Domestic Autoimmune Drugs Face Fierce Competition as Market Enters Era of 'Hundred-Drug Battle'

The autoimmune disease drug market has once again become fraught with uncertainty.

Since Humira’s global sales reached an inflection point and Keytruda replaced it to claim the title of “blockbuster drug king,” developers of autoimmune therapies have found new momentum. Establishing a new order in a non-consensus market will undoubtedly generate substantial commercial value.

It is evident that the global market for autoimmune disease therapeutics is becoming increasingly crowded. Established leaders in the field have not exited the stage, while new multinational pharmaceutical companies are entering the fray with substantial financial resources. In June 2023, Novartis acquired Chinook Therapeutics, a leading company in IgA nephropathy treatments, for $3.5 billion, and Eli Lilly acquired DICE Therapeutics for $2.4 billion, gaining access to its portfolio of autoimmune therapies, including an oral IL-17 inhibitor.

In China, the development of novel drugs for autoimmune diseases has not been as prominent a field as that for oncology. However, as an increasing number of new targets are validated, many companies have begun to intensify their investments in autoimmune disease pipelines. Data show that dozens of domestic drug R&D enterprises have established over one hundred autoimmune drug pipelines. Among these, competition remains fierce for Chinese-made biosimilars targeting two well-established autoimmune targets, TNF-α and IL-12/IL-23. Meanwhile, emerging targets such as JAK and IL-17A have attracted extensive engagement from numerous innovative pharmaceutical companies, resulting in the largest number of products currently under development.

No Conflict Among Domestically Produced Autoimmune Drugs

In China, the autoimmune disease drug market has long been fraught with uncertainty. For an extended period during which biologics replaced traditional anti-inflammatory drugs as the mainstream treatment for autoimmune diseases, imported drugs in this sector failed to outperform domestically produced ones.

In 2002, the predecessor of 3SBio, CITIC Guojian, was established. Three years later, 3SBio launched its blockbuster product, Etanercept (Yisaipu), a TNF-α inhibitor for the treatment of rheumatoid arthritis. Two years thereafter, indications for ankylosing spondylitis and psoriasis were added.

Subsequently, this drug dominated the domestic autoimmune disease medication market for nearly 15 years. According to the prospectus of 3SBio Inc., from 2018 to 2020, sales revenue from Etanercept (Yisaipu) was the primary source of the company’s revenue, accounting for more than 99%. In September 2017, Etanercept was included in the National Reimbursement Drug List, which further boosted its sales. Financial reports show that in 2018, sales of Etanercept reached RMB 1.11 billion, a year-on-year increase of 9.7%, capturing a 64% share of the domestic TNF-α inhibitor market.

Throughout this period, Enbrel, the originator product of etanercept, and Humira, the blockbuster TNF-α drug that achieved tremendous sales overseas, were consistently outperformed by Yisaipu in the Chinese market. Enbrel and Humira were launched in China in 2010. Stripped of their first-mover advantage as original star drugs and burdened by medication costs at least twice as high, their domestic sales remained sluggish. In 2018, Humira’s sales in sample hospitals barely approached RMB 20 million, merely one-twentieth of Yisaipu’s sales volume during the same period.

Early Domestic Sales of Autoimmune Biologics Data Source: VCBeat, compiled based on public information

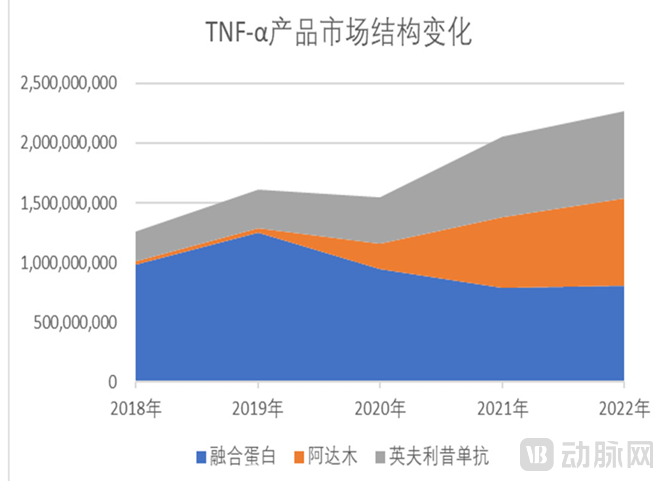

However, market dominance built on external factors is easily shaken. The turning point came in 2019. In that year, Humira and Remicade were included in the National Reimbursement Drug List (NRDL), while Bio-Thera Solutions’ Glalix and Hisun Pharmaceutical’s Anjianning received marketing approval. That year, the annual treatment costs for Humira, Glalix, and Anjianning dropped to RMB 33,500, RMB 30,100, and RMB 29,900, respectively, far lower than Enbrel’s price of RMB 66,900 at the time. In 2020, Humira’s sales in sample hospitals reached RMB 70.08 million, representing a year-on-year increase of 270.76%. In 2022, Enbrel held a 27% market share among TNF-α inhibitors, a slight decline from the previous year.

Changes in the Domestic TNF-α Drug Market from 2018 to 2022 Data Source: 3SBio Financial Report

In fact, another reason behind Etanercept’s market dominance is that the overall size of China’s autoimmune disease drug market has yet to gain significant momentum. According to Frost & Sullivan statistics, despite a consistent upward trend, the size of China’s autoimmune disease drug market had not surpassed $5 billion by 2022, whereas the global autoimmune disease drug market during the same period approached $150 billion. In contrast, in 2022, the global oncology drug market was valued at approximately $150 billion, while China’s oncology drug market had already reached $35.4 billion.

Certainly, autoimmune drugs possess their own unique characteristics. The large patient population for autoimmune diseases, combined with long treatment durations and the strong potential for indication expansion, makes it highly likely for blockbuster drugs to emerge. In recent years, as research into the mechanisms of autoimmune diseases has deepened, new-target autoimmune therapies have gradually transformed clinical practice and patient habits in China, thereby expanding the market boundaries for autoimmune drugs.

When Etanercept was forced to step down from its pedestal, 3SBio initially attempted to move out of its comfort zone and expand into new disease areas. However, after multiple attempts, the company refocused on novel autoimmune drugs. In its financial report at the end of 2023, 3SBio stated that it would concentrate all its efforts on deepening its presence in the autoimmune field.

VCBeat has noted that since 2023, 3SBio has been progressively reducing its R&D expenditures in other therapeutic areas and even divesting its pipeline assets in those fields. In April 2023, 3SBio granted Shenyang Sunshine Pharmaceutical exclusive rights to develop its oncology candidates 602, 609, 705, and 707, as well as the ophthalmic drug candidate 601A, in mainland China and the United States. Furthermore, 3SBio transferred to Shenyang Sunshine Pharmaceutical all compounds derived from project 304R, along with all global rights associated with their subsequent development into drugs.

Interleukin Intruder

After fully tapping into the potential of TNF-α targeted therapies, the hope for expanding the market size of autoimmune disease drugs now rests on the newcomers entering this industry.

In China, IL-17A is undoubtedly the most prominent novel therapeutic target for autoimmune diseases. In addition to imported drugs already on the market, such as secukinumab and ixekizumab, publicly available information on investigational IL-17A agents reveals three tiers based on their development progress, namely secukinumab andFunakizumabThe NDA drug pipeline, represented by products developed by domestic innovative pharmaceutical companies, includes candidates such as QX002N and gumokimab that have entered Phase III clinical trials, as well as a large number of pipelines still in the early to mid-stages of research and development.

Currently, there are five IL-17A/IL-17RA targeted drugs marketed globally: secukinumab, ixekizumab, netakimab, bimekizumab, and brodalumab. Among these, secukinumab, ixekizumab, and brodalumab have been approved in China, while bimekizumab has also filed for marketing approval in the country. As novel agents for autoimmune diseases, IL-17A/IL-17RA inhibitors have significantly reduced treatment costs for patients with autoimmune conditions, although the expenses remain considerable. For instance, Novartis’s secukinumab was initially priced at RMB 2,998 per pen, resulting in an annual treatment cost of RMB 40,400. In contrast, Eli Lilly’s ixekizumab was priced at RMB 4,318 per pen, with an annual treatment cost of RMB 25,900. Of course, treatment prices dropped substantially after inclusion in the National Reimbursement Drug List (NRDL), but that is a separate matter.

Secukinumab and funalikizumab, belonging to the first tier of domestically produced drugs in China, were developed by Zhixiang Jintai and Hengrui Medicine, respectively. In March and April 2023, secukinumab and funalikizumab successively applied for market approval in China, becoming the strongest competitors to replace imported IL-17A/IL-17RA inhibitors. Currently, both secukinumab and funalikizumab have demonstrated excellent safety and efficacy in large-scale clinical studies.

Several months ago, Hengrui announced the results of a study evaluating funakizumab in patients with moderate-to-severe plaque psoriasis. The multicenter, double-blind Phase 2 trial (NCT03463187) yielded positive outcomes. Data showed that at Week 12, all funakizumab groups demonstrated improvement in PASI 75 response rates compared to the placebo group. The PASI 75 response rates were 56.8%, 65.8%, 81.6%, and 86.5% for the 40 mg, 80 mg, 160 mg, and 240 mg groups, respectively, versus 5.4% in the placebo group. Additionally, a higher proportion of patients achieved an Investigator’s Global Assessment (IGA) score of 0 or 1 with funakizumab treatment. The respective rates were 45.9%, 47.4%, 60.5%, and 73.0% for the 40 mg, 80 mg, 160 mg, and 240 mg groups, compared to 8.1% in the placebo group. No unexpected adverse reactions were observed.

Earlier this month, Zhixiang Jintai also announced the latest research data for selicrelumab. The data showed that at Week 12, 90.7% of subjects in the 200 mg selicrelumab group achieved PASI 75 (compared with 8.6% in the placebo control group), and 74.4% achieved skin clearance or almost clear (PGA 0/1) (compared with 3.6% in the placebo control group), thereby meeting the primary clinical endpoint. Meanwhile, the PASI 90 response rate was 74.4%. At Week 52, the PASI 75 response rate was 96.5%, the PASI 90 response rate was 84.1%, and the PGA 0/1 response rate was 83.7%, demonstrating sustained high-level skin lesion improvement and durable treatment response.

Zhixiang Jintai’s aggressive entry has introduced significant uncertainty into the race for leadership in China’s domestic autoimmune disease sector.

In contrast, the second tier of domestic IL-17A/IL-17RA drug developers is quite substantial, comprising not only 3SBio, a leading player in China’s autoimmune disease sector, but also prominent oncology innovators that have crossed over into this space, such as Junshi Biosciences and Akeso.

Progress in the Development of Major Domestically Produced IL-17A Drugs Data Source: Compiled by VCBeat based on public information

At least seven companies are crowded into Phase III clinical trials for IL-17A inhibitors, with highly overlapping indication selections, making the competition to break through the deadlock exceptionally fierce. More importantly, the innovative pharmaceutical companies currently at the forefront of R&D possess unquestionable and comparable capabilities in medical clinical development and commercial distribution channels.

As the former dominant player in China’s domestic biologic market for autoimmune diseases, it is regrettable that 3SBio failed to secure a position among the top tier of IL-17A drug developers. However, its deep understanding of the characteristics of autoimmune disease treatment in China and its brand recognition, built upon Enbrel (Etanercept), will undoubtedly enhance its competitive edge. Meanwhile, Junshi Biosciences and Akeso, as pioneers in the field of novel oncology drugs, along with Quansheng Bio’s founding team—who are no strangers to new drug development—can leverage their extensive experience from drug R&D to commercialization. Applying this expertise to the development of IL-17A inhibitors can help reduce uncertainties in the process.

In a sense, the race to market for IL-17A/IL-17RA-targeting drugs may well represent the first true head-to-head showdown of development capabilities among China’s innovative pharmaceutical companies.

JAK Inhibitors: Overtaking on the Bend?

When JAK inhibitors are mentioned, the immediate association for many is their use as novel oncology drugs. However, based on the number of projects in development, JAK ranks as the second most popular target among pharmaceutical companies, trailing only TNF-α, and has even surpassed IL-17A in terms of interest.

The JAK-STAT signaling pathway consists of tyrosine kinase-associated receptors, Janus kinases (JAKs), and signal transducers and activators of transcription (STATs). Activated by cytokine-stimulated signal transduction, it participates in many critical biological processes, including cell proliferation, differentiation, apoptosis, and immune regulation, making it one of the important signaling pathways in the human body.

As members of the cytoplasmic tyrosine kinase family, Janus kinases (JAKs) comprise four isoforms: JAK1, JAK2, JAK3, and TYK2, with overlapping binding partners among these isoforms. Among them, JAK1 and JAK3 are primarily involved in immune regulation, whereas JAK2 is mainly associated with erythropoiesis and thrombopoiesis.

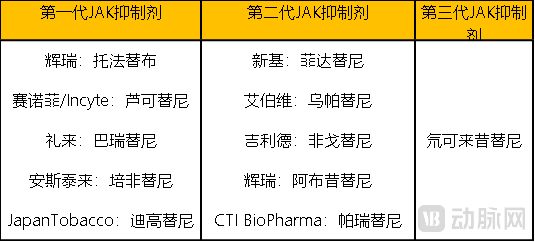

The JAK-STAT signaling pathway is implicated in the pathogenesis of various autoimmune diseases, including rheumatoid arthritis, psoriasis, and inflammatory bowel disease. Since the discovery of the world’s first JAK inhibitor in the 1990s, 11 original JAK inhibitors have been approved for market launch globally.

JAK Inhibitors of Different Generations Data Source: Compiled by VCBeat based on public information

Differences Between Generations of JAK Inhibitors Are Primarily Reflected in the Selectivity for Intracellular Signaling Pathways. First-generation JAK inhibitors are non-selective, simultaneously blocking multiple related signaling pathways and lacking selectivity. Second-generation JAK inhibitors reduce the severe adverse reactions associated with the first generation by selectively inhibiting members of the JAK family. Third-generation JAK inhibitors can highly selectively bind to corresponding domains on cells, specifically inhibiting cellular activity.

In 2017, the first JAK inhibitor entered the Chinese market, rapidly gaining clinical recognition and driving a swift expansion in its market size. Data shows that in 2022, the domestic market for JAK inhibitors reached RMB 943 million, representing a year-on-year increase of 222.95%. According to Frost & Sullivan projections, sales of JAK inhibitors in China will continue to grow steadily, with the market size expected to reach RMB 10 billion by 2024 and RMB 48.1 billion by 2030. The compound annual growth rate (CAGR) from 2019 to 2024 is projected to be as high as 92.2%.

However, overall, the development of autoimmune indications for domestically produced JAK inhibitors has lagged slightly behind that of IL-17A inhibitors. VCBeat’s research reveals that there are currently 60 JAK inhibitor variants and 313 acceptance numbers involved in registration applications in China. Among the top 10 companies in China by number of JAK inhibitor R&D projects, Hengrui Medicine, Linkcare Pharma, and Zeltis Biosciences are leading in development progress.

SHR0302, a highly selective JAK1 inhibitor developed by Hengrui Medicine, has been approved in China to conduct clinical trials for various autoimmune diseases, including rheumatoid arthritis, vitiligo, and ulcerative colitis. Among these, the development of SHR0302 for indications such as alopecia areata, atopic dermatitis, ulcerative colitis, rheumatoid arthritis, and ankylosing spondylitis is progressing most rapidly, with all having entered Phase III clinical trials. Jakotinib Hydrochloride, developed by Zelixir Pharmaceuticals, is also undergoing Phase III clinical trials for autoimmune disease indications, including intermediate- and high-risk myelofibrosis, severe alopecia areata, and moderate-to-severe atopic dermatitis.

In addition, most domestically produced JAK inhibitors for autoimmune diseases are still in Phase II clinical trials or earlier stages of development. Among them, LNK01003, developed by LinkHealth Therapeutics, is a gut-restricted agent intended for the treatment of ulcerative colitis and other conditions, attracting significant industry attention. Currently, this drug is undergoing Phase II clinical trials.

In contrast to the fierce head-to-head competition among IL-17A inhibitors, the rivalry among domestically produced JAK inhibitors for autoimmune diseases is relatively mild. However, in the JAK inhibitor market characterized by lower pricing, it remains unclear whether Chinese-made drugs, having lost their first-mover advantage, can establish a foothold against imported originator products, or even leverage stronger localization capabilities to achieve overtaking on the bend.

Autoimmune diseases represent the second-largest clinical pharmaceutical market, both globally and in China. However, the corresponding product supply side remains underdeveloped. In China, the gaps in the autoimmune drug portfolio are even more pronounced. As the market for autoimmune drugs expands, we are witnessing an increasing number of domestic pharmaceutical companies entering and investing heavily in this sector, which is not yet a hotbed of competition. It remains to be seen who will emerge as the ultimate winner.