China's Blood Products Industry Enters a Rapid Expansion Phase Amid Intensified Market Competition

Editor’s Note: This article is fromDonghai Fund, AuthorWang Jingyu, Pharmaceutical Researcher. Reprinted with permission from VCBeat.

Preface

Blood products are widely used and refer to plasma protein components derived from the plasma of healthy donors or specifically immunized donors through separation and purification, or prepared using recombinant DNA technology, as well as formed cellular blood components. They primarily include albumin, immunoglobulins, coagulation factors, anticoagulant proteins, and protease inhibitors.

The history of blood products can be traced back to the early 1940s, when they were developed to meet the urgent need for treating wounded soldiers during the anti-fascist war, and were regarded as vital strategic resources.

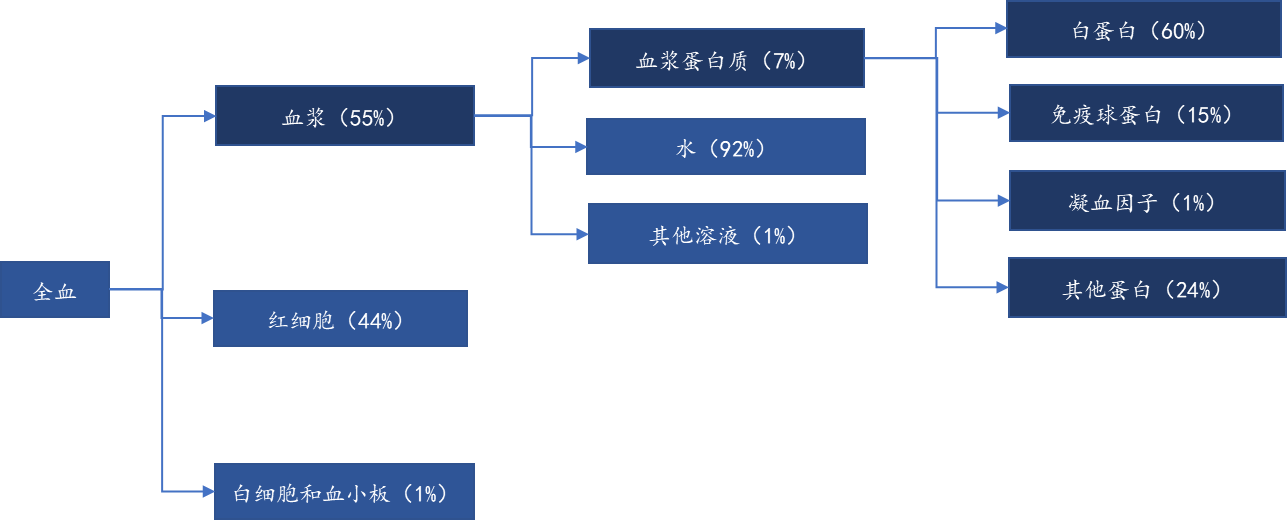

Figure 1: Composition and Content of Human Blood

Source: "Human Anatomy," PPTA, Chart by Donghai Fund

I. The global market size maintains steady growth, gradually forming an oligopolistic landscape

According to Research and Markets data,The global blood products market is projected to surpass $93.1 billion by 2030, maintaining a robust compound annual growth rate (CAGR) of approximately 10%. A review of major international blood product companies reveals that an oligopolistic market structure has been achieved through continuous mergers and acquisitions. The number of major global blood product companies has sharply declined from 102 in the 1970s to fewer than 20 today (excluding China; with five in the United States and eight in Europe).

According to data from the International Plasma Protein Therapeutics Association (PPTA) in 2021,CSL Behring, Baxter, Grifols, and Octapharma account for 78.84% of global plasma-derived therapy revenue. Currently, the CR5 (concentration ratio of the top five) of overseas plasma product manufacturers exceeds 80% in terms of production market share.

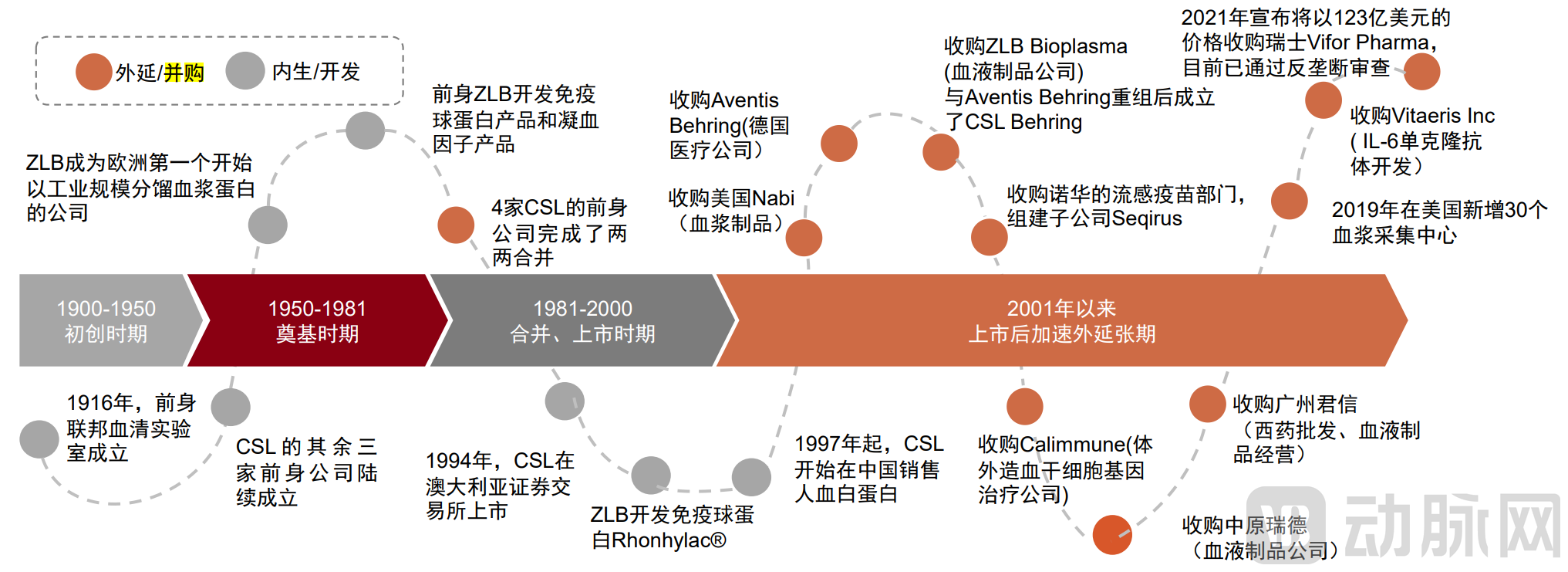

Taking CSL as an example,CSL successively acquired ZLB, Aventis Behring (USA), and China Zhongyuan Ruide, gradually expanding beyond its Australian homeland to emerge as a dominant survivor in the global consolidation of the plasma-derived therapies industry. According to CSL’s corporate announcements, as of December 2022, CSL operated 337 active plasmapheresis centers worldwide.

Figure 2: Overview of CSL’s Key Historical Milestones (as of May 2023)

Source: Capital IQ, CSL corporate announcements and website, CICC Research Department

II. China's blood products industry is in a phase of rapid development, with supply being the primary limiting factor

China's blood products industry is in a phase of rapid development.According to data from Menet, the sales of blood products in public medical institutions in China amounted to approximately RMB 46.4 billion in 2022. According to statistics from the Qianzhan Industry Research Institute, the market size of China’s blood products industry is expected to reach around RMB 78 billion by 2027, with a compound annual growth rate (CAGR) of 11.6% from 2022 to 2027.

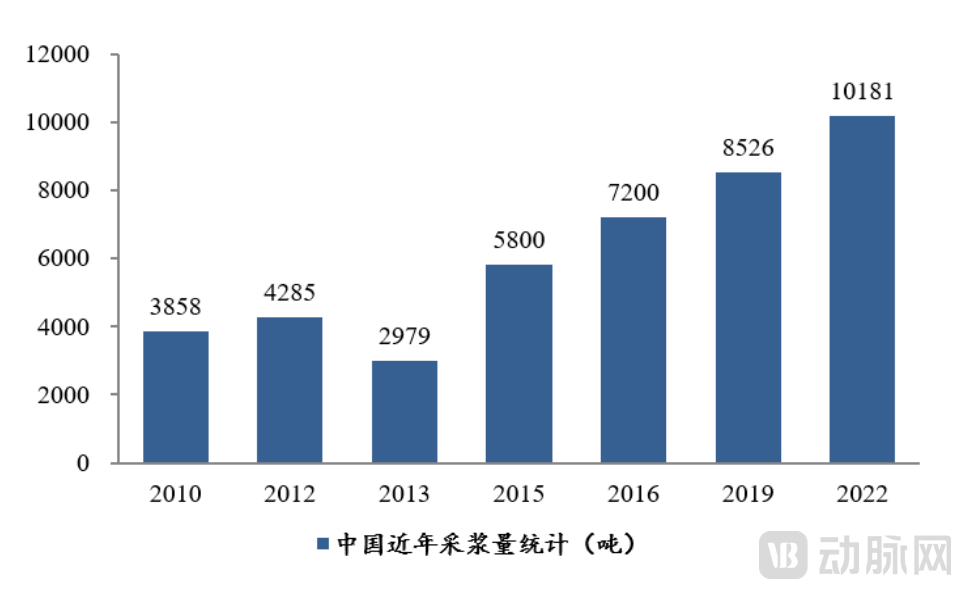

There is a significant gap between the supply and demand for plasma collection in China, with supply being the primary limiting factor.The actual demand for plasma collection is expected to exceed 16,000 tons, while the plasma collection volume of 28 domestic blood product manufacturers in China was approximately 10,181 tons in 2022.

Figure 3: Statistics on Plasma Collection Volume in China in Recent Years (tons)

Source: China Business Industry Research Institute, company announcements, National Health Commission, Soochow Securities Research Institute

The blood products industry has high entry barriers.China has implemented a series of restrictive policies on market access, source plasma collection, and production and operation in the blood products industry, thereby establishing significant policy barriers to entry.

● In 1985, the import of blood products other than albumin was banned.

● In 1996, only one plasmapheresis station was permitted within each blood collection area.

● In 2001, approval for new blood product manufacturing enterprises was halted; as of the end of 2022, there were only 28 such manufacturers in China.

● In 2002, the import of albumin from regions affected by bovine spongiform encephalopathy (BSE) was prohibited.

● In 2012, “three categories and six products” became the mandatory requirements for establishing plasma collection stations (to date, only 14 facilities meet these criteria)

Figure 4: Strict Standards Across All Stages of Blood Product Manufacturing

Source: Boya Bio-pharmaceutical Group official website, Kaiyuan Securities Research Institute

Figure 5: Domestic plasma collection systems are independent of whole blood collection systems

Source: Guan Yan Report Network, Open Source Securities Research Institute

III. Clear Provincial Planning for Plasma Collection Stations, with Frequent “Land Grabs”

China plans to establish more than 30 new plasma collection stations. During the 14th Five-Year Plan period, many regions drafted plans for adding new plasma collection stations.The Health Commission of Inner Mongolia Autonomous Region drafted the “Plan for the Establishment of Plasmapheresis Stations in Inner Mongolia Autonomous Region (2022–2025) (Draft for Comments),” which proposes the establishment of 10 plasmapheresis stations across the region from 2022 to 2025. The Health Commission of Yunnan Province formulated the “Plan for the Establishment of Plasmapheresis Stations in Yunnan Province (2021–2023),” planning to establish a total of 19 plasmapheresis stations province-wide (including 2 pilot plasmapheresis stations) on the basis of earlier pilot initiatives. The Health Commission of Jilin Province issued the “Notice on Printing and Distributing the Pilot Work Plan for the Establishment of Plasmapheresis Stations in Jilin Province,” proposing the establishment of 2 plasmapheresis stations as pilots within the jurisdiction of Changchun City.

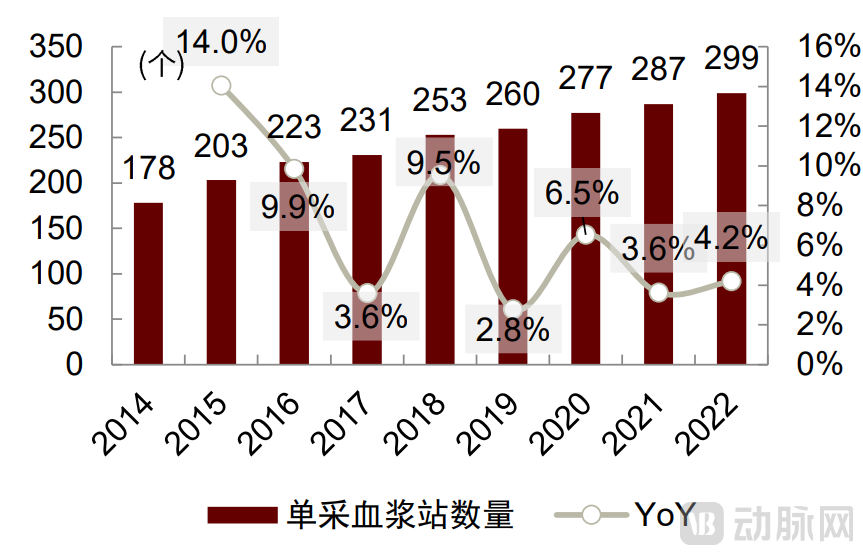

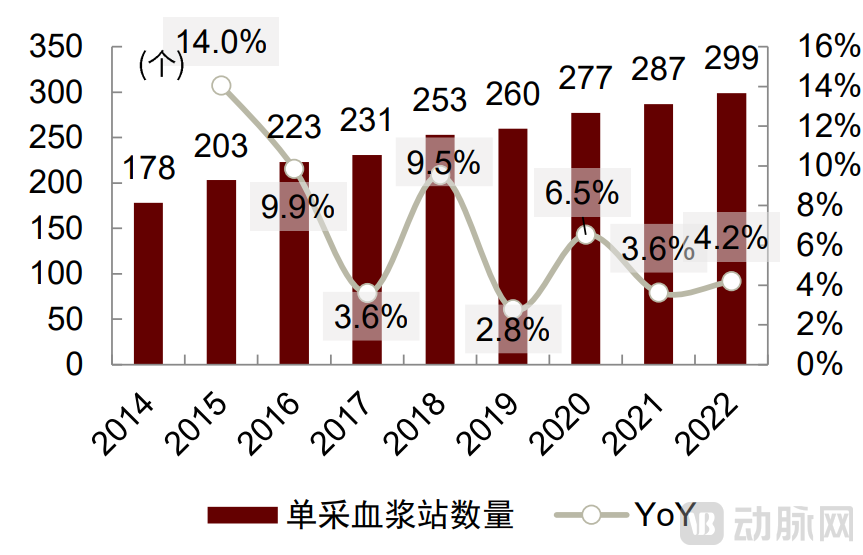

Figure 6: Number of Operating Plasmapheresis Centers in China (2014–2022)

Source: Data from CBI Research, company announcements, and CICC Research Department. Note: Some provinces have explicitly outlined plans for the establishment of single-apheresis plasma collection stations, with certain projects already implemented, such as in Yunnan Province and Henan Province; further attention may be paid to those that have not yet completed their planning. Sichuan Province, Liaoning Province, Heilongjiang Province, Guangdong Province, Jiangxi Province, and Hunan Province have clearly stated in their 14th Five-Year Plan that no additional plasma collection stations will be established.

Plasma collection volume per plasma station is lower than in Europe and the United States, but growth remains limited.In 2022, the average annual plasma collection volume per plasmapheresis center in China was approximately 34 metric tons; according to PPTA statistics, the average annual plasma collection volume per plasmapheresis center in the United States was approximately 54 metric tons in 2021.

Plasma collection stations in China are predominantly concentrated in sparsely populated areas of the central region, making it difficult to significantly raise the plasma collection ceiling for individual stations.

● Tiantan Biological's existing plasma collection stations are primarily concentrated in Gansu, Sichuan, and Hubei provinces.

● Shanghai RAAS’s plasma collection stations are primarily concentrated in Anhui and Guangxi.

● Hualan Biological's plasma collection stations are primarily concentrated in Chongqing and Henan.

● Pailin Biologics’ plasma collection stations are primarily concentrated in Heilongjiang Province.

● Boya Bio-pharmaceutical’s plasma collection stations are primarily concentrated in Jiangxi Province.

● Weiguang Biologics’ plasma collection stations are primarily concentrated in Guangdong.

Figure 7: Plasma donation frequency in China is significantly lower than in Europe and the United States

Source: Founder Securities

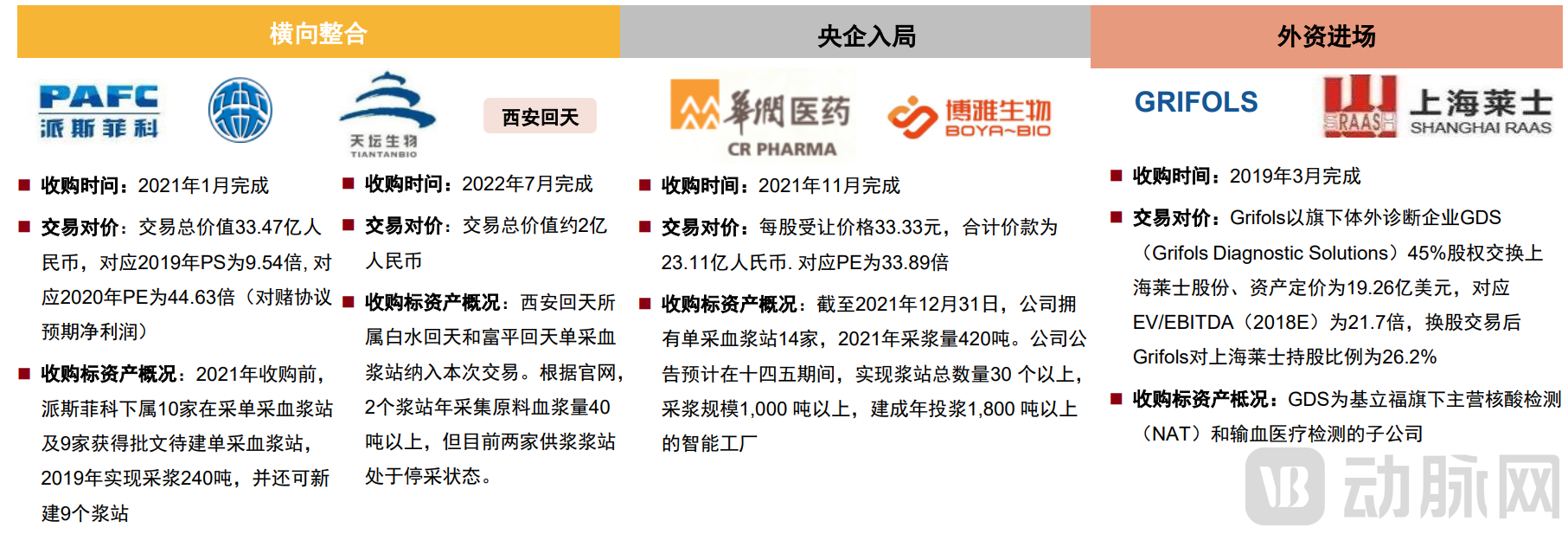

Domestic blood product companies are accelerating industry consolidation, which has entered its late stage. Companies are actively engaging in mergers and acquisitions to expand their market share and scale through partnerships, with numerous M&A cases emerging (as listed below).Through a review of most M&A cases, we found that during the 2015–2020 period, the valuation per ton of pulp capacity for most acquisitions ranged approximately between RMB 10 million and RMB 25 million per ton.

● Tiantan Biological Products restructured CNBG’s Shanghai Blood Products, Lanzhou Blood Products, Wuhan Blood Products, and Guizhou Zhongtai;

● Shanghai RAAS acquired Zhengzhou Banghe, Tonglu Biological, and Zhejiang Haikang;

● Pailin Biopharma acquired Harbin Pasifico;

Figure 8: M&A Cases of Chinese Blood Product Companies (as of H1 2023)

Source: Company announcements

IV. Industry Framework: Number of Plasma Collection Stations × Plasma Collection Volume per Station × Number of Product Varieties × Revenue per Ton of Plasma × Profit Margin

As previously mentioned, the number of plasma collection stations depends on each company’s approved capacity for such stations and their strategic planning in provinces where they hold a competitive advantage. Although there is room for growth in per-station plasma collection volume compared to developed countries in Europe and the United States, short-term increases are increasingly difficult to achieve; thus, it can be approximated as a constant.

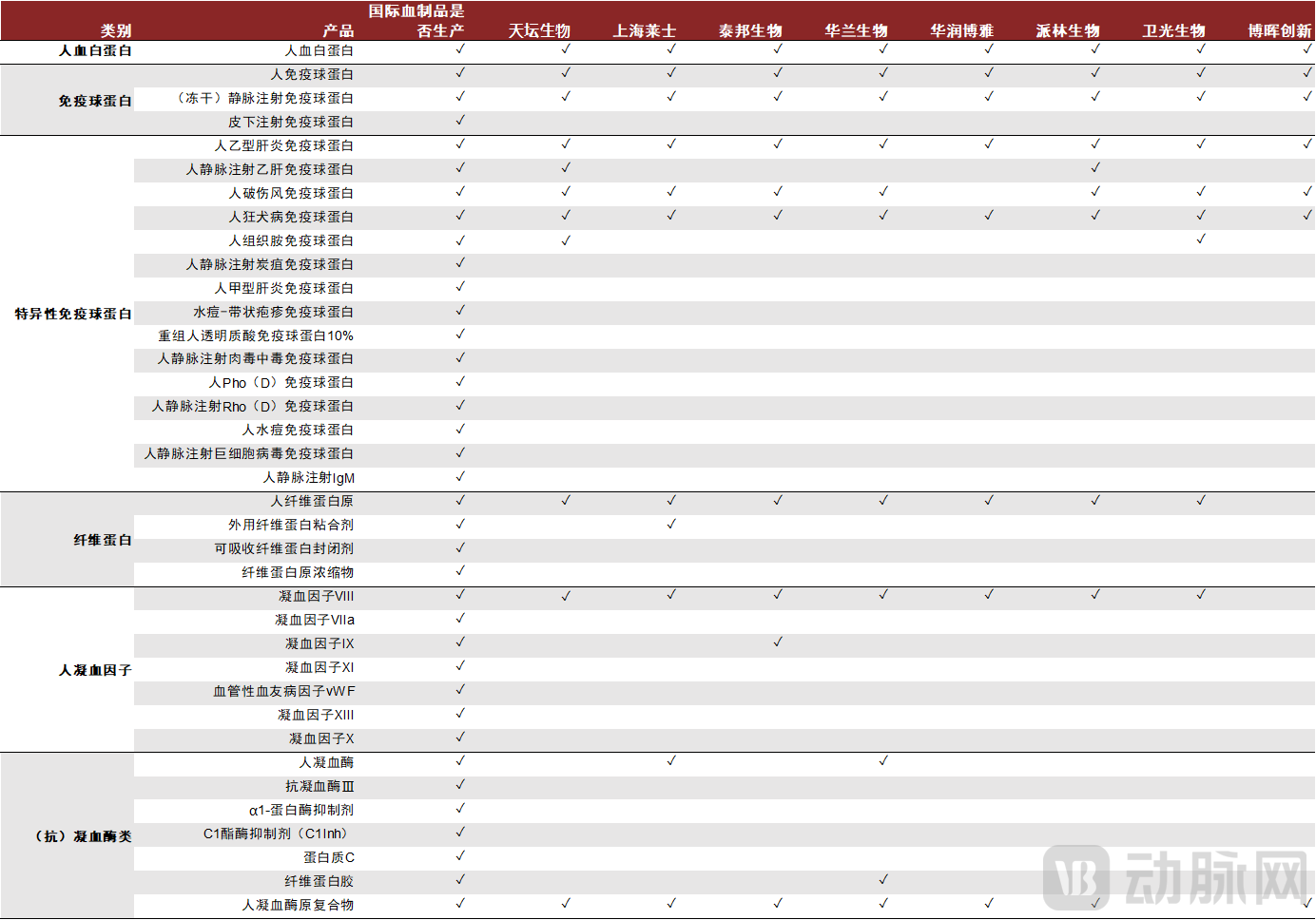

Product Variety:According to China’s Plasma Survey Report, human blood contains more than 150 types of proteins and factors. Large foreign enterprises are capable of isolating over 20 products using chromatography. In contrast, Chinese plasma-derived product manufacturers exhibit relatively low levels of plasma purification and comprehensive utilization; leading-tier companies can isolate only 10–12 products, while average companies manage merely 3–4. Tiantan Biological, Shanghai RAAS, and Hualan Biological Engineering belong to the first tier and boast the most comprehensive product portfolios.

Revenue per ton of pulp:The average revenue per ton of plasma for blood products is approximately RMB 2.5 million; Boya Bio-pharmaceutical Group achieves the highest revenue per ton of plasma, as its minor product portfolio is concentrated in fibrinogen.

Profit per Ton of Pulp:Hualan Biological Engineering and Boya Bio-Pharmaceutical achieved a profit per ton of plasma of RMB 900,000 in 2021, whereas Tiantan Biological Products and Pailin Biopharma reported figures below RMB 600,000. This significant disparity stems from differences in the number of approval licenses and specialized product portfolios. According to disclosures by listed companies, based on current market prices, Prothrombin Complex Concentrate (PCC) and Human Coagulation Factor VIII are expected to increase profit per ton of plasma by 30%–40%.

Figure 9: Product Portfolio of Blood Plasma-Derived Therapeutic Companies

Source: Company announcements, CICC Research Department

Yield Improvement:For various reasons, certain blood product manufacturers have failed to ensure effective supply of their products. For instance, some companies hold marketing authorizations for their products but choose not to manufacture or supply them due to low yields and economic unviability caused by outdated equipment, obsolete processes, or inadequate quality control, resulting in a waste of valuable resources.

● Strengthen process control without upgrading technology: No administrative approval required; yields improve immediately, but the potential for improvement is limited.

● Change in manufacturing process: Submission for CFDA approval upgrade is required, taking approximately one year.

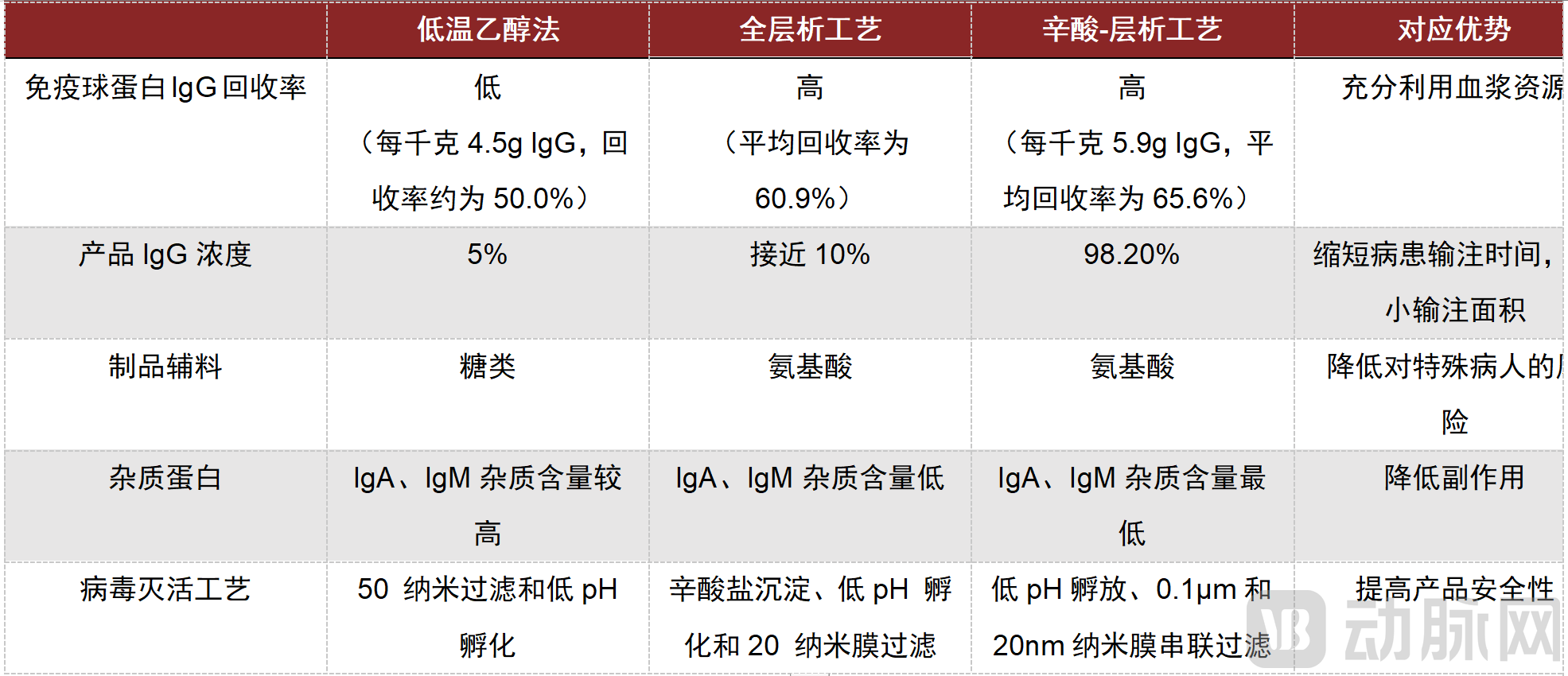

According to the 2022 annual reports of various companies, most domestic blood product manufacturers are still in the stage of producing blood products using the cold ethanol fractionation method. The purification process based on chromatography technology is currently less utilized, resulting in a gap compared with leading overseas companies. Therefore, we believe that plasma extraction technology is the core factor determining the production efficiency of blood product enterprises.

According to expert consultations, the 10% concentration chromatographic intravenous immunoglobulin (IVIG) is expected to be priced at RMB 1,900 (compared to the listed terminal price of RMB 1,200 for conventional IVIG). The estimated volume for 10% chromatographic IVIG in 2023 is 1 million bottles. Between 2028 and 2030, it is projected that 7–8 manufacturers will transition to the chromatography method, with domestic IVIG products expected to be fully upgraded by 2030.

Figure 10: Comparison of IVIG Preparation by Cold Ethanol Fractionation and Chromatography

Figure 10: Comparison of IVIG Preparation by Cold Ethanol Fractionation and Chromatography

Source: Company communications; Xing Yantao et al., Preparation and Analytical Testing of 10% Intravenous Immunoglobulin Using Full Chromatography Process, CICC Research Department

Figure 11: Yield of Major Products per Ton of Plasma

Source: Company communications, CICC Research Department

V. Demand Side: As physicians’ understanding of blood products improves, clinical usage will continue to increase

IVIG:Over the next two years, the supply-demand imbalance for intravenous immunoglobulin (IVIG) will gradually shift from "shortage" to a "tight balance": Recently, various regions have once again witnessed peaks in respiratory infections, leading to a renewed surge in clinical demand for IVIG. Coupled with "zero inventory" levels at the distribution channel level, IVIG continues to face a situation where supply falls short of demand.

● Price: Ex-factory price RMB 480–550 per bottle; hospital price RMB 560–620 per bottle

● Ratio: In-hospital to out-of-hospital = 1:1, whereas the in-hospital share was previously higher (60–70%). Of the out-of-hospital portion, less than 20% will be subject to competitive bidding.

Albumin:Human albumin is widely used in clinical practice, with the most significant applications in intensive care units (ICUs) and surgical departments. From January to August 2023, the clinical demand for human albumin remained in a state of “tight balance,” with hospital-side demand increasing by 21.34% year-on-year during this period.

● Price: Ex-factory price RMB 330–350/bottle; hospital price RMB 400–420/bottle

● Ratio: In-hospital : Out-of-hospital = 6:4; Imported : Domestic = 6:4.

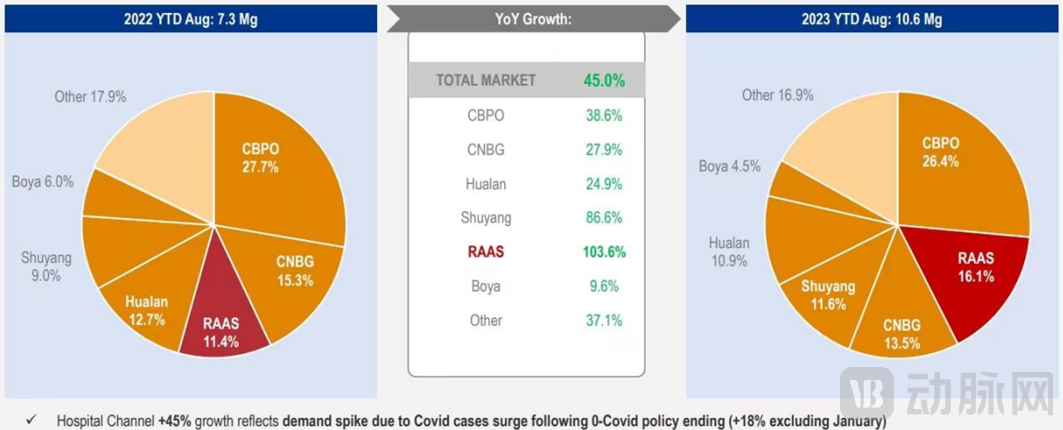

Figure 12: Sales Share and Year-on-Year Change of Intravenous Immunoglobulin (IVIG) in the Hospital Sector

Source: Public information

Figure 13: Sales Share and Year-on-Year Change of Albumin in the Hospital Sector

Source: Publicly available information

VI. Conclusion

This article systematically analyzes the global and domestic market size, supply-demand dynamics, and growth potential of the blood products industry, deconstructing its core variables and key elements from a structural framework to uncover the underlying drivers of industry growth. With rising physician awareness of blood products, steady and orderly expansion of plasma collection stations, and increasing market concentration among leading players through industry consolidation, we believe this sector represents a “long slope with deep snow” opportunity—a track conducive to sustained, compounding growth—and is poised to cultivate one or two dominant, high-quality oligopolistic enterprises with strong comprehensive capabilities.

Risk Disclosure: The areas of focus and research discussed herein represent only the key sectors currently selected by the fund manager based on market conditions and do not necessarily indicate future investment directions. The fund manager reserves the right to select investment targets that comply with contractual requirements in response to market changes, with actual investment practices prevailing. Donghai Fund Management Co., Ltd. (hereinafter referred to as “the Company”) and its related entities, employees, or agents shall not bear any liability for any person’s use of all or part of this content, nor for any losses arising therefrom. Without prior permission from the Company, no person may distribute, reproduce, reprint, or publish this content or any portion thereof in any form, nor make any deletions or modifications to this column that contradict its original intent. The Company commits to managing and utilizing fund assets in accordance with the principles of honesty, good faith, and due diligence; however, it does not guarantee that the fund will generate profits or ensure a minimum return. Investors should carefully read relevant documents, including the fund contract, prospectus, and key facts statement of the fund product, and select investment products suitable for their risk tolerance when investing in the Company’s funds. Given the relatively short operating history of funds in China, past performance may not reflect all stages of development. The information provided is for reference only and does not constitute investment advice. Funds involve risks; please invest with caution.