On the Brink of Decoupling: Can China's Innovative Drug Sector Turn Crisis into Opportunity?

WuXi AppTec

New Drug R&D and Production Service Provider

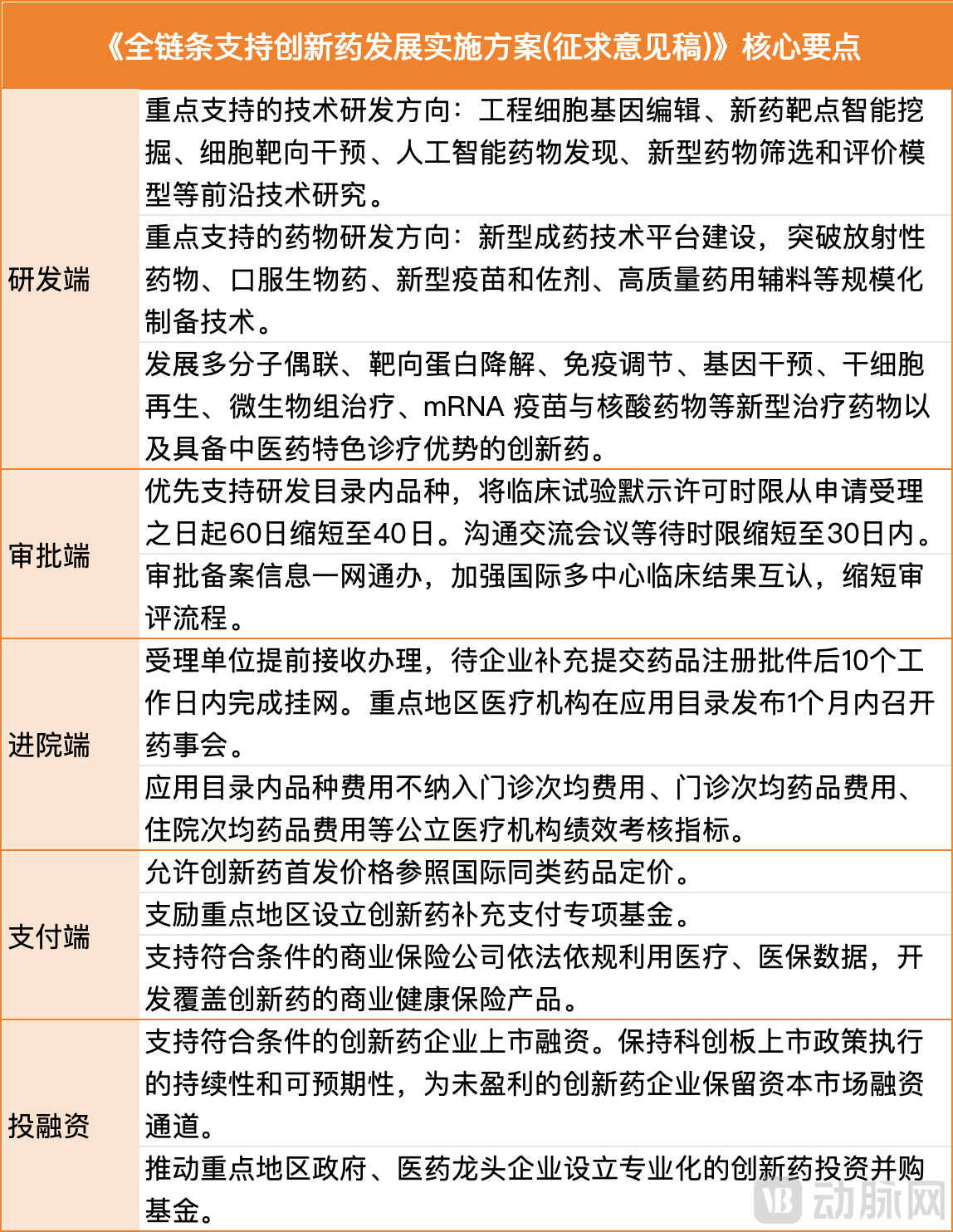

On the evening of March 13, a document circulated among biopharmaceutical professionals on WeChat Moments and group chats. The core of the document lies in providing full-chain support for the development of innovative drugs, leveraging policy guidance and support to comprehensively promote key stages including R&D, approval, utilization, and reimbursement of innovative drugs.

On the same day, BIO, one of the world’s largest and most influential biotechnology innovation industry organizations, announced that it would revoke WuXi AppTec’s membership and terminate its collaboration with the company to demonstrate support for the U.S. Biosecure Act. BIO stated, “Our adversaries abroad have indicated their intention to become the world’s preeminent hub for biotechnology… The United States and our allies cannot allow this to happen. Securing and advancing our leadership in biomanufacturing will be a critical, multi-pronged component of ensuring and advancing biotechnology as a strategic imperative.”

Due to the unique nature of their products, biopharmaceuticals have long been considered an industry less susceptible to “China-U.S. decoupling,” yet they have now become a bargaining chip in strategic competition.

It is imperative to promote the high-quality development of China’s pharmaceutical industry and enhance its international competitiveness from a national strategic perspective. Although this document providing full-chain support for innovative drugs has been issued, its implementation details and the concrete rollout of specific policies remain to be observed.However, it underscores China’s strategic positioning of the innovative drug industry: Amidst a shifting global landscape and intensifying international competition, the research and development of innovative drugs and the growth of this sector are not only vital to public health and societal well-being but should also serve as a key instrument for China to counter overseas suppression and containment.

Funding plays a pivotal role in the development of innovative drugs, which is why the document has sparked widespread discussion.The disclosed details reveal that, on the financing and investment front, support will be provided for eligible innovative drug companies to list and raise capital, maintaining access to capital market financing for pre-profit innovative drug enterprises, and continuing to back qualified firms through initial public offerings (IPOs), follow-on financings, and mergers and acquisitions. On the payment side, fiscal funds will be leveraged to guide and drive the development of innovative drugs, while improving pricing mechanisms and health insurance reimbursement access for these drugs; key regions are also encouraged to establish special supplementary payment funds for innovative drugs.

It’s Time for the Capital Required by Innovative Drugs to Make a Comeback.

IPOs, Long-Term Capital, and State-Owned Assets: Opening the Floodgates for Innovative Drug Financing

Over the past year, the surge in business development (BD) transactions in the biopharmaceutical market has, from another perspective, reflected tightening and scarcity on the financing end, compelling innovative drug companies to seek new sources of capital to sustain their operations. Some investment firms have even ceased sourcing new projects, focusing instead on finding ways to “offload” their existing portfolio companies. At certain industry conferences, one of the objectives for investors’ attendance is to help portfolio projects identify potential transaction counterparties.

However, the cash inflow from business development (BD) is quite limited, and licensing of core pipelines also affects valuation and subsequent development. Innovative pharmaceutical companies need strong investment and financing support to grow. The capital market plays a significant, and in some cases even decisive, role in the development of the biopharmaceutical industry. Looking at venture capital (VC) funding in the U.S. biopharmaceutical market, although funding in 2023 dropped significantly compared to the peak in 2021, it has stabilized at around $6 billion overall, which is comparable to pre-pandemic levels. This figure reflects only VC funding; the XBI Index, which tracks the secondary market for U.S.-listed biotech companies, has risen by more than 24% over the past six months, and year-to-date refinancing by U.S.-listed biotech firms has exceeded $4 billion.

Behind every billion-dollar molecule lies an investment of several times that amount, and inevitably, the acceptance of bubbles.

Last year, Bi Jingquan, Vice Chairman of the Economic Committee of the National Committee of the Chinese People’s Political Consultative Conference and Executive Vice Chairman of the China Center for International Economic Exchanges, pointed out that China’s biomedical industry remains in a “climbing uphill and overcoming obstacles” phase. He specifically highlighted the severe challenges facing the biomedical sector, including weakened expectations, a sluggish capital market, and difficulties in corporate financing.

Data shows that early-stage venture capital and private equity fundraising in China’s biopharmaceutical sector reached $17.2 billion in 2018–2019, surpassing the United States; this figure declined to $16.2 billion in 2020–2021, while the U.S. increased to $21.2 billion. By 2022–2023 (as of September 26), China’s total dropped to $4.5 billion, an 84% decrease compared with 2018–2019, whereas the U.S. continued to grow. Over the past three years, the market capitalization of the biopharmaceutical sector on China’s stock markets has evaporated by nearly RMB 600 billion.

Unable to secure new investment, many innovative drug companies will shut down within a short period. The innovative drugs and overseas licensing deals launched in recent years are mostly the results of venture capital investments from five years ago. The significant decline in venture capital will inevitably lead to a reduction in innovative drug achievements in the coming years.

According to documents circulating online, financing and exit channels for innovative drugs will be gradually opened up, or rather, upgraded.

Dispelling the Gloom of “Suspension of the Fifth Listing Standard on the STAR Market,” IPOs Are Set to Resume:Support eligible innovative drug companies in raising capital through public listings, maintain the consistency and predictability of the listing policies on the STAR Market, preserve access to capital market financing for pre-profit innovative drug companies, and continue to support eligible innovative drug companies in conducting initial public offerings (IPOs), follow-on financings, and mergers and acquisitions.

Attract more long-term capital to leverage robust financial strength and patient support, enabling biopharmaceutical companies to compete globally:Actively guide government-funded industrial investment funds, such as the Fund for Guiding the Transformation of Scientific and Technological Achievements and the Advanced Manufacturing Industry Investment Fund, as well as venture capital funds established by central state-owned enterprises, to provide precise support to eligible projects. Promote medium- and long-term investors, including pension funds (such as the National Social Security Fund) and enterprise annuities, to explore investments in innovative drugs. Encourage governments in key regions and leading pharmaceutical enterprises to establish specialized investment and M&A funds focused on innovative drugs.

State-owned capital, as the main force in the primary market, has reduced investment in innovative drugs due to risk control constraints; a new assessment mechanism should be established to avoid gaps in innovation.Explore the establishment of management models and performance evaluation mechanisms for state-owned venture capital firms that align with the investment characteristics and development patterns of innovative drugs, promote the issuance of detailed implementation rules for due diligence exemption, and encourage state-owned venture capital firms to invest in new targets, new mechanisms, new structures, and new technologies.

Gold Emerges After the Sand Is Washed Away: Payment Rewards True Innovation

In addition to investment and financing, the payment-side policies for innovative drugs outlined in the document also warrant close examination: drugs included in the reimbursement list are excluded from cost-control performance metrics, thereby allowing for a reasonable expansion in the utilization of innovative drugs; initial pricing permits innovative drugs to reference international prices for comparable products, with preferential medical insurance policies granted to those on the reimbursement list; and a diversified payment system is promoted, with support for commercial health insurance.

In recent years, the medical insurance negotiations have generally adopted a price reduction strategy of more than 50% for drug prices, which objectively has prompted some generic drug companies to achieve domestic substitution of multinational corporations (MNCs). However, faced with significant compression of medical insurance payment prices, some innovative pharmaceutical companies have chosen to avoid the medical insurance market and instead focus on the self-pay market. This phenomenon highlights the dilemma that innovative pharmaceutical companies face in achieving reasonable returns under the current medical insurance payment environment.

Providing appropriate preferential treatment to innovative drugs during negotiations can help innovator pharmaceutical companies achieve financial returns commensurate with their R&D investments, thereby sustaining their innovation momentum. Controlling the reimbursement prices of non-innovative drugs also helps free up medical insurance funds, enabling more patients to benefit from innovative therapies.

Previously, Bi Jingquan also emphasized that the price formation mechanism for innovative drugs is a critical issue bearing on the very survival of China’s biopharmaceutical industry. Both enterprises and investors conduct risk-return assessments when selecting R&D projects or investment targets, with an expected price in mind. Whether this expected price can be realized should be determined by the market.

However, healthcare insurance experts have pointed out: “The key to whether innovative drugs can be included in the national medical insurance scheme lies in whether they truly meet urgent clinical needs and demonstrate clear clinical advantages. For new drugs that claim significant efficacy but lack sufficient clinical data support, their marketing hype should be viewed with caution to avoid blind inclusion in the insurance coverage. Even for innovative drugs with proven clinical value, reimbursement pricing must still be based on pharmacoeconomics and health technology assessment; the room for premium pricing is limited and must not contravene the fundamental principles governing the operation of the medical insurance fund.”

At its core, market mechanisms and national policies must be leveraged to deter speculative projects characterized by low-level homogenization in the innovative drug industry. In certain targets or therapeutic areas with ample room for R&D and market expansion, China is not short of first-tier players capable of rapid clinical follow-up with clear strategic thinking. However, those who merely jump on bandwagons and engage in involutionary “trend-chasing” will ultimately be eliminated by a market trend dominated by professionalism and innovation.

For instance, several star GLP-1 products in China are expected to accelerate their market entry through the priority review pathway, with a competitive landscape against multinational corporations (MNCs) beginning to take shape. Meanwhile, companies attempting to capitalize on the GLP-1 target by skirting regulatory or scientific boundaries are also emerging frequently. Similarly, amid the surge in bispecific antibody products and the booming development of antibody-drug conjugates (ADCs), the market has recognized the R&D capabilities of Chinese biotech firms. However, at certain industry conferences, some companies have presented biological mechanisms with obvious flaws, attempting to exploit the situation for their own gain.

When the source of living water is tapped, identifying and protecting innovation become the next key priorities.Which companies are genuinely developing novel targets? Which projects possess clear clinical value? How can the industry truly achieve, as stated in the document, more than 10 First-in-Class drug approvals and over 10 innovative drugs registered and launched overseas by 2027?

Innovative drugs bear no original sin; may the sands of time wash away the dross to reveal the gold, and may the spring light of biomedicine shine upon the land.