How Swedish Orphan Biovitrum (Sobi) Defied Acquisition Bids from Pfizer, Biogen, and AstraZeneca to Carve a Niche in the Competitive Rare Disease Market

Sobi

Rare Disease Drug Provider, Specialty Drug Developer and Marketer

In September 2021, as early autumn brought cooling temperatures to Sweden, the healthcare market had yet to ignite significant interest in the Nordic region. Nevertheless, a major acquisition deal still sent shockwaves through the otherwise calm Nordic capital markets: private equity giant Advent International and Aurora, an affiliate of GIC Special Investments, proposed a $7.6 billion acquisition of Swedish rare disease pharmaceutical company Sobi. The two firms offered SEK 235 per share ($25.72 per share), representing a 34.5% premium over Sobi’s opening price on August 25, 2021.

At the time, it was the largest acquisition by value in the Nordic market in several years.

However, for the two major investment firms to successfully complete the acquisition, they need to secure support from 90% of Sobi’s shareholders. It is rare for a high-value acquisition deal to gain such widespread attention, yet few people delve into a thorough discussion of this particular clause.

As Sweden entered winter and December arrived, just as everyone assumed the acquisition was a done deal, pharmaceutical giant AstraZeneca suddenly intervened, blocking the highly anticipated transaction by citing its withholding of the 8% stake it held.

Regarding the underlying reasons, there has been a flurry of speculation within the industry. According to Bloomberg, if Sobi is ultimately sold, the rights to palivizumab—marketed as Synagis for the treatment of severe respiratory syncytial virus (RSV) in children—held by Sobi will be lost. These rights originally belonged to AstraZeneca. Reportedly, it was not until late 2018 that AstraZeneca agreed to divest and sell the U.S. rights to Synagis to Sobi.

On the surface, it appears that AstraZeneca, as an unexpected interloper, blocked this acquisition; however, as early as 2015, Sobi had already rejected acquisition offers from Pfizer and Biogen on the grounds that they were “too low.”

Who exactly has given Sobi such confidence and resilience, enabling this Nordic company—repeatedly at the center of controversy—to maintain its independent operations through numerous upheavals? As former partners have exited via acquisition, what has allowed Sobi to stand firm to this day, even after a significant drop in market capitalization?

Restructuring, Mergers, and Rebirth: The Swedish Rare Disease Giant Born from a Brewery

Sobi’s official website states that the company’s history dates back to the 1930s, with its predecessor, Kabivitrum, initially formed through the merger of two companies, Kabi and Vitrum. Tracing its roots further reveals that Sobi’s heritage can be traced all the way back to Kongens Bryghus, a brewery established in the 17th century.

Kongens Bryghus, originally situated at the corner of the Frederiksholm Canal in Copenhagen, the capital of Denmark, was twice destroyed by fire and rebuilt during the Thirty Years' War. It later relocated across the river and operated as a warehouse until the early 19th century. By the late 19th century, Kongens Bryghus had become a renowned brewery brand. It subsequently merged with several other breweries, leading to the establishment of the new company Kärnbolaget Aktiebolag Biokemisk Industri in Malmö, Sweden, in 1931, with Kabi founded as its subsidiary.

However, at that time, Kabi was only engaged in the partial production of vitamin C formulations, and it would still be some time before it formally entered the medical field.

The company’s true entry into the healthcare sector occurred during World War II. There was an urgent need on the battlefield for a safe, effective, compact, and easily storable and transportable plasma volume expander to treat wounded soldiers. Meanwhile, Professor E.J. Cohn at Harvard University in the United States and his research team developed a process known as cold ethanol fractionation to purify human serum albumin from human blood, marking the birth of the first blood-derived product.

In response to wartime policies, Kabi began producing dried plasma for the armed forces and subsequently expanded its production scope to include various blood products, such as albumin. With the successful isolation of intramuscular human immunoglobulin and human coagulation factor VIII, along with the establishment of an industrialized production system for blood products, Kabi has continuously developed its blood products business.

In 1972, after merging with Vitrum, Kabi was officially renamed KabiVitrum, the predecessor of Sobi. In the 1980s, KabiVitrum partnered with Genentech to jointly develop the methionine-free growth hormone Genotropin.

Unexpectedly, the name KabiVitrum did not last long either. In 1990, Procordia, the state-owned enterprise that owned KabiVitrum, acquired a stake in Pharmacia, a well-known Swedish pharmaceutical company, and merged several of Pharmacia’s divisions to establish Biovitrum.

At this juncture, Biovitrum, having undergone multiple mergers and restructurings, had completely distanced itself from its 17th-century origins as a riverside brewery, transforming into a modern pharmaceutical enterprise. It successively entered into a series of agreements with Wyeth (now part of Pfizer) and Syntonix (later associated with Biogen, Bioverativ, and now Sanofi). These strategic collaborations precisely enhanced Biovitrum’s R&D capabilities in hematology, seemingly laying the groundwork for the company’s next phase of development.

Finally, in 2010, Biovitrum’s investors acquired the Swedish orphan drug pioneer Swedish Orphan International and established a new company, Swedish Orphan Biovitrum AB, known as Sobi.

We need to pay special attention to the emergence of Sobi, as this acquisition brought Orfadin® (nitisinone), which later became an important drug for Sobi; it was also in this year that the company's leadership decided to advance its two existing hemophilia candidate drugs into pivotal Phase 3 clinical trials, subtly outlining Sobi's future development direction.

Boldly Trim Early-Stage Pipeline, Strategically Focus on Core Therapeutic Areas

In 2013, just three years after its establishment, Sobi went public on the Nasdaq Stockholm Exchange, leveraging its substantial historical foundation and an increasingly refined business model, thereby becoming the first pharmaceutical company to list in Sweden in nearly eight years.

Since then, Sobi has built its rare disease business through a series of acquisitions while repeatedly rejecting takeover offers from Pfizer and Biogen on pricing grounds. It can be said that it is precisely because Sobi understands the significance of mergers and acquisitions to its development journey that it has been particularly cautious in considering its own exit strategy.

In 2018, Sobi acquired global rights to Gamifant® (emapalumab) from antibody therapeutics developer Novimmune. Gamifant® is the first therapy approved by the U.S. Food and Drug Administration (FDA) for the treatment of primary hemophagocytic lymphohistiocytosis (HLH). This move strengthened Sobi’s immunology franchise.

2019 was a pivotal year for Sobi.

On one hand, accelerating acquisitions: In addition to completing the acquisition of U.S. rights to AstraZeneca’s lower respiratory tract infection drug Synagis (palivizumab), thereby securing the right to receive 50% of future U.S. market revenues from AstraZeneca’s candidate drug MEDI8897, Sobi also acquired U.S. biopharmaceutical company Dova for $915 million. This deal granted Sobi Doptelet® (avatrombopag), indicated for adult patients with primary chronic immune thrombocytopenia (ITP) who have had an insufficient response to other therapies, which was then in Phase 3 clinical trials.

On the other hand, perhaps recognizing that for large pharmaceutical companies, mergers and acquisitions (M&A) remain one of the few effective strategies to replenish their pipelines—given the scarcity of suitable M&A targets—Sobi has not only precisely identified its acquisition targets but also made every effort to secure development and exclusive commercialization rights. This strategy is evident in its collaborations with companies such as Apellis Pharmaceuticals and ADC Therapeutics.

Furthermore, Sobi made a bold decision: to strengthen its focus on late-stage R&D in hematology and immunology, while discontinuing discovery or early-stage research outside its core therapeutic areas.

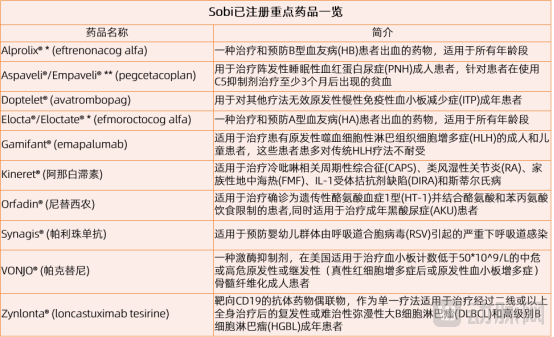

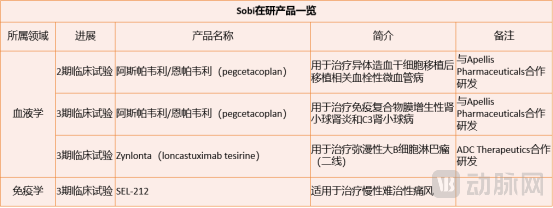

Currently, Sobi centers its operations on rare diseases, focusing on three core therapeutic areas: hematology, immunology, and specialized care. The company has a clearly defined product portfolio, comprising both marketed products and those in Phase II and Phase III clinical trials.

Source: Sobi official website; graphic by VCBeat

Source: Sobi official website; Graphic by VCBeat

Synagis® (Palivizumab)

Palivizumab is a humanized monoclonal antibody. Humanized monoclonal antibodies are typically generated by grafting the complementarity determining regions (CDRs) of non-human monoclonal antibodies onto the amino acid sequence of human monoclonal antibodies, thereby preserving the antibody’s neutralizing activity while reducing the immunogenicity of xenogeneic antibodies.

Palivizumab was developed by humanizing the murine monoclonal antibody 1129, grafting its complementarity-determining regions (CDRs) onto a human IgG1 antibody framework. This biologic was initially developed by MedImmune and received approval from the U.S. Food and Drug Administration (FDA) in 1998. Palivizumab was subsequently acquired by AstraZeneca in 2007 and then by Sobi in 2008. It remains the only approved monoclonal antibody for prophylactic use.

Palivizumab is expensive and has a short half-life, requiring monthly intramuscular injections throughout the HRSV infection season; therefore, it is recommended only for premature infants, immunocompromised children, and elderly patients with pulmonary comorbidities.

Synagis® (palivizumab) is one of Sobi’s key products and a major source of its revenue.

VONJO® (pacritinib)

Pacritinib, an oral tyrosine kinase inhibitor originally developed by Baxter International and its partner CTI Biopharma, has been acquired by Sobi. Pacritinib exhibits dual activity against JAK2 and FLT3. Studies have shown that mutations in these kinases are directly associated with the development of various hematologic cancers, including myeloproliferative neoplasms, leukemia, and lymphoma.

Pacritinib effectively treats disease symptoms while causing less drug-induced thrombocytopenia and anemia, side effects commonly observed with currently approved and investigational JAK inhibitors; therefore, pacritinib offers advantages over other JAK inhibitors.

Orfadin® (Nitisinone)

Nitisinone is a 4-hydroxyphenylpyruvate dioxygenase inhibitor, used in combination with dietary restriction of tyrosine and phenylalanine for the treatment of hereditary tyrosinemia type 1 (HT-1) in adults and children.

Nitisinone is the only effective drug for the treatment of HT-1 and is recommended as the first-line therapy in international guidelines.

Currently, Orfadin® (nitisinone) is an important component of Sobi’s Specialty Care business segment.

Acquisition Turmoil Triggers Market Cap Plunge; Core Product Revenue Stages a Dramatic Recovery

Looking back at 2023, the biopharmaceutical industry faced numerous challenges, particularly evident in the widespread pipeline cuts by major companies and a growing market trend toward “fewer products.” Although Sobi still achieved an 18% revenue growth in 2023, this does not mean that its development since its formal establishment has been smooth sailing.

Let us revisit the unfinished M&A deal from late 2021: AstraZeneca, holding an 8% stake in Sobi, along with several other shareholders, voted “against” the transaction and decided to retain their shares. As a result, EQT Partners and GIC Special Investments ultimately secured only 87% of the shares, forcing the abandonment of what would have been Europe’s largest acquisition that year.

What was not previously mentioned is that following the announcement, Sobi’s stock price plummeted by nearly 25%, wiping out almost a quarter of its market capitalization.

Sobi did not collapse.

At this point, Sobi’s deep-rooted strengths from its earlier years began to pay off. Throughout 2022, Sobi, which had previously pursued a high-profile expansion strategy, suddenly shifted course and embarked on a low-key turnaround path: accelerating R&D and regulatory submission processes to rapidly drive product commercialization and escape its predicament.

This year, Sobi achieved significant milestones: its product Gamifant® (emapalumab) was approved in China for the treatment of hemophagocytic lymphohistiocytosis (HLH); Alprolix®* (eftrenonacog alfa) received FDA approval as a breakthrough therapy for the treatment of Hemophilia A; and Zynlonta was approved in the European Union for the treatment of relapsed or refractory diffuse large B-cell lymphoma.

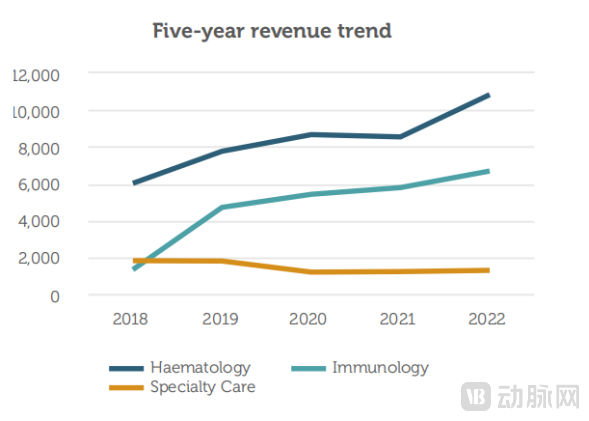

Meanwhile, Sobi’s 2022 Annual Sustainability Report indicates that the company’s overall product revenue has been on a continuous growth trajectory over the past five years. Although revenue from specialized care products showed a slight downward trend after 2019, Sobi’s core portfolio—hematology and immunology products—has continued to grow steadily, with hematology revenue experiencing a greater year-over-year increase in 2022 compared to previous years.

Sobi’s Product Revenue Trends Over the Past Five Years

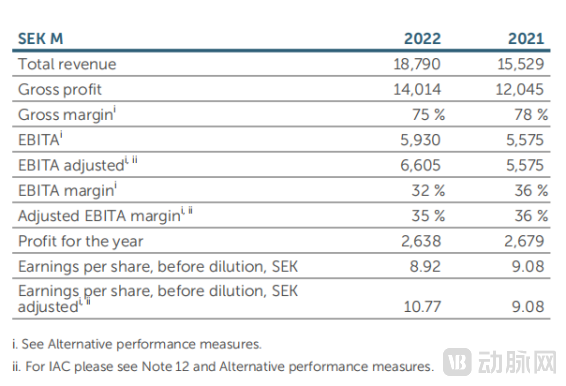

In 2022, Sobi’s total revenue reached SEK 18.79 billion, representing a 21% increase compared to 2021. Revenue from the Hematology segment amounted to SEK 10.831 billion, a 27% year-over-year increase, primarily driven by sales of proprietary products, fees for the production of active pharmaceutical ingredients (APIs) for Pfizer’s ReFacto AF/Xyntha, and royalties from Sanofi’s sales of Elocta®/Eloctate®** (efmoroctocog alfa) and Alprolix®* (eftrenonacog alfa). Revenue from the Immunology segment totaled SEK 6.679 billion, a 16% increase from the previous year, mainly attributable to product sales. Revenue from Specialty Care was SEK 1.28 billion, reflecting a 6% year-over-year increase.

Sobi's Financial Revenue in 2022

Epilogue: A Challenging Future, Expanding into the Asian Market

In May 2023, following a one-year turnaround, Sobi returned to the capital markets by announcing the acquisition of CTI BioPharma (NASDAQ: CTIC), a commercial-stage biopharmaceutical company focused on the development and commercialization of novel targeted therapies for hematologic cancers. Sobi will acquire CTI in an all-cash transaction at $9.10 per share of common stock, implying an equity value of approximately $1.7 billion. Notably, this offer price represents an 89% premium over CTI’s closing stock price on May 9, 2023.

Interestingly, VONJO® (pacritinib), the product acquired by Sobi, had already received accelerated approval from the FDA in 2022. It can be said that Sobi strategically targeted this asset when launching its premium-priced acquisition. Given that hematology-related products, particularly plasma-derived therapies, account for nearly half of Sobi’s revenue, adding VONJO® to its portfolio is expected to further strengthen Sobi’s competitive position in the rare disease sector, which is increasingly contested by major industry players.

However, even for Sobi, which has overcome numerous challenges, the future is not without obstacles. Following the acquisition of VONJO® (pacritinib), Sobi will immediately face competition from Incyte and GlaxoSmithKline, whose respective products Jakafi and momelotinib share similar mechanisms of action with VONJO® (pacritinib).

Fortunately, Sobi’s Q4 2023 financial report, released in early 2024, showed that revenue continued to grow steadily. Moreover, at the beginning of 2024, Sobi established a joint venture in South Korea. Guido Oelkers, CEO of Sobi, stated that operations in South Korea would commence with Doptelet® and Aspaveli®/Empaveli®, further expanding treatment options for patients with rare diseases.