Chinese CGM Makers Face Tough Competition in European Market Amid Aggressive Domestic Price Wars

Sinocare

Rapid Detection of Chronic Disease: Product R&D, Production, and Sales

yuwell

Developer and Manufacturer of Basic Medical Devices

Sibionics

Medical Device R&D and Manufacturing Company

MicroTech Medical

Developer of Medical Device Products for Diabetes Management

In 2023, domestic CGM manufacturers finally drove down the price of continuous glucose monitors (CGMs) through fierce competition.

Two years ago, the prevailing price for domestic CGM products ranged from RMB 400 to RMB 600. Currently, the unit price of CGM products has dropped by approximately 50%. During the 2023 Double 11 shopping festival, the unit prices of CGM devices from Sinocare and Yuwell even fell to the range of RMB 100 to RMB 200.

Sinocare and Yuwell have adopted such aggressive strategies because, as late entrants to the market, they aim to rapidly gain a foothold. It is reported that Yuwell’s CGM product was approved for market launch in March 2023, while Sinocare’s CGM product went on sale in April 2023. In contrast, Abbott’s CGM was approved in 2016, Medtronic’s CGM in 2020, and the CGM products of Sibionics, MicroTech Medical, and Infinovo Medical were approved in November 2021.

As more continuous glucose monitoring (CGM) systems gain regulatory approval and enter the market, competition in China’s CGM sector has intensified significantly. Taking the 2023 Double 11 shopping festival as an example, Sinocare increased its advertising spending ahead of the event, boosting exposure for its CGM products through Focus Media elevator advertisements to capture consumer mindshare. Meanwhile, it lowered CGM product prices under the guise of promotional discounts, leveraging price advantages to attract users. These measures, combined with Sinocare’s established brand and channel strengths, resulted in sales of over 100,000 boxes of its CGM products during the Double 11 period, with total online omni-channel sales exceeding RMB 210 million.

Yuwell also launched an offensive during the Double 11 Shopping Festival, with its CGM product sales exceeding RMB 10 million and blood glucose meter sales increasing by over 30% year-on-year. Sibionics is a regular participant in major promotional events such as the 618 Mid-Year Shopping Festival and Double 11; during Double 11, its CGM sales surpassed RMB 67 million, representing a 110% year-on-year increase.

Judging by the results, sales of domestically produced CGMs have surged over the past two years, with Chinese companies continuously capturing market share from overseas giants such as Abbott and Medtronic, thereby increasing the localization rate of CGMs.

Nowadays, influenced by multiple factors such as cost, brand, distribution channels, profit margins, and competition, the pricing of continuous glucose monitoring (CGM) systems in the Chinese market has stabilized. Domestic and international companies have reached a tacit understanding to avoid engaging in prolonged price wars. After all, while striving to win in competition, companies must also ensure profitability.

In addition to the domestic market, companies such as Sinocare, Yuwell, Sibionics, MicroTech Medical, and Infinovo Medical are also setting their sights on the international market, hoping to ride the wave of medical device exports and sell Chinese-made CGMs globally.

Looking back, one can often identify the pivotal times, places, and events that have shaped the course of history. In the field of continuous glucose monitoring (CGM), October 2023 was the key time, Europe was the key location, and global expansion was the key event for China’s CGM industry.

In October 2023, Sinocare’s CGM product obtained the EU MDR certification, marking the first MDR certificate issued by TÜV Rheinland Greater China for a domestically produced CGM product. In late October, Sibionics’ CGM product, SIBIONICS GS1, also received the EU MDR certification. Also in October, Yuwell stated in response to investor inquiries that it was applying for MDR certification for its CGM product.

Following product approval, the next objective for companies such as Sinocare and Sibionics is commercialization. Sinocare stated, “For the sales of CGM products in the EU region, the Company will draw on its prior experience in BGM sales by developing cross-border e-commerce platforms and establishing local European teams to enter the EU market.”

It is worth noting that prior to this, CGM products from companies such as Infinovo Medical, MicroTech Medical, and Movea Tech had already obtained EU CE certification and were widely sold in the European market. For instance, Infinovo Medical’s CGM products have entered more than 30 overseas countries and regions; MicroTech Medical’s CGM product, AiDEX G7, began commercialization in the European market as early as March 2021; and Movea Tech’s CGM products were gradually included in the national healthcare reimbursement systems of Denmark, Sweden, Italy, the Netherlands, the Czech Republic, and other countries starting in 2018.

To accelerate their global expansion, Chinese CGM manufacturers have increased their investments in exhibitions and academic promotion, aiming to rapidly penetrate the European market. For instance, the Annual Meeting of the European Association for the Study of Diabetes (EASD), held in October 2023, is the largest diabetes conference in Europe, attracting over 15,000 representatives from more than 130 countries worldwide. Domestic companies such as Sibionics, Sinocare, Yuwell, Movea Tech, MicroTech Medical, and Infinovo Medical all participated. These companies sought to attract distributors from various regions across Europe by showcasing new products, establishing connections, and negotiating partnerships to quickly enter the European market.

In addition to the European Association for the Study of Diabetes (EASD) Annual Meeting, various companies also participated in conferences across different European countries, tailored to regional market characteristics and corporate strategies. In March 2023, Infinovo Medical attended the Société Francophone du Diabète (SFD) Annual Congress, the largest diabetes conference in French-speaking regions, where it showcased its calibration-free continuous glucose monitoring (CGM) product. In February 2023, MicroTech Medical participated in the 16th International Conference on Advanced Technologies & Treatments for Diabetes (ATTD), which drew approximately 4,800 experts and scholars, and exhibited its products at the event.

In addition, some domestic CGM manufacturers are simultaneously expanding into markets outside Europe. For instance, Sinocare has entered the U.S. market, with its CGM product receiving FDA 510(k) clearance in December 2023. In the same month, Sinocare completed certification under the Medical Device Single Audit Program (MDSAP) for its quality management system and obtained the MDSAP certificate issued by SGS. This signifies that Sinocare has met the medical device quality management system requirements of regulatory authorities in multiple countries, including Australia, Brazil, Canada, and the United States, laying a solid foundation for its global expansion.

MicroTech Medical has established a presence in the Middle East, Africa, and South America. In January 2023, MicroTech Medical showcased its one-stop blood glucose management solution at the Arab Health 2023, the largest medical device exhibition in the Middle East. In May 2023, it participated in Hospitalar – The International Medical Equipment and Supplies Exhibition of Brazil, the largest and most comprehensive medical equipment exhibition in South America, with its latest generation of products...

Overall, Europe has emerged as the most popular destination for CGM companies expanding overseas.

In the global medical device market, Europe is a market that cannot be ignored.

From an economic perspective, Europe is the most economically developed continent globally, with the European Union’s total GDP reaching approximately $16.65 trillion in 2022. Meanwhile, countries such as Germany, France, and Belgium allocate a significant proportion of their spending to healthcare and sanitation. For instance, Germany’s healthcare expenditure amounted to €440.6 billion in 2020, accounting for approximately 13.1% of its GDP; France’s healthcare expenditure was approximately €227.5 billion, representing about 10% of its GDP.

Europe ranks among the top in the global medical device market, likely benefiting from its advanced economy and ample healthcare budgets. According to MedTec Europe, the European medical device market was valued at approximately €135 billion in 2022, accounting for about 27% of the global market, making it the second-largest medical device market after the United States.

In the CGM market, a report released by Debon Securities shows:The global CGM market reached $5.7 billion in 2020, with the United States and Europe collectively accounting for approximately 70%. Consequently, the European market is a critical battleground that no global CGM manufacturer is willing to forsake.。

On the other hand, supported by medical insurance systems, the CGM market in Europe is expected to maintain a growth rate of 18%-20%, further attracting the attention of global CGM manufacturers.

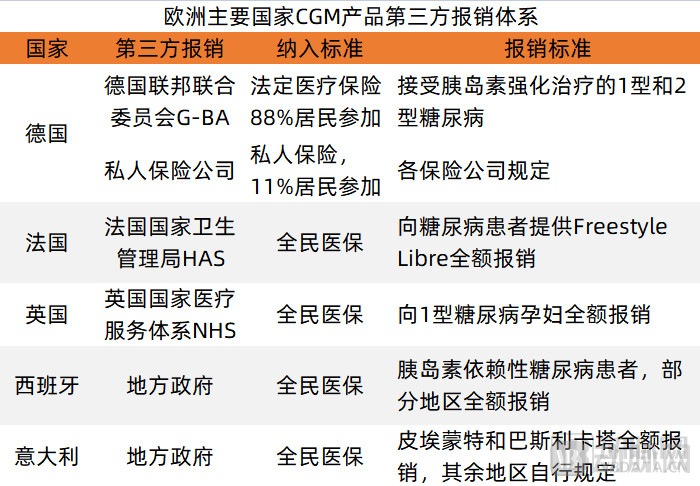

From the perspective of health insurance coverage, many European countries have incorporated continuous glucose monitoring (CGM) systems into their reimbursement frameworks. For instance, the United Kingdom and France provide full reimbursement for eligible patients, covered by their national healthcare systems. In Germany, patients who meet the criteria receive either partial or full reimbursement, funded by private health insurers. These comprehensive coverage systems alleviate the out-of-pocket financial burden on patients, thereby incentivizing the purchase and use of CGM devices.

Meanwhile, CGM manufacturers such as Abbott have promoted multiple real-world studies on CGM conducted in Europe, aiming to use data to persuade payers to recommend and encourage patients to use CGM.

For example, a retrospective study in France showed that among patients with type 2 diabetes using insulin once daily, the use of continuous glucose monitoring (CGM) significantly reduced acute diabetic complications and decreased hospitalizations by 67%. Supported by clear clinical evidence, France announced in June 2023 the approval of an expanded reimbursement scope for CGM, extending coverage from only patients with type 1 and type 2 diabetes requiring intensive insulin therapy to all patients with diabetes using basal insulin.

For payers, CGM can help patients control their condition, reduce complications, and lower total healthcare expenditures. Therefore, it is expected that more countries (healthcare payers) will follow France’s lead in expanding reimbursement coverage for CGM.

An anonymous distributor stated, “The inclusion of CGM in U.S. medical insurance coverage drove its penetration rate to 25.8% by 2020, whereas the penetration rate in other regions worldwide was only 10%, or even lower. In light of this, the inclusion of CGM in insurance reimbursement schemes in countries such as France could significantly boost CGM penetration in the European market. This also presents an opportunity for Chinese CGM manufacturers.”

Large market and rapid growth, but the European market is difficult to penetrate.

First, competition in the European market may be more intense than in the domestic Chinese market. Previously, companies such as Abbott and Dexcom stated in their quarterly reports that Europe would be a key focus for future growth. On the other hand, Abbott and Dexcom have already established a presence in the European market, securing a first-mover advantage; meanwhile, Medtronic’s CGM product received CE certification in September 2023, marking its entry into the European market. Coupled with the influx of a number of Chinese CGM manufacturers, competition in the European market is expected to become even more fierce.

The aforementioned distributor stated, “Competition in the Chinese market is also fierce, but companies such as Sibionics have managed to capture a portion of market share from overseas giants, demonstrating that domestically produced CGMs meet clinical needs in terms of performance and that their strategies and approaches are recognized by the market. However, in the European market thousands of miles away, domestic CGM manufacturers still need to take into account various factors such as local language, culture, and market characteristics.”

Secondly, there are significant linguistic and cultural differences between the European market and China, with the EU alone having 24 official languages. Moreover, most of these countries have relatively small populations, resulting in limited market size and product demand. This necessitates that Chinese CGM manufacturers carefully consider their overseas expansion strategies: Should they establish direct sales teams in each country? If so, what should be the team size? These disparities also pose challenges for Chinese CGM manufacturers in terms of promotion, marketing, and sales.

Furthermore, there are subtle differences in medical device regulatory frameworks among EU member states. European countries outside the EU, such as the United Kingdom, Switzerland, and Norway, exhibit even greater divergences from EU regulations. The evolving landscape of medical device regulations has complicated the sales environment for CGM manufacturers.

Finally, markets in different countries have distinct characteristics. For example, in the French market, public hospitals account for approximately 55%, while private hospitals account for approximately 45%. Both sectors rely on centralized procurement for medical devices. In public hospital centralized procurement, the top-ranked bidder captures the entire market share, with a contract period of 2–4 years. In private hospitals, the group’s procurement department manages the tendering process. For each product, 1–3 suppliers are shortlisted, and physicians independently choose from this list; the group does not proactively recommend products from any specific company.

In the Italian market, public hospitals account for 75% and private hospitals for 25%, with both sectors primarily relying on regional independent procurement. In the public hospital market, hospitals typically issue tenders independently and hold absolute decision-making power. The winning bidder secures a 50% market share, while other shortlisted suppliers compete for the remaining share, with contract cycles lasting 1–3 years. In the private hospital market, most private hospitals in Italy are part of regional groups, where centralized group procurement departments manage tendering processes, primarily awarding contracts to the lowest bidders.

Overall, while the European market is a highly attractive opportunity, it presents significant challenges for market entry. Relevant enterprises must formulate clear strategies, make adequate preparations, and pursue steady, pragmatic growth.

Faced with the highly attractive yet challenging European market, which type of domestic CGM company is more likely to rapidly enter the market?

From the industry’s perspective, leading companies such as Sinocare, MicroTech Medical, and yuwell—those with overseas expansion experience, established international distribution channels, and dedicated overseas teams—are better positioned to rapidly penetrate global markets.

For example, Sinocare has established branches (subsidiaries) in countries such as Vietnam and the Philippines, built local sales teams, and formed strategic partnerships with international partners to accelerate its expansion into overseas markets. To date, Sinocare’s business has covered more than 200 countries and regions, including Germany, France, Italy, Spain, Portugal, the United Kingdom, Russia, and Canada, demonstrating extensive experience in exporting blood glucose monitoring products.

In terms of distribution channels, in addition to its traditional sales network, Sinocare has established a cross-border e-commerce presence. Currently, Sinocare operates self-built independent websites in European languages such as German, French, and Spanish, and maintains storefronts on third-party international platforms including eBay, Amazon, AliExpress, Shopee, Lazada, Cdiscount, Jumia, and Joom.

Meanwhile, Sinocare has established cooperative overseas warehouses in 17 countries across Europe, North America, and Southeast Asia, achieving localized logistics. Leveraging e-commerce channels and superior logistics services, Sinocare will accelerate its penetration into the retail market.

Additionally, Sinocare will iteratively upgrade its existing products to meet the market demands of different countries, ensuring they better align with local users' habits and needs.

Similar to Sinocare, MicroTech Medical and yuwell also possess extensive experience in overseas expansion. Notably, MicroTech Medical has successfully marketed its Equil patch insulin pump system in more than 20 countries across the Asia-Pacific region, Europe, the Middle East, and Africa. In the first half of 2023, yuwell’s overseas revenue reached RMB 368 million, accounting for 7.39% of the company’s total operating revenue.

Compared with leading enterprises that possess advantages in talent, capital, and experience, innovative companies embarking on their first international expansion also have the opportunity to rapidly penetrate overseas markets. By leveraging powerful distributors, these innovative firms can quickly sell their products abroad. However, in the long run, innovative companies must also formulate a global expansion strategy, advancing in stages to ultimately achieve the internationalization of their products, brands, and academic influence.