2023 White Paper on Innovative Drugs and Supply Chain: Analysis of Nearly 400 Financing Events, Over 100 Clinical Pipelines, and BD/M&A Activities

2023 was a year filled with challenges and transformations for China's biopharmaceutical industry.

The challenge lies in the tightening of IPOs and the persistently sluggish financing environment, which have left many companies in the industry grappling with strained or even broken capital chains. Meanwhile, their drug pipelines remain critically underfunded, all while facing fierce market competition. Yet, encouragingly, numerous positive shifts are underway.

For instance, in terms of policy, the impact of cost-containment measures such as centralized procurement and national reimbursement drug list adjustments gradually softened in 2023, while support for innovative drugs was strengthened. In the area of global expansion for innovative drugs, Toripalimab, a PD-1 monoclonal antibody developed by Junshi Biosciences, received approval from the U.S. FDA, becoming the first self-developed and domestically produced innovative biologic from China to be approved in the United States. This milestone marks a new level of internationalization in China’s innovative drug research and development.

Out-licensing deals are becoming a critical source of cash flow for Chinese biotech companies. Both domestic licensing collaborations and cross-border out-licensing transactions reached new highs in 2023, with antibody-drug conjugates (ADCs) leaving a significant mark on the history of license-out deals by Chinese pharmaceutical companies.

For China’s biopharmaceutical sector, 2023 was a year of subdued market sentiment, yet also an inspiring one.

To gain a comprehensive understanding of the performance across all aspects of China’s primary biopharmaceutical market and to better grasp the industry’s development trends in 2024, VCBeat hasIn 2023, nearly 400 financing deals and close to 100 clinically approved pipelines in China’s innovative drug and supply chain sectorsandNearly 100 BD Deals/M&A TransactionsA detailed retrospective study was conducted to benefit the industry.

2023 in Numbers: Industry Challenges and Transformation Amid the Capital Winter

1Investment and Financing: Total funding continues to halve; the trend of favoring early-stage and small-scale investments is no longer prominent, while upstream supply chain projects are increasingly favored by capital.

Annual Changes in Total Financing Amount in China's Biopharmaceutical Sector from 2019 to 2023

Data Source: VBInsight, VCBeat

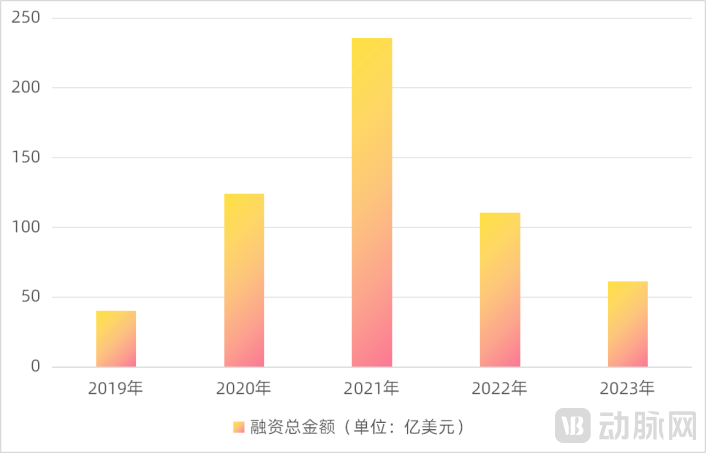

The capital winter persists, with the primary market growing even colder.According to incomplete statistics from VBInsight, the total financing amount in China's biopharmaceutical sector in 2023 was $6.159 billion, approximately half of the 2022 total ($11.056 billion) and one-quarter of the 2021 total ($23.595 billion).

Year-on-Year Changes in Average Financing Amount and Number of Financing Events in China’s Biopharmaceutical Sector, 2019–2023

Data source: VBInsight, VCBeat

In terms of the average financing amount and the number of financing events, the number of financing events in China’s biopharmaceutical sector in 2023 (514) fell to the 2020 level (534), while the average financing amount ($12 million) dropped to the 2019 level ($11 million).

Based on research interviews, VCBeat believes that the continued cooling of financing in the biopharmaceutical sector in 2023 was driven not only by global macroeconomic factors such as geopolitical tensions and U.S. interest rate hikes, but primarily by a combination of internal and external factors.

Internal CausesThis stems from the previously overheated biopharmaceutical market, where most projects were overvalued but subsequently failed to meet expectations, leading the industry to undergo a valuation reassessment.

External CausesThe main factors are twofold: 1) The tightening of IPO approvals in 2023, along with stringent policy controls on share reductions and refinancing, has transmitted financing pressures upstream; 2) Anti-corruption campaigns in the healthcare sector have further impacted industry development.

The phenomenon of investing in early-stage and small-scale ventures persists, but the growth trend is no longer pronounced.A clear trend in the performance of industrial capital in the 2022 investment and financing market was a focus on early-stage and small-scale investments; however, this prominent phenomenon did not continue in 2023. Early-stage investment and financing activities in 2023 have fallen back to approximately 60% of normal levels.

Proportion of Early-Stage Investment and Financing Events in China, 2019–2023

Data Source: VBInsight, VCBeat

Some investors have explained the reasons behind this phenomenon. Before mid-2021, due to an overheated capital market, many projects were overvalued while their actual business progress failed to keep pace. In search of projects with more reasonable valuations, numerous investors turned their attention to “underwater” projects that had never raised funding or to early-stage companies that had completed only one round of financing.

ButAmid the global downturn in the biopharmaceutical development cycle and shifts in China’s domestic policy landscape, the timing of the end of this downturn has become increasingly uncertain.. The originally anticipated two- to three-year downturn cycle might have allowed early-stage projects to navigate through successfully; however, as the expected end date of the downturn extends into a longer time horizon, the additional advantages of investing in early-stage and small-scale ventures are no longer present.

Companies capable of self-sustaining operations and maintaining stable cash flows have a greater chance of surviving the capital winter, making them the preferred investment targets for most institutional investors in the current market.

This has given rise to another characteristic of investment and financing in the biopharmaceutical sector in 2023:Project financing in the upstream supply chain is relatively active.

According to incomplete statistics from VCBeat Research Institute, in 2023, upstream supply chains such asTotal Financing Amount in the CXO and Innovative Drug Raw Material Supply Sectors(30.14 billion yuan)Total Financing for Fast-Follow and Innovative Drug R&D(36.33 billion yuan), CXO and innovative drug raw material supply projectsAverage Financing Amount(RMB 220 million and RMB 210 million, respectively)Far Exceeds Innovative Drug R&DProject (RMB 140 million).

2023 Overview of Investment and Financing Performance in China’s Innovative Drug Sector and Supply Chain

Data Source: VBInsight, VCBeat

In recent years, with the China-US trade war and the outbreak of the COVID-19 pandemic,Supply Chain Securityimportance has been elevated to an unprecedented level. In addition, upstream supply chain projects haveRelatively low investment risk, relatively short investment cycle, relatively high industry entry barriers/technical barriers, substantial market space, and less intense competitionSuch characteristics are another reason why capital favors this type of project.

In addition to domestic substitution, many upstream supply chain enterprises in China that experienced rapid growth during the pandemic have already established technological advantages, and even possess the capabilityExpanding Overseas to Compete in the International Market, which provides the market with greater room for imagination.

Although the contraction in the downstream innovative drug R&D sector will inevitably impact upstream development, overall, upstream supply chain projects remain relatively resilient within a shrinking market, and structural opportunities still exist.

2IPO: Number of Listings Drops to Levels Seen Five Years Ago, Frequent Policy Releases from the Beijing Stock Exchange Bring New Vitality to the IPO Market

With IPO policies tightening and scrutiny intensifying, the number of initial public offerings in the biopharmaceutical sector fell in 2023 to levels last seen in 2019. According to incomplete statistics from VBInsight,Number of IPOs in the Biopharmaceutical Sector in 2023(27 cases)Fall to the 2019 IPO Volume(27 cases)level, marking the 2021 peak for initial public offerings (IPOs) of biopharmaceutical companies(54 cases)half of the time.

Number of IPOs in the Biopharmaceutical Sector, 2019–2023

Data Source: VBInsight, VCBeat

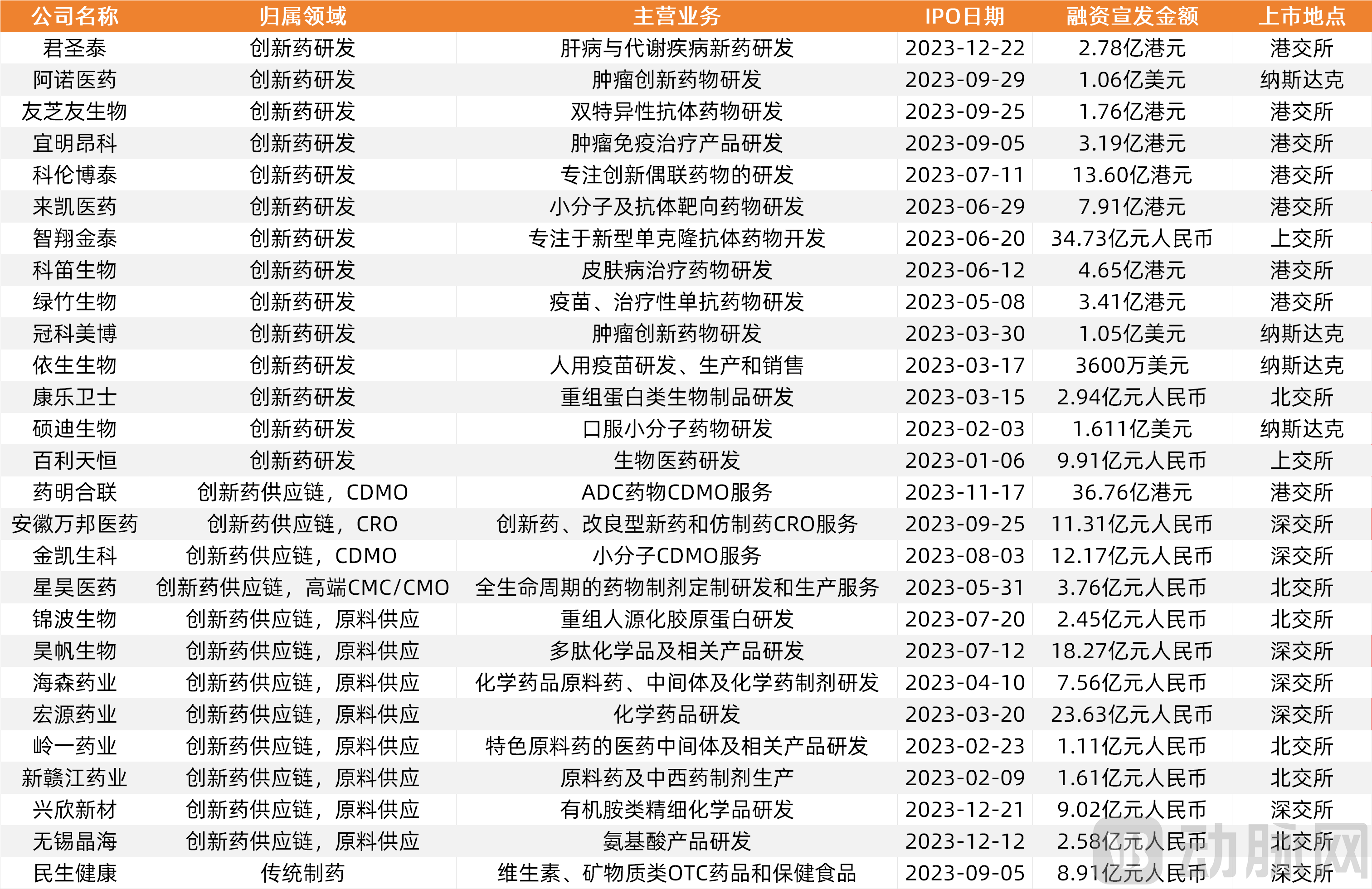

27 pharmaceutical companies successfully listed, raising up to RMB 3.47 billion.According to incomplete statistics from VCBeat, a total of 27 Chinese pharmaceutical companies went public in 2023, among which eight raised over RMB 1 billion in their initial public offerings.

Overview of IPOs in the Pharmaceutical Sector in 2023

Data Source: VBInsight, VCBeat

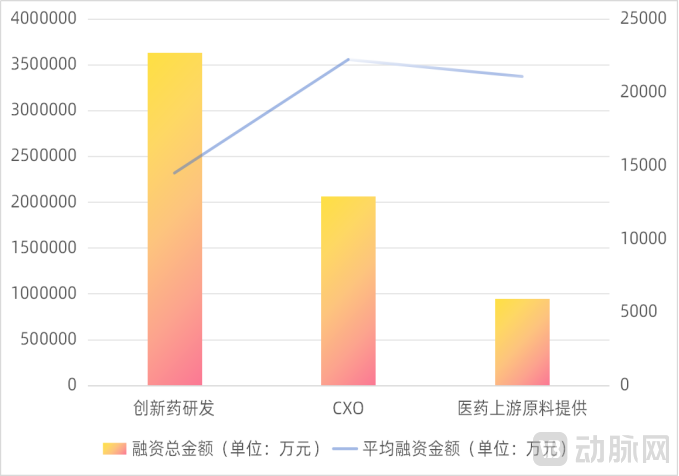

The average funding amount for upstream supply chain IPO projects is higher than that for innovative drug R&D projects.Innovative drug R&D projects had a higher number of IPOs (14 cases), but innovative drug upstream supply chain projects achieved higher average fundraising amounts. For instance, the average IPO fundraising amount for projects in the upstream CXO sector reached RMB 1.526 billion, while that for projects in the upstream raw material supply sector (RMB 946 million) was also higher than that for innovative drug R&D projects (RMB 795 million). Among the eight pharmaceutical companies with public fundraising exceeding RMB 1 billion, five belonged to the innovative drug upstream supply chain sector.

2023 IPO Landscape for Upstream and Downstream Sectors in the Innovative Drug Industry

Data Source: VBInsight, VCBeat

All 27 pharmaceutical IPOs fell within the small-molecule chemical drug and biologic macromolecule sectors; Top 2 Pharmaceutical IPOs(WuXi XDC, ZhiXiang JinTai)All-in on the Antibody Drug Race.

Statistics on the Sub-sector Classification of IPO Companies in the Pharmaceutical Sector in 2023

Data source: VBInsight, VCBeat

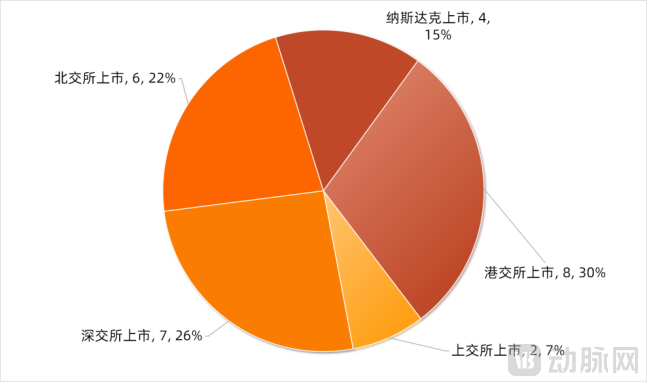

Policy Tightening on the STAR Market Enters an Uncertain Phase, While Frequent Policy Releases from the Beijing Stock Exchange Inject New Vitality into the IPO Market.In 2023, the STAR Market, which had originally carried high expectations for the biopharmaceutical sector, entered a period of uncertainty amid policy-driven tightening. With IPO thresholds raised on the Shanghai and Shenzhen stock exchanges as well as in overseas markets due to various factors, the Beijing Stock Exchange (BSE) has emerged with distinct advantages, including high inclusivity, a compact and controllable timeline, and rapid review processes. It has provided a new listing option for a large number of innovative small and medium-sized enterprises (SMEs), becoming both a new direction and a primary venue for their public listings.

2023 Distribution of IPO Locations for Domestic Innovative Drug and Supply Chain Companies

Data Source: VBInsight, VCBeat

In 2023, the Beijing Stock Exchange intensified its reform efforts to optimize listing system arrangements.The rules were successively revised to shorten the fund freeze period for new share subscriptions, abolish issuance pricing, and optimize the transfer listing system.Further streamlining diverse and convenient listing pathways has become one of the choices increasingly adopted by companies in their IPO planning.In particular, it has attracted significant attention from leading enterprises in specialized, refined, distinctive, and innovative (“SRDI”) niche sectors, as well as high-revenue companies facing challenges on their path to going public, signaling promising prospects for expansion and quality improvement.

According to incomplete statistics from VCBeat,In 2023, six pharmaceutical companies were listed on the Beijing Stock Exchange,Including Kangleyiwei, Xinghao Medicine, Jinbo Biopharma, Lingyi Pharmaceutical, Xin Ganjiang Pharmaceutical, and Wuxi Jinghai. Among them,There are numerous cases of companies that were rejected by the STAR Market but successfully listed on the Beijing Stock Exchange.For instance, Jinbo Bio, a collagen product developer that successfully listed on the Beijing Stock Exchange (BSE) in July 2023, chose the BSE after being rejected by the STAR Market, ultimately achieving a successful IPO and witnessing a significant surge in its stock price post-listing.

Currently, under the guidance of the China Securities Regulatory Commission (CSRC), the Beijing Stock Exchange is accelerating the formulation of relevant institutional rules for direct initial public offerings (IPOs) on the exchange, with more opportunities expected in 2024.

Multiple senior industry experts have pointed out that the state's long-term policy guidelines will undoubtedly provide strong encouragement for the development of the biopharmaceutical industry,Strict control over IPOs is a phased, short-term measure and will not be maintained in the long run.Historically, the A-share market has experienced eight IPO suspensions.

During the IPO tightening cycle, actively explore new opportunities on the Beijing Stock Exchange or seek exit routes through secondary share transfers and M&A.

3Over 200 Policies: Revitalizing Traditional Chinese Medicine, Promoting Innovative Drug Development and Enhancing Clinical Quality, and Regulating Online Drug Sales

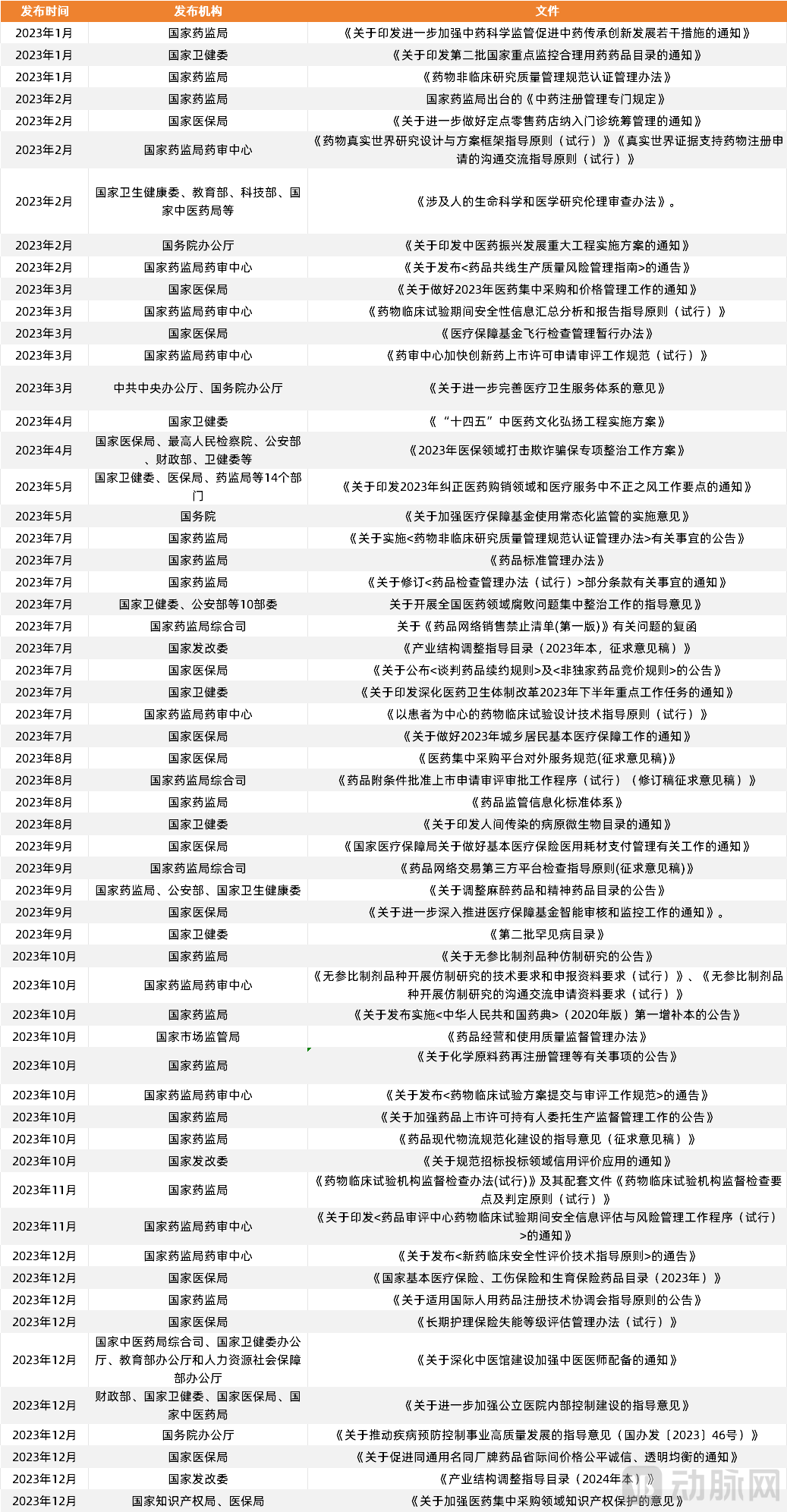

In 2023, more than 200 policies related to the pharmaceutical industry were issued at the national level, and approximately 1,400 relevant policies were released at the provincial level. By category, health insurance-related policies accounted for the largest proportion in 2023, nearing half of the total, followed by policies concerning medical services, pharmaceuticals, and healthcare reform.

A Review of Key National Policies in the Biopharmaceutical Sector in 2023

Data source: Collected and compiled from public news channels, VCBeat

Due to space constraints, a detailed elaboration is not provided here; the report interprets selected policy highlights of note, including:

1. The state has issued multiple policy documents to promote the revitalization and development of Traditional Chinese Medicine (TCM).

2. The impact of cost-containment policies, such as volume-based procurement and national reimbursement drug list adjustments, is gradually moderating, while support for innovative drugs is being strengthened.

3. Accelerate the review and approval of innovative drugs, with increased attention given to pediatric medicines and drugs for rare diseases.

4. Further tightening of approval for fast-follow drugs.

5. Standardize online drug sales and online transactions.

6. The revised Catalogue for Guiding Industrial Structure Adjustment features a more focused list of encouraged sectors.

7. Anti-corruption in the healthcare sector.

8. Strengthen the supervision of medical insurance funds.

9. Promote the improvement of clinical trial quality.

10. Strengthen pharmaceutical patent protection and optimize the system of primary responsibilities for Marketing Authorization Holders (MAHs).

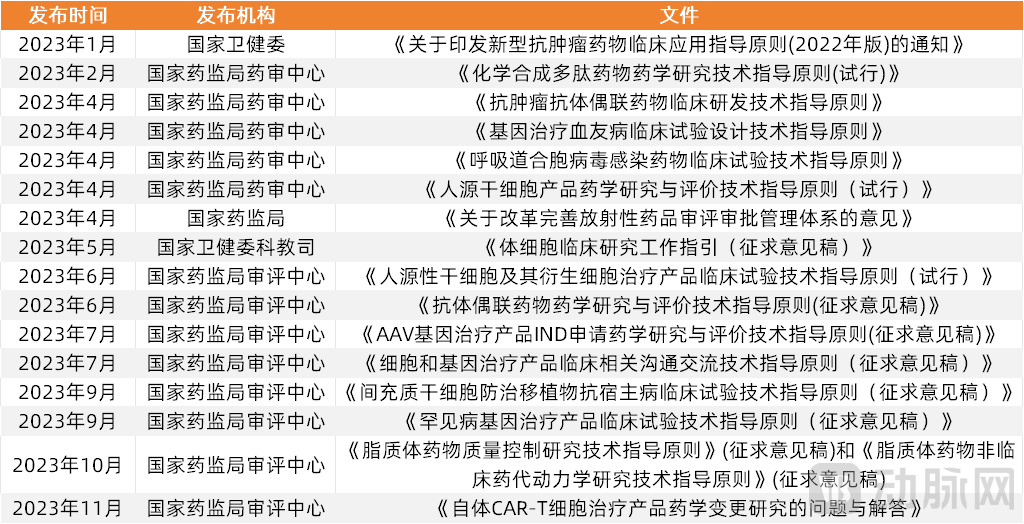

Furthermore, to guide the clinical trial design of innovative drug products across various therapeutic areas, standardize the rapid development in related fields, and enhance the quality and efficiency of communication between applicants and regulatory authorities, China issued multiple policies in 2023 targeting, includingNovel Anti-Tumor Drugs, Peptide Drugs, Antibody-Drug Conjugates, Liposomal Drugs, Cell Therapies, Gene Therapy Drugs...and other clinical research guidelines for various drug categories.

Clinical Research Guidelines Issued in China for Various Subsectors of Biopharmaceuticals in 2023

Data source: Compiled from public news channels, VCBeat

Interpretation of Innovative Tracks in Niche Segments of Innovative Drugs and the Supply Chain

1Antibody Drugs and Radiopharmaceuticals See Counter-Trend Growth in Financing; High Yield in Radiopharmaceutical R&D with Nearly 20 Pipeline Candidates Approved for IND

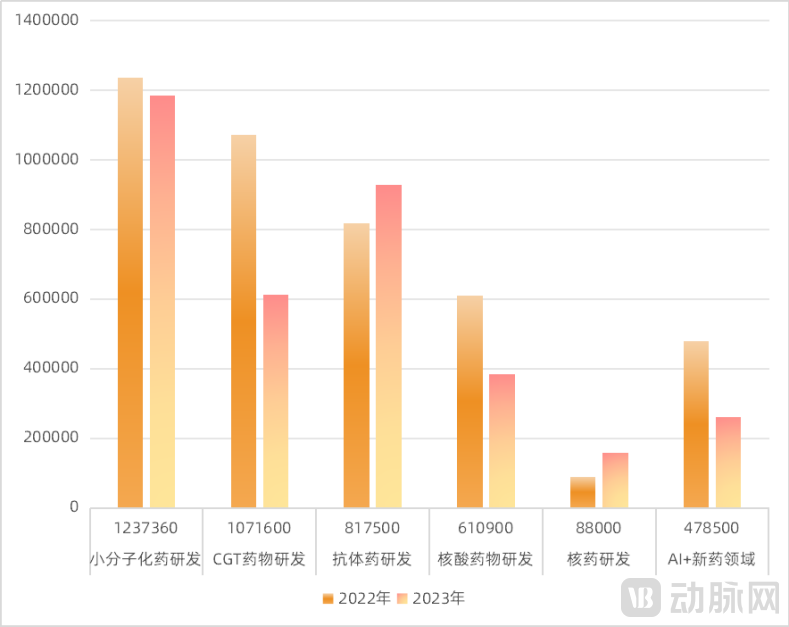

Compared with 2022, only the antibody drug and radiopharmaceutical segments within the innovative drug sector achieved counter-trend financing growth in 2023.Overall, financing activity in the small-molecule chemical drug sector remained largely unchanged, essentially on par with 2022 levels. The shifts in financing enthusiasm across various subsectors of innovative drug R&D reflect a risk-averse sentiment in the capital markets.

Comparison of Investment and Financing in Various Sub-sectors of Innovative Drugs in 2022 and 2023 (Unit: RMB 10,000)

Data Source: VBInsight, VCBeat

Small-molecule chemical drugs and antibody therapeutics represent relatively mature tracks within the innovative drug sector. The industry has a comprehensive understanding of these areas, the market potential is substantial, and numerous project pipelines have advanced to the mid-to-late stages of clinical development. Consequently, financing performance in these two sectors has been relatively stable. In 2023, six and five innovative drug companies specializing in small-molecule chemical drugs and antibody therapeutics, respectively, completed their initial public offerings (IPOs).

Overall, the projects that secured substantial financing against the trend in the small-molecule chemical drug and antibody drug sectors in 2023 shared common characteristics, mostly beingPossesses core technology platforms, features a sufficiently differentiated product pipeline, ranks among the market leaders in clinical development progress, and demonstrates steady advancement in clinical trials with robust clinical data..

Taking Tianchen Bio, an antibody-based therapeutics company, as an example, the company has developed a diverse product pipeline leveraging its three independently developed technology platforms (Sundoma, InCibitor, and NeXine). Currently, three Class I innovative drug candidates have entered clinical trials. Among them, LP-003, indicated for allergic rhinitis and chronic urticaria, has advanced to Phase II clinical trials and is expected to enter Phase III clinical trials sequentially in 2024.

According to the Phase I clinical data of LP-003 presented by the company at the 2023 European Rhinology Society Conference, LP-003 demonstrates higher affinity and superior biological activity compared to omalizumab, the first-generation global anti-IgE antibody. This suggests potential for enhanced efficacy, allowing for reduced dosage. Additionally, its longer half-life enables less frequent administration, thereby improving patient compliance. The company’s complement drug candidate, LP-005, also completed dosing of the first patient in its Phase I clinical trial by the end of 2023. Following the completion of Series A+1 and A+2 financing rounds in 2022, Tianchen Biopharma continued to buck the trend in 2023 by securing over RMB 100 million in Series B1 financing.

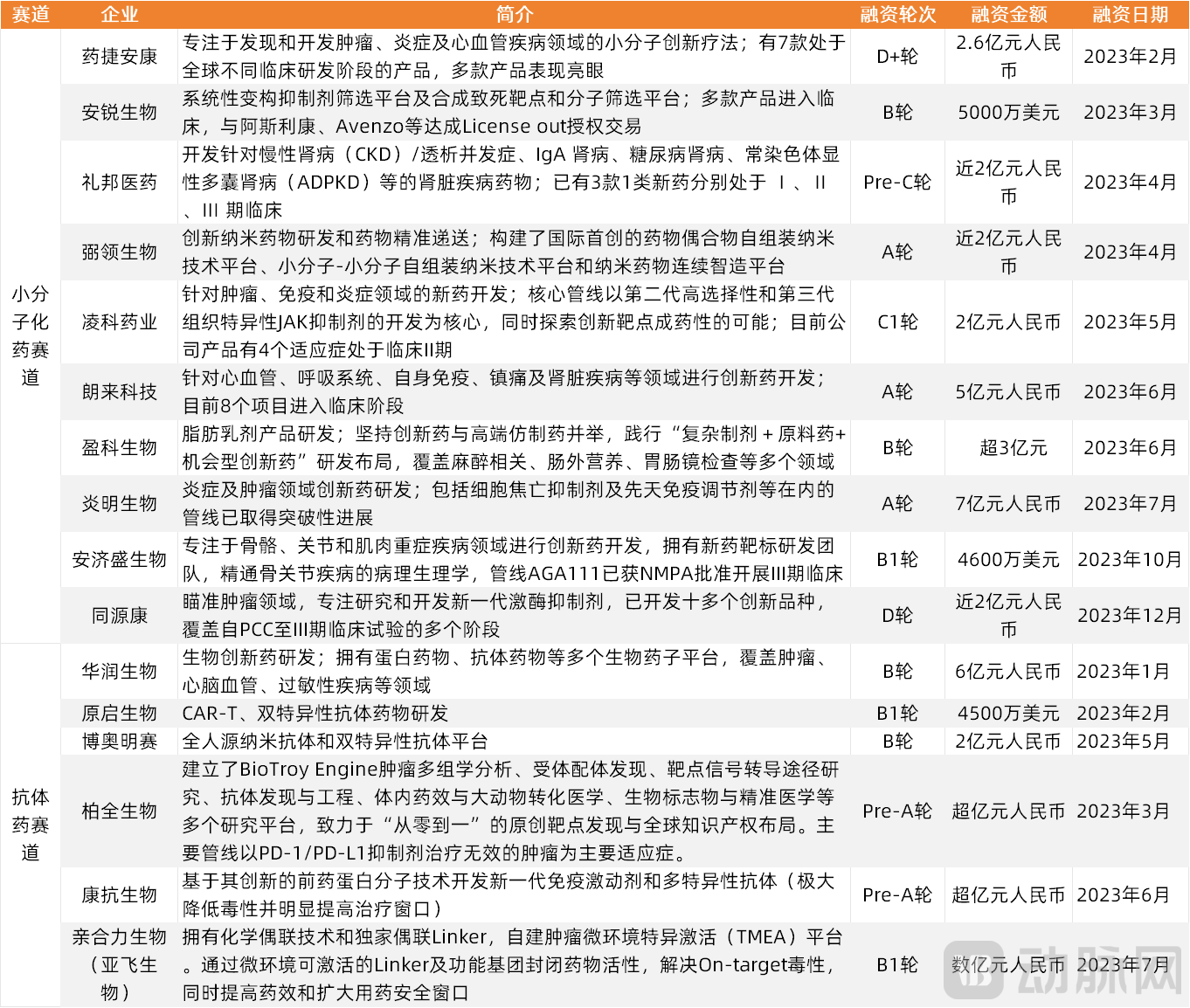

VCBeat has compiled detailed information on the top 10% of projects by funding amount in the small-molecule drug and antibody drug R&D sectors (excluding IPOs; in cases of equal funding amounts, projects with earlier financing rounds are prioritized for display; this criterion applies to similar comparisons hereinafter without further notice) for industry reference.

Top 10% of Projects in the Small-Molecule Chemical Drug and Antibody Drug R&D Sectors by Financing Amount in 2023

Data sources: VBInsight, public reports from various companies, VCBeat.

It can be observed that, in terms of project types, large-scale financing projects in the field of small-molecule chemical drug R&D are mostly focused on the development of new drugs for cardiovascular diseases, autoimmune disorders, inflammatory conditions, and renal diseases, with someDrug DeliveryTechnologically distinctive projects such as Biling Bio and Yingke Bio have also been favored by capital. In the antibody drug sector, indications remain primarily concentrated in the fields of oncology and autoimmune diseases.Bispecific Antibodies, Polyclonal Antibodies, ADCsThe drug project’s potential is viewed favorably.

The nuclear medicine sector has seen the most dramatic surge in investment and financing, with the total amount rising approximately two-fold compared to 2022.From a previously niche sector to a fiercely contested battleground for major pharmaceutical companies, the radiopharmaceutical market continued to heat up in 2023.

The commercial success of Lutathera and Pluvicto has ignited global pharmaceutical companies’ enthusiasm for entering the radiopharmaceutical sector. Overseas pharmaceutical giants are continuously increasing their investments, while numerous Chinese pharmaceutical companies are rushing to join the fray, driving sustained growth in the popularity of radiopharmaceuticals. According to incomplete statistics from VBInsight, there were 10 financing events in the radiopharmaceutical field in 2023, with a total financing amount of RMB 1.58 billion. The number of financing events and the total financing amount increased by 42.9% and 79.8% year-on-year compared to 2022.

Financing Landscape in the Radiopharmaceutical Sector in 2023

Data Source: VBInsight, VCBeat

Among them,Xiantong Medicine single-handedly boosted the financing momentum across the entire nuclear medicine sector in 2023.Secured over RMB 1.1 billion in substantial financing in July 2023, backed by a diverse group of investors, including nearly 20 state-affiliated funds, industrial conglomerates, and renowned investment institutions.

In 2023, Xiantong Medicine also demonstrated outstanding business performance. Its first approved radiopharmaceutical product, Ouning® (Florbetaben [18F] Injection), received marketing approval from the Center for Drug Evaluation (CDE) in September 2023, becoming the first Aβ-PET imaging agent approved in China for the diagnosis of Alzheimer’s disease (AD). This product has a disruptive impact on AD diagnosis, reportedly enabling detection up to 15 years earlier. Moreover, it is the first positron emission tomography (PET) imaging agent approved in China in nearly two decades, providing significant encouragement to the domestic radiopharmaceutical sector, which has experienced slow growth over the long term.

In 2023, radiopharmaceuticals also demonstrated remarkable performance in terms of clinical approvals.According to incomplete statistics from VCBeat, a total of in 202316 Radiopharmaceutical Pipelines Approved for IND, companies such as Nuoyu Pharma, Xiantong Medicine, and Dongcheng Lannacheng have also seen their pipelines successively reach the stage of IND application acceptance by the end of 2023.

In terms of targets and indications, many domestic R&D pipelines for radiopharmaceutical-drug conjugates (RDCs) are benchmarked against Novartis’s two approved products, developing either generic or improved novel drugs. PSMA and SSTR are hot targets in radiopharmaceutical development, with numerous pipelines focused on prostate cancer and neuroendocrine tumors.

2023 IND Approvals for China’s Nuclear Medicine Pipeline

Data Source: Compiled from publicly available information across various channels, VCBeat.

Currently,China’s innovative radiopharmaceuticals are in a phase of rapid development, progressing from 0 to 1.To mitigate development risks, target clustering and pipeline homogenization are inevitable.

In the future, key attention should be focused onInnovation in radiopharmaceutical targets, indications, and radionuclides; focus on upstream and downstream supply chain collaboration, as well as synergies between radiopharmaceutical companies and ADC/PDC developers; monitor the development of the radiopharmaceutical CRO/CDMO sector.Both in China and overseas, the research, development, and production of radiopharmaceuticals have entered a period of high output.

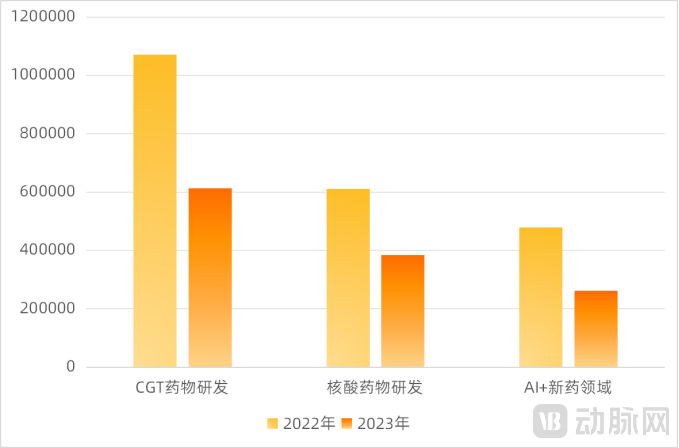

2CGT and AI-driven new drug financing show signs of cooling, while small nucleic acid therapeutics buck the trend with 17 candidates entering clinical trials, on the eve of a commercial explosion

Compared with the investment and financing fervor in 2022, the CGT R&D capital market entered a cooling-off period in 2023.According to incomplete statistics from VBInsight, the industrial think tank of VCBeat, there were 67 financing and investment events in the CGT drug R&D sector in 2023, with a total financing amount of RMB 6.134 billion. Compared with 2022, the number of financing events in the CGT drug R&D sector decreased by 30.2% year-on-year, the total financing amount dropped by 42.8% year-on-year, and the average financing amount declined by 19.7% year-on-year.

Comparison of Investment and Financing in CGT, Nucleic Acid Drugs, and AI-Driven New Drug R&D in 2022 and 2023 (Unit: 10,000 Yuan)

Data Source: VBInsight, VCBeat

Regarding the cooling of financing for CGT drug development, some investors have pointed out that there are multiple factors, mainly influenced by the current capital environment.

First, the current field of CGT drug development is in a relatively early stage. Many therapies that once held great promise, such as those for treating solid tumors and universal cell therapies, have yet to achieve substantial breakthroughs in China. Due to safety risks and other issues, clinical trials for similar products abroad have frequently encountered setbacks, and technologies such as stem cell therapy remain immature. From a technical perspective, the risks associated with CGT drug development are currently relatively high. Given that most capital investors are currently prioritizing stability, enterprises are facing significantly greater difficulties in securing financing.

Furthermore, certain CGT sectors that have reached successive stages of maturity, such as cell therapy for hematologic malignancies and gene therapy for ophthalmic and rare diseases, are currently facing challenges including homogenized competition and market saturation. Given the substantial R&D investments and high pricing associated with CGT drugs, coupled with the limited payment capacity of patients in China and the difficulty for the national medical insurance system to absorb these costs, domestic commercial insurance has not yet provided comprehensive coverage. Consequently, domestic investors hold a less optimistic outlook on the future market prospects of the CGT sector in China.

Regardless of overall market sentiment, the projects that secured financing in the capital markets in 2023 clearly indicated the industry’s strategic direction, demonstrating that investors continue to recognize the value and future growth potential of CGT therapies.

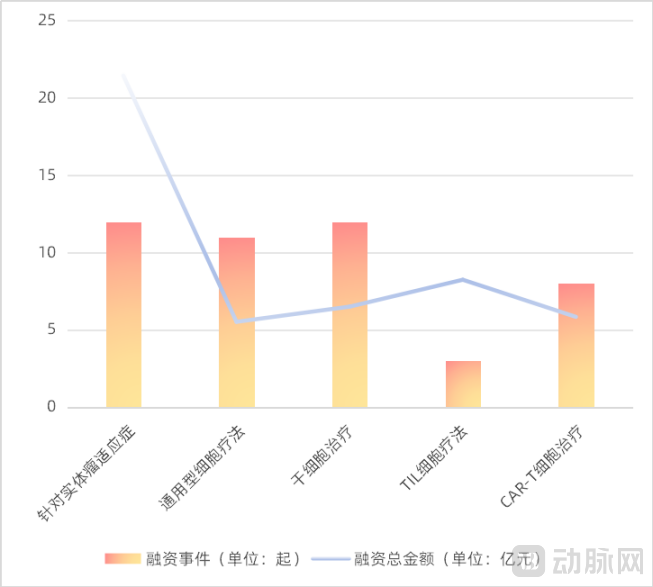

Cell Therapy Drug Development,According to incomplete statistics from VCBeat Research Institute, in 2023, the field of cell therapy research and developmentA total of 46 financing events occurred, with a total financing amount of RMB 3.756 billion.

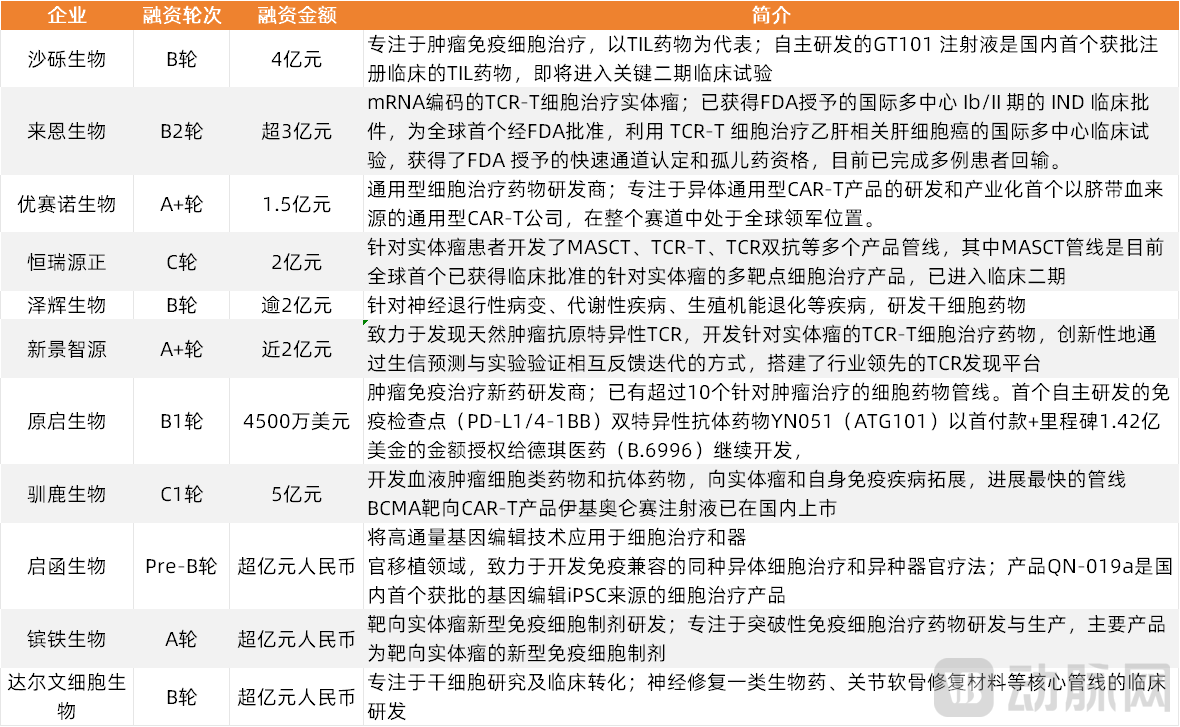

Among them, Huasaiboman, Yuanqi Bio, and Gravel BioThree Companies Developing TIL Cell Therapy Drugs Secured a Total of RMB 824 Million in Financing; including Reindeer Biotech, Lion Biologics, Hengrui Yuanzheng, Xinjing Zhiyuan, and others12 cell therapy drug developers targeting solid tumor indications secured RMB 2.144 billion in financing.

including Ucella Bio, BaseBio, and others11 Companies Targeting the Development of Universal Cell Therapy Drugs Secure 552 Million Yuan in Financing; including companies such as Zehui Biologics, Qihan Biotech, Anling Biotech, and Darwin Cell Biology, which utilizeStem Cell TechnologyTargeting oncology, neurodegenerative diseases, anti-aging, organ transplantation, and articular cartilage repair materials12 companiesCell Therapy CompaniesSecured RMB 650 Million in Financing. There were 8 financing deals related to CAR-T cell therapy, totaling RMB 584 million, of which 5 involved the development of universal CAR-T products or targeted solid tumor indications.

Cell Therapy R&D in 2023: Enterprise Types Favored by Capital and Their Financing Performance

Data Source: VBInsight, VCBeat

Top 20% Funded Projects in the Cell Therapy Drug Development Sector9 cases involving solid tumors or universal types, and 2 cases related to stem cells.

Top 20% of Projects in the Cell Therapy R&D Sector by Funding Amount

Data sources: VBInsight, corporate public reports, VCBeat.

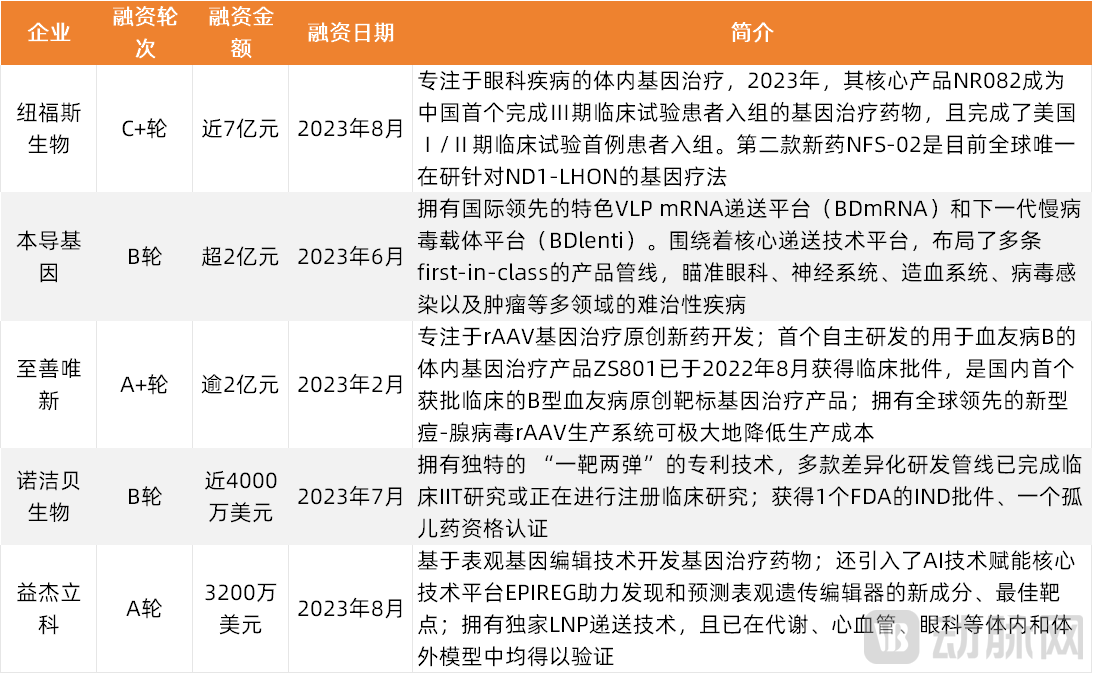

Gene Therapy Drug Development,According to incomplete statistics from VCBeat, in 2023, the field of gene therapy drug developmentA total of 21 financing events occurred, with a total financing amount of RMB 2.57 billion.

including Nuofus Biotech, Shenxi Biotech, Zhishan Weixin, and Nuojebei BiotechEleven companies developing gene therapy drugs via the AAV route secured RMB 1.518 billion in financing,Most companies primarily focus on disease areas such as metabolism, CNS, and ophthalmology, while others target conditions like hemophilia B (Zhishan Weixin) and inner-ear hearing loss (Xingao Tuowei).

including RayWind Biotech, Base Therapeutics, Yijie Lico, and Yaotang BiologicsSix companies developing gene therapy drugs based on gene-editing technology secured RMB 602 million in financing.

Notably, Base Therapeutics and EpiGene, two startups developing gene therapies based on cutting-edge base editing and epigenetic editing platforms, deserve attention; they secured significant funding rounds of tens of millions of USD and $32 million, respectively, in 2023.

Prime Editing/Base Editing/Epigenetic Editing Companies That Secured Financing in the Past Two Years

Data Source: VBInsight, VCBeat

BaseBio’s core base editing technology offers advantages such as “zero off-target” effects, high targeting efficiency, and a compact size, providing significant benefits in enhancing the safety and efficacy of clinical applications for both in vivo and in vitro gene editing. This technology enjoys freedom to operate (FTO) in China, Europe, and the United States.

EpiReg, Yijielike’s core technology platform, leverages a CRISPR-Cas-derived epigenetic editing system to precisely modify epigenetic marks at any genomic locus without cleaving DNA, thereby avoiding issues such as off-target effects, short half-life, and poor patient compliance.

These cutting-edge gene-editing technologies have unlocked vast potential for the industry, attracting significant attention from investors over the past two years.

Top 5 Gene Therapy Drug R&D Projects by Funding Amount

Data sources: VBInsight, public reports from various companies, VCBeat.

CGT drug development funding cools as technical hurdles recede; global project initiation gains favor with capital.Multiple investors believe that,The primary cause of the current winter in the CGT sector stems from external objective environmental factors, rather than limitations in technological development itself.

For instance, the IND applications for current universal CAR-T therapies in China have just been submitted for approval, and it will take at least two to three more years before any assessment can be made.The CGT sector continues to hold substantial therapeutic and investment value.

Furthermore, given the relatively short development history of CGT therapies,In China, the technological gap in the CGT sector that needs to be closed compared to overseas counterparts is not significant, thanks to a relatively flexible R&D environment, more robust national policy incentives and support for rare diseases, and abundant domestic clinical resources.These are all unique advantages that help accelerate the rapid development of domestic CGT drug R&D enterprises.

It is essential to adopt a more global perspective in product initiation and base strategies on the global market. This requires cell and gene therapy (CGT) drug development companies to possess strong innovative capabilities, rather than merely following a fast-follow model. Companies such as Legend Biotech and Gracell Biotechnologies currently serve as excellent examples of this approach.

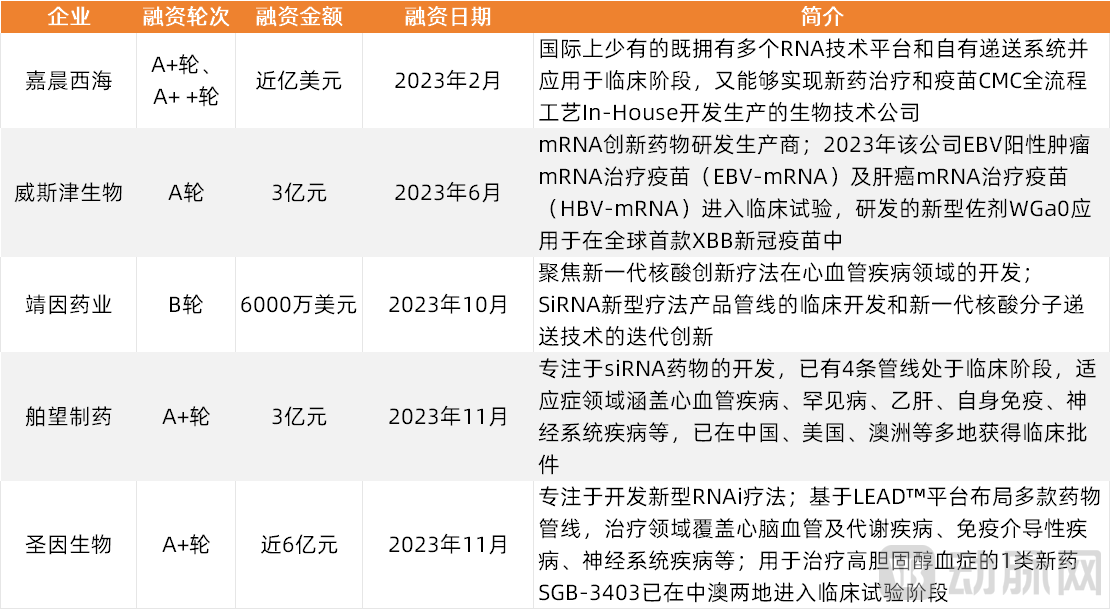

In the post-pandemic era, the hype surrounding the mRNA industry has returned to rationality, while small nucleic acid therapeutics have bucked the trend to take center stage, attracting fervent capital investment.According to incomplete statistics from VBInsight, there were 35 financing events in the field of nucleic acid drug R&D in 2023, with a total financing amount of RMB 3.84 billion. Compared with 2022, the number of financing events decreased by 18.6% year-on-year, the total financing amount decreased by 37.1% year-on-year, and the average financing amount decreased by 22.8% year-on-year.

As the global impact of the COVID-19 pandemic gradually subsides, and given the relatively slow progress in mRNA vaccine development for indications such as influenza and cancer, along with existing hurdles in delivery systems for mRNA therapeutics,In 2023, enthusiasm in the capital markets for nucleic acid drugs, represented by mRNA therapeutics, cooled.

However, this does not mean that mRNA technology is not anticipated by capital.Some investors pointed out that,mRNA technology possesses unique advantages not found in other technologies:Short development cycles and rapid responsiveness; superior immunogenicity, eliciting both humoral and cellular immunity without the need for adjuvants; and flexibility in drug formulation. Theoretically, mRNA technology can produce any protein required by humans, whether for disease prevention or treatment, offering immense prospects for future development. In contrast to the fervor surrounding mRNA technology during the COVID-19 pandemic, the industry is now gradually returning to a path of rational development.

As the top-funded company in the nucleic acid therapeutics sector in 2023, Jiachen Xiha is a nucleic acid drug developer. Its current pipeline spans multiple therapeutic areas, including oncology, infectious diseases, rare diseases, and medical aesthetics. In the fields of oncology treatment and infectious disease vaccines, the company has initiated four registrational clinical trials across three indications within these two therapeutic areas in both China and the United States within one year.

Top 20% of Projects in the Nucleic Acid Drug R&D Sector by Funding Amount

Data Sources: VBInsight, Public Corporate Reports, VCBeat

Another area worthy of attention is the nucleic acid drug sector, which is demonstrating robust momentum.Oligonucleotide Therapeutics, its performance in 2023 was noteworthy both in the capital markets and in terms of domestic clinical progress.

Three of the Top 5 Financings in the Nucleic Acid Drug R&D Sector in 2023 Were Companies Developing Small Nucleic Acid Drugs.Their commonalities lie in a scarce team, profound technological accumulation, proprietary delivery technology platforms with independent intellectual property rights, and rapid pipeline advancement.

In 2023, four oligonucleotide drugs were approved for market launch.They are Tofersen, an ASO drug co-developed by Biogen and Ionis; Nedosiran, an RNAi therapy for PH1 from Novo Nordisk; Izervay, a nucleic acid aptamer drug from Astellas; and Eplontersen, an ASO therapy co-developed by AstraZeneca and Ionis.

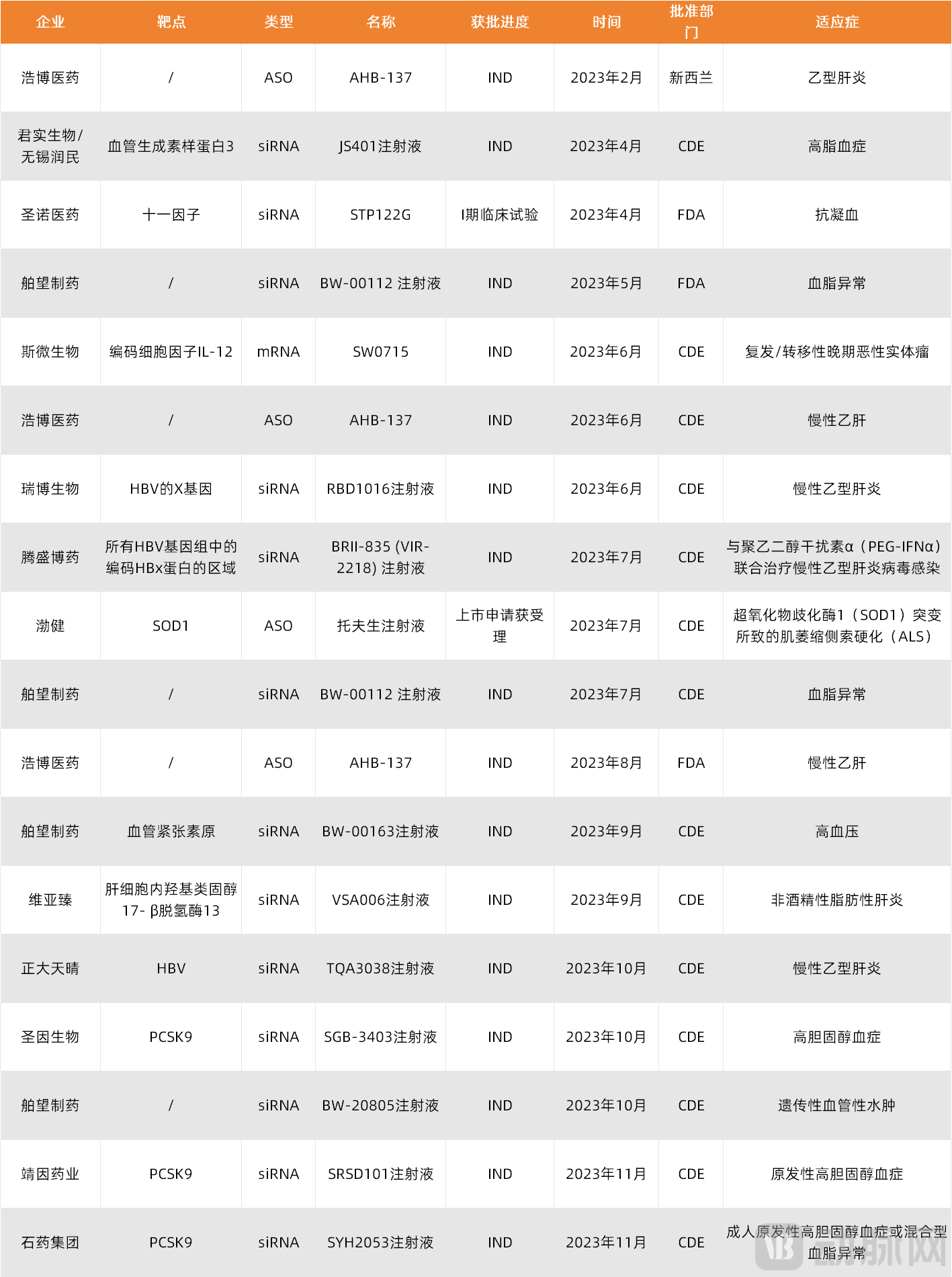

In terms of clinical approvals, according to incomplete statistics from VCBeat Research Institute,In 2023, 17 small nucleic acid drugs entered clinical trials.Among them, companies such as Bowang Pharma and Haobo Pharma have had pipelines approved in multiple regions, or multiple pipelines approved in 2023. The field of small nucleic acid drugs has already become a new blue ocean that innovative pharmaceutical companies are striving to enter.

2023 IND Approvals for Small Nucleic Acid Drug Pipelines in China

Source: Public reports from various companies, compiled by VCBeat.

Small nucleic acid drugs have mitigated druggability risks, possess substantial room for indication expansion, and are now at the tipping point of an application explosion.Theoretically, oligonucleotide therapeutics represent a highly ideal class of drugs, offering solutions for many clinically challenging diseases.

On the one hand, small nucleic acid drugs exhibit high druggability.— Under current technological conditions, small nucleic acid drugs can silence any gene in the liver. Theoretically, as more delivery technologies are developed, small nucleic acid drugs will be able to target every gene in the entire genome, finding broad applications in the treatment of genetic diseases, tumors, viral infections, and chronic diseases. In contrast, traditional small-molecule drugs and antibody drugs can target only about 4% of gene products.

On the other hand, small nucleic acid drugs have a relatively long half-life, allowing for extended dosing intervals. From the perspectives of cost and clinical demand, small nucleic acid drugs are particularly well-suited to meet the needs of the Chinese market.Taking PCSK9 as an example, the siRNA drug Inclisiran requires only one injection every six months, whereas monoclonal antibodies targeting PCSK9 necessitate two injections per month. This confers a unique advantage to small nucleic acid drugs in the treatment of many chronic diseases. Given the vast market for chronic disease management in China, the development prospects of small nucleic acid drugs have attracted significant attention from investors.

Furthermore, compared with gene therapy,Small nucleic acid drugs involve only mRNA and do not affect the genome, implying a higher safety profile.

After more than four decades of development, breakthroughs in nucleic acid chemical modification technologies and delivery platforms represented by GalNAc conjugation have enabled small nucleic acid therapeutics to overcome the bottlenecks of drug development. The field has gradually matured and expanded into multiple disease areas. With further advancements in drug delivery technologies, small nucleic acid therapeutics are now at a tipping point for explosive growth. In particularLeveraging their advantages in patient compliance, small nucleic acid drugs are entering the chronic disease market and are now on the eve of a commercial explosion.

AI-Driven New Drug Financing Cools as Hype Fades; Investors Prioritize ResultsAccording to incomplete statistics from VBInsight, the AI-driven new drug R&D sector witnessed 30 financing events in 2023, with a total funding amount of RMB 2.61 billion. Compared with 2022, the total financing amount in the AI-driven new drug sector decreased by 45.3% year-on-year, the number of financing events dropped by 26.8% year-on-year, and the average financing amount declined by 25.3% year-on-year.

Some investors pointed out that the reason lies in,AI-driven new drug discovery was once overhyped, but it appears that significant time will still be required before it can be truly implemented and play a pivotal role in new drug development. However, for some relatively simple applications, AI has already become highly mature and easy to deploy, fully demonstrating its high efficiency.

This is also reflected in the financing trends for AI-driven new drug development:AI-driven new drug projects that secured substantial financing in 2023,Either they possess inherent advantages and deep technical accumulation in the field of drug development, primarily leveraging AI technology to enhance efficiency as a “cherry on top,” such as Drug Farm and Yijieli Tech; or they demonstrate rapid progress in clinical pipelines, directly validating the efficacy of their AI-driven drug discovery engines through results, such as Dezhi Pharma and Zhuliyuan Bio; or they boast a vast customer base, directly validating the efficacy of their AI-driven drug discovery engines through extensive collaborative achievements and tangible cash-flow revenue, such as DeepModeling Technology and Tenmed.

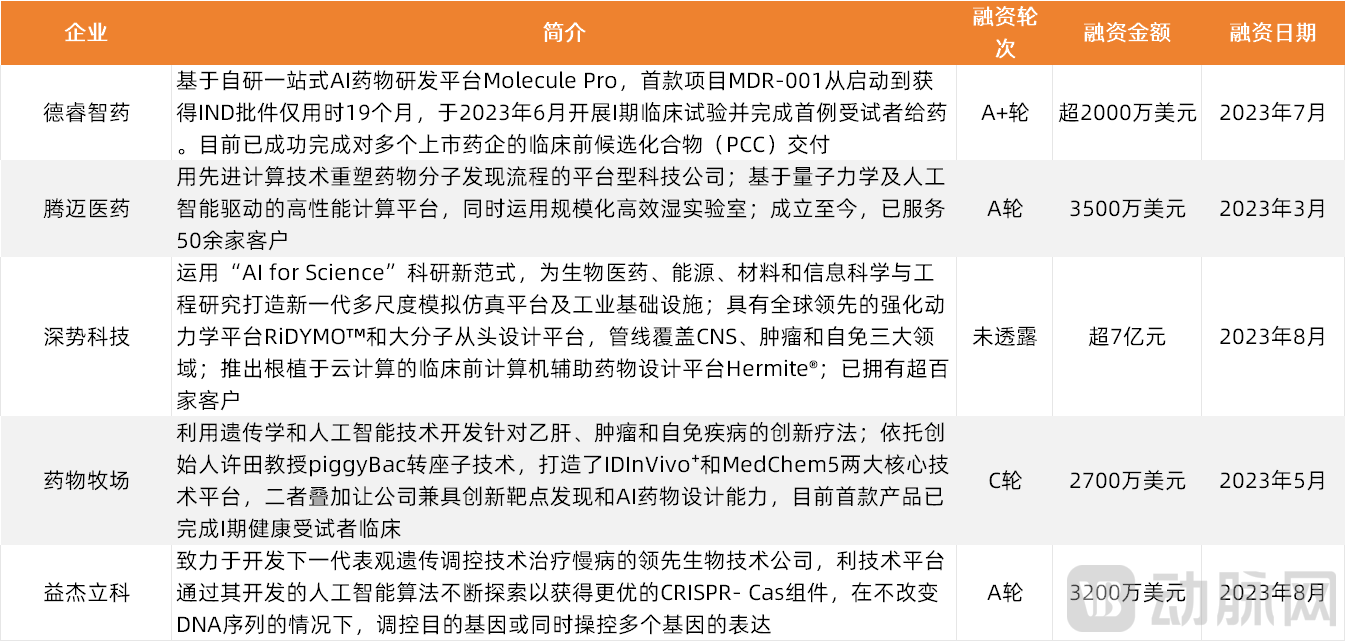

Top 5 Projects by Funding Amount in the AI-Driven New Drug Development Sector

Data Sources: VBInsight, public reports from various companies, VCBeat Research Institute

However, while pipeline progress and customer acceptance are factors that help these projects gain capital favor, what also matters is the unique characteristics of the projects themselves and the effectiveness of their AI engines. As one investor pointed out, there are three main reasons why DeepModeling Technology has been well-received by investors:

First, the project focuses on the "AI for Science" direction, featuring a unique development strategy and addressing market pain points with substantial growth potential. It targets critical fields such as biomedicine, energy, materials, and information science and engineering to solve fundamental research problems. This approach not only helps address current challenges in drug development but also resolves issues in material development and battery technology. Second, the team is led by an academician, boasting strong R&D capabilities and solid technical expertise. Third, the team demonstrates strong execution skills, combining both professional and commercial competencies.

Looking at the overall financing in the AI + new drug field,AI-driven protein development and design companies such as Molexule and Zhiyu Bioscience; Jushu Biology, which leverages AI as its core underlying technology for ultra-high-throughput engineered cell modification and protein production; and Precise Biotechnology, which provides omics data mining services and differentiated new drug development strategies to pharmaceutical companies through an AI-enabled multi-omics data mining and analysis platform.Companies that combine technological feasibility with self-sustaining revenue capabilities were the preferred investment targets in the capital market in 2023.

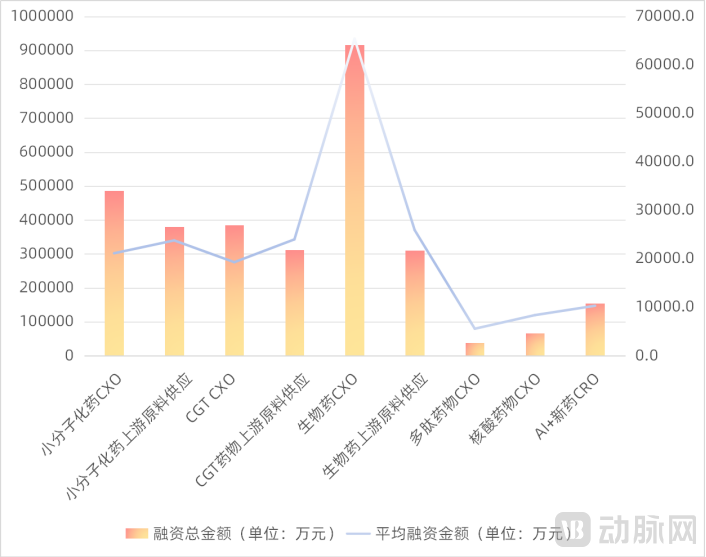

3Capital Stabilizes, Upstream Supply Chain Projects Gain Favor, Cash Flow Reigns Supreme

Amid the current complex macroeconomic environment, the prevailing sentiment among the majority of investors is to prioritize stability. This has been reflected in the capital markets, where CXO companies and upstream suppliers of pharmaceutical raw materials—characterized by lower risk and positive cash flows—have emerged as particularly favored investment targets in 2023.

Besides the aforementioned reasons, including the state’s increasing emphasis on supply chain security in recent years, upstream supply chain projects are characterized by high entry barriers, relatively low investment risk, and shorter cycles. These attributes make them relatively resilient investments amid industry contraction, thereby strengthening investors’ willingness to invest. Furthermore,The asset-heavy nature of the upstream supply chain also means that most projects in this sector secure larger financing volumes than innovative drug R&D projects.

In 2023, Upstream Supply Chain Projects Generally Attracted More Capital Than Innovative Drug R&D Projects

Data source: VBInsight, VCBeat

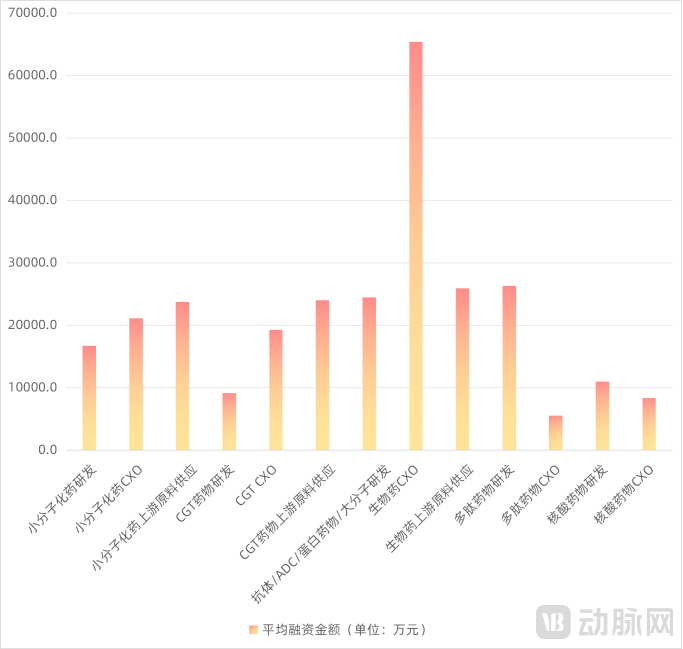

From the perspective of specific sub-sectors, the average financing amount for CXO and upstream raw material supply projects in the fields of small-molecule chemical drugs, large-molecule biologics, and CGT is higher than that in the innovative drug R&D sector. The reason lies in the fact that, after years of development,In most of the aforementioned sectors, the competitive landscape is beginning to take shape, with projects generally at mid-to-late stages and involving substantial financing volumes.

The average financing amount for project types in emerging sectors such as CXO and upstream raw material supply for peptide drugs and nucleic acid drugs is lower than that in the innovative drug R&D sector, becauseThese sectors are in a relatively early stage of development, with downstream demand growth lagging behind the aforementioned areas. Industrial ecosystems such as CXO (Contract X Organization) and raw material supply are still in their nascent stages.However, the financing volume in this sector is relatively small, having a negligible impact on the overall financing volume of supply chain projects and thus not affecting the broader market performance.

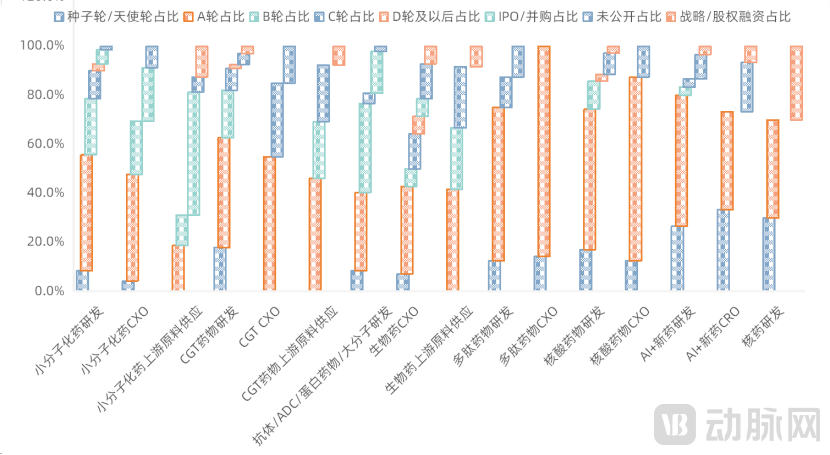

Distribution of Financing Rounds for Investment Deals in Various Sub-sectors of the Innovative Drugs and Supply Chain Fields in 2023

Data Source: VBInsight, VCBeat

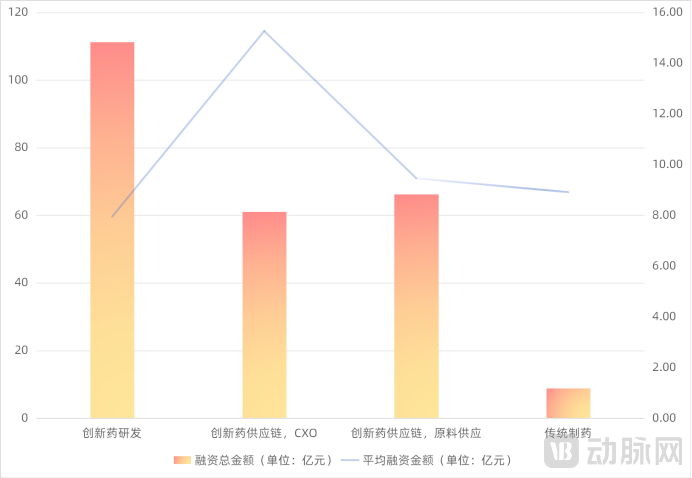

Specifically, regarding upstream supply chain project types, CXOs outperformed suppliers of pharmaceutical raw materials.Among them, biologic drug CXOs lead the pack, ranking first in both total financing amount and average financing per deal. Next are small-molecule chemical drug CXOs, which saw 23 financing events in 2023, with a total financing amount of RMB 4.86 billion and an average financing amount of RMB 210 million.

Financing Performance of Upstream Pharmaceutical Supply Chain Projects in 2023

Data source: VBInsight, VCBeat

Currently, due to factors such as geopolitical influences, U.S. interest rate hikes, increased tariffs, and the downturn in the biopharmaceutical cycle, leading domestic CXO companies have also faced significant pressure over the past two years. Both international and domestic contract signings have been substantially impacted. Overall, the secondary market performance in the CXO sector has been lackluster.

However, the primary market for CXO remains relatively hot. Some investors point out that the reason lies inShortages of CXO capabilities persist across different molecular entity domains, such as antibody-drug conjugates (ADCs), peptides, and small nucleic acids, where qualified teams and talent remain scarce in the market.

There are also some like doingCXOs capable of conducting comprehensive translational medicine research—encompassing the synthesis of specialized molecules, proprietary activity evaluation models, experimental animals, and disease models—are also scarce assets in the current market., due to sufficient differentiation and relatively high competitive barriers, it continues to attract investor interest.

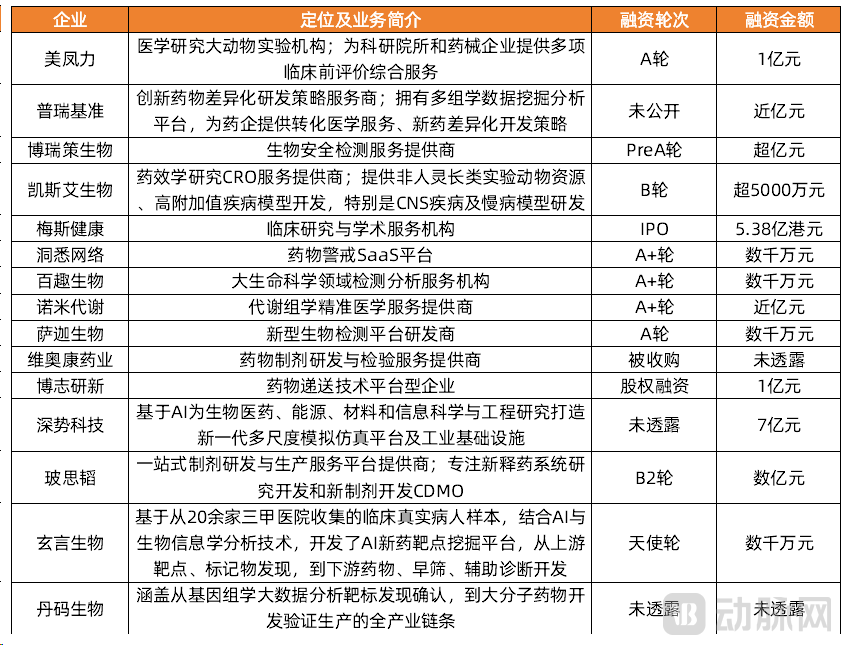

Distinctive CXOs That Secured Financing in 2023

Data sources: VBInsight, publicly available corporate reports, and VCBeat.

Furthermore, an analysis by VCBeat of CXO projects that secured substantial financing in 2023 revealed that three categories of CXO companies are favored by investors.

Top 10 Pharmaceutical CXO Financings in 2023

Data sources: VBInsight, public reports from various companies, VCBeat.

The first is a CXO company spun off from a leading CXO firm,Such as Kanglong Biology and Langhua Pharmaceutical. These types of targets are particularly popular in the capital market, with investors pointing out the reasons behind this:

On the one hand,As a service sector upstream of the pharmaceutical industry, CXO companies’ overall systems, brand reputation, and service capabilities are crucial.Global CXO leaders such as Lonza, which originally emerged from the chemical industry and achieved a leading position in that sector, subsequently expanded into biologics and cell and gene therapy (CGT), where they have also attained leadership. This trajectory has already demonstrated the feasibility of cross-sector expansion for leading CXOs. In other words, competitive advantages established by a CXO in one domain can be extended to others. Once a robust operational framework is in place, it essentially boils down to recruiting specialized professionals to handle specialized tasks. China’s WuXi AppTec group has set a prime example of development, one that aligns perfectly with the underlying logic of industry evolution.

On the other hand, the reason lies inThe spin-off of industry leaders is relatively secure.On one hand, listed companies possess relatively strong R&D capabilities and commercialization experience, along with extensive management expertise and proficiency in capital market operations. On the other hand, some listed companies have the capacity to repurchase shares, further bolstering investor confidence. Consequently, a large number of institutional investors actively participated in early-stage investments in such projects.

Second, there are CXOs that have emerged from the transformation or strategic expansion of the earliest cohort of leading cell and gene therapy (CGT) companies into the contract research, development, and manufacturing organization (CXO) sector.such as GenScript ProBio and Puxin Biologics.

Third, CXO companies founded by academic and industry professionals who were either educated in China or returned after completing their studies abroad, leveraging their technology, resources, and teams, have successfully advanced multiple products in the field of CGT drug development and CXO services.such as Paizhen Biotechnology, Yunzhou Biotechnology, and Xingcheng Biotechnology.

As a rising star in the CGT CXO sector, Xingcheng Biotech has garnered favor from prominent investment firms—including Legend Capital, Hillhouse Venture Capital, and Legend Star—within just one year of its establishment, completing a Series A financing round worth hundreds of millions of RMB in 2023. To date, the company has successfully delivered multiple plasmid, viral vector, and mRNA projects, enabling its partners to secure multiple FDA and CDE clinical trial approvals (INDs) for plasmids and rAAV viral vectors without any deficiency letters.

The rapid development of Xingcheng Biotech and its favorability among numerous top-tier investors also reflectAlthough there are numerous participants in the current CGT CDMO industry, teams with excellent CGT CDMO capabilities remain scarce assets.In particular, its robust CMC capabilities and unique chromatography-free plasmid production process promise significant future growth potential.

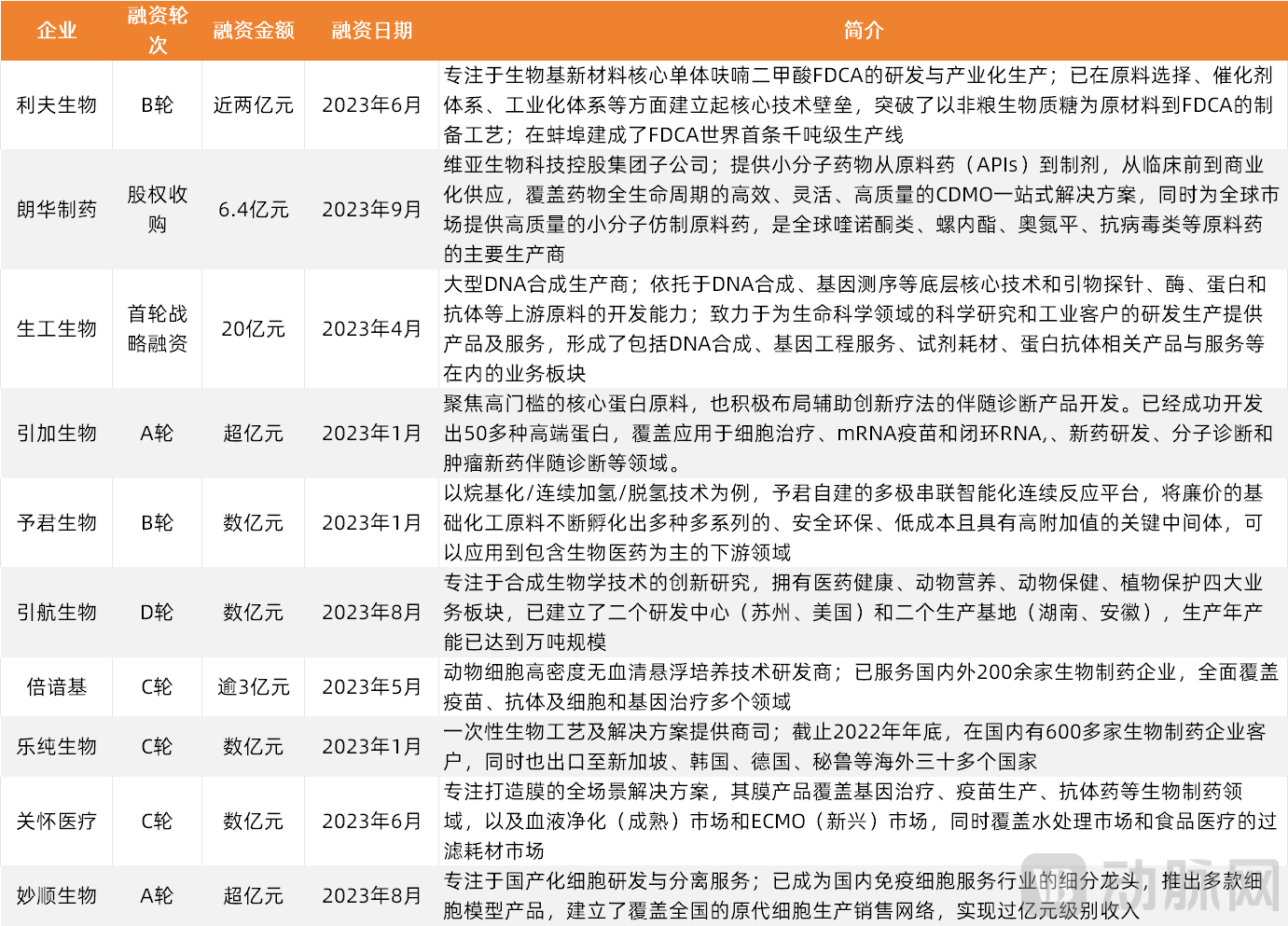

Innovative drug upstream raw material supply chain projects sought after share characteristics with CXO, both are inYears of deep industry engagement, robust technological reserves, a notable market share or leadership in niche segments, late-stage project focus, strong cash flow, and relatively low investment risk..

Top 10 Financings in the Upstream Raw Material Supply Sector for Innovative Drugs in 2023

Data sources: VBInsight, public reports from various companies, VCBeat.

4IPOs on Hold, Financing Cools: Challenges and Pathways Amid the Capital Winter—BD, Global Expansion, and M&A

As IPOs tighten and financing cools, in order to continue advancing the pipeline and sustain team survival,Engaging in outbound technology licensing and product licensing transactions, as well as pursuing mergers and acquisitions for integration and launch, is increasingly becoming the choice of domestic innovative drug R&D companies.

Amid the current industry winter, the slowing pace of IPOs and higher thresholds will become the new normal over the next two to three years. It has become an industry consensus to accept this cyclical change, proactively adjust corporate strategies, and pursue diverse approaches for survival, transformation, and exit.

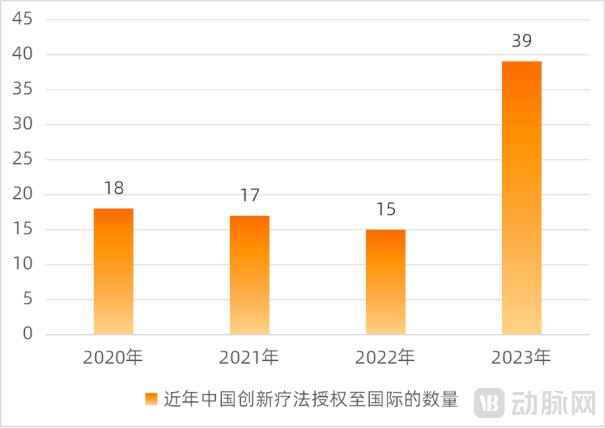

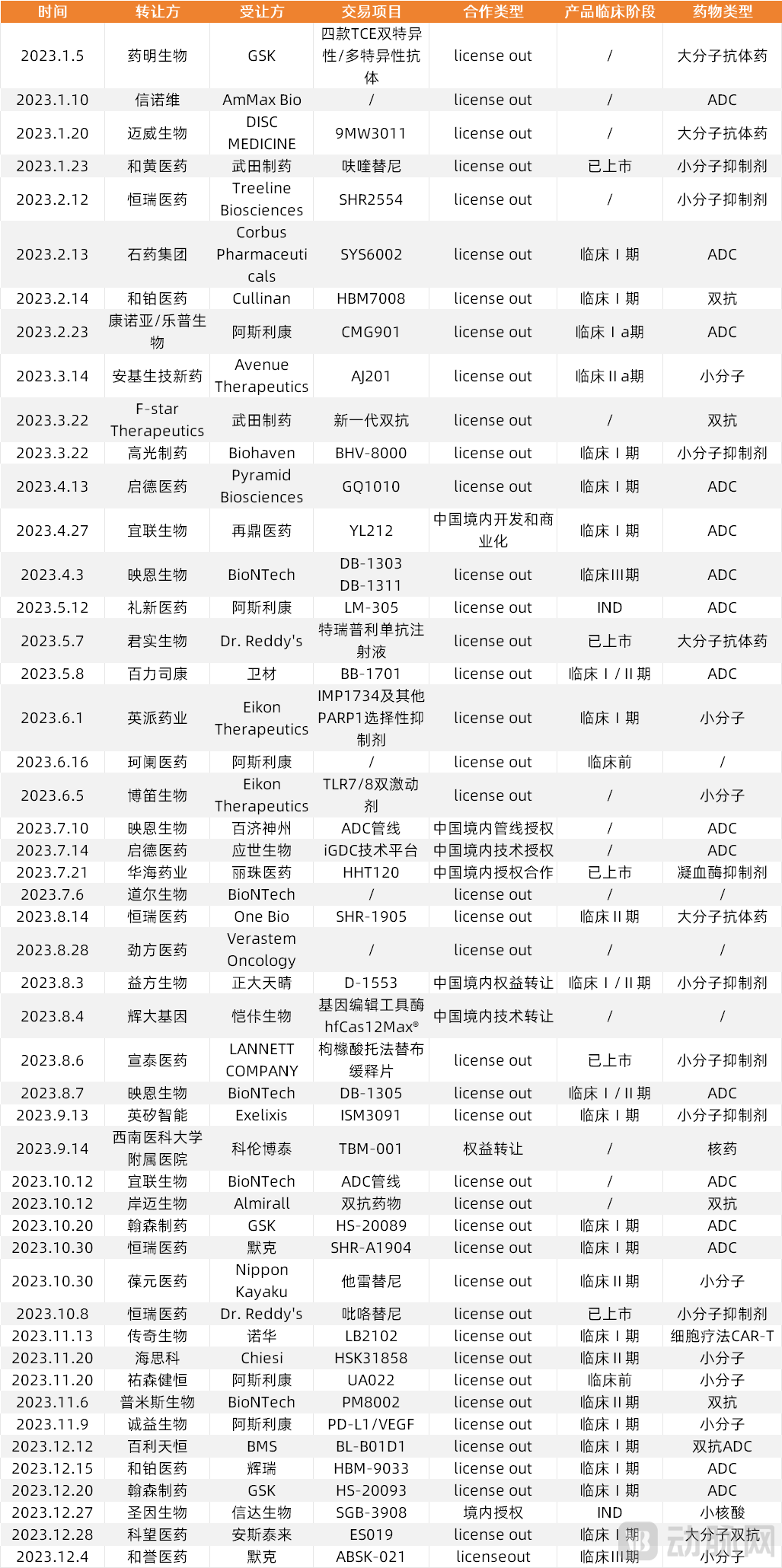

In 2023, 39 Chinese innovative drugs secured international licensing deals, reaching a four-year high

Data source: WuXi AppTec, VCBeat

As IPOs tighten and financing cools, out-licensing deals are becoming a critical source of cash flow for Chinese biotech companies.In 2023, out-licensing deals for innovative drug companies’ new drug pipelines reached a new high. According to incomplete statistics from VBInsight,The number of license-out deals by Chinese innovative pharmaceutical companies reached 53 in 2023, with a total transaction value of $42.59 billion.

2023 Outbound Licensing Deals for Technologies/Products by Chinese Innovative Pharmaceutical Companies

Data Source: VCBeat New Medicine, Eggshell Research Institute

Regarding the reasons behind this phenomenon, some investors have pointed out that in the current environment, it is difficult for Biotech companies to secure external financing, leaving them with no choice but toDivest equity stakes in promising projects to established large pharmaceutical companies in exchange for cash flow, ensuring the continuation of the most critical projects.Therefore, starting from the first half of this year, Chinese biotech companies have begun large-scale “license-out” transactions, which is also a crucial strategy for self-reliance in navigating the industry winter.

Maximizing the value of technology platforms through diverse business models and partnerships to facilitate global expansion, while generating cash flow via technological innovation, licensing, and technical services, is emerging as a new business model that revitalizes the value of technology.Fruquintinib from Hutchmed and toripalimab from Junshi Biosciences are both sold in the United States at prices more than 20 times higher than those in China, a trend that is attracting an increasing number of biotech companies to consider global market strategies from the very inception of their projects.

The frequent out-licensing of innovative biotech projects overseas also signals that the R&D capabilities of domestic innovative drugs have gained recognition from global pharmaceutical companies.Innovative drug assets are increasingly sought after through business development (BD) transactions, with out-licensing becoming a new normal practice.

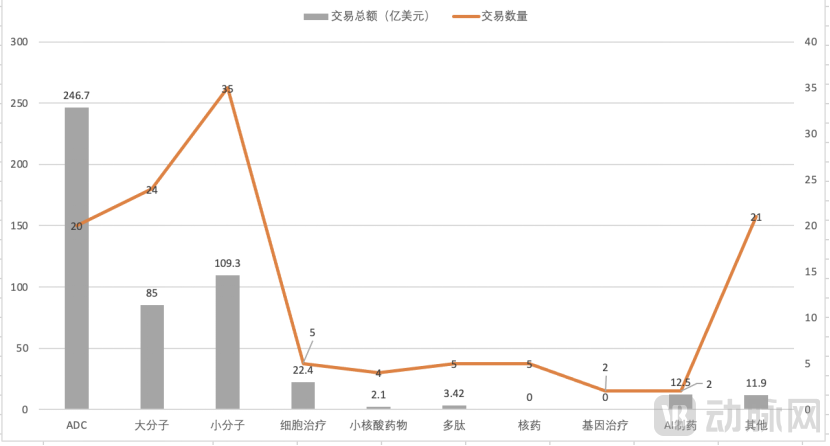

BD Deals of Chinese Innovative Drug Companies by Sector in 2023

Data Source: VBInsight, VCBeat

An Analysis of Drug Types in BD Deals Among Chinese Pharmaceutical Companies in 2023: ADCs, Large-Molecule Drugs, and Small-Molecule Drugs Dominate the BD MarketAmong them, the ADC sector emerged as the hottest area in 2023, leading by a substantial margin in total transaction value.In 2023, a total of 20 business development (BD) deals were concluded in the antibody-drug conjugate (ADC) field, with a total value reaching $24.67 billion. Among these, there were 14 license-out transactions.

On the other hand,As IPOs tightened, mergers and acquisitions among Chinese pharmaceutical companies increased in 2023 compared to 2022.A total of 83 M&A transactions occurred, with a total transaction value reaching RMB 36.61 billion, representing an increase of over 45% compared to RMB 24.97 billion in 2022. The average transaction size also rose from RMB 340 million to RMB 440 million.

In late 2023, AstraZeneca acquired Gracell Biotechnologies for $1.2 billion, marking the first time a multinational pharmaceutical company had acquired an innovative Chinese biotech firm and paving the way for new transaction models in the 2024 M&A market. Shortly thereafter, in early 2024, Johnson & Johnson acquired Ambrx for $2 billion; Ambrx was the first U.S. pharmaceutical company to be fully acquired by Chinese capital. These successful cases have instilled significant confidence in primary market investors in China, opening up new exit pathways for investors in innovative pharmaceutical companies.

Mergers and acquisitions (M&A) as an exit strategy are mainstream in Europe and the United States, while China is still in the early stages. As initial public offerings (IPOs) for Chinese innovative drug companies face obstacles, M&A exits will become one of the mainstream options. The acquisition of Chuanxin Biopharma by Baike Biologics, a subsidiary of Changchun High-Tech, also confirms that M&A represents a faster exit path for innovative drug companies.

However, multiple investors have pointed out thatRecent large-scale acquisitions have provided a strong start for the biotech sector. In the long term, mergers and acquisitions (M&A) in China’s biopharmaceutical industry are expected to increase, although they will not occur on a large scale in the short term.

First, mergers and acquisitions (M&A) are inherently complex, as they require joint decision-making by multiple stakeholder groups from both companies’ teams, making implementation particularly challenging, especially in China.

Second, if the potential buyer is a large domestic pharmaceutical company, its current willingness to acquire biotech firms remains relatively low. This is due to the inherent innovative nature and associated risks of biotech companies, including whether their product pipelines align with the existing portfolio strategies of large pharmaceutical enterprises. If the buyer is a multinational pharmaceutical corporation, the biotech firm’s pipeline and technology platform must possess sufficient global competitiveness while also aligning well with the multinational’s pipeline strategy.

However, in any case,Amid the current headwinds facing IPOs and a cooling financing environment, business development (BD), global expansion, and M&A are increasingly becoming integral components of a virtuous cycle in the development of China’s biotech ecosystem.

5CAR-T’s Business Model Proven; Clinical Progress in Solid Tumor-Targeted and Universal Cell Therapies Flourishes

Commercialization has further matured, with two truly domestic CAR-T products approved in 2023.They are respectively Icilocabtagene Autoleucel Injection, a BCMA-targeted CAR-T product jointly developed by Xunlu Biopharma and Innovent Biologics (for the treatment of relapsed or refractory multiple myeloma), and Nacilocabtagene Autoleucel Injection, a CAR-T product developed by Heyuan Biopharma (for the treatment of adult relapsed or refractory B-cell acute lymphoblastic leukemia).

Among them, Iqioleucel is the first BCMA-targeted CAR-T therapy approved in China and the first CAR-T product with truly end-to-end localization in the country. Nakioleucel is the first CAR-T product approved for marketing in China for the treatment of leukemia.

The production and commercialization logic of cell therapy is gradually being validated.Although numerous challenges remain in commercialization, the production and commercialization logic for cell therapies is gradually being validated with the successive market launches of four CAR-T drugs: Fosun Kite’s Yikaida®, JW Therapeutics’ Beinuoda®, and Fukesu® and Yuanruida®, which are jointly developed and commercialized by Gracell Biotechnologies and Innovent Biologics.

Overview of CAR-T Products Currently Approved for Marketing in China

Data source: Compiled from public information, VCBeat

According to publicly disclosed information, the unit prices of Axicabtagene Ciloleucel Injection, Relmacabtagene Autoleucel Injection, Icabtagene Autoleucel Injection, and Naacabtagene Autoleucel Injection are RMB 1.2 million, RMB 1.29 million, RMB 1.166 million, and RMB 999,000 per vial, respectively.

In terms of current commercialization across various products, Relma-cel injection generated 165 prescriptions in 2022, with the company’s total annual revenue reaching RMB 146 million. In the first half of 2023, JW Therapeutics reported revenue of RMB 87.74 million. Fosun Pharma disclosed in its 2023 interim report that, as of the end of the reporting period, Axi-cel injection had benefited more than 500 lymphoma patients. Naqi-cel injection, developed by Hesy Biologics, is the world’s first CAR-T therapy with a treatment cost below RMB 1 million. Just four days after its market approval, the first prescription was issued by the Institute of Hematology & Blood Diseases Hospital, Chinese Academy of Medical Sciences.

To further advance the commercialization of CAR-T, the aforementioned companies are actively exploring a variety of innovative payment models,For instance, Fosun Kite has actively explored collaborations with various stakeholders on innovative payment solutions, and its product, Axicabtagene Ciloleucel, has been included in more than 40 commercial insurance plans and in the supplemental medical insurance schemes (Huimin Bao) of 18 provinces and municipalities.

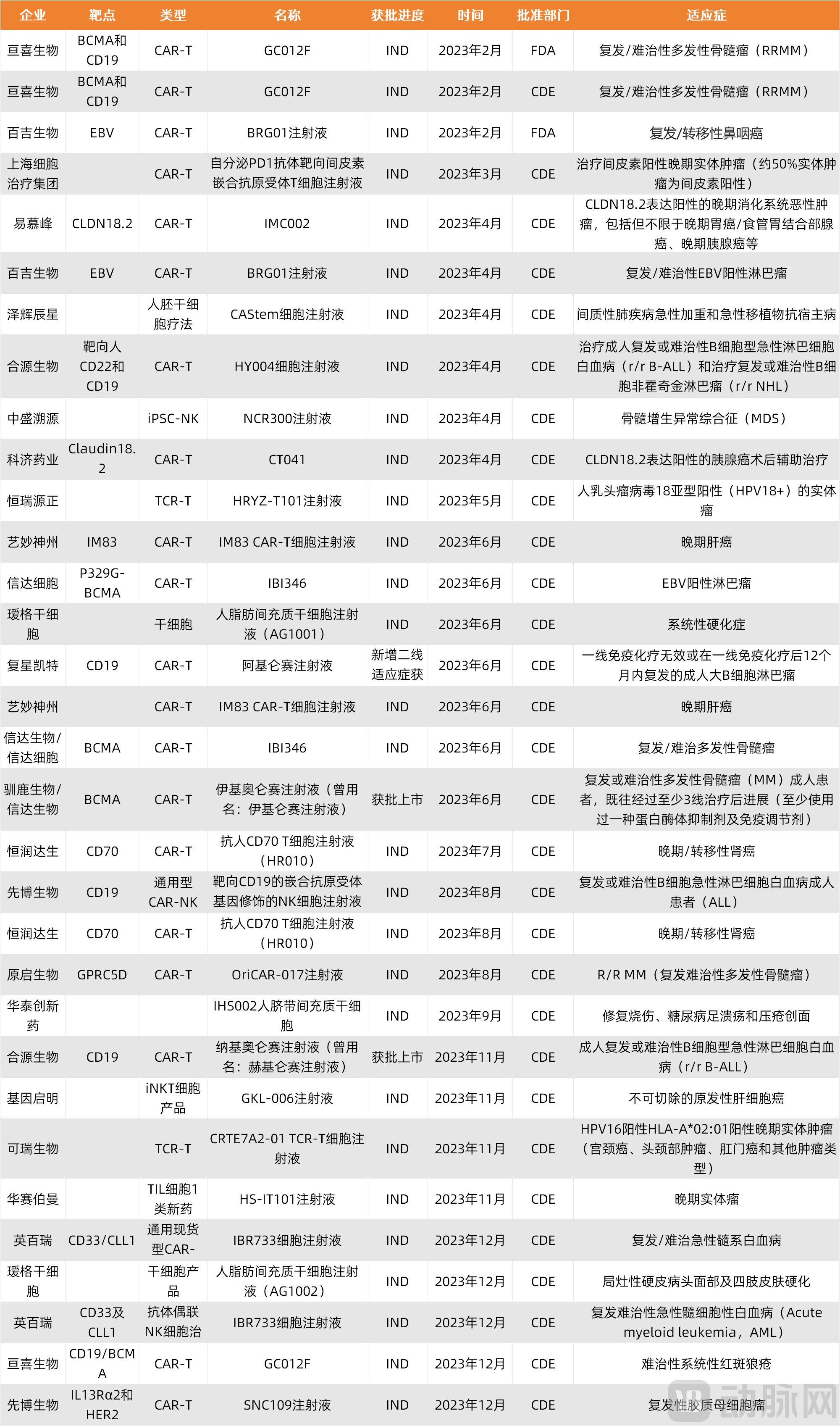

Continuing the clinical approval trends for cell therapy drugs seen in 2022, CAR-T therapies remain mainstream, while various other novel cell therapies continue to emerge.According to incomplete statistics from VCBeat Research Institute, 32 cell therapy pipelines entered clinical trials in 2023, representing a further increase compared to the 23 approved in 2022. Among the cell therapy pipelines that received Investigational New Drug (IND) approval, CAR-T therapy remains the mainstream approach, while other emerging therapies include universal cell therapies, TCR-T, iPSC, and TIL.

CAR-T pipeline targets are relatively concentrated, with most still focusing on popular single targets such as CD19, BCMA, CLDN18.2, CD70, and HER2, as well as dual targets including CD19/BCMA, IL13Rα2/HER2, and CD22/CD19. Their indications are also largely concentrated in the field of hematologic malignancies, such as multiple myeloma, lymphoma, and leukemia.

ButWith the successful validation of multi-target therapies, such as dual-target CAR-T and CAR-T combination therapies, as well as novel targets, CAR-T therapies for solid tumors—including liver cancer, gastrointestinal cancers, and renal cell carcinoma—are increasingly advancing into clinical trials. In addition, allogeneic cell therapy products, such as “off-the-shelf” and “universal” formulations, are being developed.It has become one of the important directions in the field of tumor immune cell therapy.

The World’s First TIL Therapy Is Set for Approval, as Eight Domestic Companies Advance Their TIL Therapies into Clinical Trials.On May 26, 2023, Iovance announced that the FDA had formally accepted its Biologics License Application (BLA) for lifileucel in patients with advanced melanoma and granted it Priority Review designation. The PDUFA date for lifileucel was set for February 24, 2024. Lifileucel is poised to become the first approved TIL therapy globally.

By the end of 2023, eight TIL therapies developed by domestic companies, including Jingfeng Biologics, Shali Biologics, Junsaibio, CytoMed Therapeutics, Zhiling Biopharma, Lanma Medical, Houwu Biologics/Guangdong Tiankeya Biologics, and Huasaiboman, had successively entered clinical trials.2024 May Become the First Year of Industrialization for Global TIL Cell Therapy.

Overview of IND Approvals for Domestic Cell Therapy Pipelines in China in 2023

Data Source: Compiled from public news reports, VCBeat.

6Five More Gene Therapies Launched Globally, 22 Enter Clinical Trials in China; AAV Gene Therapy Remains Dominant

Compared with the 15 gene therapy drug pipelines approved for clinical trials in 2022, the number of approvals reached a new high in 2023, with 22 candidates entering clinical development. In terms of vector types, AAV remains the mainstream choice.

Status of IND Approvals for Domestic Gene Therapy Pipelines in 2023

Data source: Compiled from public news, VCBeat

Given the conflict between the high cost of gene therapy and China’s current medical insurance system, product development based on the global market may represent a more optimal growth path.This requires enterprises to possess strong innovation capabilities, rather than merely adopting a fast-follower model.

Globally, five additional gene therapies were approved in 2023, the same number as in 2022.Among them, Casgevy is the world’s first approved CRISPR gene-editing therapy, indicated for the treatment of two inherited blood disorders: transfusion-dependent β-thalassemia (TDT) and sickle cell disease (SCD).

Overview of the Five Gene Therapy Products Approved for Global Launch in 2023

Data source: Public news summary and compilation, VCBeat.

7Clinical Review of Antibody Drugs: ADCs and Bispecific Antibodies Each Command Their Own Territory; the Industry’s Pain Point Is Not Target Homogenization but Technology

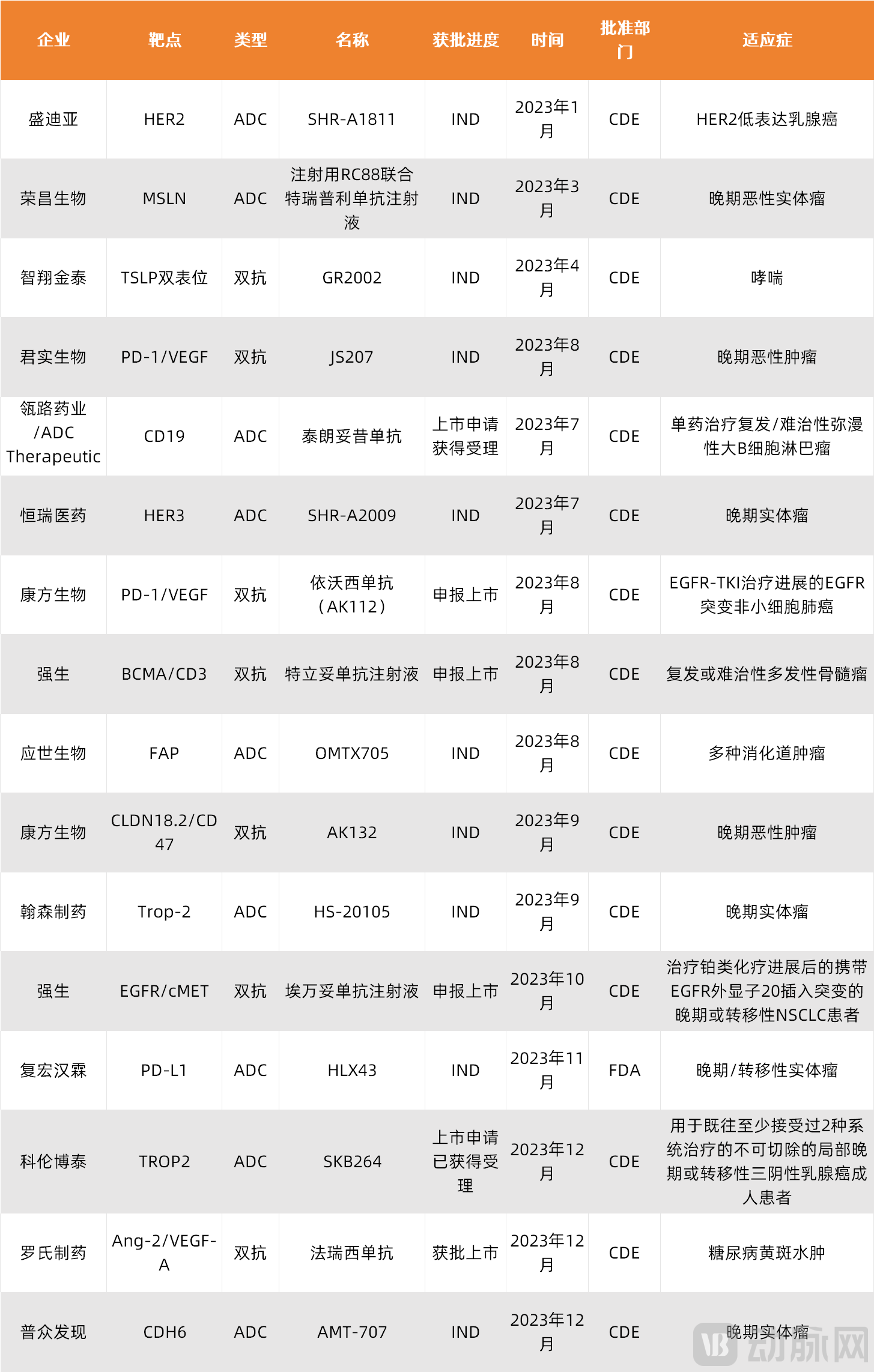

2023 China: IND Approvals for ADC and Bispecific Antibody Pipelines

Data source: Compiled from public news reports, VCBeat.

In 2023, the targets for approved antibody-drug conjugate (ADC) pipelines remained focused on popular candidates such as HER2, MSLN, and TROP2, with indications primarily covering various types of cancer. In response to the congestion in ADC target selection, many pharmaceutical companies have adopted differentiated strategies in the ADC field.Differentiated exploration of targets.

Recently,Domestic pharmaceutical companies’ clinical applications for ADCs also include certain niche targets.For instance, Hansoh Pharma and Mabwell Therapeutics have laid out strategies targeting B7-H3; Henlius has focused on STEAP1; Angkuo Pharma is developing candidates against CDH6; and Jiangsu Hengrui Pharmaceuticals and BeiGene are pursuing CEA.

From a target-centric perspective, the ADC landscape appears highly competitive. However, unlike pure antibody therapies, ADCs do not exert their therapeutic effect by modulating the intrinsic function of the target to kill tumor cells. The target serves merely as a delivery vehicle; the actual therapeutic agent is the toxin. Furthermore, the clinical efficacy of ADC drugs is influenced by the various combinations of antibodies, linkers, and small-molecule toxins.The clustering of targets in the ADC field is not a major concern; the primary focus remains on the efficacy of the final product.

Exploring combination therapies and other approaches is also an important strategy and research direction for achieving better efficacy of antibody-drug conjugates (ADCs) and overcoming drug resistance.Furthermore, ADCApplications in Non-Oncological DiseasesIt is also a new blue ocean.

In the bispecific antibody field, three products—Akeso’s ivonescimab (targeting PD-1 and VEGF), Johnson & Johnson’s teclistamab (targeting CD3 and BCMA), and amivantamab (targeting EGFR and cMET)—submitted marketing applications to the Center for Drug Evaluation (CDE) in 2023. Additionally, Roche’s faricimab (targeting Ang2 and VEGFA) received CDE approval for marketing on December 18, 2023.

Currently, more than 40 companies in China are involved in the research and development of bispecific antibody drugs.Among them, Akeso’s ivonescimab is the first domestically produced bispecific antibody to be marketed, as well as the world’s first PD-1/CTLA-4 bispecific antibody, while Innovent Biologics has the largest pipeline of bispecific antibodies.

Major business development (BD) collaborations are frequently announced, with clinical and commercialization pipelines continuously updated and iterated. Antibody-based therapeutics are increasingly shifting toward emerging modalities such as antibody-drug conjugates (ADCs), bispecific antibodies, and even multispecific antibodies. In the coming year, ADCs and bispecific antibodies are poised to bring greater dynamism to the industry in terms of antibody drug pipelines and BD/mergers and acquisitions activities.

The above is an excerpt of the main content of the report. Below are the outstanding innovation case studies of the year. Scan the QR code on the poster to access the full report.