong compared to other years since 2018; second, with the heightened compliance thresholds for the STAR Market and the ChiNext Board in China, the number of enterprises listing on the Shanghai and Shenzhen Stock Exchanges has also decreased substantially.

Global Distribution of Healthcare IPOs by Capital Market in 2023 Data Source: VCBeat Database

3. Domestic IPOs: 70% are biopharmaceutical companies; the Shenzhen Stock Exchange is the most popular, followed by the Hong Kong Stock Exchange

Among the top 10 healthcare IPOs in China, there were seven biopharmaceutical companies, two medical device companies, and one healthcare service company, with innovative biopharmaceutical enterprises remaining the main force in IPOs. Notably, Zhixiang Jintai, an innovative monoclonal and bispecific antibody drug company from Chongqing, went public in June 2023. Founded by the controlling shareholder of Zhifei Biological Products, a leading domestic biological vaccine enterprise, the company has established two technology platforms: a monoclonal antibody drug discovery platform based on a novel phage display system, and a bispecific antibody drug discovery platform. Additionally, it has built an efficient recombinant antibody drug process development platform for drug development, forming a complete industrial chain layout encompassing innovative drug discovery, process development, clinical research, and commercial production.

Top 10 Healthcare IPOs in China in 2023 Data Source: VCBeat Orange Database

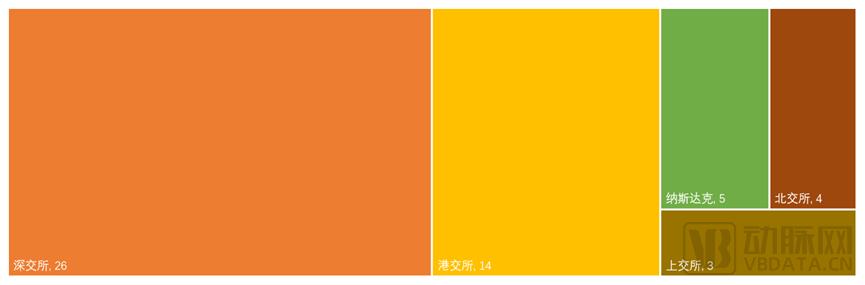

In China, the Shenzhen Stock Exchange (SZSE) emerged as the preferred capital market for healthcare IPOs in 2023, with 26 companies listing there, accounting for half of the total. The Hong Kong Stock Exchange (HKEX) was the second most popular global capital market for domestic healthcare IPOs in 2023, a finding that came as quite a surprise. This trend is likely driven primarily by the cost-effectiveness of the HKEX’s listing requirements and associated costs, coupled with the approaching exit deadlines for early-stage institutional investors. Furthermore, the number of domestic healthcare IPOs on the NASDAQ, Beijing Stock Exchange (BSE), and Shanghai Stock Exchange (SSE) was broadly similar.

2023 Capital Market Distribution of Domestic Healthcare IPOs in China Data Source: Arterial Orange Database

4. BSE’s market enthusiasm still needs to be boosted, but listed companies have delivered strong performance

In November 2021, the Beijing Stock Exchange (BSE) officially commenced trading, with the first batch of 81 companies listing simultaneously. Amid tightening IPO standards on the STAR Market of the Shanghai Stock Exchange and the ChiNext Board of the Shenzhen Stock Exchange, coupled with declining liquidity on the Hong Kong Stock Exchange, market attention has increasingly shifted toward the BSE. However, current data indicate that the BSE has not yet become the preferred capital market for domestic healthcare companies. 2023 marked the second full year of trading since the BSE’s inception, during which four biopharmaceutical companies chose to list on the exchange. Among these four, except for a slight decline in the stock price of Kangle Weishi, the market capitalizations of the others surged significantly on their listing days and continued to climb. Notably, Jinbo Bio, which listed in July 2023, has seen its stock price rise by 1,090.95% since its IPO.

Healthcare Companies Listed on the Beijing Stock Exchange in 2023 and Their Market Capitalization Performance Data Source: VCBeat Orange Database

IV. Analysis of Investment Institutions: Leading Firms Maintain High-Frequency Investment Activity

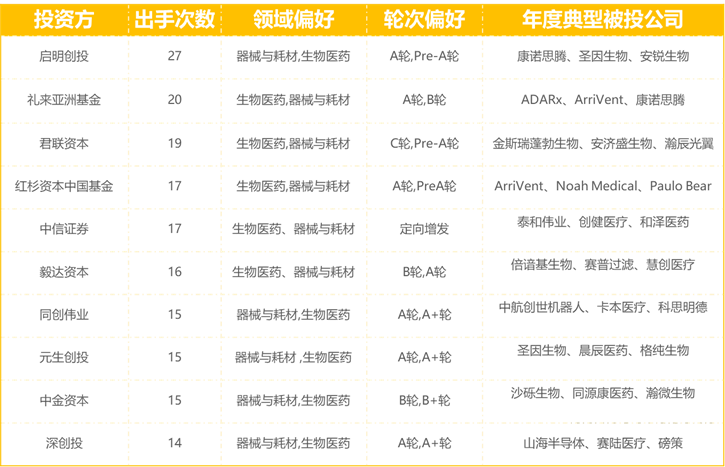

Qiming Venture Partners made a total of 27 investments, becoming the most active investment firm of the year, while domestic investment firms significantly reduced their deal activity.

In 2023, top-tier venture capital firms maintained a high frequency of investment activity. Among them, Qiming Venture Partners led the pack with 27 deals in the global healthcare market, ranking first. Lilly Asia Ventures and Legend Capital followed in second and third place, with 20 and 19 deals, respectively. Notably, unlike the previous trend of top firms clustering around headline-grabbing projects, these leading investors demonstrated greater independence in their project selection in 2023.

Top 10 Most Active Investors in the Global Healthcare Primary Market in 2023 Data Source: Artery Orange Database

On one hand, value investment has been adopted as a core strategy by more investment institutions. Different investment firms, based on their varying understandings of clinical needs, select differentiated high-potential sectors and identify specific projects with growth advantages from within them, inevitably leading to diversified investment portfolios. On the other hand, amid the capital winter, most medical innovation enterprises face financing difficulties. Investment institutions tend to allocate limited funds to projects they are familiar with, or even have previously invested in, thereby enhancing investment certainty while providing essential financial support to portfolio companies.

V. Analysis of Hotspot Regions

1. China Leads the World in Financing Activity, Yet Average Deal Size Still Needs Improvement

In 2023, China was the most active region globally in the primary healthcare market, completing a total of 1,301 financing transactions with a total funding amount of $10.962 billion. The United States ranked second in terms of investment and financing activity in the healthcare primary market, completing 1,145 financing transactions with a cumulative funding amount reaching as high as $34.933 billion. Among these, the average financing amount for domestic healthcare innovation projects was $8.42 million, while this figure for U.S. projects was $30.5 million, approximately 3.6 times higher than that of China. This indicates that there is still significant room for growth in China's healthcare primary market.

Hotspots for Primary Market Investment and Financing in Global Healthcare, 2023 | Data Source: VCBeat Orange Database

2. Jiangsu is the hottest region for healthcare investment and financing, with nearly 80% of funding concentrated in this hotbed

In 2023, Jiangsu Province was the hottest region for healthcare venture capital and private equity investment in China, completing a total of 256 financing deals with a cumulative amount of USD 1.843 billion. Guangdong Province ranked second, with 221 financing deals involving a total amount of USD 1.566 billion. Shanghai ranked third, completing 207 financing deals with a total amount of USD 2.652 billion.

Hotspots for Primary Market Investment and Financing in China’s Healthcare Sector in 2023 Data Source: Artery Orange Database

Hotspots for Primary Market Investment and Financing in China’s Healthcare Sector in 2023 Data Source: Artery Orange Database

In 2023, there were a total of 1,034 primary market financing deals in the healthcare sector originating from the Yangtze River Delta, Guangdong Province, and Beijing. In other words, nearly 80% of domestic healthcare financing events in 2023 came from these hotspots, clearly indicating a trend toward clustered development of medical innovation in China. However, it is worth noting that even in Shanghai, where healthcare innovation projects command the highest valuations, the average financing amount of approximately $12 million still falls short of the average for U.S. projects. Combined with the previous analysis, while the mainstream financing rounds in China are similar to those in the global market, there remains significant room for optimization in China’s healthcare innovation projects.

Please scan the QR code to add the assistant and obtain the full report. If you have already added the assistant, please proactively inquire: