NVIDIA Bets Big on Generative AI and Healthcare: $10 Billion Invested in 2023 Alone

NVIDIA

Artificial Intelligence Computing Service Provider

The year 2023, which has just passed, was chilling to the core. In contrast, AI, after years of dormancy, has surged once again alongside large language models, voraciously absorbing global venture capital and showing strong potential to lead the Fourth Industrial Revolution.

OpenAI, which brought this technology to the forefront, once held an absolute advantage in the race. Subsequently, established AI giants such as Google, Microsoft, and Baidu joined the fray. With a proliferation of large models, the competitive landscape for general-purpose large language models has begun to grow increasingly nuanced.

The gold-mining potential of innovative technologies has yet to gain widespread recognition, but the “water sellers” along the way have already reaped substantial profits. In 2023 alone, NVIDIA’s stock price tripled amid the massive computational demand spurred by generative AI, pushing its market capitalization past the $1 trillion mark and now nearing $2 trillion.

Amid its rapid acceleration, NVIDIA has rarely altered its AI layout strategy.

Over the past decade, with each potential foundational technological shift in the internet world—from deep learning to blockchain and Web 3.0—this tech giant has consistently reaped substantial profits from its GPU-driven computing power business. Consequently, NVIDIA has been content to maintain its role as an intermediary, developing various tools for the bustling community of entrepreneurs while rarely entering the fray itself.

And now, facing the rise of large language models, NVIDIA has also chosen to dive in headfirst, making bold and sweeping investments.

The UK-based advisory firm Dealroom compiled statistics on NVIDIA’s primary market transactions in 2023. Over the course of the year, NVIDIA made a total of 35 investments, approximately six times the number from the previous year, with every single investment being AI-related.

During the investment process,NVIDIA appears to exclude no application scenarios, nor does it concern itself with the funding round or size of its targets.Whether it is upstream general-purpose large models, midstream enterprise SaaS, downstream To-C vertical applications, or Series B and C projects in large-model infrastructure construction with valuations often reaching tens of billions, as well as seed-round To-C startups valued at under one million, NVIDIA is present wherever there is innovation and the potential for industrial intelligence.

Meanwhile, NVIDIA has made significant adjustments to its investment approach and focus.

In building its AI ecosystem, NVIDIA has historically prioritized “stability.” For the most part, it has relied on the NVIDIA Inception program to lower the barriers to AI R&D and accelerate growth for AI entrepreneurs by providing GPU resources and AI development platform support, while simultaneously deepening the integration of its hardware and software solutions with startups to continuously expand the foundation of its ecosystem.

Last year, NVIDIA’s venture capital arm, NVentures, led nearly all transactions within the year, with more than half of the deals spearheaded by NVentures, assuming greater risks in exchange for accelerating industry development.

This shift is clearly beneficial for startups. Although NVIDIA has explicitly stated publicly:Companies joining the ecosystem will also adhere to the rules, with no “queue-jumping” allowed to secure chips earlier than users outside the ecosystem.However, straightforward cash support and the establishment of a more direct, in-depth, and close relationship with NVIDIA will bring about tangible changes to the development of startups.

The shift in NVIDIA’s strategic focus offers valuable guidance, potentially signaling the cutting-edge direction of AI technology development. In 2023, NVIDIA showed a particular preference for the upstream segment of generative AI.General-Purpose Large Language Modelswith the midstream'sMedical AI。

The rationale behind betting on general-purpose large language models (LLMs) is easy to understand. The capability ceiling of general-purpose LLMs in a given region determines the upper limit for LLM-based applications within that same region. Since the surge in popularity of ChatGPT, AI giants such as Google, Microsoft, and Meta have spared no effort in investing in R&D in this area. Naturally, NVIDIA is unwilling to remain a mere bystander and miss out on a potentially epoch-making transformation.

Consequently, shouldering the heavy burden of “national AI” advocates’ calls for the “nationalization” of general-purpose large models, NVIDIA has successively invested in three general-purpose large model developers—Infection AI, Cohere, and Mistral—expanding its own general-purpose large model footprint across Europe and the United States. It has also injected capital into open-source large model development platforms such as Hugging Face and Replicate, thereby securing a firm grip on the pivotal hub for value conversion of general-purpose large models.

When it comes to specific niche application scenarios, NVIDIA’s strategic layout is somewhat surprising. Among the 30 projects listed in the statistical table, only one or two in sectors where NVIDIA excels, such as gaming and industrial applications, have received investment, with generally modest funding amounts.In contrast, medical AI, which has been in flux for decades, saw 13 projects secure financing.。

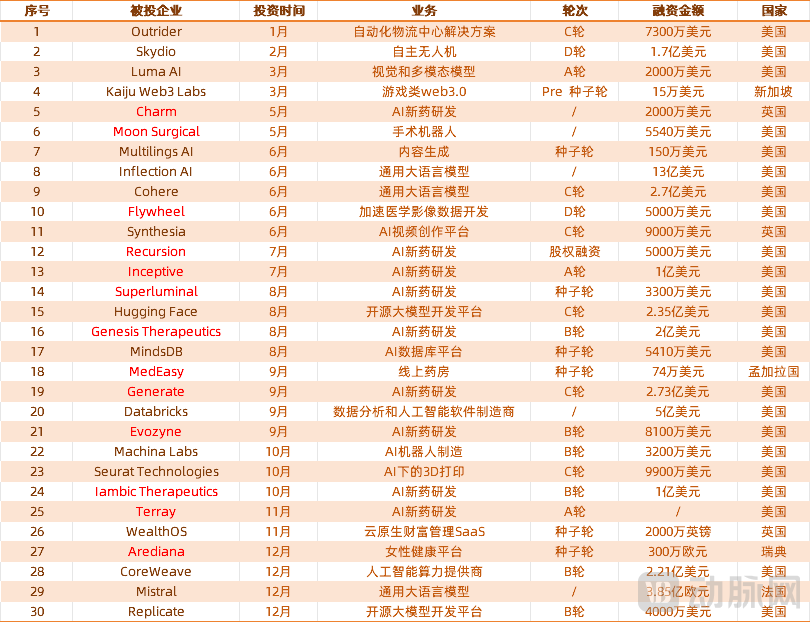

NVIDIA’s Investment Portfolio in 2023 (Incomplete Statistics; Companies Highlighted in Red Are Related to the Pharmaceutical Industry; Compiled by VCBeat)

A simple classification of the 13 projects reveals two in medical computer vision, two in internet healthcare, and nine in new drug R&D. The nine new drug R&D projects involve Charm Therapeutics, Recursion, Inceptive, Superluminal Medicines, Genesis Therapeutics, Generate:Biomedicines, Iambic Therapeutics, and Evozyne. Among them, Generate:Biomedicines secured the largest funding round at $273 million, setting a full-year financing record for the previous year, while the smallest project raised no less than RMB 100 million.

A Renaissance in the Age of Artificial Intelligence?

The peak period for AI-driven drug development was from 2020 to 2022. During that time, even seed-stage startups could secure financing in the hundreds of millions of yuan, while multinational corporations (MNCs) were actively seeking pilot partners for their digital and intelligent transformation. Many startups secured collaboration agreements worth billions of yuan with these MNCs.

However, due to a lack of successful case studies in the industry, clinical trials for star products such as DSP-1181 and REC-3599 have ended in failure one after another. Coupled with the Federal Reserve’s continuous interest rate hikes, financing costs in the primary market have remained high. By 2023, both the volume of financing in the global AI-driven new drug development sector and the total value of collaborations with multinational corporations (MNCs) had declined from their peak levels.

Computer vision and internet healthcare are facing similar fates. Both technologies have been deeply integrated into diagnostic and treatment workflows after years of refinement, becoming indispensable components of medical scenarios. However, due to inefficient profit conversion rates, the valuations of related companies and the investment scales of institutional investors have significantly contracted compared to previous years.

From this perspective, NVentures’ timing appears to have been midway up the mountain—on the downhill side.

Let’s examine specific targets in greater detail. Companies that have recently secured financing are also actively seeking to transform and mitigate risks. For instance, when explaining the use of funds, AI-driven drug discovery companies that previously emphasized preclinical research have noticeably decreased such focus; instead, they are shifting toward building technology platforms or increasing investment in business development, thereby aligning themselves more closely with the CXO model.

Most of the medical AI companies held by NVentures are concentrated in preclinical research. A brief overview of these projects: CHARM Therapeutics possesses DragonFold, a protein-ligand co-folding technology based on 3D deep learning, and is engaged in the high-risk development of small-molecule therapeutics targeting cancer and other therapeutic areas that were previously difficult to target; Superluminal Medicines focuses on high-value G protein-coupled receptor (GPCR) targets, producing relevant experimental drug candidates in the shortest possible time, also without any prior precedent to follow.

In other words, in terms of target selection, NVIDIA has also deviated from the trend and confronted risks head-on.

Although neither the timing nor the target selection aligned with the broader trend, NVIDIA’s approach has its own rationale.First, the pace of industry financing does not necessarily align with the pace of technological development; breakthroughs in key technologies typically emerge only after years of sustained effort. Second, the advent of disruptive technologies may restructure the entire industry, thereby redefining the value proposition of each enterprise within it.

Furthermore,NVIDIA also holds the decisive factor of "computing power."In the era of deep learning, algorithms and data dictated model capabilities; however, in the era of large models, computational power may exert a more decisive influence on model capabilities than algorithms and data.

Therefore, regarding generative AI and its related technologies, NVIDIA, with its computational power advantage, is more convinced of its disruptive potential than any investment institution and is more likely than any other enterprise to realize this disruption, thereby addressing the persistent challenges facing current AI and shaping the landscape of a new era in diagnosis, treatment, and pharmaceutical development.

In practical scenarios, the empowering role of technologies such as generative AI across various healthcare settings remains largely at the stage of incremental improvement; only in some frontier research has the potential to fundamentally disrupt these scenarios been identified.

NVIDIA’s most heavily invested area in AI-driven new drug R&D is a typical scenario poised to be disrupted by generative AI. A brief breakdown of the evolution of computer-aided drug development reveals three broad stages: non-computer-aided drug development, Computer-Aided Drug Design (CADD), and Artificial Intelligence-Driven Drug Discovery (AIDD).

CADD can simulate, calculate, and predict the interactions between drugs and receptor biomacromolecules, design and optimize lead compounds, and to some extent reduce the cost of drug development. However, CADD suffers from low hit rates in activity prediction and lacks molecular generation capabilities. Within the existing chemical space, traditional CADD struggles to break away from conventional paradigms to generate drug molecules with novel scaffold structures.

AIDD addresses some of the limitations of CADD. By leveraging models such as recurrent neural networks and generative adversarial networks to learn structural features and rules of chemical molecules from training datasets, AIDD can thoroughly explore chemical space to generate a vast number of novel structures that go beyond the scope of pharmaceutical R&D experts’ experience. It is capable of de novo generation of molecules with specific properties and can also make basic judgments and decisions.

After years of practice, the efficacy of AI-driven drug discovery (AIDD) in reducing new drug development costs remains questionable. This is because AIDD training data are derived from historical marketed drug data and published literature, most of which have been naturally phased out during the iterative process of drug development, thereby making it difficult to develop first-in-class drugs.

Secondly, even if AI-generated compounds demonstrate promising results in vitro, they often fail to meet expectations in vivo. Consequently, although more than 100 AI-discovered new drug candidates worldwide have entered clinical trials, none has yet completed the entire development process; the vast majority remain in Phase I and Phase II clinical trials.

Can generative AI address the critical shortcomings of AI-driven drug discovery (AIDD), namely its lack of creativity and limited utility in in vivo testing? This remains an open question.

In March 2023, NVIDIA launched BioNeMo, a comprehensive suite of generative AI cloud services for customizing foundational AI models, offering algorithmic and computational resources that, in theory, can address the issue of efficacy in in vivo experiments.

According to NVIDIA, BioNeMo provides an innovative computational approach that enables scientists to conduct generative AI research in a low-code, user-friendly environment, thereby reducing the need for experiments and, in some cases, completely replacing them.

Kimberly Powell, Vice President of Healthcare at NVIDIA, believes that the revolutionary power of generative AI has opened up vast prospects for the life sciences and pharmaceutical industries. NVIDIA’s BioNeMo cloud service is now being utilized as an AI-driven drug discovery laboratory, offering pre-trained models and enabling the customization of models with proprietary data to support various stages of the drug development process.This capability enables researchers to identify appropriate therapeutic targets, design molecules and proteins, and predict their interactions within the human body, thereby facilitating the development of optimal drug candidates.。

Publicly available information indicates that NVIDIA has not provided data to substantiate the capabilities of generative AI. However, research by XtalPi, a leading AI-driven drug discovery company, shows that its phage display platform, XpeedPlay, can leverage large models to generate hit antibodies at ultra-high speeds, thereby providing empirical evidence for the efficiency gains enabled by generative AI.

Specifically, while studying the structure of VHH antibodies (natural heavy-chain-only antibodies found in camelid serum, used for cancer treatment, and not naturally occurring in humans), the platform helped XtalPi identify 100 billion of the most promising new VHH antibody sequences by simultaneously optimizing multiple drug-like properties. Meanwhile, the average expression level of the AI-generated sequences was 59.6 mg/L, significantly surpassing the 37.1 mg/L average of the positive control group. Twenty-six sequences were randomly selected for testing, and researchers found that 25 were successfully expressed in vitro recombinant systems, yielding an expression success rate of 96.1%, far exceeding the industry average.

Beyond clinical trials, NVIDIA invested in numerous AI companies focused on preclinical research in 2023 and migrated their R&D operations to the BioNeMo platform, a move that appears aimed at addressing the lack of innovation.

Today, BioNeMo not only boasts computing power that is difficult for other platforms to match, but also hosts more than ten generative AI models, including small-molecule modeling tools, the OpenFold protein prediction model, and the Phenom-Beta model developed with Recursion for target and drug discovery, thereby essentially providing a comprehensive suite of mainstream tools required for preclinical research.

The value of these tools can be indirectly assessed through NVIDIA’s collaborations with life sciences companies. Currently, NVIDIA has reached generative AI cooperation agreements with multinational corporations (MNCs) such as Novartis, Genentech, and Amgen. Bucking the investment trend, NVIDIA may leverage generative AI to reshape the technological landscape and uncover the true value of AI in new drug development.

While the trillion-dollar market for AI-driven new drug development is certainly enticing, NVIDIA has not abandoned “traditional” medical AI application areas such as medical computer vision and internet-based healthcare.

In 2018, NVIDIA launched the Clara platform, providing medical imaging AI researchers with a software development toolkit for medical images to standardize imaging data and accelerate AI training. Several leading domestic medical imaging AI companies are customers of this platform.

Over the following years, NVIDIA Clara has been continuously optimized and expanded, extending its reach into every aspect of computer vision applications in healthcare, a clear testament to NVIDIA’s strong commitment to this business segment.

Unlike AI for new drug development, AI related to computer vision, particularly imaging AI, has long been characterized by a model of “R&D as medical devices, sales as healthcare IT,” resulting in overall weak sales performance and revenues that fail to cover upfront costs.

Therefore, such enterprises urgently need rational tools like generative AI to either reduce upfront R&D time and costs or enhance algorithm generalization, thereby enabling higher average transaction values during the sales process.

At present, there are no cases demonstrating that generative AI can directly improve the generalizability of algorithms; however, the NVIDIA Clara platform has already delivered significant value in reducing R&D time and costs. In 2023, NVentures acquired Flywheel, a leading medical imaging platform, which may further enhance NVIDIA’s platform capabilities.

Furthermore, as domestically produced image-guided surgical robots gained batch regulatory approvals and imaging AI entered the window of opportunity to transition from diagnostic assistance to therapeutic support, NVIDIA also secured stakes in the international market by investing in Moon Surgical, a laparoscopic surgical robotics company, and Neocis, the first surgical robotics company in the dental field.

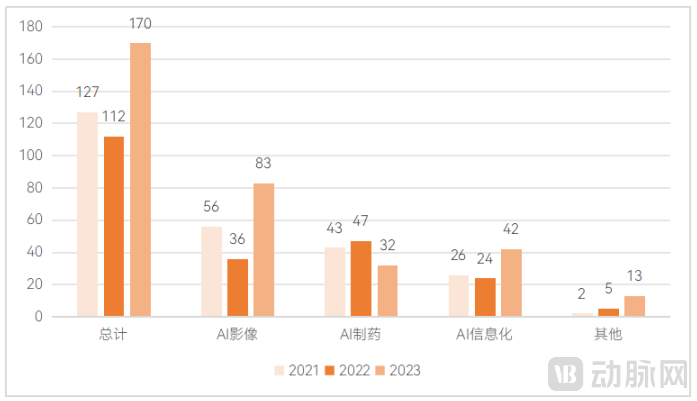

Financing Trends in Different Segments of China’s Medical AI Industry, 2021–2023: Rapid Growth in AI Imaging, Including Surgical Robotics

This is a field even more cutting-edge than drug development. By integrating AI into surgical procedures, NVIDIA would be the first to achieve large-scale deployment in a new healthcare submarket worth hundreds of billions of dollars.

As NVentures’ investments in the healthcare sector are predominantly early-stage, it may take several years to assess the validity of its investment thesis.

What is certain, however, is that the penetration of AI technology across the entire healthcare industry is irreversible. Just as Clinical Decision Support Systems (CDSS) have become standard in primary care and AI-powered imaging has taken root in tertiary hospitals, AI will subtly integrate into pharmaceuticals and medical devices, becoming an essential component.

Therefore, even though large language models have not yet fully demonstrated their value in the healthcare sector, investing in generative AI by following NVIDIA’s lead remains a sound strategy.

After all, in this brand-new AI era, computing power may deliver value far beyond our imagination.