Madrigal Pharmaceuticals Submits IPO Prospectus Following FDA Approval of First-Ever NASH Drug Rezdiffra

Madrigal Pharmaceuticals

Developer of Fatty Liver Disease Treatment Drugs

In the early hours of March 15, 2024, the U.S. Food and Drug Administration (FDA) granted accelerated approval to Rezdiffra (resmetirom), in combination with diet and exercise, for the treatment of non-cirrhotic NASH in adult patients with moderate to advanced liver fibrosis (consistent with stage F2 to F3 fibrosis). This marks the first FDA-approved therapy for NASH in 40 years.

NASH, also known as MASH, saw its nomenclature updated by experts at the 2023 European Association for the Study of the Liver (EASL) Congress. According to projections by the Global Liver Institute, MASH will affect the lives of 357 million people worldwide by 2030. Data from Frost & Sullivan indicates that the global market size for MASH therapeutics is expected to reach $10.7 billion in 2025 and grow to $32.2 billion by 2030.

The market is sufficiently attractive, so competition is naturally fierce. For decades, giants including Pfizer, Novartis, and Gilead have stumbled in their R&D efforts for MASH drugs. However, as the first MASH drug to cross the finish line, Resmetirom’s commercial prospects remain fraught with uncertainty.

As Resmetirom is Madrigal Pharmaceuticals’ first marketed drug and targets MASH, a highly promising therapeutic area, its commercialization strategy has naturally become a focal point of attention.

As a biotech company, Madrigal Pharmaceuticals forgoes partnerships with multinational corporations (MNCs) and initiates commercialization preparations after its drug enters the FDA’s Priority Review pathway.

Since mid-2023, Madrigal has been making adjustments to its executive team. First, Bill Sibold was appointed as the new CEO and a member of the board of directors, replacing Dr. Paul Friedman, who had served as CEO since 2016. Friedman will remain on the board.

Prior to joining Madrigal, Sibold served as Executive Vice President of Sanofi Specialty Care and President of Sanofi North America, leading a large organization of approximately 10,000 employees across five specialty areas—immunology, oncology, rare diseases, rare hematologic disorders, and neurology—and was a key member of Sanofi’s Executive Committee.

In addition, Madrigal recruited Carole Huntsman, another executive from Sanofi, as its Chief Commercial Officer. Previously, Huntsman served as the Head of North America and U.S. Regional Lead at Sanofi Genzyme. Under her leadership, Sanofi Genzyme launched a multiple myeloma drug, and Dupixent became the first biologic approved for the treatment of atopic dermatitis in children.

Notably, Sibold and Huntsman played a pivotal role in driving the sales of the immunologic drug dupilumab (Dupixent) during their tenure at Sanofi. In 2020, Dupixent’s sales rose by 75% year-on-year to reach €3.5 billion, maintaining robust growth thereafter and surpassing €10.7 billion (approximately $11.7 billion) in 2023.

Furthermore, Madrigal announced that Mardi Dier will join the company as Chief Financial Officer. With over 20 years of executive finance leadership experience in biotechnology companies, Dier brings extensive expertise in operational and strategic decision-making, capital raising, financial planning and analysis (FP&A), global supply chain management, investor relations, and business development.

Meanwhile, Madrigal conducted a series of financing rounds to support the remaining clinical stages and the commercialization activities of Resmetirom. Shortly after obtaining outstanding data from the Phase 3 MAESTRO-NASH clinical trial, Madrigal raised $500 million through a public offering of 1.2 million shares of common stock and prepaid warrants for 2 million shares of common stock. Prior to this, Madrigal had also raised $259 million in its Series B financing round.

Despite Madrigal’s advance preparations and the replacement of its Chief Financial Officer, the $759 million in funding ($259 million + $500 million) is far from sufficient to bring a new drug to market. According to a report by Deloitte, the average cost for top global pharmaceutical companies to successfully launch a new drug has increased from $1.188 billion in 2010 to $2.284 billion in 2022.

Thus, despite Resmetirom’s positive clinical outcomes, its commercialization remains an uphill battle, particularly for a clinical-stage biotech company.

McKinsey conducted an analysis showing that, although the number of small biopharmaceutical companies going public for the first time has more than tripled over the past decade, these companies have generally struggled to meet their sales expectations during the later commercialization stages.

Nevertheless, Madrigal’s series of strategic moves appears to be a step in the right direction, aimed at capitalizing on the substantial commercial opportunities in the MASH field. As the first approved MASH therapy, it must overcome the challenges posed by high development costs and educate patients, physicians, and payers about the role of Resmetirom in treating MASH. In this effort, Sanofi’s commercialization experience with Dupixent will play a significant role.

Of course, there is also a view that Madrigal should still partner with a more established pharmaceutical company, as the market has certain doubts about the “financial prospects” of Resmetirom.

Unlike previous high-potential blockbuster drugs that went to market, Resmetirom, despite the recognized prospects of the MASH market, has faced various skepticism as the first to cross the finish line. The company’s stock price peaked after the drug entered the FDA’s Priority Review pathway and has since been on a steady decline.

First, Resmetirom’s first-mover advantage is not substantial, and it faces numerous competitors.

Resmetirom has garnered significant anticipation due to its marked improvement in the key clinical endpoint of liver fibrosis. Data from the Phase 3 MAESTRO-NASH trial of resmetirom, published in The New England Journal of Medicine, showed that in this study involving 966 patients across 14 countries, both the 80 mg and 100 mg doses demonstrated statistically significant differences compared with placebo (P<0.001) across three primary endpoints: resolution of MASH without worsening of liver fibrosis, improvement in liver fibrosis by at least one stage without worsening of NAFLD, and changes in low-density lipoprotein cholesterol levels.

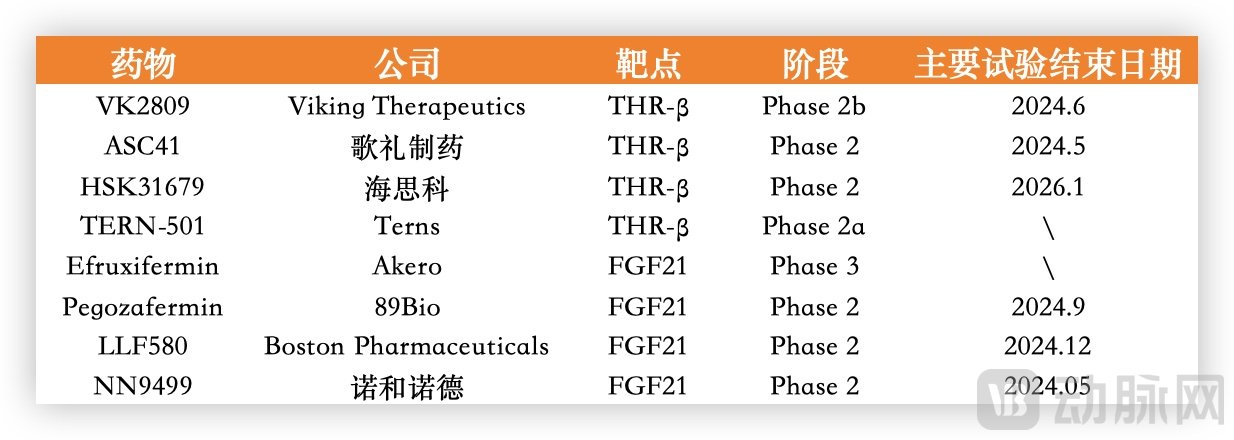

MASH Drugs with Advanced R&D Progress, Data Sourced from Public Information

Resmetirom is a highly selective THR-β agonist. Based on the global clinical pipeline, Resmetirom faces at least 10 competitors targeting the same mechanism. Among these, VK2809 from Viking Therapeutics is one of the most advanced candidates.

Phase 2 clinical study data for VK2809 demonstrated that, compared with the placebo group, patients in the VK2809 (1–10 mg) group experienced a statistically significant reduction in median liver fat content (−37.5% to −55.1% vs. −5.4%), and those in the 2.5–10 mg group also showed a statistically significant reduction in mean liver fat content (−36.8% to −51.7% vs. −3.7%). More importantly, up to 84.9% of patients in the VK2809 group achieved at least a 30% reduction in liver fat content.

Secondly, in terms of efficacy, Resmetirom may not be the optimal choice either.

In early March, Akero Therapeutics announced the latest data from its Phase 2b HARMONY clinical trial evaluating efruxifermin (EFX) for the treatment of MASH. This Phase 2b study assessed the efficacy and safety of the investigational drug EFX in patients with pre-cirrhotic MASH and stage 2 or 3 fibrosis.

EFX is an FGF21 analog designed based on the bioactivity profile of native FGF21. As a member of the fibroblast growth factor family, FGF21 can mediate direct autocrine effects on adipose tissue metabolism, reduce hepatic steatosis and inflammation, reverse fibrosis, increase insulin sensitivity, and improve lipoprotein profiles, thereby treating MASH.

The study had previously met its primary endpoint, whereby at 24 weeks, 39% and 41% of patients in the once-weekly EFX injection groups receiving 28 mg and 50 mg doses, respectively, achieved a ≥1-stage improvement in fibrosis without worsening of MASH, compared with 20% in the placebo group.

The 96-week updated data show that the primary endpoint response rate in the high-dose group increased to 75% (p<0.001), compared with 24% in the placebo group. The study also met its histological endpoint: 36% (p<0.01) of patients in the high-dose group and 31% (p<0.01) in the low-dose group achieved an improvement of at least two stages in liver fibrosis without worsening of MASH, whereas only 3% of patients in the placebo group achieved this outcome.

Furthermore, among patients who showed improvement at Week 24, 92% and 83% of those in the two dose groups, respectively, maintained their improved status when assessed at Week 96, compared with 40% in the placebo group. Clinical results indicate that long-term use of EFX may lead to sustained improvement in fibrosis and broaden the anti-fibrotic treatment response in the treated patient population.

Following the publication of this clinical data, Akero’s stock price surged 36% in premarket trading. In its ongoing Phase 3 SYNCHRONY trial, Akero will continue to evaluate EFX in patients with pre-cirrhotic MASH and MASH-related cirrhosis.

In addition, several drugs targeting PPAR agonists have entered Phase II clinical trials and demonstrated promising potential. Meanwhile, numerous GLP-1 drugs have also achieved excellent results in clinical studies for MASH.

What truly puzzles the market is whether GLP-1 will reshape the landscape of the MASH market.

Semaglutide’s groundbreaking success in weight loss has made GLP-1 a highly sought-after target among pharmaceutical companies. As research has deepened, it has been discovered that binding of GLP-1 to hepatic cell receptors can reduce hepatic steatosis, hepatocyte injury, and glucose output, while also attenuating hepatocellular inflammation and fibrosis in MASH. Consequently, MASH has emerged as the next therapeutic frontier for GLP-1–targeted interventions.

In February, Eli Lilly announced the results of a Phase 2 clinical trial of tirzepatide for MASH during its fourth-quarter 2023 earnings call.

Data show that 73.9% of patients receiving the highest dose of tirzepatide achieved the primary endpoint, defined as resolution of MASH without worsening of liver fibrosis after one year of treatment, compared with 12.6% in the control group. In the low-dose group, tirzepatide enabled 51.8% of patients to reach the primary endpoint.

Notably, all dose groups of tirzepatide treatment achieved clinically meaningful improvements in the secondary endpoint of at least a one-stage improvement in liver fibrosis without worsening of MASH.

Lilly’s data has convinced the market that GLP-1 could disrupt the MASH market.

Following the release of Eli Lilly’s data, shares of multiple companies focused on the MASH sector declined. Madrigal Pharmaceuticals’ stock fell for three consecutive days, dropping by 11.3%, 8.6%, and 9.11% respectively. Akero Therapeutics’ share price also slid by 12.3%, while 89bio’s stock plummeted by 17%.

GLP-1-based MASH Drugs with Advanced R&D Progress; Data Sourced from Public Information

Not only Eli Lilly, but also Boehringer Ingelheim (BI) announced in late February the results of its Phase 2 clinical trial of Survodutide, a dual GCGR/GLP-1R agonist, for the treatment of MASH.

This double-blind, placebo-controlled Phase II trial evaluated three doses of survodutide (2.4 mg, 4.8 mg, and 6.0 mg). The results demonstrated that all doses tested improved MASH, meeting both the primary and secondary endpoints of the trial.

“The results of the MASH studies indicate that survodutide has the potential to become a best-in-class therapeutic agent. We believe its true differentiating factor is the direct glucagon receptor agonist activity in the liver,” said the Head of Boehringer Ingelheim’s Global Human Pharma division. Currently, survodutide has been granted Priority Review designation by both the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) for the treatment of fibrotic MASH.

Furthermore, Novo Nordisk’s semaglutide and Merck & Co.’s efinopegdutide are both actively conducting clinical trials for MASH, with both having yielded positive data.

The Rise of GLP-1 Has Sparked Market Doubts Over Whether the MASH Market Size Can Meet Expectations. In short, obesity and diabetes are considered the primary drivers of MASH, and GLP-1 receptor agonists are currently an effective solution for addressing both conditions. Particularly in the field of weight loss, the sales volume growth of GLP-1 drugs has been phenomenal. Consequently, the market is questioning whether the growth rate of the MASH patient population will slow down as a result.

On the other hand, from a clinical perspective, there is a viewpoint that prioritizing weight loss before treatment holds greater value. For instance, when evaluating the cost-effectiveness of resmetirom, the Institute for Clinical and Economic Review (ICER) noted that although resmetirom offers net health benefits compared to lifestyle modifications alone, it recommends considering GLP-1 receptor agonists for weight reduction first, prior to initiating treatment for MASH.

The entry of GLP-1 drugs has placed immense pressure on companies in this therapeutic area. An extreme viewpoint even suggests that MASH medications may evolve into adjunctive therapies to GLP-1 agents.

In addition to studying efruxifermin (EFX) as a monotherapy for MASH, Akero has conducted research on the combination of EFX with GLP-1 receptor agonists. Clinical data showed that after 12 weeks of treatment, patients with MASH receiving EFX plus semaglutide achieved a 65% reduction in liver fat fraction from baseline, as measured by non-invasive magnetic resonance imaging–proton density fat fraction (MRI-PDFF). In contrast, the control group treated with semaglutide alone exhibited only a 10% reduction in liver fat, and the difference between the two groups was statistically significant.

Although the introduction of GLP-1 agonists may relegate many previous “lead actors” to “supporting roles,” Resmetirom’s first-mover advantage is tangible. If it can leverage this opportunity to scale up volume, it stands to capture a significant market share. In the days leading up to the drug’s approval, the market made its choice, driving up Madrigal’s stock price.

Despite certain uncertainties in the MASH market, the substantial incremental growth potential has prompted numerous Chinese pharmaceutical companies to actively compete for strategic positioning. According to incomplete statistics, there are currently more than 20 drug candidates in China at the clinical development stage, including those from Ascletis Pharma, Chia Tai Tianqing Pharmaceutical, Zhongsheng Pharmaceutical, TopAlliance Biosciences, and CSPC Pharmaceutical Group.

At the beginning of the year, Ribo Life Science and BI entered into a collaboration to jointly develop innovative oligonucleotide therapies for the treatment of MASH. Under the terms of the agreement, in addition to an upfront payment, Ribo Life Science is eligible to receive milestone payments based on the initiation of clinical studies, regulatory approvals, and commercial success, as well as tiered sales royalties on marketed products, with the total transaction value exceeding $2 billion.

Ascletis Pharma’s strategic layout in the MASH field primarily centers on FASN inhibitors and THR-β agonists. In January, Ascletis Pharma announced that its drug ASC41 had achieved positive interim results from its Phase 2 clinical trial. Currently, Ascletis Pharma’s ASC40, ASC41, and ASC42 have all entered Phase 2 clinical development.

ZSP1601, a PDE inhibitor from Allist Pharmaceuticals, has currently entered Phase 2b clinical trials. It is the first Class 1 oral small-molecule innovative drug approved for clinical trials in China for the treatment of MASH. Phase 2a data demonstrated that ZSP1601 significantly improved hepatic biochemical function; patients in the group receiving 100 mg twice daily experienced a 25.5% reduction in liver fat content from baseline, outperforming the 12.8% reduction observed in the placebo group. These findings warrant anticipation for subsequent clinical developments.

Lanifibranor, a PPAR agonist introduced by Sino Biopharmaceutical from Inventiva, is the first oral MASH drug in China to enter Phase III clinical trials. Meanwhile, Sino Biopharmaceutical has adopted a comprehensive strategy in the MASH field, with targets covering FXR, PPAR, FGF-21, GLP-1, and THR-β.

Mazdutide is a weight-loss and glucose-lowering drug jointly developed by Innovent Biologics and Eli Lilly. It is the first GLP-1R/GCGR dual agonist to undergo clinical development with differentiated dosing regimens for populations with varying degrees of obesity. Innovent is also advancing its research in the field of MASH, having already received approval for its clinical trial application. Notably, besides Innovent Biologics, several other companies have established pipelines targeting this mechanism, including Daurio Biosciences’ DR10624, PegBio’s PB-718, United Laboratories’ UBT251, and Tubiao Anchuang’s TB001.

In the field of MASH, as the pathogenic mechanisms have not yet been fully elucidated, a diverse array of therapeutic targets—including FXR, FGF21, GLP-1R, PPAR, ASK1, and THR-β—are currently being explored. However, it remains uncertain which approach will ultimately prevail. As the first drug to cross the finish line, resmetirom is poised to capture a portion of the market share through its first-mover advantage. Nevertheless, with the increasing competitive pressure from subsequent therapies, including GLP-1 receptor agonists, how the MASH market will evolve remains to be seen.