Headwinds for CDMO Leaders and Oversupply Concerns: Does the Industry Still Have a Future?

WuXi AppTec

New Drug R&D and Production Service Provider

WuXi XDC

End-to-End CDMO Service Provider for Biologics Conjugation Drugs

On February 14, the first trading day for Hong Kong stocks after the Spring Festival, shares of the WuXi group plummeted. By market close, WuXi AppTec had dropped more than 18%, WuXi XDC over 8%, and WuXi Biologics over 9%. This followed a sudden plunge on January 26, just before the Spring Festival, when WuXi AppTec and WuXi Biologics closed down 10% and 18%, respectively. The sharp decline in WuXi group stocks also dragged down the Hang Seng Innovative Drug ETF, which fell 7.65% by the end of the day.

It is not only the WuXi group that has been affected; the stock prices of other CDMO companies, including Pharmaron, Tigermed, and Asymchem, have also been impacted.

The incident stemmed from the “Biosecure Act” proposal submitted by a U.S. legislator, and WuXi AppTec issued three clarification announcements on January 27, February 5, and February 19.

The market is highly sensitive because overseas markets, particularly U.S. clients, constitute a significant source of revenue for domestic CDMO companies. For instance, 65.67% of WuXi AppTec’s total revenue in the first three quarters of 2023 came from U.S. clients. In 2023, overseas revenue accounted for approximately 80% of WuXi Biologics’ total revenue, with more than half of its projects originating from North America. Other companies, including Asymchem, Pharmaron, and Porton Pharma Solutions, have also derived over 80% of their revenue from overseas business in recent years.

Of course, the proposal is merely a trigger. The weakening performance, shifts in the broader macroeconomic environment, and intensifying industry competition are the challenges facing the CDMO sector. Only by addressing these issues can the industry regain market trust.

The outbreak propelled the CDMO industry into the spotlight. Now, in the post-pandemic era, the crisis of overcapacity and shifts in the macroeconomic environment have once again placed the CDMO sector at a crossroads of destiny.

Taking Asymchem as an example, its financial report shows that the total revenue from January to September 2023 was approximately RMB 6.383 billion, a year-on-year decrease of 18.29%. The revenue from small-molecule CDMO services was RMB 5.565 billion, down 22.01% year on year. Although Asymchem stated that, after excluding the impact of large orders, its small-molecule CDMO business achieved a year-on-year growth rate of 25.5%, its performance, as a leading enterprise in China’s small-molecule CDMO industry, also reflects the broader industry trends.

Another CDMO company, Porton Pharma Solutions, released its annual earnings forecast, projecting total revenue for 2023 to be between RMB 3.517 billion and RMB 3.869 billion, representing a year-on-year decline of 45%–50%. The previously reported third-quarter results showed that revenue from its small-molecule CDMO business amounted to RMB 2.942 billion, down 43% year on year.

Others, such as Hepalink Pharmaceutical, saw a 15.55% year-on-year decline in its CDMO business in the first half of 2023, while Jiuzhou Pharmaceutical also experienced a 6.79% year-on-year decline in the third quarter of 2023.

As a technology-intensive industry, CDMO requires a large pool of specialized technical talent. In the past, the sector experienced rapid growth by leveraging the “engineer dividend.” The pandemic triggered an explosive surge in the industry, with capacity rapidly expanded, allowing CDMO companies to ride this wave of favorable momentum. However, as the impact of the pandemic waned and orders declined, the drawbacks of overcapacity quickly became apparent, ushering the industry into a period of adjustment.

On one hand, there is overcapacity; on the other, downstream companies have begun to seek upstream transformation, leading to significant changes in the ecosystem of China’s CDMO industry.

In addition to professional CDMOs such as Asymchem and Porton, some pharmaceutical companies that previously acted as clients are beginning to venture into the CDMO business.

such as Antairui Lin, a subsidiary of Henlius; Chembio, a subsidiary of Innovent Biologics; Funeng Bio, a subsidiary of Tianshi Real/Betta Pharmaceuticals; Taikang Bio, a subsidiary of Mabwell; Shengguo Bio, a subsidiary of 3SBio; Youdao Bio, a subsidiary of Yangshengtang; Baifan Bio, a subsidiary of Guilin Sanjin; and Yi'an Jishi, a subsidiary of Transcenta Holding.

In the past, during a period of high growth in innovative drug R&D, many pharmaceutical companies began expanding their production capacity. However, as the growth of innovative drug R&D slowed, or when marketed drugs failed to achieve expected sales volumes and subsequent product pipelines could not keep pace, this idle capacity became an issue that had to be addressed. Particularly in the current environment, businesses capable of generating cash flow are highly attractive to enterprises. Therefore, transforming excess capacity into a CDMO platform has become a rational choice for many pharmaceutical companies.

On the other hand, intensifying industry competition has also hindered CDMO companies in their initial public offerings (IPOs). For instance, in January 2024, two CDMO companies consecutively withdrew their applications from the Beijing Stock Exchange. A review of the inquiry records clearly reveals the regulators’ emphasis on the stability of production and operations.

In such a macro environment, the domestic CDMO industry will inevitably face intense involution. Amidst this turmoil, it is not only domestic CDMOs that are affected; some foreign-invested CDMOs are also feeling the chill.

Not only in China, but CDMO companies abroad are also beginning to show signs of divergence.

Recently, Lonza, a global CDMO giant, decided to close its biotechnology plant located in the Sino-Singapore Guangzhou Knowledge City within the Guangzhou Development District. This facility was Lonza’s third plant in China and the ninth biotechnology plant in its global network, with a total investment exceeding $100 million. Shortly before this, Lonza had just announced the closure of its mammalian clinical production facility in California, USA, resulting in 218 layoffs.

Lonza’s rationale for the successive closure of two plants was straightforward: a lack of orders. Although the shutdowns resulted in CHF 183 million in asset impairment losses and an additional CHF 50 million in restructuring-related costs, they did not deter Lonza from proceeding with the plant closures.

As a global leader in pharmaceutical CDMO, Lonza’s decision to shut down its Guangzhou Knowledge City plant reflects numerous issues. Not only is Lonza, as an industry giant, affected, but other foreign-invested CDMOs are also facing declining performance.

New Vision Pharmaceuticals, a CDMO established in 2012, shut down its aseptic blow-fill-seal production facility in Florida, USA, in February 2024. Acquired by Morgan Stanley Strategic Value Investing in 2018, the CDMO was still expanding its business through the acquisition of competitors’ assets just two years prior. Only two years later, it faced a turning point.

Not only New Vision, but since 2023, multiple CDMO companies have encountered business crises.

In August 2023, Emergent BioSolutions announced a reduction in investment in its CDMO services business, de-emphasizing its growth, and laid off more than 400 employees. Emergent BioSolutions was once ranked first among the top ten CDMOs combating the novel coronavirus by Fierce Biotech. However, its CDMO business has suffered significant setbacks following the exposure of quality standard issues.

Thermo Fisher Scientific was not spared from this wave of business downturn. In February 2023, it laid off 230 employees across its three production sites in San Diego, including engineers and scientists engaged in manufacturing. In April, it closed a plant in Princeton, New Jersey, resulting in 113 layoffs. In May, a second round of layoffs affected 218 employees at its three San Diego facilities. In August, it planned to cut 205 jobs at its plant in Alachua, Florida. In November, it announced the closure of its facility in Auburn, Alabama, with 97 employees laid off.

As industry pioneers, including Lonza, Thermo Fisher Scientific, and Boehringer Ingelheim, they bring extensive experience and technical capabilities in development, manufacturing, regulatory registration, and supply. While entering the Chinese market, they have also introduced management philosophies, technical standards, and talent development models, thereby contributing to the growth of China’s CDMO industry.

On the one hand, the adage “teach the apprentice, starve the master” holds true; as domestic CDMOs develop, they face intensifying competition. On the other hand, amid shifts in the global landscape, both domestic CDMOs and multinational CDMOs are confronting the strong rise of competitors from South Korea and India.

Chinese companies, long known for their fierce internal competition, are now facing intense pressure from CDMO firms in South Korea and India.

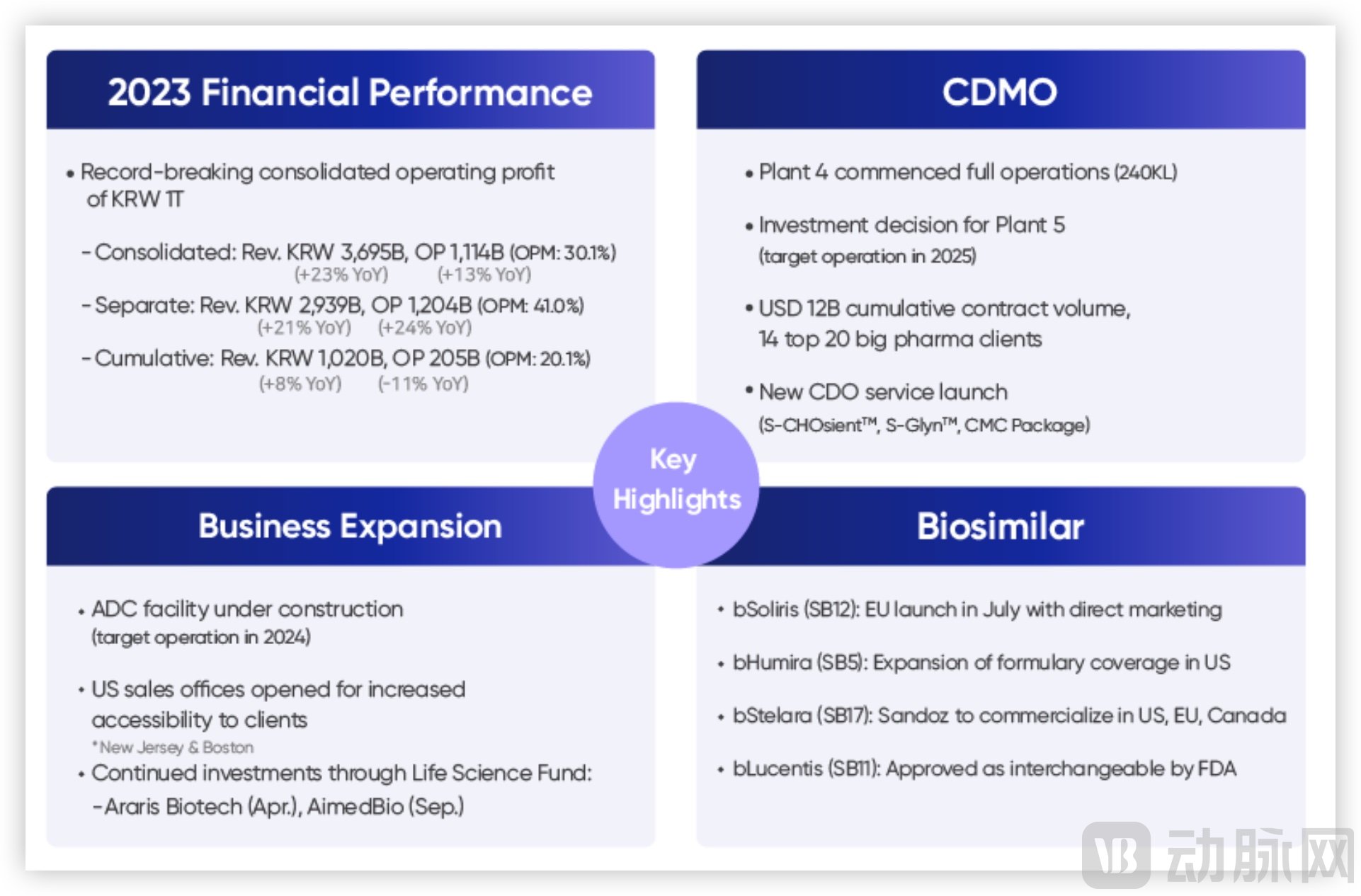

According to the 2023 annual report of Samsung Biologics, its total revenue reached KRW 3.69 trillion (approximately USD 2.76 billion), with profits amounting to KRW 1.1 trillion (approximately USD 800 million). This not only set a new historical high for the company but also made it the first biotechnology firm in South Korea’s history to achieve annual profits exceeding KRW 1 trillion.

In April 2023, the Korea Bio Industry Association (KBIA) and the Biotechnology Innovation Organization (BIO) of the United States signed an agreement focused on strengthening cooperation in the bioeconomy sector, marking the first such accord between the two parties. Under the agreement, both sides will work together to ensure stable supply chain management, including sharing information on policy changes. Additionally, they will enhance information exchange in areas such as research and development, drug manufacturing, and market trends.

Subsequently, a large volume of orders from the United States poured in. In June, Samsung Biologics secured a $411 million long-term partnership with Pfizer; in July, Pfizer placed an additional order worth $897 million. Meanwhile, CDMO orders from Roche continued to increase, reaching a total value of $213 million, with both parties agreeing to extend the contract term from the end of 2024 to the end of 2027. Thereafter, Samsung Biologics reached a letter of intent for a CDMO collaboration valued at $1.12 billion with a U.S. biopharmaceutical company.

Securing large-scale clients has been the primary driver behind Samsung Biologics’ explosive performance growth. From 2016 to 2019, its client base consisted mainly of small and mid-sized biotech firms, with multinational corporations (MNCs) gradually emerging as customers starting in 2020. By 2023, Samsung Biologics disclosed in its financial report that 14 of the top 20 global pharmaceutical companies were its clients, contributing over $1.2 billion in revenue.

Thanks to the commissioning of its fourth plant in the second half of 2023 and the full utilization of capacity at Plants 1–3, Samsung Biologics has reaped substantial rewards. According to Samsung Biologics, Plant 4 is still in the ramp-up phase and is expected to contribute approximately 30% of revenue in 2025. The combined capacity of all four plants currently stands at 604,000 liters, surpassing that of Lonza and Boehringer Ingelheim. Construction of Plant 5, with a planned capacity of 180,000 liters, has already begun and is scheduled to start operations in April 2025, five months ahead of schedule.

Not only Samsung Biologics, but also South Korean CDMOs such as SK pharmteco and Lotte Biologics are rapidly expanding their production capacity.

On the other hand, competitors from India are also exerting significant pressure on domestic CDMO companies in the small-molecule CDMO sector.

India’s four major CDMOs—Syngene, Aragen Life Sciences, Piramal Pharma Solutions, and Sai Life Sciences—all achieved significant growth in their 2023 performance.

Sai Life Sciences reported a 25%–30% increase in sales in recent years, with production capacity nearly doubling since 2019 and expected to rise by another 25% in 2024 to meet demand. It is not only Sai Life Sciences; several other companies have also reported significant profit growth in recent quarters. For instance, Aragen attributed part of its revenue growth to new contracts with new clients, including several among the top 10 global pharmaceutical companies.

In addition to shifting orders overseas, these pharmaceutical companies also hope to establish India as a second manufacturing hub outside of China and build their own supply chain systems. Taking Piramal Pharma as an example, approximately 15% of its active pharmaceutical ingredients (APIs) currently come from China, and the company is rebuilding its supply chain system in response to customer demands.

Over the past two decades, Chinese CDMO companies have remained the preferred choice for related business activities, driven by the industry’s advantages in low cost and high efficiency. This supply-demand dynamic reached its peak during the outbreak of the pandemic. However, as the impact of the pandemic wanes and the international landscape shifts, many foreign pharmaceutical companies are beginning to seek alternative suppliers in their supply chains to mitigate potential risks.

Against this backdrop, Indian CDMOs have been able to absorb outsourced orders, ushering in a period of rapid growth.

Mordor Intelligence, an India-based consulting firm, estimates that the revenue of India’s CDMO industry was $15.6 billion in 2023, compared with $27.1 billion for China’s CDMO industry. Over the next five years, India’s CDMO sector is projected to grow at a rate exceeding 11%, while China’s is expected to expand at approximately 9.6%.

After nearly a decade of rapid growth, China’s CDMO industry is facing challenges from South Korea and India.

Faced with numerous adverse factors, what should domestic CDMO enterprises do? Perhaps we can draw some lessons from the practices of our competitors.

Taking Samsung Biologics as an example, the company has begun to actively strategize for the future to sustain its performance. Its CEO stated that, in addition to continuing capacity expansion to accommodate more orders, the primary tasks are to complete cGMP certification for its antibody-drug conjugate (ADC) production facilities by 2024 and to construct relevant production facilities for biosimilars.

Samsung Biologics Targets ADCs and Biosimilars as Key Growth Drivers for 2024; Image Source: Company Website

Another established CDMO, Charles River, also announced its financial results for Q4 2023 and the full year 2023 on February 14. Although Q4 revenue decreased by 7.9% year-over-year, it maintained a 9.2% quarter-over-quarter growth, and full-year 2023 revenue increased by 3.9% year-over-year. The key driver was the incremental growth from the CGT (cell and gene therapy) sector, which kept the CDMO business on a growth trajectory.

In other words, these CDMO companies, which are still in their growth phase, are focusing on capacity building beyond just manufacturing capabilities to attract more orders from niche segments.

In the past two years, enthusiasm for the research and development of innovative antibody-drug conjugate (ADC) drugs has surged. According to Frost & Sullivan, there have been over 100 ADC-related transactions since 2022, with the total transaction value exceeding $6 billion since 2024. This downstream fervor has naturally invigorated the upstream sector. Frost & Sullivan projects that the global ADC CDMO market size will reach $11 billion by 2030, representing a growth of more than 600% compared to 2022.

In this context, an increasing number of domestic CDMO companies are beginning to position themselves in the ADC sector. Traditional CDMOs such as WuXi XDC, Porton Pharma Solutions, and Asymchem, along with companies that have transitioned from ADC drug development, including Allorion Therapeutics, MabPlex, and Sherpa Biologics, as well as Haoyuan Chemexpress, which entered the ADC field early on, have all become key players in China’s CDMO industry’s ADC sector.

Taking Porton Pharma Solutions as an example, after its ADC drug R&D center in Shanghai became operational in September 2023, the company invested an additional RMB 1.085 billion to expand its ADC commercialization platform in Chongqing. This expansion includes the construction of two new antibody drug substance production lines, two ADC conjugation production lines, one ADC conjugated drug product filling line, and one fully automated packaging line, achieving an annual production capacity of 46,080 kg of ADC conjugated drug substance and 2.2 million vials of finished ADC conjugated drug products.

WuXi XDC’s new commercial-scale biologics conjugation drug substance and drug product manufacturing facilities in Wuxi commenced operations in the second half of 2023. Overall production capacity is projected to expand to approximately six times its 2019 level by late 2025 to early 2026. As China’s first ADC CDMO to go public, WuXi XDC has grown alongside its existing clients by providing services from the early stages of the product development cycle. As these early-stage clients progress toward later-stage and commercial phases, WuXi XDC is poised to achieve significant additional revenue growth in the future.

As can be seen, both WuXi XDC and Porton PharmaSolutions are evolving toward one-stop, end-to-end CDMO services to meet the demands of ADC manufacturing processes and deepen client stickiness. Competition in the ADC CDMO sector has only just begun.

Furthermore, CDMOs have also begun to position themselves in the emerging CGT sector.

Similar to ADCs, the manufacturing process for CGT is more complex; however, possessing relevant one-stop capabilities makes it more attractive to customers.

Consequently, listed companies such as WuXi AppTec, Pharmaron, and Porton Pharma Solutions have already established their presence in this sector, with their related businesses achieving varying degrees of growth. Meanwhile, CDMO enterprises including Baizhino Biologics, Bayo Biosciences, VectorBuilder, Junhou Biologics, Auscan Biologics, PackGene, and Yiming Cell Therapy are also actively involved. Furthermore, certain cell and gene therapy (CGT) companies have transitioned into CGT CDMOs, such as GenScript ProBio, Puruijin Biotech, and Wujiahe Gene.

As the first CGT CDMO listed on the STAR Market, Obio Technology has cumulatively served over 150 related projects and, by 2023, had established a CDMO platform comprising 15 GMP vector production lines and 20 GMP cell production lines. Porton Biologics has completed the construction of its gene and cell therapy CDMO industrialization base in Suzhou, expanding its capacity to include 10 viral vector production lines and 12 cell therapy production lines.

On February 20, WuXi Advanced Therapies, a subsidiary of WuXi AppTec, announced that the U.S. Food and Drug Administration (FDA) had approved its Philadelphia facility for the analytical testing and manufacturing of AMTAGVI. As a result, WuXi Advanced Therapies’ Philadelphia site has become the first CTDMO (Contract Testing, Development, and Manufacturing Organization) in the United States to receive FDA approval for supporting the commercial production of personalized T-cell therapies for solid tumors. As the first FDA-approved, one-time-use, personalized T-cell therapy product for the treatment of solid tumors, AMTAGVI imposes numerous requirements on manufacturing processes. This approval further validates WuXi AppTec’s capabilities.

In the future, as cell and gene therapy (CGT) expands from hematologic malignancies to solid tumors and from rare diseases to common conditions, a wave of immune cell therapies—including tumor-infiltrating lymphocyte (TIL) therapy, T-cell receptor-engineered T-cell (TCR-T) therapy, and chimeric antigen receptor natural killer (CAR-NK) cell therapy—will continue to emerge, driving further growth in the CGT contract development and manufacturing organization (CDMO) sector. In addition, peptide drugs, which also feature complex manufacturing processes and challenging cost control, represent another new source of growth for the CDMO industry.

As the number of market entrants increases, the CDMO industry inevitably undergoes consolidation.

On February 5, Novo Nordisk announced the acquisition of CDMO giant Catalent for $16.5 billion (approximately RMB 119 billion). It is not only Novo Nordisk; in recent times, multinational corporations (MNCs) such as Daiichi Sankyo and AbbVie have also been expanding their own production capacities, aiming to bring manufacturing in-house rather than relying on contract development and manufacturing organizations (CDMOs).

The halo of the CDMO “water seller” role is gradually fading.

For CDMO companies, tangible challenges include price pressures from clients, an increasing number of industry competitors, and the flow of new growth in emerging sectors toward leading enterprises. In response to intense competition in the domestic market, some companies have begun targeting overseas markets, where competition is equally fierce.

“It is less a case of overcapacity and more one of insufficient effective capacity—that is, production capacity recognized by overseas clients,” an industry practitioner told VCBeat. Overseas clients place greater emphasis on the internationalization capabilities of CDMO enterprises and their track record of successful past projects.

For CDMO companies to truly embark on a path of rapid development, they cannot rely merely on paper-based capacity and technology; rather, success depends on qualifications and client trust accumulated over the long term, as well as the experience embedded within their organizational structures through project collaborations. Even industry leaders in China such as the WuXi group have only about 20 years of history, making this aspect particularly lacking for many emerging CDMO enterprises.

Effectively managing cross-regional and cross-time-zone teams to ensure optimal resource allocation and maximize productivity poses a significant challenge for emerging CDMO companies during business expansion. Only by addressing these issues—while scaling up operations and capacity, maintaining quality control, optimizing costs, and ensuring on-time delivery—can these companies survive in the fiercely competitive market.

The CDMO industry is currently in a period of adjustment following a decade of rapid growth, during which certain changes, and even structural shifts, are inevitable. While companies must adapt to the changing macro environment, the key to surviving this adjustment phase lies in their technological capabilities, quality control, validated projects, and extensive track record of success.

References:

2024 VC forecast:Clinical-stage CDMOs likely to have uptick in demand but specialization critical

Reuters:Indian drug manufacturers benefit from Big Pharma interest beyond China