Healthcare Giants Slash Costs Amid Market Shift: Amazon, CVS, and Walgreens Pivot to Efficiency

One Medical

Digital Basic Medical Service Provider

Amazon

International E-commerce Website

Amazon Pharmacy

Online Pharmacy Service Provider

Not long ago, Amazon announced the elimination of approximately 115 positions within its One Medical and Amazon Pharmacy divisions, with the final number of layoffs potentially exceeding 400. This move has sparked rumors about whether Amazon is poised to exit the healthcare market. However, Amazon stated that this adjustment is actually a step toward cost reduction and efficiency improvement—as part of Amazon’s 2024 targets, the healthcare division is required to cut costs by $100 million.

It’s not just Amazon; its competitors have recently been racing down the same path. These once deep-pocketed “big players” are now scrutinizing every expense. Cost reduction and efficiency improvement have become the dominant themes at the start of 2024.

Amazon has long harbored significant ambitions in the healthcare sector and has made rapid strides over the past one to two years. In early 2023, in particular, Amazon delivered a modest shockwave by leveraging its financial might, successfully completing all regulatory reviews and finalizing its acquisition of One Medical. In this acquisition battle, Amazon outmaneuvered retail pharmacy giant CVS with a purchase price of $3.9 billion—the third-highest in its corporate history—exerting substantial pressure on its competitors.

In the United States, patients seeking medical care at a hospital typically need to schedule appointments with physicians well in advance, with consultation times determined by the doctors’ availability. After waiting for weeks or even months, patients arrive at the hospital as scheduled, only to face lengthy queues at the front desk and complete cumbersome paperwork, including personal information and medical history forms.

In fact, this is almost a common ailment faced by healthcare systems worldwide.

One Medical is a membership-based community healthcare service platform that operates both offline clinics and an online digital platform. Its philosophy is to leverage robust health information technology to address the key pain points faced by patients in the United States, namely long appointment wait times, prolonged in-clinic waiting periods, and high costs.

At One Medical, patients can schedule appointments with physicians anytime and anywhere, even securing same-day visits. When visiting the comfortably designed clinics, patients wait no longer than five minutes yet enjoy ample consultation time with their doctors. Additionally, patients have access to 24/7 virtual care through the One Medical website or mobile app. Access to these services requires an annual membership fee of less than $200 ($149–$199).

By adopting a strategy of extensive site selection and high coverage, One Medical has established clinics in high-traffic areas such as shopping malls, office buildings, and residential communities, positioning them as close as possible to members’ locations to reduce their travel costs. Prior to its acquisition by Amazon, the company had amassed over 760,000 members and operated 188 brick-and-mortar clinics, enjoying a strong reputation among patients.

In addition to One Medical, Amazon was also involved in the acquisition of Signify Health mid-year; although it ultimately lost out to CVS, the multi-billion-dollar sums at stake underscored Amazon’s deep pockets in the healthcare sector.

This acquisition also signaled a shift in Amazon’s healthcare strategy, marking a more aggressive push to integrate offline medical services with online internet-based healthcare. Subsequent moves, such as the shutdown of Amazon Care—which had overlapping business lines with One Medical—and the launch of the Amazon Clinic platform featuring on-site third-party healthcare providers, exemplify this strategic direction.

Almost simultaneously with the completion of its acquisition of One Medical, Amazon began to further integrate its healthcare services with its membership ecosystem. The initial foray was Amazon Pharmacy’s launch of RxPass in early last year, a service widely regarded as a “game-changer.”

Amazon RxPass for Amazon Prime Members

RxPass is a bundled service designed exclusively for Amazon Prime members. For a flat monthly fee of $5, enrolled Amazon Prime members can receive regular, free shipping on over 50 generic medications covering more than 80 common conditions. Statistics indicate that these 50+ generic drugs accounted for as much as 32% of all generic prescriptions in the United States in 2021. The median out-of-pocket cost for these medications when purchased with insurance typically ranges from tens to hundreds of dollars.

For patients with chronic conditions requiring long-term medication, particularly those needing multiple drugs, the appeal of the $5-per-month RxPass is evident. Even chronic disease patients who were not previously Amazon Prime members may find it worthwhile to subscribe to the service.

In fact, one of Amazon’s objectives in launching RxPass is to strengthen its penetration among middle-aged and elderly users—the demographic with the lowest adoption rate—by offering affordable generic drugs. After all, for just $14.99 per month, Amazon Prime members can add RxPass for a total monthly cost of only $19.99; even if they are effectively paying more for the subscription than for the medications themselves, this still represents significant savings compared to monthly prescription costs that can run into tens of dollars.

This represents a significant investment for Amazon. According to statistics, generic drugs accounted for approximately 86% of all prescription drug dispensing volume in the United States in 2022, yet they represented only 20% of total prescription drug spending by value. Consequently, most industry insiders believe that while Amazon’s initiative will indeed reduce patients’ out-of-pocket costs for generic medications, it will undoubtedly lead to greater losses for Amazon.

By year-end, Amazon further expanded its One Medical services to Amazon Prime members. Prime members can access a One Medical membership for $9 per month or $99 per year, which is $100 less than the standard annual fee of $199 for a standalone One Medical membership. They can also add up to five family members and friends to their plan at an even greater discount, priced at just $6 per person per month or $66 per person per year.

After becoming a member, you can access 24/7 on-demand urgent telehealth consultations (typically lasting under five minutes per session) via the One Medical app, thereby addressing the issue of prohibitively high emergency room costs in the United States. You can also schedule in-person visits at One Medical clinics or book unlimited-duration telehealth consultations during business hours through the app; however, these services require payment through insurance or out-of-pocket.

In contrast to its aggressive, cost-no-object acquisitions and expansion efforts over the past two years, Amazon’s first move at the start of 2024 was to cut hundreds of jobs at One Medical and Amazon Pharmacy. It has set a target for One Medical to reduce its fixed operating costs from 41% of total revenue to 20% by 2028, and plans to significantly lower the cost per patient visit from $372 in 2023 to $322 in 2024.

Clearly, Amazon, once flush with cash, is now facing financial constraints, with its intent to control costs being quite evident.

Nevertheless, claims that Amazon might abandon its healthcare ventures are overly exaggerated. After all, the healthcare sector has been relatively insulated compared to Amazon’s other business units. In contrast, since late 2022, Amazon has undergone multiple rounds of large-scale layoffs, affecting a total of 27,000 employees. Notably, the single layoff event in 2023, which involved 18,000 jobs, marked the largest workforce reduction in Silicon Valley in recent years.

In recent years, the cash-rich Amazon has been aggressively expanding its workforce and making waves in the healthcare sector time and again. One of its key targets is CVS, the largest pharmacy chain in the United States, which has gradually transformed into a comprehensive health solutions provider spanning multiple fields. In fact, over the past year or so, CVS has leveraged its financial strength to counter Amazon’s intense competitive pressure.

First is the acquisition of Signify Health. Last March, CVS officially closed its $8 billion acquisition of Signify Health. This deal, which began in September 2022, marked CVS’s comeback victory, successfully outmaneuvering Amazon and UnitedHealth to secure the target.

Of course, CVS paid a hefty price for this move—Signify Health had a market capitalization of just $6.6 billion one month before the deal was announced, yet it commanded a premium of as much as 21% in merely a month. Considering that CVS had just lost the bidding war for One Medical to Amazon only a month earlier, this counterstrike significantly boosted CVS’s morale and seems to have been worth it.

Signify is a U.S.-based primary care provider whose core competency lies in its nationwide healthcare network spanning all 50 states, comprising approximately 10,000 physicians, nurses, and physician assistants. These family practitioners regularly conduct home visits to enrolled patients, delivering medical and health services. According to statistics, Signify Health provided approximately 1.9 million home visits to 40 million members in 2021.

Furthermore, since the onset of the COVID-19 pandemic, Signify Health has also launched internet-based medical services.

Beyond healthcare, Signify Health is deeply rooted in its local communities, having established partnerships with more than 600 medical and social care organizations and 200 community-based organizations. These collaborations connect patients with appropriate follow-up care and community resources, addressing the social determinants of health at their root. Issues such as food insecurity, transportation barriers, social isolation, and poverty fall within its scope of focus. As a result, Signify Health has earned a strong reputation in the communities it serves.

From Signify’s business perspective, this represents a natural “traffic gateway.” It not only helps CVS achieve its goals in home care and managed health management but also enables it to reach more users through differentiated services, establish broader and deeper connections with community resources, and organically integrate these efforts with its nearly 10,000 stores across the United States, thereby forming a robust grassroots service network.

The acquisition of Signify Health was merely the beginning for CVS. Just two months after completing that deal, CVS announced the acquisition of Oak Street Health. This time, the price tag was even higher, reaching a staggering $10.6 billion.

Oak Street Health operates primary care centers across 21 U.S. states, with most located in relatively underserved areas characterized by lower quality of medical services, unmet healthcare needs, and higher rates of unnecessary medical spending. Its target audience primarily focuses on individuals eligible for Medicare.

Overall, although Signify Health and Oak Street Health have slightly different business models, both operate within the home-based healthcare sector. CVS aims to achieve strategic complementarity between its home-based healthcare offerings and its existing businesses. By integrating customer bases across different business lines, CVS seeks to achieve comprehensive service coverage, fuse multiple business segments to effectively reduce costs, and win the favor of payers with more competitive bundled service pricing.

These two acquisitions cost CVS nearly $20 billion, demonstrating its “financial prowess” to be no less formidable than Amazon’s. In fact, large-scale acquisitions have been commonplace throughout CVS’s history. For instance, in 2015, CVS consecutively acquired Omnicare and Target’s pharmacy business, with the former costing $12.7 billion and the latter $19 billion. Similarly, in 2017, CVS acquired Aetna, then the third-largest insurer in the United States, for $69 billion.

Compared to these epic acquisitions, the purchases of Oak Street Health and Signify Health seem like mere “pocket change” for CVS.

CVS indeed has such confidence. In its fiscal 2023 third-quarter earnings report, CVS reported quarterly revenue of $89.8 billion, a year-over-year increase of 10.6%. However, a cause for concern is that while CVS’s revenue grew, its profits did not. Financial data show that operating profit in Q1 and Q2 of fiscal 2023 declined by 5.1% and 10.4%, respectively, year over year. Although operating profit in Q3 rose slightly by 2.5% year over year, it showed no signs of sequential growth.

CVS quickly lowered its 2024 earnings forecast, marking the third consecutive time it has reduced its annual performance targets. The company also announced a restructuring plan worth nearly $500 million, which includes laying off 5,000 employees and implementing a series of cost-cutting measures, such as exploring the use of artificial intelligence to improve operational efficiency, reducing reliance on consultants and vendors, and cutting travel expenses, with the goal of saving $800 million in 2024.

At the beginning of 2024, CVS further announced that it would close some CVS pharmacies located within Target stores in early 2024, with a plan to shut down 900 stores over three years. Currently, it operates more than 9,000 pharmacies in total, nearly 1,800 of which are situated inside Target stores. This amounts to almost one-tenth of its existing pharmacy count.

CVS, known for its blockbuster acquisitions, is equally aggressive in cost control!

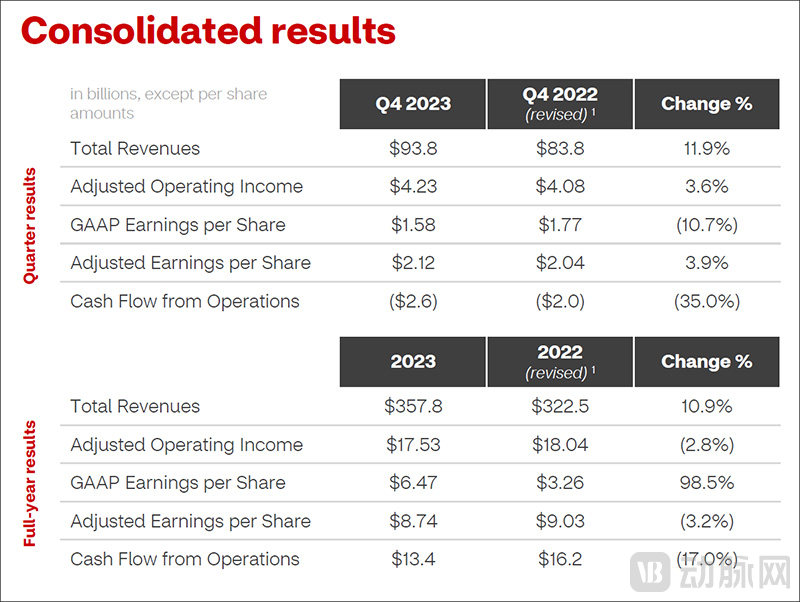

CVS’s 2023 Annual Report Showed Strong Performance

In the newly released 2023 fiscal year annual report, CVS reported full-year revenue of $357.8 billion, a year-on-year increase of approximately 11%. Among this, the newly formed Healthspire healthcare segment (including Aetna, MinuteClinic, pharmacy benefit manager Caremark, provider network Signify Health, and primary care clinic operator Oak Street Health) saw its revenue grow by 10.2%, reaching $186.8 billion for the year, accounting for as much as 52% of total revenue.

On the other hand, CVS also anticipates a further increase in its medical costs, proactively lowering its performance forecast once again by reducing the 2024 expected adjusted operating revenue for the Healthspire division to $7.4 billion, a decrease of as much as $90 million.

Undoubtedly, this also means that the main theme for CVS in 2024 will be cost reduction and efficiency improvement. Perhaps significant cost-control measures will make a comeback.

Walgreens was once the largest pharmacy chain in the United States, but it was surpassed by CVS in 2005. As internet giants such as Amazon have increasingly focused on expanding into the healthcare sector in recent years, Walgreens has had to remain highly vigilant and respond strategically. In its efforts to transform its business model, the company has completed several major acquisitions in recent years, including a $5.2 billion investment to become the majority shareholder of primary care provider VillageMD, a $2.3 billion acquisition of specialty pharmacy company Shields Health Solutions, and a $722 million acquisition of CareCentrix, which specializes in home-based clinical care management services.

Last January, Walgreens again backed its subsidiary VillageMD in completing the $8.9 billion acquisition of Summit Health-CityMD. However, the impact of these acquisitions has not been as favorable as anticipated, or perhaps has yet to materialize. In any case, Walgreens’ performance has consistently fallen short of expectations since then, compelling the company to embark early on a path of cost reduction and efficiency improvement.

In May, the pharmacy chain announced a 10% workforce reduction, affecting 504 employees, which it claimed would save more than $100 million in costs. Subsequently, it released its semi-annual report for fiscal year 2023, revealing a net loss of $3 billion for the first half of the year. This marked the first time since 2020 that its profitability had fallen short of analysts’ expectations. Compared with the $4.5 billion profit recorded in the first half of fiscal 2022, this represents a precipitous decline.

Walgreens executives stated that a significant factor contributing to the loss was the $5.4 billion the company paid in opioid litigation settlements. For years, major retailers have been accused of playing a substantial role in the opioid epidemic in the United States. In 2022, CVS and Walgreens reached agreements with plaintiffs, each paying approximately $5 billion to local governments to settle the lawsuits.

In response to its lackluster performance, Walgreens announced the closure of 300 stores in the UK and 150 in the US, thereby raising its cost-cutting target from the previously announced $3.5 billion to $4.1 billion.

Walgreens’ 2023 Performance Fell Short of Expectations

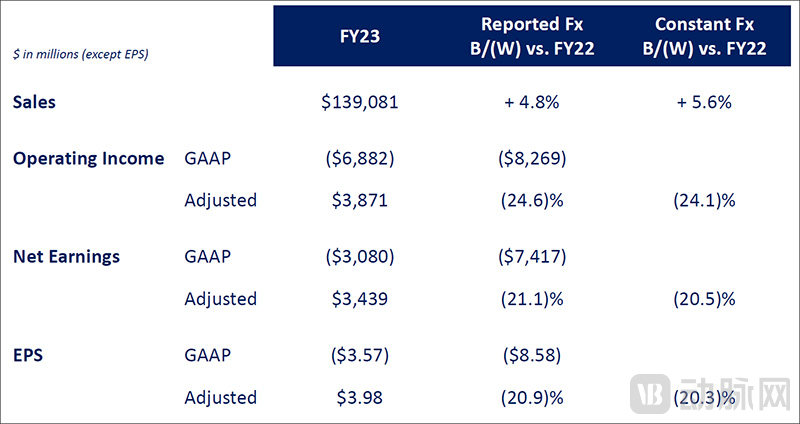

Nevertheless, Walgreens’ annual report released last October (with its fiscal year ending in August each year) showed weak performance, with full-year revenue reaching $139 billion. Earnings once again fell short of expectations, marking the first time in nearly a decade that the company missed earnings estimates for two consecutive quarters. Particularly disappointing was its heavily invested healthcare services division, which generated only $6.6 billion in annual revenue, accounting for just 4.7% of the company’s total revenue.

Subsequently, Walgreens announced plans to close approximately 60 VillageMD clinics in the next fiscal year to focus on clinics in more profitable regions. This move also triggered significant changes in its executive leadership, with a number of senior executives, including the CEO, being replaced.

Since the beginning of 2024, Walgreens’ streak of bad luck has continued. As a representative of the U.S. pharmaceutical retail sector, Walgreens has been included in the Dow Jones Industrial Average (DJIA) since 2018, when it replaced General Electric. This iconic index, established in 1896, comprises 30 corporate giants selected by the Dow Jones Industrial Average Committee from the S&P 500 Index to best represent the U.S. economy.

Due to consecutive declines in recent performance, Walgreens’ stock price has fallen by 68% over the past five years, ranking last among the components of the Dow Jones Industrial Average (DJIA). In late February, Walgreens was removed from the DJIA. While it is not unusual for companies to be added or removed from the index depending on market conditions, its replacement was none other than Amazon, one of its key competitors. This outcome is likely the last scenario Walgreens’ executives would have wished to see.

Compared with the relatively resilient performance of CVS and Amazon, Walgreens has underperformed for several consecutive quarters, facing significantly greater pressure to cut costs and improve efficiency. If it fails to halt its downward trend promptly, a gradual reversal of fortune in the competitive landscape is not impossible. Therefore, Walgreens may well undertake more substantial cost-cutting and efficiency-enhancing measures in 2024.

It is not difficult to observe that the current environment is far from ideal. Even in the U.S. stock market, which appears to be performing well on the surface, healthcare giants—once flush with cash—are now more focused than ever on cost reduction and efficiency improvement. Their operational focus is gradually shifting from aggressive spending to drive revenue growth to meticulous cost control, akin to “splitting a penny in half.” The large-scale acquisitions that once frequently occurred, drawing awe at their display of “financial might,” are increasingly being replaced by layoffs and store closures.

These moves by the industry giants undoubtedly hold significant reference value for the direction of the sector.

Currently, the global primary market is also undergoing adjustments. Investment strategies have gradually shifted from prioritizing growth potential to focusing on commercialization capabilities and profitability. An increasing number of investors believe that profitability is now paramount; companies with high growth but severe unprofitability are becoming less attractive for investment. This trend warrants deep reflection by enterprises, prompting them to adjust their strategies, make every effort to reduce costs and improve efficiency, and, when necessary, take decisive measures such as divesting non-core assets to ensure survival.

After all, history is always written by the victors, and only by surviving can one have the chance to have the last laugh.

References:

Nathaniel Meyersohn,CNN:Amazon launches $5-a-month unlimited prescription plan

Samantha Delouya,CNN:Amazon officially joins the Dow Jones Industrial Average, booting out Walgreens

Maia Anderson,healthcare-brew.com:CVS healthcare division saw strong growth in 2023

Maia Anderson,healthcare-brew.com:CVS slashing 5,000 jobs to cut costs after string of multibillion-dollar acquisitions

Marissa Plescia,medcitynews.com:Believing Amazon’s Job Cuts Signal an Exit From Healthcare Would Be ‘Overly Simplistic,’ Expert Says

Marissa Plescia,medcitynews.com:Amazon Links Prime Membership With One Medical: Will This Improve Access?

Marissa Plescia,medcitynews.com:Is Amazon’s RxPass Breaking New Ground in Creating Access to Affordable Drugs?