12 Leading Investment Firms Reveal the Hottest Medical Sector of the Year in IPO Prospectus

VCBeat

Internet Medical Health Media

Delian Capital

Investment institutions focusing on technology-driven projects in high-end manufacturing, cutting-edge technology, and healthcare.

Green Pine Capital

Venture Capital Management Institution

Cenova Capital

Investment institutions focused on healthcare and life sciences

SCGC

Investment Institutions in Innovative Fields

Dalton Venture

Venture Capital Institutions in the Medical and Health Field

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

MPCi

Venture Capital Institutions in High-Tech Startup Fields

WinX Capital

Investment Institutions in the Greater Health Field

At this very moment, China’s healthcare innovation industry is yearning for certainty more than ever before.

On one hand, the financing environment took a sharp downturn in 2023, posing significant challenges for many companies. Frequent occurrences of pipeline cuts, asset sales, and large-scale layoffs have cast a shadow over the entire industry.

On the other hand, the medical innovation industry appears to be standing at the threshold of a new era, with surging waves of global expansion, business development (BD) collaborations, and mergers and acquisitions coming to the fore. However, significant divergences remain within the industry regarding how to interpret these trends and what actions market participants should take.

At such moments,Understanding of the current industry landscape and judgment of trends often determine whether each practitioner adopts a contraction or expansion strategy, as well as how to adjust the pace of business and market operations.

To this end, VCBeat spent one month conducting surveys and interviews with frontline healthcare investors—the group most sensitive to the ebb and flow of market trends—to explore potential new industry directions for the next phase from their perspective, thereby providing a reference for market entrants to re-anchor their value coordinates.

First, we extend our gratitude to the twelve star investment firms that participated in this interview:CDH VGC, Delian Capital, Dalton Venture, China Renaissance, Legend Capital, Matrix Partners China, WinX Capital, Mingfeng Capital, Cenova Capital, SCGC, Green Pine Capital, and Paradise Silicon Valley (listed in alphabetical order by Pinyin initials), as well as 15 healthcare investors who participated in the questionnaire survey.

During interviews and research, VCBeat has observed that while certain consensuses are taking shape within the industry, there remain conflicts and divergences in perceptions and judgments regarding specific niche sectors. In the following sections, this article will present and elaborate on these changes from both macroscopic and microscopic perspectives.

In this article, you will learn:

(I) Macro Perspective: Cooling Venture Capital and Product Explosion, Global Expansion Begins

· Riding the High and Fast Waves of Global Expansion: Three Core Challenges and Two Key Points

· The M&A Wave Crashes Ashore: A Major Industry Reshuffle and a New Opportunity

· Current Core Task: Cash is King, Tighten Your Belt to Survive

(II) Micro Perspective: Innovation Stems from Real Clinical Needs, and Only the Resilient Can Go Far

① Biopharmaceutical Sector: GLP-1 drugs, ADC platforms, and CGT therapies are highly sought after, presenting significant opportunities;

② Innovative Medical Devices Sector: Ophthalmology and Cardiovascular Fields Ignite Investment Enthusiasm, with Commercialization Capability Becoming a Key Metric;

③ Digital Healthcare Sector: AI is sparking a new revolution in medical scenarios, with digital therapeutics products receiving intensive regulatory approvals;

④ Medical Services Sector: Consumer healthcare specialties are shifting towards a “small but beautiful” model, while critical and emergency care specialties focus on deepening expertise and comprehensive service delivery.

In 2023, the venture capital and private equity boom, which had been surging for years, continued to cool down.

According to data from the VCBeat database, total financing in China’s healthcare primary market amounted to $10.9 billion last year, a 31% year-on-year decline, with transaction volumes returning to levels seen between 2017 and 2018.

It can be said that,In the current market, the “fast-company” logic of recent years—where projects sought financing, established valuations, and rapidly went public—has fundamentally shifted. Identifying new sources of incremental growth has become a critical imperative for the industry.

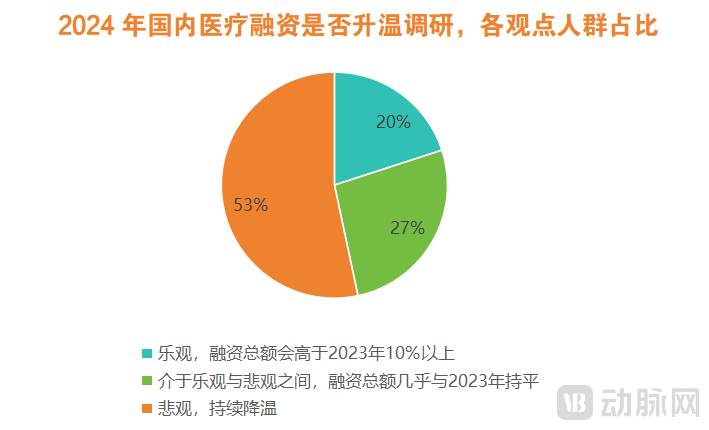

Faced with the chilling sentiment in the capital market, a majority of healthcare investors surveyed—53% to be precise—generally believe that healthcare venture capital and private equity investment will continue to cool down in 2024. Behind this trend lies the fact that the current healthcare industry is paying the price for its overly aggressive expansion in recent years.

“While there are macroeconomic factors contributing to the difficulty of investment exits, more importantly, the primary and secondary markets had previously been overly optimistic in estimating the intrinsic value of assets, leading to a certain degree of bubble. We should recognize that now is the time to bridge the gap between price and value, and it is also an opportunity driven by external pressures to enhance asset quality and promote industrial upgrading. We also believe that as long as Chinese innovative enterprises continue to improve the quality and efficiency of their R&D assets, becoming more competitive and capable of going global, recognition from capital markets and global buyers is only a matter of time. As the saying goes, ‘No construction without destruction; no survival without risk.’” Wang Junfeng, Co-Chief Investment Officer at Legend Capital, told VCBeat.

Additionally,An indisputable fact is that the boom in medical venture capital investment in recent years has provided substantial support for R&D at healthcare innovation companies, laying the foundation for the current approval and market launch of innovative products, as well as their subsequent surge.

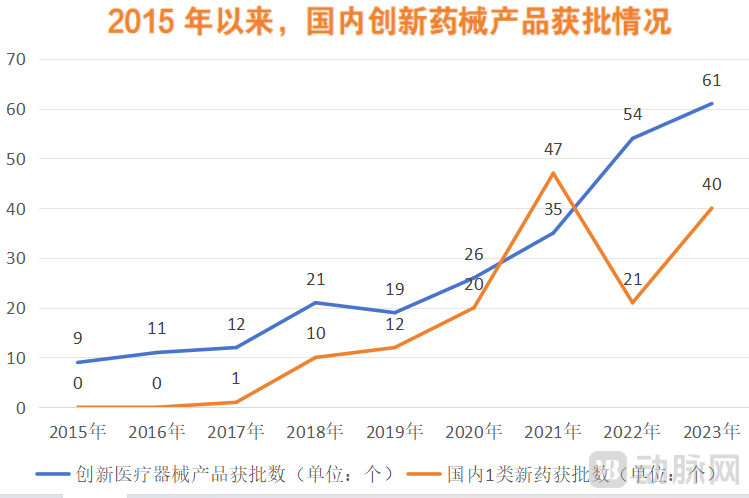

The true value is reflected in the data. In the medical device sector, the approval of innovative medical devices is accelerating. Between 2022 and 2023, a total of 115 innovative medical devices were approved in China, surpassing the combined total from the eight-year period between 2014 and 2021. A number of innovative medical devices that fill domestic gaps, reach world-leading levels, and address urgent clinical needs have been approved for market launch, providing more treatment options for patients in China and making the "window effect" increasingly prominent.

In the field of innovative drugs, a total of 34 domestically produced Class 1 new drugs were approved in 2023, representing a 156% increase from 2022 and setting a new historical record.

(Data source: VCBeat Orange Database)

(Data source: VCBeat Orange Database)

Furthermore, a notable detail is that approved domestic Class 1 new drugs are no longer primarily concentrated among a few established companies; instead, many new players have emerged. Among them, innovative enterprises such as Biocytogen Pharmaceuticals (Bo Rui Sheng Wu), Jingxin Pharmaceutical, Qilu Pharmaceutical, IASO Biotherapeutics, Xuanzhu Biopharma, and Simcere Pharmaceutical have seen their first Class 1 new drugs approved for marketing, marking these companies’ entry into the commercialization phase of innovative drugs.

In response, more than one investor stated that since the surge in scientist-led startups began in 2021, it has fueled a boom in the translation of medical research into clinical applications, with an increasing number of innovative achievements emerging and being implemented. AndThese innovative drugs and medical devices were positioned for globalization from the outset. Coupled with the gradual implementation of China’s volume-based procurement policy, this has accelerated a new wave of overseas expansion by innovative enterprises.

Taking innovative drugs as an example, according to incomplete statistics from Donghai Securities, there were at least 120 overseas licensing transactions involving Chinese innovative drugs between 2021 and 2023, with a total transaction value approaching $85 billion. In January alone this year, more than 15 license-out deals had been completed, with disclosed upfront payments totaling approximately $370 million and the overall transaction value exceeding $10 billion.

The global expansion of medical device companies is also accelerating. For instance, the overseas revenue of China’s A-share listed medical device companies surged from RMB 25.7 billion in 2018 to RMB 108.1 billion in 2022, representing a compound annual growth rate (CAGR) of 43.2%, while the proportion of overseas revenue increased from 22% to 34.1%.

Amid the surge in global expansion, frequent large-scale M&A transactions are injecting fresh vitality and vigor into the entire industry.Since the beginning of 2024, AstraZeneca’s $1.2 billion acquisition of Gracell Biotechnologies and Haier Group’s proposed RMB 12.5 billion takeover of Shanghai RAAS Blood Products, China’s leading blood products company, have sparked a wave of mergers and acquisitions, bringing warmth to the cooling venture capital and private equity environment.

Undoubtedly, amidst the ebb and flow, a new narrative logic for the healthcare industry gradually unfolded in 2024.

· Riding the High Waves of Global Expansion: Three Core Challenges and Two Key Points

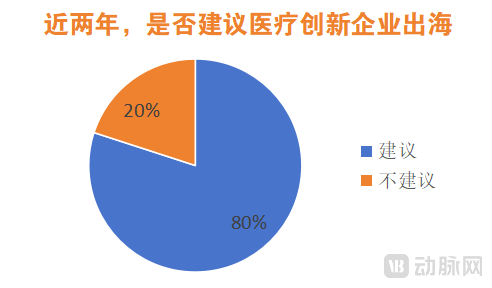

Going global is becoming a choice for many medical innovation companies, but not all investors are optimistic about this trend.

For instance, regarding global expansion, Sun Linghao, Managing Director at Matrix Partners China, believes that Chinese medical innovations are now ready for large-scale international deployment. On one hand, after years of accumulation, certain innovative products from Chinese healthcare companies have become globally competitive. On the other hand, a cohort of professionals with overseas business experience has joined these enterprises, playing an increasingly important role.

From the perspective of conservative investors, global expansion can help companies tap into international markets, which is a positive aspect. However, they also caution against potential future risks, particularly the significant uncertainty arising from current geopolitical influences, as well as the considerable challenges inherent in going global, which place substantial demands on a company’s products and teams.

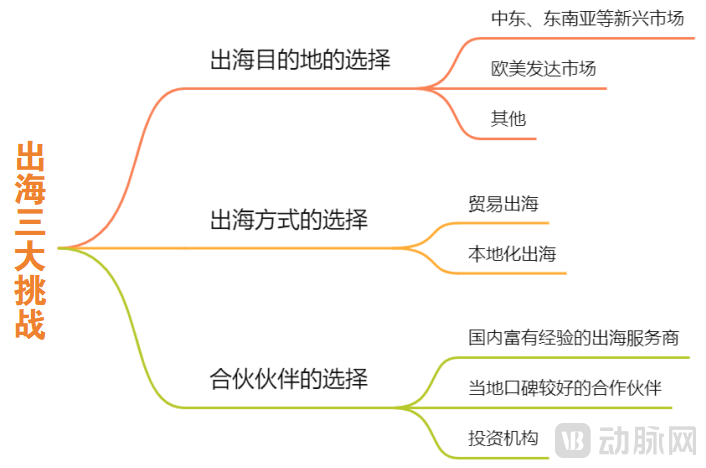

To this end, VCBeat has synthesized the views of frontline investors and broadly summarizedThere are three major challenges in going global, all of which center on selection.

First, the selection of overseas destinations.Whether in developed markets such as Europe and the United States, or in emerging markets like the Middle East and Southeast Asia, differences in policy, culture, and economic development levels result in varying degrees of difficulty for companies expanding overseas. For instance, as a hub for countries along the “Belt and Road Initiative,” Southeast Asia boasts advantages such as geographical proximity, convenient transportation, and cultural similarities; however, its pharmaceutical industry chain remains incomplete.

Second, the choice of overseas expansion strategy, specifically whether to pursue international expansion through trade or through localization. The answer to this question often determines the subsequent costs for medical companies going global. Expanding via trade is relatively asset-light, helping companies enter markets, enhance brand reputation, and build trust with customers. However, in regions with strong local protectionism, localized expansion may be a better strategy.

Third, the selection of partners. In the process of expanding overseas, identifying suitable partners is an unavoidable hurdle, as this involves customer resources and marketing networks. Several investors have stated that medical enterprises embarking on their initial overseas expansion should either collaborate with experienced domestic cross-border service providers or, ideally, find partners with a strong reputation and credibility who are well-established in the target overseas markets.

It is precisely because of the three major challenges ahead,An increasing number of investment firms are actively strategizing and positioning themselves to empower and assist their portfolio companies in expanding into overseas markets.

(Three Major Challenges in Going Global, Chart by VCBeat)

(Three Major Challenges in Going Global, Chart by VCBeat)

Wang Junfeng, Co-Chief Investment Officer of Legend Capital, told VCBeat: “Leveraging Legend Capital’s industrial resource network, we help our portfolio companies connect with business development teams at European and American pharmaceutical firms and facilitate the international expansion of their assets into these markets. Furthermore, Legend Capital’s healthcare investment arm has taken a pioneering approach to the Southeast Asian market, guiding Chinese assets and technologies into countries such as Indonesia and Singapore, thereby providing cost-effective pharmaceuticals and medical device products to hundreds of millions of people in the region.”

“Over the past six months, our team has traveled to Europe and the United States to visit numerous large corporations and startups, helping our portfolio companies seek overseas M&A and business opportunities,” said Sun Linghao, Managing Director at Matrix Partners China. He added that Matrix Partners China will continue to adhere to this strategy in 2024.

In addition to helping Chinese companies expand overseas, attracting foreign enterprises into China has also become a major trend.For example, Fei Simin, a partner at Mingfeng Capital, told VCBeat that in 2024 the firm would focus on opportunities among overseas consumer healthcare companies, paying attention to international brands, new technologies and materials, and the latest R&D achievements, with the aim of “bringing in” these technologies and enterprises.

However, during this process, many investors also cautioned,There are two key points to note regarding the current global expansion of medical innovations.

First, the global expansion of medical enterprises is shifting towards high-quality output rather than low-cost appeal, while increasingly relying on global supply chains for the integration of worldwide resources. Second, the internationalization of medical innovation companies is a strategic battle for market positioning that tests comprehensive strength; strategy formulation should avoid both short-termism and excessive long-termism, instead focusing on mid-term development.

In short, whether medical innovation enterprises can successfully navigate the path of global expansion is not only a validation of their innovative capabilities but also an inevitable route to embracing international markets and creating greater value. This will also drive medical innovation companies to press forward with determination in this year’s wave of overseas expansion.

· The M&A Wave Crashes Ashore: A Major Industry Reshuffle and a New Opportunity

A Wave of M&A Is Surging.

In recent times, news of large-scale mergers and acquisitions in the healthcare industry has been frequently reported.On February 22, Gracell Biotechnologies announced the formal completion of its merger agreement with AstraZeneca, with a transaction value of approximately $1.2 billion (over RMB 8.5 billion), representing an 86% premium. This marks the first instance in history of a Chinese innovative biopharmaceutical company being fully acquired by a multinational corporation (MNC).

Upon completion of the merger, Gracell Biotechnologies will cease to be a publicly listed company and will become a wholly-owned subsidiary of its parent company. Its American Depositary Shares (ADSs) will no longer be listed or traded on any stock exchange. In the announcement, Gracell Biotechnologies also stated that it had filed the relevant applications to suspend trading of its ADSs on the Nasdaq Stock Market effective February 22, 2024 (New York time).

Meanwhile, Novartis announced the acquisition of Chinook Therapeutics to further strengthen its footprint in nephrology; China Resources Double-Crane Pharmaceutical announced the acquisition of 100% equity interest in China Resources Zizhu, held by Beijing Pharmaceutical Group, for RMB 3.115 billion; Sinopharm Group plans to privatize China Traditional Chinese Medicine Holdings Co. Limited for HKD 15.45 billion; and Mindray Medical intends to spend RMB 6.65 billion to acquire controlling interest in Hytek Medical, a company listed on the STAR Market...

“As the investment and financing market cools down and valuations for innovative projects become more rational, we expect M&A activities by listed companies to further accelerate. This opens another door for exits,” Sun Qi, Founding Managing Partner of Dalton Venture, told VCBeat.

Gao Jieliang, Senior Partner at CDH Innovation & Growth Fund (VGC), also believes that M&A exits are a way to generate high returns besides IPOs. “For instance, license-out deals in the innovative drug sector can be understood as a form of de facto M&A exit. Additionally, in the medical device sector, R&D cycles are short and capital requirements are relatively low, but the market size for individual products is small. This prevents many companies from growing into large independent entities, making M&A a promising exit channel in the future.”

As an effective means of optimizing resource allocation and promoting industrial consolidation, the rise of the M&A wave has undoubtedly brought new opportunities to companies facing financing difficulties.

“Mergers and acquisitions (M&A) for high-quality, innovative biotechnology products are more like a ‘natural outcome,’ a logical and foreseeable result,” said Zhang Chunyan, Managing Director at Cenova Capital. “In 2023, Seven and Eight Biopharmaceuticals, the first company we incubated and established, was acquired in its entirety by Eikon Therapeutics. Its core asset is a globally innovative TLR7/8 agonist currently in clinical trials. Another M&A deal involved Apton Biosystems, an early-stage portfolio company, which reached an agreement to be acquired by Pacific Biosciences, a global leader in third-generation sequencing life science technology, based on its developing high-throughput short-read sequencing technology.”

However, the investors interviewed generally believe that,Mergers and acquisitions, while creating new opportunities, are not a “lifeline” for most companies; instead, they are more likely to accelerate the industry’s major reshuffle.

The reason is that mergers and acquisitions often impose stricter standards and conditions on target assets. In particular, industrial capital places significant emphasis on the innovation and commercial maturity of the target company’s business, as well as its synergy with the acquirer’s existing operations.

During this process,Broadly speaking, two types of healthcare companies are poised to gain favor with large enterprises and institutions, ushering in new development opportunities: first, innovative companies with differentiated product pipelines and strong R&D capabilities; second, profitable companies with mature product portfolios and smooth commercialization progress.

“Some so-called ‘innovative enterprises’ built on the capital bubble in previous years have slim chances in this wave of M&A. They focus on imitation and love high-profile publicity, but in reality, there is little innovation. With a single target or technology, dozens or even scores of players are laying out their strategies, resulting in severe homogenization and very low value.” One investor even pointed out, “Mergers and acquisitions by large enterprises are intended to optimize and strengthen their operations, not to “rescue others from crisis.””

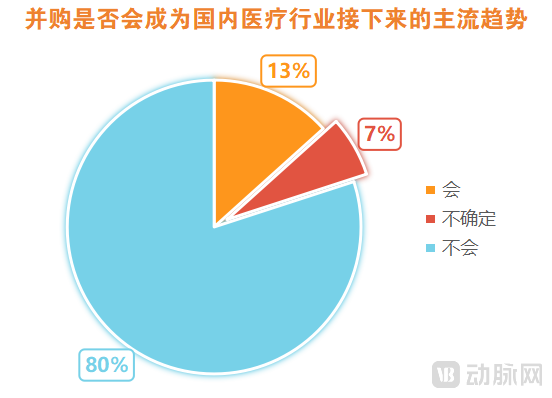

Interestingly, among the 15 healthcare investors who participated in VCBeat’s survey, the vast majority (12) held a negative view on whether mergers and acquisitions would become the mainstream trend in the healthcare industry in the near future. They generally believed that domestic healthcare innovation enterprises lack significant differentiation, making it difficult for them to form complementary relationships with large corporations.

However, in 2024, the M&A boom will persist for a while, propelling a cohort of companies with high innovative and commercial value to the forefront. Meanwhile, many other enterprises will become like waves dashed upon the shore, serving as hidden footnotes in the surging era of venture capital.

· Current Core Task: Tighten our belts to survive; cash is king.

Opportunities never lie externally; one must look within.

The harsh climate of the capital markets in 2023 dealt a severe blow to companies with weak cash-generation capabilities. Many projects resorted to discounted financing to raise funds, and even a number of high-profile unicorns collapsed, including Pear Therapeutics, the first publicly traded digital therapeutics company; Surgalign, a top-100 global orthopedic medical device manufacturer; and Smile Direct Club, a global dental care giant. This trend is poised to continue into 2024.

Against the backdrop of tightening investor funding, “tightening one’s belt” has become a common strategy across the industry.

“How to navigate market cycles and thrive amid pressures from both the primary and secondary markets has become a frequent topic of discussion among industry insiders. And”Survival hinges on cash flow!“Zhou Jufeng, a partner at Paradise Silicon Valley Medical Investment, told VCBeat, ‘Cash flow can be categorized into operating cash flow, investing cash flow, and financing cash flow. Different measures can be taken for each type of cash flow.’”

Taking investment cash flows as an example, during difficult periods, it is advisable to reduce investments in assets with long liquidation cycles, such as land and factories (fixed assets), and to adopt leasing arrangements whenever possible.

Luo Fei, Founding Partner of Green Pine Capital, also stated that companies face three main types of cash flow challenges. “The first type involves companies lacking revenue, relying primarily on financing to address cash flow needs. The second type includes companies that have obtained regulatory approval and launched their products in the market, but the resulting cash inflows fall short of expectations. The third type pertains to companies needing to make trade-offs in R&D for development purposes. Whereas they might have initially aimed to pursue multiple product pipelines, they now need to decide which product lines to retain and which to discontinue.”

In the face of the first scenario,Enterprises need to break the inertia of relying solely on financing to resolve cash flow issues.Solutions include reviewing existing funds on the books, streamlining expenses, and shifting from quarterly or semi-annual cash flow reviews to monthly monitoring of cash reserves.

For the second scenario, the focus is onStrengthen Budget Management. During periods of favorable economic conditions, the budgets of medical innovation enterprises are not rigid, with weak binding constraints. Effective budget management should encompass multiple aspects, including revenue and expenditure, personnel management, and more.

The third scenario requires enterprisesMaking Trade-offs in R&D, which requires case-by-case analysis based on the specific circumstances of each enterprise.

“When the entire industry is on an upward trajectory, with abundant capital and a vibrant financing environment, financial management plays a subordinate role,” emphasized Luo Fei, Founding Partner of Green Pine Capital, whileIn the current environment, financial management has become particularly critical. This cannot be addressed by the finance department alone but requires the direct involvement of the company’s top leader.

Lin Guanyu, Investment Director of the Health Industry Fund Investment Department at SCGC (Shenzhen Capital Group), also highlighted milestone metrics. He recommended that R&D-focused enterprises prioritize the timing of obtaining Proof of Concept (PoC) data to plan their financing and business development (BD) rhythms accordingly. “For drugs targeting non-oncology indications, after obtaining preliminary human safety data, companies may consider conducting small-sample Phase 1b trials or Investigator-Initiated Trials (IITs), in compliance with regulatory and ethical requirements, to rapidly acquire initial PoC data and explore potential clinical strategies, thereby gaining additional time windows. For enterprises developing new Traditional Chinese Medicine (TCM) drugs, drug combinations with a long history of clinical application can accumulate human use experience through hospital preparations, in accordance with regulatory provisions, which can help alleviate the pressure of clinical trials on corporate cash flow.”

In addition, Zhang Chunyan, Managing Director of Cenova Capital, stated that in the face of the challenge to “survive,”Companies Should Focus Most on “Value Regression”This carries a dual implication: on one hand, it means that enterprises should prioritize cost reduction and efficiency enhancement in their management and operations, shifting from the previous extensive, involutionary growth model to high-quality development that is guided by clinical needs and driven by innovative technologies; on the other hand, it indicates that a rational regression in valuation levels is essential to sustain corporate development. The past “price-to-dream ratios” reflected blind enthusiasm detached from risk and fundamentals, and timely value correction has become a “mandatory course” for enterprises.

“Companies should develop a clear plan for the progress of their core business over the coming year, based on their own circumstances, and focus human, material, and financial resources on achieving their core KPIs, so that the company can truly continue to create value,” Sun Linghao, Managing Director at Matrix Partners China, told VCBeat.

It is worth noting that amid the current cash flow crunch, a sense of pessimism has gradually taken hold in the medical innovation industry. In response, several investors with more than a decade of experience have stated that cyclical fluctuations are an inherent law of industry development, and that behind these challenges lie opportunities for truly innovative companies to step into the spotlight.

“The ebb and flow of industry cycles act as a natural selection process, where only the fittest survive. This is not only an advantage of the market but also an opportunity for ‘gold’ to shine!” stated Zhou Jufeng, Partner at Paradise Silicon Valley Medical Investment.

Compared to macro trends, industry insiders are more concerned with where the niche investment opportunities lie in 2024.

This question is not easy to answer, as short-term investment opportunities are influenced by various factors, including the macroeconomic environment, market sentiment, and policy signals. No one can guarantee which niche sector will buck the trend and soar during a specific period.

What is certain, however, is that both the policy-driven push for source innovation in recent years and the intensifying involution within the industry indicate that,Genuine Innovation Driven by Patients’ Real Needs Has Become the Key Competitive Advantage for Healthcare Startups, innovations that enhance medical efficiency and meet genuine clinical needs represent the core investment areas.

Of course,The Essence of True Innovation Is Not Technological Determinism, but a Company’s “Comprehensive Resilience”, namely, a comprehensive assessment of technological strength, product portfolio, business model, and level of internationalization. Only enterprises that possess both genuine innovation and strong resilience can achieve steady and long-term success.

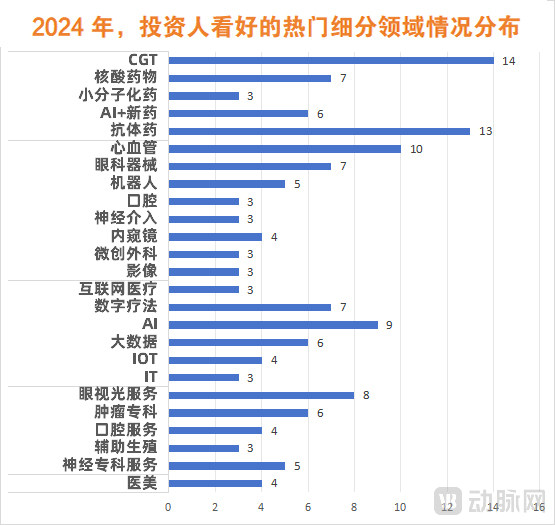

Based on the aforementioned logic, VCBeat, incorporating insights from investors, will separately discuss the key sub-sectors and the underlying rationale that investment institutions are currently focusing on and will continue to prioritize in the near future, across four major segments: biopharmaceuticals, innovative medical devices, digital health, and healthcare services.

(Data source: Survey questionnaire. Track logic is not strictly categorized and is primarily derived from track keywords provided by respondents.)

Biopharmaceutical Sector: GLP-1 Drugs, ADC Platforms, and CGT Therapies Gain Traction, Offering Significant Opportunities

The Biopharmaceutical Sector Never Seems to Lack Hot Topics.

In 2023, GLP-1 drugs ignited a nationwide fervor for weight loss in China. Meanwhile, CGT therapies and ADC platforms continued to attract significant interest. The vast majority of investors believe that this trend will continue in 2024.

How Hot Are GLP-1 Drugs? The Prestigious Academic Journal Science Named GLP-1 the Scientific Breakthrough of 2023 Last December, Fueling the Market Capitalization Surges of Eli Lilly and Novo Nordisk. In China, major biopharmaceutical companies have quickly followed suit. Huadong Medicine and HeRenHui Biotechnology have successively received approval to launch GLP-1-based weight-loss products, while multiple pharmaceutical firms, including Hengrui Medicine, Tonghua Dongbao, CSPC Pharmaceutical Group, and Livzon Group, have entered the fray.

“Across both primary and secondary markets, the GLP-1 concept has virtually become the sole consensus and the leading driver of market trends in the pharmaceutical industry,” said Zou Guowen, founder of WinX Capital. Last year, institutional investors sequentially closed deals on three projects related to the GLP-1 concept, including HuiSheng Biopharma, Innovent Bio (Yinuo Pharmaceutical), and ZhiTai Biologics.

Moreover, GLP-1 has also driven business development (BD) deals among leading pharmaceutical companies. For instance, last November, Chengyi Biotech and AstraZeneca entered into an exclusive collaboration on a small-molecule GLP-1 receptor agonist; last December, Roche acquired the biotechnology company Carmot Therapeutics with a $2.7 billion upfront payment. Carmot Therapeutics possesses a dual-target GLP-1/GIP drug in clinical development and an oral GLP-1 receptor agonist.

Although there are numerous market entrants, the competitive landscape of GLP-1 is far from settled. For instance, in terms of R&D trends, innovative companies still have opportunities in areas such as long-acting formulations, oral administration, and multi-target therapies.

A series of investment opportunities will also emerge around the core of GLP-1.: The ecosystem includes CDMO-related service providers, upstream industries such as amino acids and fatty acid side chains, as well as GLP-1 formulation injection pens. Meanwhile, the structural lifestyle changes driven by GLP-1 therapies will also trigger increased demand for products like CGMs, and even give rise to medical aesthetic solutions addressing varying degrees of tissue volume loss resulting from weight reduction.

Looking again at ADCs, they were undoubtedly the brightest highlight last year: multiple transactions centered on ADCs took place in 2023, with numerous multinational corporations (MNCs) entering into collaborations with Chinese pharmaceutical companies.As Baili Tianheng granted BMS the development and commercialization rights to its EGFR×HER3 bispecific antibody-drug conjugate (ADC) BL-B01D1, the total transaction value reached up to $8.4 billion, including an upfront payment of $800 million.

“The numerous landmark overseas licensing deals for Chinese-made ADCs in 2023 have established ADCs as a new hallmark of Chinese innovative drugs going global. ADCs are a typical representative of New Modality therapies,” said Jiang Jiajia, Managing Director of the Healthcare and Life Sciences Division at China Renaissance, in an interview with VCBeat. “Over the past few years, increased capital support for Chinese innovative enterprises has concentrated more resources into New Modalities. Chinese innovative drugs like ADCs have accumulated substantial expertise, and their teams demonstrate strong execution capabilities, enabling them to seize global opportunities firmly when they arise.”

(Image source: China Renaissance)

(Image source: China Renaissance)

Furthermore, China Renaissance believes that one of the reasons for the frequent acquisitions by multinational corporations (MNCs) in China is their recognition of solutions to extend the lifecycle of PD-(L)1 inhibitors. On December 15 last year, the world’s first “PD-1 + ADC” combination therapy was approved, successfully challenging the landscape of first-line cancer treatment and boosting both the ADC and PD-(L)1 sectors. This is because PD-(L)1 inhibitors are facing a patent cliff, with the core patents for Opdivo and Keytruda expiring in 2027 and 2028, respectively. The impact of “PD-(L)1 + ADC” combination regimens on the standard of care for first-line treatment will further extend the lifecycle of PD-(L)1 drugs.

“Following the surge in popularity of ADC platforms, CGT therapies are highly anticipated in China’s new drug landscape over the next two to three years.“Jiang Yangzhi, a partner at Delian Capital, predicts that ‘the biological mechanisms of CGT therapies are very clear, and they all involve molecular formats that have previously been developed into drugs. In 2023, the FDA approved five gene therapies and two cell therapies, validating the prediction made by former FDA Commissioner Scott Gottlieb in early 2019. Current FDA Commissioner Robert Califf also stated at a national hearing in May 2023 that the Center for Biologics Evaluation and Research (CBER) plans to add 150–200 staff members to focus on the review of CGT therapies. In essence, CGT therapies represent a typical form of engineering-driven innovation; the curtain has only just risen, and they hold great promise across more targets and indications. China also possesses comparative advantages in these molecular formats. HeYuan Bio, E-MuFeng, and ZhiShan WeiXin, in which Delian Capital invested two to three years ago, have recently demonstrated strong performance.’”

Throughout the past year, cell and gene therapy (CGT) entered a harvest season, with six CGT drugs approved for market launch globally, setting a new historical record. Additionally, CGT products achieved significant breakthroughs across multiple dimensions, including the first gene-editing drug, the first allogeneic cell therapy product, and the first gene therapy drug for ex vivo treatment.

Notably, last December, the U.S. FDA approved the first gene-editing therapeutic drug, accelerating the clinical launch of gene-editing therapies in the United States. Developed jointly by CRISPR Therapeutics and Vertex Pharmaceuticals, Casgevy is the world’s first CRISPR/Cas9-based gene therapy, indicated for the treatment of sickle cell disease (SCD).

Beyond the bustling activity in the industry, local governments are also boosting the development of CGT.On February 1, 2024, the Beijing Municipal People’s Government officially released the “List of Key Tasks for the 2024 Municipal Government Work Report,” which explicitly listed strengthening the layout of cell and gene therapy as one of the key tasks. In September last year, the Shanghai Municipal Science and Technology Commission issued the “Notice on the Guidelines for Project Declaration of the 2023 ‘Science and Technology Innovation Action Plan’ Special Project on Cell and Gene Therapy in Shanghai,” providing targeted support for four major thematic areas: research on new targets and mechanisms in cell (gene) therapy, research on key core technologies, investigator-initiated clinical studies, and the construction of clinical medical research centers.

Additionally, VCBeat has learned that local governments have planned specialized industrial parks and actively addressed bottlenecks in application processes and medical insurance policies, thereby providing substantial software and hardware infrastructure to support the development of the CGT industry.

Certainly, investment opportunities in the biopharmaceutical sector extend beyond GLP-1 drugs, ADC platforms, and CGT therapies. Lin Guanyu, Investment Director of the Healthcare Industry Fund at SCGC (Shenzhen Capital Group Co., Ltd.), stated that SCGC follows key logical threads including population aging, shifts in disease spectra, consumption upgrading, and cost reduction with efficiency improvement. Starting from clinical needs, the firm focuses on high-quality enterprises in niche sectors such as CNS disorders, consumer healthcare, anti-aging, and synthetic biology.

Luo Fei, Founding Partner of Green Pine Capital, stated that the firm would deploy innovative technologies around new disease clusters, with a current focus on areas such as neurological disorders. Taking Basiceus, a company invested in by Green Pine Capital last year, as an example, the enterprise specializes in the field of nervous system diseases. It possesses small-molecule and peptide drug R&D platforms, in vitro molecular and cellular drug screening platforms, and in vivo animal efficacy evaluation platforms. Furthermore, it has established a comprehensive system covering drug design, screening, evaluation, CMC, and clinical research, enabling rapid development.

Not only that,A review of the financing landscape over the past five years reveals that small-molecule chemical drugs account for more than one-quarter of all financing events in the biopharmaceutical sector, underscoring their status as a core investment track.Meanwhile, there is also consistent investment in AI-driven new drug development, 3D-printed pharmaceuticals, and the pharmaceutical supply chain, with ample opportunities still available.

Innovative Medical Devices Sector: Ophthalmology and Cardiovascular Fields Ignite Investment Enthusiasm, with Commercialization Capability Becoming a Key Metric

Domestic Innovative Medical Devices Are Entering a Critical Turning Point.

On the one hand, breakthroughs in multiple key upstream technologies for medical devices—such as software, complex functionalities, and real-time 3D imaging in ultrasound—have been achieved, driving domestic substitution into deeper waters. On the other hand, the commercialization of innovative medical device enterprises in China is accelerating, with 56 innovative medical device products approved in 2023.

In other words, companies developing innovative medical devices have entered a phase of accelerated marketization, making commercial implementation capability a key indicator for assessing their long-term stability and success.

In terms of specific target selection, institutions vary in their approaches. For instance, Matrix Partners China (MPCi) pays particular attention to “new players” in traditional major sectors, where there are opportunities for generational leapfrogging in commercialization. Following this logic, MPCi has invested in companies such as Ruilong Nuofu, Weiguang Medical, and New Light Vision. Over the past year, these enterprises have achieved rapid development; for example, Haishan Yi®, China’s first modular surgical robot developed by Ruilong Nuofu, has completed registered clinical trials in multiple departments.

“In the field of innovative medical devices, we pay particular attention to equipment and consumables that address clinical challenges currently without solutions, or where existing methods have significant room for improvement, thereby offering substantial incremental clinical value. Examples include devices for aortic arch lesions and structural heart disease; these products possess the potential to save lives or improve quality of life,” said Zhou Jufeng, Investment Partner at Paradise Silicon Valley Medical.

Fei Simin, a partner at Mingfeng Capital, told VCBeat that the firm is bullish on the consumer healthcare market and its niche sectors. It will continue to focus on differentiated pipeline opportunities within materials, investing in and empowering the application of new materials in healthcare—particularly in medical aesthetics—as well as exploring the potential for combining and compounding existing materials and their applications in serious medical care.

“In the medical device sector, the integration of complex technologies is gradually becoming mainstream. The upgrading of China’s domestic medical device industry has progressed from passive devices to active devices, and from low-end imitation to independent innovation driven by the convergence of multiple technologies. From a technological perspective, continuous attention is being paid to innovative technologies, including the application of foundational technologies such as minimally invasive techniques, new materials, artificial intelligence (AI), and robotics in the healthcare industry. From an application perspective, traditional fields such as cardiovascular disease, orthopedics, general surgery, and neurology have large patient populations and significant unmet needs, warranting sustained focus. Meanwhile, I believe consumer healthcare has emerged as a new key growth track, with substantial development potential in areas such as medical aesthetics, weight management, and ophthalmology,” stated Gao Jieliang, Senior Partner at CDH Innovation & Growth Fund (VGC).

Across various sectors, ophthalmology and cardiovascular medicine ignited investment enthusiasm last year, attracting numerous institutions to enter the market.

First, looking at the ophthalmology sector, its financing activity has remained highly active for three consecutive years. Product categories such as intraocular lenses (IOLs), optometry and vision care, minimally invasive glaucoma surgery (MIGS), ophthalmic equipment, and ophthalmic surgical robots have garnered significant attention.

“Humanity’s fear of blindness is second only to the fear of death. Many ophthalmic diseases are difficult to recover from after injury, making them clinically challenging conditions. Moreover, similar to the central nervous system (CNS) field, drug development in ophthalmology has progressed relatively slowly, creating significant opportunities for medical devices,” said Jiang Yangzhi, Partner at Delian Capital. “Delian Capital has recently made successive investments in the ophthalmology sector, including HiSight and Yaoshi Medical. Both companies have achieved substantial progress with their products. We hope that their products will receive regulatory approval as soon as possible, enabling patients to access these effective solutions earlier and addressing unmet clinical needs.”

Moreover, the surge in the ophthalmology sector is also driven by significant room for domestic substitution. It is worth noting that imported brands have historically dominated the ophthalmic device market, with import penetration reaching as high as 90% in the high-end segment. Furthermore, the optometry and vision care field exhibits strong consumer-driven characteristics, making it more resilient to policy uncertainty under the volume-based procurement (VBP) regime.

Therefore, multiple investors have indicated that in 2024, R&D breakthroughs and commercial progress in mid-to-high-end ophthalmic devices continued to be a focal point for capital. Additionally, the trend of ophthalmic devices evolving from specialized medical use toward consumer-oriented applications will further extend opportunities.

In the cardiovascular field, there is a vast amount of unmet clinical needs and mature market education, so it has always been the focus of medical technology innovation and a hot spot for investment in the device sector.Since the launch of centralized procurement, the cardiovascular sector has been steadily shedding its bubbles, steering the industry onto a virtuous trajectory driven by innovative products.

In terms of distribution across sub-sectors, products such as intracardiac echocardiography (ICE), ventricular assist devices (artificial hearts), polymer heart valves, shockwave balloons, atrial shunts, and bioresorbable stents have garnered the most attention.

From the perspective of industry development, cardiovascular innovation companies delivered strong performance in 2023. In terms of technological innovation, the long-awaited FDA approval of two renal denervation (RDN) products marked a significant milestone; the first domestically produced pulsed field ablation (PFA) system for atrial fibrillation received market approval, with this new technology creating an entirely new incremental market; furthermore, tissue-engineered blood vessels and polymer-based heart valves hold promise for ushering in a materials revolution.

Furthermore, the domestic cardiovascular industry chain has strengthened its capabilities, with leading enterprises that master the production of upstream precision tubing and raw materials emerging as top-tier suppliers in terms of both scale and technology.

Jiang Jiajia, Managing Director of the Healthcare and Life Sciences Division at China Renaissance Capital, told VCBeat that in the medical device sector, sub-sectors such as electrophysiology, endoscopy, high-end biomedical materials, specialized fields (including dentistry and orthopedics), and medical aesthetics have also achieved encouraging momentum.

For instance, the cardiac electrophysiology sector demonstrated encouraging industry progress at the turn of the year. Currently, China has a low penetration rate for cardiac electrophysiology procedures, making it a market with sustained expansion potential. Within this sector, MicroPort EP has established a comprehensive product portfolio through years of dedicated R&D, while Mindray, a leading domestic medical device manufacturer, has rapidly entered the field through strategic M&A. As an emerging technology in cardiac electrophysiology, Pulsed Field Ablation (PFA) achieved a breakthrough in late 2023. Medtronic’s PulseSelect became the first PFA system to receive FDA approval, followed closely by Boston Scientific in January 2024, when its FARAPULSE system gained FDA clearance for market launch.

“This has undoubtedly boosted the confidence of domestic companies in this field. In the future, as more companies race to obtain regulatory approvals, an increasing number of Chinese enterprises will be able to compete on a level playing field with international giants, leveraging their independent innovation and technological prowess,” said Jiang Jiajia.

China's endoscopy industry also achieved leapfrog development in 2023.The primary drivers behind this trend are policy support and breakthroughs in new technologies. These include favorable policies such as domestic procurement standards, subsidized loan procurement, and the “Thousand Counties Project,” as well as a shortened registration cycle (with reclassification from Class III to Class II medical devices). Meanwhile, fundamental technological innovations—such as integrated fluorescence, 3D, and 4K imaging technologies—have laid the foundation for Chinese manufacturers to overtake competitors on the curve.

Undoubtedly, amid technological breakthroughs and accelerating commercialization, the narrative of domestically produced innovative medical devices is gradually shifting from a focus on low-value consumables and distribution toward mid-to-high-end import substitution and independent innovation.

Digital Healthcare Sector: AI Sparks a New Wave of Revolution in Medical Scenarios, with Digital Therapeutics Products Gaining Intensive Approvals

Digital healthcare has been rapidly transforming the medical and health industry since its inception. For instance, in 2023, ChatGPT became the most sensational news across the entire technology sector, demonstrating generative AI’s capability to produce text or images from complex user prompts, which prompted numerous healthcare companies to follow suit.

For example, Siemens Healthineers leverages generative AI to enable users to quickly locate and highlight corresponding areas in reports by clicking on medical images, through the loading, linking, and preparation of an intelligent chat system. Additionally, Siemens Healthineers uses AI to dynamically generate diagnostic imaging reports and prioritize them based on importance, allowing physicians to process information more efficiently.

For another example, Dajing TCM has launched the “Qihuang Wenda·Large Model,” which has evolved into three sub-models. The first sub-model is a large clinical diagnosis and treatment model based on confirmed diseases; it can provide syndrome differentiation (diagnosis) results and treatment plans (Chinese herbal prescriptions) according to the disease, symptom, and sign information provided by users.

“If we were to identify a single exciting systemic variable in the healthcare industry over the next decade, it would undoubtedly be AI. It will bring about profound changes across various sectors. AI is not just ChatGPT; it will have a deep and far-reaching impact on the industry. In healthcare, beyond its applications in medical imaging and surgical navigation, AI-powered products can also empower the research and development of medical devices and pharmaceuticals,” said Sun Qi, Founding Managing Partner of Dalton Venture.

Furthermore,Digital technology’s empowerment of biotechnology also offers significant room for imagination.“IBAT is a key focus area for Delian Capital. IBAT = IT + AT + BT, representing the empowerment of biotechnology by information technology and artificial intelligence,” said Jiang Yangzhi, Partner at Delian Capital. Qinglian Bai’ao is a company in which Delian Capital invested in 2023 to establish its presence in the field of plasma proteomics. Leveraging its technologies for capturing low-abundance proteins and automating sample pre-processing, the company provides proteomic data support to address prominent challenges in new drug development, such as the “lack of novel targets” and the need to “enhance druggability.” The simultaneous publication of three landmark articles on plasma proteomics in Nature earlier this year serves as the most compelling evidence of this capability.

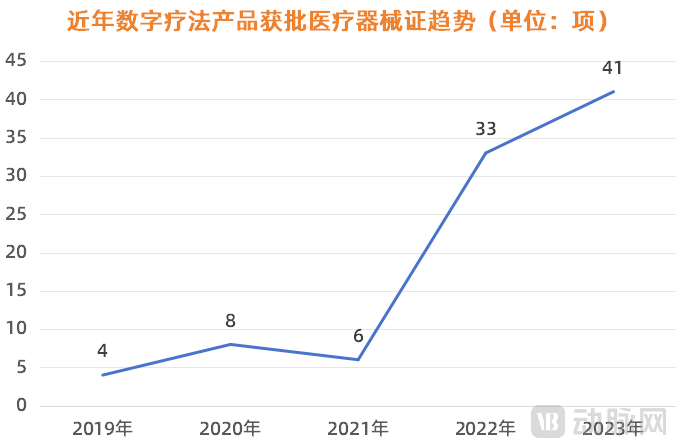

Digital therapeutics continued to achieve breakthroughs in 2023, with a total of 41 digital therapeutic products approved throughout the year., primarily focusing on the treatment of psychiatric/neurological disorders, respiratory therapy, ophthalmology, and post-operative/sports rehabilitation.

As a new hotspot in digital healthcare, the keyword for digital therapeutics is “intervention.” Digital products will become the core of diagnosis and treatment, directly assuming the role of drugs or medical devices to deliver genuine clinical efficacy. Like traditional pharmaceuticals, they require evaluation through evidence-based medicine and approval from drug regulatory authorities. In a sense, as a novel therapeutic modality, the emergence of digital therapeutics has redefined the form of medication.

However, multiple investors have stated that while digital therapeutics are developing rapidly, attention must also be paid to patient experience, as it determines reimbursement. Based on most current digital therapeutic products, the majority enhance the efficiency of healthcare delivery or physicians, with no significant improvement in patient efficiency.

Medical Services Sector: Consumer-Oriented Specialties Pivot to “Small and Beautiful,” While Critical Care Specialties Focus on Deepening Expertise

China’s private healthcare services sector is undergoing a structural transformation.

Currently, consumer healthcare specialties such as ophthalmology, dentistry, and medical aesthetics have become highly mature, with several regional leaders emerging, leading to intensified competition. In this context,Consumer Healthcare Specialties Are Shifting Toward a "Small and Beautiful" Model。

Taking ophthalmology as an example, the era of high-growth dividends for specialized eye hospitals has passed, while the dividend era for “small yet beautiful” optometry clinics has begun. Last year, whether it was Autek China raising RMB 1.5 billion through a private placement to expand into the terminal optometry market (eye clinics and optometry centers), Aier Eye Hospital stating at its shareholders’ meeting its intention to “build 1,000 optometry clinics,” or Huaxia Eye Hospital planning to newly establish 200 optometry centers, all these moves underscore the emphasis industry giants are placing on the “small yet beautiful” optometry market.

In the dental sector, chain expansion and scaling were the dominant themes over the past decade. However, in the last one to two years, some investors have gradually come to believe that scaling may not be an optimal model for dental practices, with “small but beautiful” clinics being better suited to market demands. The rationale is that the core of the dental business lies in dentists. To establish a nationwide chain, it is necessary to replicate dentists’ capabilities on a large scale. Yet human talent cannot be replicated, and the cost of recruiting high-quality dentists is substantial. Consequently, as scaling efforts ramp up, dental institutions often find themselves unprofitable.

Beyond consumer healthcare, critical and severe specialty fields such as cardiology, oncology, and neurology are also emerging as opportunity windows in the non-public medical sector. This January, Meizhong Jiahe, a leading private oncology healthcare provider, listed on the Hong Kong Stock Exchange, joining other private enterprises specializing in critical and severe care such as Hygeia Healthcare and Sanbo Brain Hospital.

The increasing number of enterprises securing financing and completing initial public offerings (IPOs) demonstrates that private specialized medical services, provided they possess excellent diagnostic and therapeutic capabilities and innovation, can transcend disciplinary barriers and emerge as market leaders in various niche segments.

In future trends,The specialty of critical and severe care focuses on achieving depth and thoroughness.For instance, the aggregation of high-quality expert resources is a top priority, particularly for specialized medical service institutions focused on serious healthcare. Taking the publicly listed Sanbo Brain Hospital as an example, its flagship institution is Capital Medical University Sanbo Brain Hospital. In the rankings of medical service capabilities published by the Beijing Municipal Health and Family Planning Commission, this hospital has consistently ranked among the top in neurosurgery alongside Tiantan Hospital and Xuanwu Hospital for many consecutive years. In terms of its expert team, Sanbo Brain Hospital boasts renowned neuromedicine specialists such as Luan Guoming, Yu Chunjiang, Shi Xiang’en, Wang Baoguo, Yan Changxiang, Wu Bin, Lin Zhixiong, and Fan Tao, thereby forming a robust team of experts.

Additionally,High-quality enterprises will also emerge in the more segmented medical specialty services sector.. For instance, in fields such as pediatric dentistry, otorhinolaryngology and ophthalmology, and aesthetic dermatology, there is still significant room for improvement in patient education. In this context, introducing segmented and precise positioning while ensuring the quality of medical services and patient experience can effectively capture the corresponding customer base.

It is important to note that the healthcare services sector is a “slow industry,” requiring investment institutions to possess the patience and perseverance of long-termism.