The End of Burn-and-Build: Healthcare Players Are Racing to Boost Revenue in 2024

Amid the harsh winter, the entire healthcare industry is becoming more “materialistic.”

Taking the secondary market as an example, according to incomplete statistics from VCBeat, in less than two months after entering 2024,17 Healthcare Companies Have Terminated Their IPOs. Upon examining the underlying reasons, the primary and most critical flaw is generally “failure to pass financial due diligence,” which includes issues such as losses, or doubts regarding the authenticity and sustainability of performance. In this regard, industry experts have stated, “Currently, the entire A-share market has clear requirements for profitability and the scale of net profit. Therefore, it is basically impossible for loss-making enterprises to go public at present.”'Stable monetization capability' has become a key focus of regulators。”

As the secondary market evolves, the primary market naturally adjusts in response.Investment strategies have gradually shifted from prioritizing team and technology to focusing on commercialization capabilities and profitability.In this regard, some investors stated, “During the market upswing in previous years, most healthcare companies could still secure funding as long as they possessed solid technology or a top-tier founding team. However, over the past one to two years, financing has become problematic for enterprises lacking strong cash flow capabilities or having vague ‘timetables’ for commercialization and profitability.”

In fact, healthcare entrepreneurs have long recognized this reality, with the pressure to generate revenue weighing on them from an early stage. Consequently, over the past period, keywords such as “transformation,” “strengthening commercial capabilities,” and “cost reduction and efficiency enhancement” have frequently appeared on corporate objective lists. For innovative healthcare companies that are both capital- and time-intensive, they have already begun to consider:Should we continue to advance R&D, or slow down to prioritize profitability first?

Not to mention the local governments across China that have been in the spotlight in the healthcare sector over the past year. Burdened with the mandate of attracting investment, they adopt a more pragmatic and direct approach when laying out their healthcare industry strategies, particularly in selecting projects for implementation, where they place significant emphasis on financial statements and cash flow conversion capabilities.

Therefore, from any perspective, “profitability” has become a consensus across the entire healthcare industry. What, then, are the underlying logics driving this trend? Furthermore, what effective strategies and best practices can the industry currently draw upon to enhance profitability? Finally, how should healthcare enterprises navigate the challenging trade-off between long-term value creation and short-term financial gains?

The Era of Securing Financing with Just a PowerPoint Presentation Has Passed

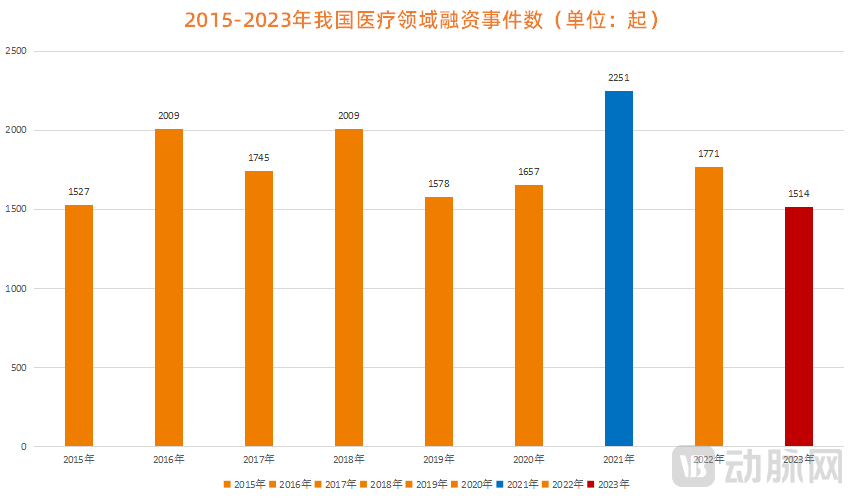

Financing in the primary market is becoming increasingly difficult. From the most intuitive perspective, according to incomplete statistics from the VCBeat Orange Database,In 2023, China’s healthcare sector completed a total of 1,514 financing rounds, representing a year-on-year decline of 15.51%. Compared with the peak year of 2021, the number of financing events decreased by nearly 1,000.。

Comparison of the Number of Financing Events in China’s Healthcare Sector, 2015–2023 (Data Source: VBInsight)

Comparison of the Number of Financing Events in China’s Healthcare Sector, 2015–2023 (Data Source: VBInsight)

Amid this sharp decline, enterprises are the ones most acutely feeling the impact. Multiple interviews conducted by VCBeat have revealed that over the past year or two, healthcare companies have gone to great lengths to secure financing. The more respectable approach involves incessantly participating in various roadshows and continuously engaging with diverse investors, while the less dignified route entails lowering valuations and raising capital at a discount. Yet even so, their efforts often fall short of expectations.

However, healthcare companies that manage to secure financing are not faring much better; they, too, are treading on thin ice. According to a leading investor, a biotech startup with promising technological prospects recently raised only RMB 10 million in its angel round.The core team had to pay out of their own pockets and collectively take a 50% pay cut just to barely sustain the company’s normal operations and development.. In response, investors stated that if the project had raised funds during the industry’s peak years, the amount secured would have been at least two to three times higher than it is now.

The primary reason for this disparity lies in investors’ heightened emphasis on the “monetization capability” of portfolio companies. In light of this, investors explained, “As the market cools, investors are becoming more cautious; meanwhile, their available capital has dwindled. Consequently, they are continuously compressing investment return horizons and placing greater emphasis on the profitability of their portfolio companies.。”

If this is the case in the primary market, the secondary market, which places greater emphasis on authenticity, is naturally even more direct. It is reported that among the nearly 17 healthcare companies that failed their IPOs this year, 90% were stalled by financial issues—either remaining unprofitable or experiencing significant declines or volatility in performance.

Taking the IVD sector, a “hard-hit area” for failed IPOs, as an example, throughout 2023,No Companies Listed on the A-Share Market Throughout the Year, the underlying reason is that as the pandemic subsided, demand for related testing plummeted, leading to a precipitous decline in overall revenue. For non-pandemic-related healthcare companies, their “performance instability and poor growth potential” are primarily attributable to their small market share or extreme reliance on a single product or customer.

In this regard, an investor remarked, “The market benefits driven by contingent events such as the COVID-19 pandemic are not truly competitive. As the epidemic subsides, the initial windfall will quickly turn into pressure on the company’s future performance, given that neither regulators nor the market look favorably upon a company whose financial results deteriorate shortly after its IPO.” This is also evident from the frequent use of terms like “market size” and “sustainability” in the inquiry letter, which underscores the core focus on assessing the company’s monetization capability, as it directly impacts post-listing performance.

Of course, it is not only the capital market that cares about “liquidity”; in fact,In certain niche sectors, commercialization and monetization have already reached maturity.。

For instance, in the field of AI healthcare, a senior executive at an AI large-model startup told VCBeat, “Although investors remain optimistic about AI large models and generally maintain a high level of tolerance, pressures have mounted after a period of development. Currently, many investors place significant emphasis on ‘financial statements,’ paying particular attention to the ‘timeline’ for profitability among large-model companies.”This is because the long-standing model of unchecked cash burn is facing challenges, with some investors beginning to focus on when AI companies will ultimately achieve self-sustaining profitability.。

The same holds true in the field of brain science. Although earlier this year, Neuralink, Elon Musk’s brain-computer interface company, implanted a brain chip in its first human patient, boosting confidence across the industry, returning to the market itself, after years of focusing primarily on technology and future speculations,Current investors have also begun to focus on the ability of brain-computer interface companies to "deliver results.", namely, whether the core product has been registered and approved, whether it is recognized in the clinical market, and whether there are paying customers, among other factors.

In short,“The era of burning cash” has generally come to an end, with the entire healthcare industry now focused on revenue.。

How Innovative Drugs Achieve Profitability: “Strategic Flexibility” Is Key

Everyone knows that the healthcare industry is in the midst of a harsh winter, yet no one knows when this winter will end.. Nevertheless, even so, an industry consensus has already been formed, namely thatEveryone is exploring more diversified "profit models"。

Take the innovative drug sector as an example. Many view 2024 as a pivotal year for Chinese pharmaceutical companies to realize the value of their innovation achievements. A review of numerous annual reports from the past two years reveals that these companies have largely converged on a consistent strategy: cost reduction, efficiency enhancement, and focus. Leading pharmaceutical firms, in particular, are sending a clear signal to the market through their actions and data:At the appropriate time, know when to appropriately “bow your head” and seek change.。

In this regard, an investor remarked, “In the days ahead, pharmaceutical companies’ ‘rules for survival’ should be relatively flexible,”On the offensive front, it can accelerate product commercialization, empower its own sales team, and achieve self-sustaining revenue generation; on the defensive front, it allows for bundling assets to identify suitable buyers and enable a clean exit.。”

Specifically, innovative pharmaceutical companies must first proactively embrace cash flow management. On one hand, they should form strategic alliances to address their own weaknesses, thereby accelerating product development and commercialization. On the other hand, they need to actively transform by adjusting their pipeline strategy through in-licensing, making new choices in disease areas.

For instance, a large number of pharmaceutical companies have concentrated their efforts on the medical aesthetics sector in recent years. Although their strategies for entering the medical aesthetics market vary, current performance has confirmed that expanding into medical aesthetics can serve as a second growth curve for revenue development. Taking Huadong Medicine as an example, according to its latest financial report, the company’s medical aesthetics segment generated RMB 1.874 billion in revenue during the first three quarters of 2023, representing a year-on-year increase of 36.99%.

Of course, one must not view things from only one perspective. While profits are being made, problems also arise; namely, although the newly developed medical aesthetics business is profitable, it requires continuous investment of capital, manpower, and resources. Therefore,Balancing Multiple Core Business Lines: A Critical Test of Pharmaceutical Companies’ Ability to Manage Collaborative and Parallel Operations。

However,Proactively embracing cash flow, pursuing diversified collaborations, and optimizing pipeline and asset allocation are undoubtedly critical strategies for many domestic innovative pharmaceutical companies to achieve sustainable operations at the current stage.. However, if none of the aforementioned pathways prove viable, exiting at an appropriate juncture may well be a prudent choice.

In this regard, investors also expressed agreement. He stated, “Over the next 5 to 10 years, more than a thousand domestic innovative pharmaceutical companies will undergo natural selection through upgrades, transformations, mergers, and restructurings. However, only a small proportion will emerge as winners, while the majority will achieve transformation and sustained survival through integration-driven exits and strategic pivots.”

So, how can one make a graceful exit?Either being acquired by large domestic or international pharmaceutical companies to become part of their product pipelines or technology systems, or forming new consortia with large CDMO enterprises and professional CSO firms.。

In fact, such approaches are relatively common in European and American markets. However, China currently lacks the mature ecosystem to support them. This is due to the absence of truly large-scale biopharmaceutical companies and professional Contract Sales Organizations (CSOs) in the country. Furthermore, continuous capital inflows have led to significant valuation bubbles for many innovative drug developers, resulting in an inversion between primary and secondary market valuations. Additionally, these companies still demonstrate a strong preference for independent operations. All these factors contribute considerable uncertainty to this pathway.

But from"Big Fish Eat Little Fish"From the perspective of underlying logic, allowing struggling innovative pharmaceutical companies to merge with mature pharmaceutical enterprises not only relieves “small fish” of the immense pressure from repurchase valuation adjustment mechanism (VAM) agreements, but also injects innovative talent and capabilities into “big fish.” This approach mitigates talent loss to a certain extent and accelerates the metabolic turnover of the entire industrial ecosystem.

Recent industry data has been gradually validating this point. According to statistics from Zero2IPO Research, domestic IPOs in China declined by 13% year-on-year from January to October 2023, while mergers and acquisitions (M&A) increased by 29.9% over the same period. This trend signals that private equity (PE) and venture capital (VC) firms have begun to embrace M&A as an exit strategy amid the current phase of tighter IPO regulations.

Key Profit Drivers for Medical Device Companies: Global Expansion, a “Two-Legged” Strategy, and a Graceful Exit

Having discussed innovative drugs, we now turn our focus to another hot sector: medical devices.

In fact, compared with innovative drugs, medical devices face greater uncertainty in commercialization: First, the sector is highly fragmented with intense competition, and there are limited therapeutic areas capable of yielding blockbuster products. Second, accurate understanding of clinical needs is critical; even with rapid regulatory approval, whether product design truly meets clinical demands remains a key determinant of success. Third, academic promotion capabilities are essential. Unlike in the past, when established markets were readily available, domestic medical device companies must now proactively educate and develop the market.

In addition, the long-term monopoly of overseas giants in many niche sectors is a significant issue. For instance, a medical device company that recently terminated its IPO ranked among the top domestic manufacturers in terms of market share, yet it still lagged considerably behind international leaders. Consequently, regulators questioned its market potential. Furthermore, the impact of “volume-based procurement” cannot be overlooked, as it directly lowers the industry’s growth ceiling, thereby affecting the overall size of the end-market.

So, against this backdrop, how can domestic medical device companies break through in terms of commercialization?

According to an industry expert's analysis,As domestically developed innovative medical devices continue to reach the market with policy support, the bottleneck to profitability has gradually shifted from the R&D and manufacturing stages to the commercialization stage at the downstream end of the industry chain., therefore, for medical device companies,The primary approach to achieving self-sustaining growth is to collaborate in addressing operational “bottlenecks.”. For instance, the recent collaboration between Medis Medical and Baiyang Pharmaceutical aims to leverage Baiyang’s professional brand operation and promotion capabilities to rapidly bring its independently developed innovative devices to market.

Of course, “going global” is also one of the highly watched paths. On the eve of the Spring Festival, VCBeat conducted exclusive interviews with 15 leading institutions,They all regard global expansion as a highly significant industry trend this year., with two core reasons: first, after years of accumulation and refinement, certain innovative products from Chinese medical device companies have gained a degree of competitiveness globally; second, influenced by the domestic market environment, expanding overseas also means greater market potential and profit margins.

However, global expansion also presents significant challenges. As “going global” is a broad concept encompassing numerous countries, profitability varies by market—some countries offer lucrative opportunities while others do not. Therefore, selecting the right markets and adapting to local market dynamics are both critical.

Therefore, it is not difficult to observe that over the past year, investors have been making multi-dimensional efforts to support their portfolio companies in expanding overseas. For instance, in 2023, Matrix Partners China’s core team traveled globally to visit numerous large enterprises and startups, with the primary objective of helping its portfolio companies seek opportunities for international business collaborations, investments, and mergers and acquisitions. Entering 2024, Matrix Partners China will continue to adhere to this strategy.

Legend Capital is no exception. According to Wang Junfeng, Co-Chief Investment Officer of Legend Capital, the firm has taken the lead in entering the Southeast Asian market through its healthcare investments. It has invested in several platform-based enterprises, facilitating the deployment of Chinese technologies and assets in Southeast Asia. In Indonesia, in particular, Legend Capital has guided more than 40 Chinese companies into the market and engaged in direct dialogue with the Indonesian Ministry of Health, the National Agency of Drug and Food Control (BPOM), and other regulatory authorities.

However, “going global” primarily applies to relatively mature medical device products. For device sectors still in the exploratory phase, there should be a distinctly different path toward achieving self-sustainability. For instance, in the field of brain science, Yang Zhiwen, Founding Partner of Nuoyu Capital, once stated, “Currently,Neuroscience companies should pursue long-term value and remain committed to cutting-edge innovation, while also being adept at capturing short-term gains., products capable of continuously generating cash flow over the next two to three years.”

This constitutes the core logic behind why medical device companies must pursue a “two-pronged” strategy to maintain their competitive edge: one prong represents traditional business lines that generate the primary cash flow, while the other consists of continuously iterated innovative products that offer substantial profit margins. In this regard, a medical device investor remarked, “You cannot rely on a single product to dominate the market indefinitely. When certain products are included in volume-based procurement programs, there must be other innovative products to sustain high profitability. This is also the key reason why investment institutions are currently placing particular emphasis on platform-type companies.”

Certainly, M&A exit is also a major option for many medical device companies to convert their cash flow. In fact, the growth of most global medical device giants has been inseparable from wave after wave of M&A booms. However, similar to innovative drugs, China does not yet have a relatively mature M&A market; relevant M&A data are not particularly striking, and the overall acquisition pace in both the primary and secondary markets remains relatively slow. Nevertheless, investors have already begun to recognize this trend. A senior medical device investor told VCBeat, “"If a portfolio company approaches us now expressing interest in being acquired, we would be very supportive of such an outcome."。”

Balancing Competing Demands: How to Make Trade-offs and Achieve Equilibrium?

Continue R&D, or Prioritize Profitability?This is an issue facing the vast majority of healthcare professionals today.

If asked a few years ago, at the height of the healthcare industry’s boom, most people would have unhesitatingly answered: R&D. However, in light of the current market winter, companies are facing significant survival challenges, and thus the answer has changed; most people would now prioritize profitability first.

This is understandable, as R&D investment can certainly help a company move faster, but strong commercialization capabilities enable it to go further. However,In the current market environment, the industry should demonstrate greater patience and confidence in the monetization and profitability of healthcare enterprises.。

Meanwhile, for the entire healthcare industry, it is inappropriate to “condemn everyone outright” simply because of current constraints imposed by profitability demands, after all, in the medical field,Addressing Unmet Clinical Treatment Needs Is an Evergreen Topic, in some cutting-edge niche areas, the industry still requires substantial investment. The challenge, however, lies in determining how to support such capital-intensive projects that demand years of solitary perseverance and carry a high risk of failure—a path that all stakeholders are currently exploring.

However, regardless of the circumstances, from the perspective of the current overall macro environment,It is imperative to prioritize operating cash flow and free cash flow., this is the bargaining chip for healthcare professionals to continue competing fiercely within the industry.

1. “Where Will the Pharmaceutical Industry Head in 2024 After the Darkest Hour?” — Deep Blue View;

2. “Don’t Criticize Chinese Large Model Companies for Their Profitability” – Huxiu;

3. “Cost Reduction, Efficiency Enhancement, and Focus: How Hengrui, Fosun, CSPC, and Others Are Seizing New Opportunities Through Transformation” – E-Drug Manager;

4. “IPO Breaks, M&A, and Sell-offs: Where Is the Future Direction for Biotech?” — New Pharmaceutical Technology;

5. “Innovative Medical Devices Under the Spotlight: The Safe-Haven Attribute Shattered” — Device Home