On the Eve of a Major Reshuffle: Power Is Shifting in Global Pharma, as Revealed by Top 10 Companies' Q1 2026 Earnings

Johnson & Johnson

Medical Device R&D and Manufacturer

The financial reports for the first quarter of 2026 have mostly been released, and the competitive rankings in the global pharmaceutical industry have undergone a profound restructuring. By placing three sets of key data side by side, the overall pattern emerges automatically.

Group 1: Eli Lilly's quarterly revenue reached $19.8 billion, a year-on-year increase of 56%, securing the top position on the global pharmaceutical revenue leaderboard. At the same time, the full-year performance guidance has been raised to a range of $82 billion to $85 billion. Back in 2019, this company was still lingering at the bottom of the industry's top ten. In seven years, it has risen to the center of industrial power.

Group Two: Novo Nordisk's quarterly revenue exceeded $15 billion for the first time, propelling it into the top four pharmaceutical companies globally. The entire portfolio of semaglutide contributed approximately $8.3 billion. A decade ago, considering a Danish insulin company as part of the "top tier of global pharmaceuticals" would have been seen as unrealistic. Today, no one is laughing.

Group Three: Merck fell out of the top five. Due to the expiration of Entresto's patent, Novartis' single-quarter revenue declined by 5% year-on-year. Pfizer, weighed down by a cliff-like drop in COVID-19 vaccine sales, slipped to eighth place. These three companies encountered the same barrier: the patent cliff. In front of this barrier, no one is spared.

These three sets of figures are not isolated incidents but rather three links in the same logical chain. As one end rises sharply, the other accelerates its decline, pushing the entire competitive landscape into structural reorganization. And we are standing at the prelude to this reorganization— the real reshuffling has only just begun.

The Great Shuffle: Who's Rising, Who's Falling, Who's Stabilizing

To understand the driving force behind the changes in rankings, it is necessary to observe two pictures simultaneously: one is revenue, and the other is market value.

Revenue reflects the operating performance of the past year. Market value represents the discounting of market expectations for many years to come. The gap between the two implies the market's deepest judgment.

Ranked by revenue, the global pharmaceutical first-tier lineup has been reshuffled in the first quarter of 2026.: Eli Lilly leads with a revenue of approximately $19.8 billion. Johnson & Johnson's pharmaceutical business follows with about $15.4 billion, while AstraZeneca secures the top three with approximately $15.3 billion in total revenue. Novo Nordisk is close behind with around $15.1 billion. The threshold for entering the top ten has further increased to approximately $12.337 billion.

Figure: Ranking of Top Global Pharmaceutical Companies by Q1 2026 Revenue

Look at the market value againLilly has dropped from a peak of trillion dollars to approximately 959.3 billion, still nearly twice the size of the second place. Johnson & Johnson, at about 574.3 billion, ranks second. AbbVie, at approximately 367.8 billion, ranks third. AstraZeneca and Merck respectively rank fourth and fifth with 316.4 billion and 299.8 billion.

Cross-compare the market capitalization ranking with the revenue ranking, and three structural fissures become clearly apparent:

The First Rule: The Metabolic Track Replaces Oncology as the Largest Growth Engine in the Pharmaceutical Industry。

The most dramatic changes in the rankings — Eli Lilly surged from the bottom of the industry to the top, and Novo Nordisk broke into the top four from around tenth place — are both rooted in the GLP-1 metabolism track.

This is not a coincidence, but the concentrated realization of track dividends. The shift in industry logic often happens quietly, without prior notice.

Article 2: Over-reliance on a single blockbuster drug is evolving from a once protective moat into a systemic risk.

Merck's Keytruda raked in approximately $8 billion in a single quarter, already claiming the top spot in global单品 sales. However, its patent protection is set to end on schedule in 2028. When the market fully prices in this estimated $23 billion gap, the capital market's verdict through "voting with their feet" will be far more efficient than analysts' predictions.

Article 3: In the face of the patent cliff, there is no room for侥幸.

Novartis' Entresto Quarterly Sales Plummeted 42% to $1.31 Billion, Directly Impacting the Company’s Overall Revenue with a 5% Year-on-Year Decline. Pfizer's COVID-19 Vaccine Sales Dropped Sharply from a Peak of Nearly $38 Billion to $232 Million in a Single Quarter.

The free fall after the exclusivity period ends spares no drug. This is the harshest lesson of the patent system: it grants you a monopoly long enough to reap profits, then promptly withdraws this barrier the moment it expires.

Beneath the Surface: The Deep Logic of Seating Changes

1. Metabolism Track: The $100 Billion Race Under the Duopoly

Lilly's Mounjaro, the glucose-lowering version of tirzepatide, generated $8.66 billion in a single quarter, representing a 125% year-over-year increase. Zepbound, the weight-loss version of tirzepatide, achieved $4.16 billion in the same period, marking an 80% year-over-year growth. Combined, the two products amounted to approximately $12.8 billion, accounting for about 65% of the company’s total revenue.

Within a quarter, the incremental contributions of these two products have surpassed the annual output of most global pharmaceutical companies' entire pipelines. The commercial ceiling for a single drug is being redefined by this set of data.

Novo Nordisk's full range of semaglutide products totaled approximately $8.3 billion. However, the other side of the data reveals the pressure Novo Nordisk is facing: Ozempic sales declined by 8% year-on-year, Rybelsus dropped by 15%, and the overall market in China fell by approximately 22.5%. Wegovy increased by 12% year-on-year to $2.863 billion, being the only highlight still showing growth.

Figure: GLP-1 Core Single Product Q1 Sales Data

Under the dual-headed pattern, Eli Lilly's competitiveness in the metabolic track is further expanding: capturing 60.1% of the U.S. market share, the oral GLP-1 drug Foundayo has been approved for marketing, aThe Moat of Product MatrixHas begun to take shape.

2. Oncology Track: The Throne Remains, But Shadows Are Lengthening

Keytruda's Single-Quarter $8 Billion Revenue Retains Its Status as the World's Top-Selling Drug. However, This Achievement Bears the Countdown to Patent Expiration: 2028.

Merck attempted a defensive layout with the subcutaneous injection formulation Keytruda QLEX, which contributed approximately $128 million in a single quarter. The aim is to buy some time for this brand after the expiration of the intravenous infusion patent.

But the capital market won't change its judgment just because of an improvement in injection methods. When the fate of a product is tied to the lifespan of a single patent, tweaks can only delay the inevitable, not reverse it.

AstraZeneca is a more noteworthy diversified example in the oncology field. Tagrisso revenue reached $1.833 billion, increasing by 5%. Imfinzi grew by 30% to $1.694 billion. Enhertu surged 34% to $831 million, with an annualized brand scale of approximately $5 billion.

The three drugs are positioned in three distinct细分 markets of oncology: EGFR-mutant lung cancer, immune checkpoints, and HER2 ADC, with no competitive overlap between them. This structure implies that even if one drug faces patent expiration pressure, the other pipelines can still provide a buffer.

The valuation premium that AstraZeneca commands in the market is essentially pricing this structural resilience — not betting on the luck of a single molecule, but purchasing a risk-diversified pipeline layout.

3. Autoimmunity Track: The Quiet Growth Axis

Sanofi's total revenue in the first quarter was approximately $12.29 billion, a year-on-year increase of 13.6%. The core driver remains Dupixent, with single-quarter sales reaching €4.2 billion, a year-on-year increase of 30.8%, or approximately $4.9 billion. Over the past decade, Dupixent has expanded from a treatment for atopic dermatitis to multiple indications including asthma, sinusitis with nasal polyps, and eosinophilic esophagitis, with annual sales now surpassing the $20 billion mark.

Johnson & Johnson's pharmaceutical segment revenue increased by 11.2% year-over-year to $15.4 billion, with its immunology business as the core pillar.

The growth logic of the autoimmune track is certain and continuous: a large patient base, mostly requiring lifelong medication, and a high degree of standardization in clinical endpoints. However, the potential of traditional TNF inhibitors and IL inhibitors is nearly exhausted. The real growth lies in the next generation of autoimmune therapies, especially whether TCE can achieve immune reset, meaning whether it can rewrite immune memory.

That is the next truly exciting turning point in this track.

4. Patent Cliff: The Mirror of the Weightless

Novartis and Pfizer respectively demonstrated two forms of the patent cliff.

Novartis Pulled by the Gravity of a Single Product: Entresto Plummets 42% in a Quarter, with an Estimated Annual Loss of $4 Billion. A Core Pillar Nearly Vanished Overnight.

Pfizer, on the other hand, is experiencing a systematic contraction after the retreat of the COVID-19 dividend. Sales of the COVID-19 vaccine plummeted from a peak of over $10 billion in a single quarter in 2021 to about $232 million now, marking the complete closure of a temporarily constructed revenue channel.

The patent cliff is not an accidental event; it is the quid pro quo of the patent system. When a drug contributes billions or even tens of billions of dollars in annual profits to a company, the end of its exclusivity period will be repeatedly discounted by the capital market until there is no room left.

Many companies regard the patent exclusivity period as a moat. But a moat is not permanent property; it’s merely a lease that must be returned to generics upon expiration.

Outlook: The Center of Next-Generation Industrial Power

1. The ceiling for single-drug treatments continues to rise.

A basic fact is that the commercial ceiling for single products in the metabolic sector has yet to reach its boundary.

Lilly Raises 2026 Full-Year Revenue Guidance to $82 Billion to $85 Billion. If Estimated Based on Tirzepatide's Current 65% Share, Its Annual Contribution Is Expected to Exceed $53 Billion. Semaglutide’s 2025 Full-Year Sales Have Reached $29.3 Billion, and the Total Series Is Expected to Reach $35 Billion in 2026.

The combined annual sales of the two drugs are approaching $90 billion. This figure has surpassed the total annual revenue of the vast majority of pharmaceutical companies globally. The upper limit rule of single-drug commercial value is being redefined by GLP-1.

2. The race for GLP-1 is far from over

The competitive density in the GLP-1 track is accelerating on a quarterly basis. Since the first quarter of 2026, three key developments have been reshaping the competitive landscape:

Oral Formulations Break Injection Monopoly. Eli Lilly's Foundayo Approved for Market Launch, Currently the Only GLP-1 Oral Drug with No Dietary Restrictions and Can Be Taken at Any Time. The Oral Weight-Loss Version of Wegovy Pill Contributed $354 Million in a Single Quarter; Its Initial Sales Growth Has Surpassed That of the Injectable Form During the Same Period.

Biased Agonist Completes First Prescriptions in China. On April 27, 2026, Enoglutide, a new generation cAMP-biased GLP-1 receptor agonist, was simultaneously prescribed for the first time in Beijing and Shanghai. The biased mechanism is believed to selectively activate specific signaling pathways, maintaining weight loss and blood sugar reduction efficacy while reducing gastrointestinal adverse reactions such as nausea.

Multi-Target Extends to Quintuple Agonist. On April 29, 2026, *Nature* published a preclinical study: the world's first single-molecule quintuple receptor agonist targeting GLP-1R, GIPR, and PPARα/γ/δ completed concept validation, demonstrating superior metabolic improvement effects in animal models.

From single-target to dual-target, and then to triple-target and five-target, the imaginative space of this track is far from closed. GLP-1 is no longer just the story of a drug; it represents the ongoing deep exploration of a biological pathway.

3.ADC: The Next Certain Growth Pole

The ADC track is becoming the sector with the most systematic investment opportunities in the field of oncology.

Frost & Sullivan predicts that the global ADC market size will expand from approximately USD 14 billion currently to about USD 64.7 billion by 2030, with a compound annual growth rate of approximately 30%, significantly higher than the overall level of biologics. Frost & Sullivan further predicts that the ADC market is expected to exceed USD 66 billion by 2030.

The technical logic driving this continued growth is clear: Enhertu has validated the feasibility of ADCs replacing chemotherapy across various cancer types. TROP2 ADC Datroway's quarterly revenue grew more than 10 times year-over-year, and its annualized sales have surpassed $100 million after partnering with Daiichi Sankyo.

These facts imply that a new generation of bispecific ADCs and immune agonistic ADCs is moving from proof-of-concept to clinical trials, opening new therapeutic windows.

4. Three Main Lines of the Next-Generation Platform

After GLP-1 and ADC, the next generation of industrial power centers is taking shape along the following three main lines:

The First Trend: RNA Drugs Penetrating from Rare Diseases to Chronic Conditions.

The iteration speed of small nucleic acid drugs, mRNA vaccines, and therapies is accelerating. Cemdisiran, administered via subcutaneous injection every 12 weeks, has successfully completed Phase III trials in the field of myasthenia gravis, marking the official entry of siRNA therapy into the autoimmune chronic disease market.

The second line: Cell and gene therapy approaches the industrialization turning point.

The global CGT market is estimated at approximately $9.98 billion in 2024 and is projected to reach about $51.37 billion by 2030, with a compound annual growth rate (CAGR) of approximately 31.4%. The gene-modified therapy market is expected to grow from $14.8 billion in 2025 to $32.1 billion by 2030.

The technological roadmap is diversifying, with in vivo gene editing, AAV capsid engineering, and CAR-T solid tumor breakthroughs jointly driving this sector from a laboratory concept to a commercialized asset.

The third line: AI-driven drug discovery enters the platform-based valuation stage.

Within this month, Isomorphic Labs, an Alphabet subsidiary focused on AI-driven drug discovery, announced the completion of its $2.1 billion Series B financing round, equivalent to approximately RMB 14.3 billion, setting a record for the largest single financing round in AI pharmaceuticals. JiTai Technology’s IPO on the Hong Kong stock exchange recorded an oversubscription of over 6,900 times, marking the highest healthcare IPO in Hong Kong so far in 2026.

This marks a shift in the valuation logic of AI drug development on the capital market, moving from "pipeline narrative" to "platform value."

AI is no longer just accelerating the optimization of lead compounds for known targets, but is actively generating new chemical spaces, predicting off-target toxicology, and designing entirely novel delivery systems. As AI evolves from a tool into a platform, this track will no longer be subordinate to the traditional innovative drug valuation system, but will begin to independently construct its own coordinate system.

5. The Logic of Future Competition

In the next five years, the global pharmaceutical competition landscape will be defined by three main threads: the metabolic track determines scale; ADC and next-generation autoimmune therapies determine growth; RNA and gene therapy determine long-term imaginative space.

Figure: Scale Prediction of High-Growth Pharmaceutical Tracks

The "fear of missing out" sentiment among large pharmaceutical companies has been fully unleashed in the M&A wave of the first half of 2026: Bayer acquired a Phase II ophthalmology molecule for $2.45 billion; UCB acquired a TCE platform company established for less than two years for $2.2 billion; and Biogen acquired Apellis for $5.6 billion with a 140% premium.

The logic behind all these transactions is highly consistent: instead of waiting for competitors to achieve results and then catching up, it is better to directly buy out a key biological node in the track at an early stage.

But the other side of this logic is harsh. When every differentiated molecule is precisely valued, and a Phase II ophthalmology molecule can be sold for $24.5 billion, large pharmaceutical companies act out of anxiety while meticulously calculating where every penny goes.

Ultimately, what determines the ranking is still whose drug can successfully complete Phase III clinical trials. Buying into a promising field is not difficult; the challenge lies in whether the chosen field truly delivers results.

04 Reflection on China's Innovative Drugs

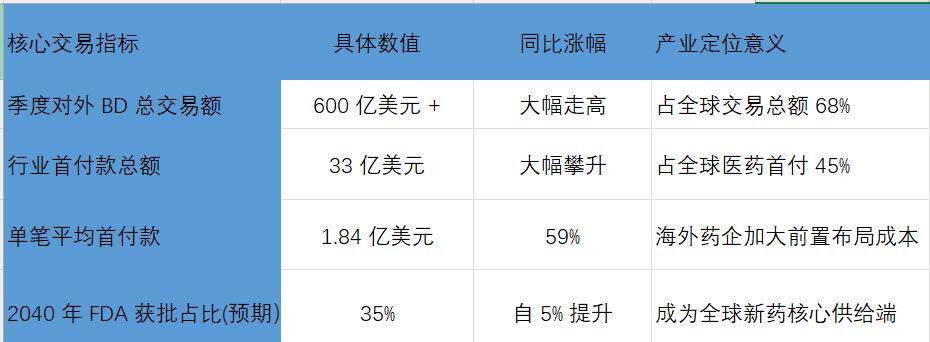

In the first quarter of 2026, the total amount of China's innovative drug outbound BD transactions exceeded 60 billion US dollars, approaching half of the total amount for the whole year of 2025. The upfront payment reached 3.3 billion US dollars, accounting for 45% of the global pharmaceutical transaction upfront payments. The total transaction amount accounted for about 68% of the global total. All these figures set new historical records.

Figure: Core Data of China's Innovative Drug BD Transactions in Q1 2026

This is not an isolated set of numbers; when embedded in the overall framework of the global pharmaceutical ranking reshuffle, three layers of reflection become clearly visible:

The first layer: China is the largest source of incremental supply under the global patent cliff pressure.

Morgan Stanley predicts that by 2040, the proportion of drugs approved by the FDA originating from China will increase from about 5% to 35%, generating approximately $220 billion in revenue in markets outside of China. This forecast itself explains why 68% of the total global BD deal value in the first quarter of 2026 flowed into China.

The Second Layer: China's structural position in the next-generation technology platform determines its bargaining power.

More than 50% of ADC projects in clinical development globally come from China.

In the TCE field, companies such as Zhengda Tianqing, Connaught, and Hengrui are on the same list of key focuses. In the small nucleic acid sector, multiple Chinese companies have already established siRNA and ASO platforms. When Chinese assets are not passively waiting for buyers but are instead being simultaneously sought after for their capabilities across multiple tracks, the balance of power in this game is shifting.

The third layer: The differentiation of the payment structure has faithfully reflected this change.

In the first quarter of 2026, the average upfront payment for China's innovative drug BD transactions reached 1.84 billion US dollars, increasing by approximately 59% compared to 2025 and 187% compared to 2022. The proportion of upfront payments is the most direct reflection of the balance of power between buyers and sellers.

When the proportion of upfront payments nearly doubles over a few years, it indicates that large pharmaceutical companies are willing to pay higher upfront premiums to lock in Chinese assets. This trend suggests that the pricing power of China's innovative drug supply system is on the rise.

05 Conclusion

These figures point to the same thing: the power map of the global pharmaceutical industry is being redrawn.

On this map, the metabolic track has replaced oncology as the largest growth engine. The ADC track is expanding at a rate of about 30% per year, extending from the anti-cancer field to broader therapeutic areas. RNA and gene therapy, on the other hand, are simultaneously opening new entry points in both rare diseases and chronic conditions. The maintenance of industrial power no longer relies on the patent monopoly of a single blockbuster drug but depends on who can secure key positions across multiple tracks while continuously and steadily delivering results that stand up to scrutiny.

China's role is transforming from a supply point on this map into a powerful variable capable of reshaping the entire landscape. And when this variable begins to participate in rule-making itself, the boundaries and direction of this map will no longer be dictated solely by others.

And we are standing at the prelude to this shift in power. The prelude is characterized by a few who have seen the direction of the tide, while the majority are still seeking their place on an outdated map. The real reshuffle is yet to come.

This article comes from the WeChat Official Account"MediShine", Author: Yao Shu, published with the authorization of 36Kr.