Expansion Amid Closures: When Will the Chain Healthcare 'Territory War' End?

Setting aside technological innovations and the volatile shifts in the primary and secondary markets for a moment, let us turn our attention to the grassroots level. What else can we observe in the healthcare sector? One prominent phenomenon is, of course, the pharmacies that saturate streets and alleys; it is reported that in many first-tier cities,A street less than 100 meters long often has five to seven pharmacies., this has become standard.

Meanwhile, on the other front, the “exchange and replacement” process within medical chain institutions is also proceeding in tandem. According to industry insiders, “InIn high-traffic areas, select prime-location stores are frequently undergoing renovation and rebranding. A site might initially operate as a medical aesthetics clinic, transition to a rehabilitation center six months later, and subsequently become a dental clinic, an ophthalmology practice, a psychological counseling center, or other types of healthcare facilities.。”

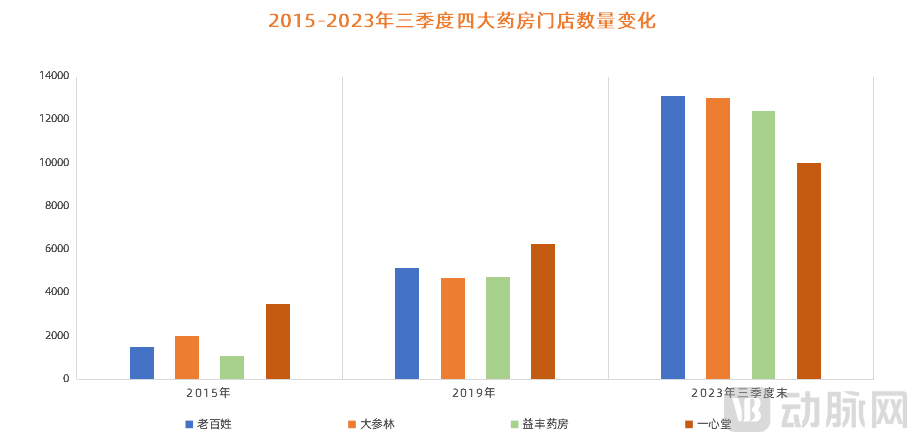

Behind these two typical phenomena lies the current “survival reality” of chain medical institutions:On one side, there is aggressive expansion to seize market share; on the other, contraction and transformation driven by economic growth pressures.Taking chain pharmacies as an example, annual report data shows that in the first three quarters of 2023, the “Big Four” pharmacy chains—Yifeng Pharmacy, Laobaixing, Dashenlin, and Yixintang—added a total of 8,114 new stores. Meanwhile, the number of store closures among chain pharmacies also hit a record high that year, with nearly 1,000 stores closed throughout the year.

In fact, this is not an isolated case; inMedical Aesthetics, Dentistry, Ophthalmology, Traditional Chinese Medicine (TCM), Rehabilitation, Health CheckupsIn the chain-based medical services sector, waves of expansion and closures are unfolding simultaneously. Is this the new normal for the industry’s development, or is the sector at a critical juncture where winners and losers will soon be determined? This question warrants in-depth investigation.

Racing to Claim Territory, Vying for the Top Spot

Over the past year or two, even amid a market downturn, the expansion of chain medical institutions has continued to intensify.

Taking pharmacies as an example, although China has entered the “era of ten thousand stores” with a chain store rate approaching 60%, the industry has not slowed down and remains in a critical phase of aggressive market expansion. For instance, Laobaixing Pharmacy plans to open 3,500 new stores in 2024; Yifeng Pharmacy has stated that it will open 3,900 stores over the next three years, excluding franchise locations; and while Jianzhijia has not disclosed its specific store expansion plan for 2024, based on its performance over the past three years, the number of new stores added in 2024 is expected to be no less than 1,000.

Figure 1. Changes in the Number of Stores of the Four Major Pharmacy Chains from 2015 to Q3 2023 (Data Source: Annual Reports)

Figure 1. Changes in the Number of Stores of the Four Major Pharmacy Chains from 2015 to Q3 2023 (Data Source: Annual Reports)

The same holds true for traditional Chinese medicine (TCM) clinics, which have attracted significant attention in recent years. According to the 2022 National Health and Health Statistical Bulletin released by the National Health Commission, there were 54,000 TCM clinics across China as of the end of 2022, an increase of 12,000 from 2019, representing a growth rate of 28.6%. Rongshujia is a typical representative; as of June 30, 2023, it announced on its official platform that it had established 1,200 Rongshujia TCM clinics nationwide, with additional locations still under development.

Of course, dental clinics are also “springing up everywhere.” According to data compiled by the Yiya DSO team over a period of more than two months, the total number of dental medical institutions in China exceeded 120,000 by the end of 2022, representing an increase of 30,671 from 2021. Chain dental clinics such as Weile Dental, Taikang Bybo Dental, Meiao Dental, and Huanle Dental have all entered the “era of 100+ clinics.”

So, what exactly is driving the aggressive expansion of chain medical institutions?

This needs to be examined from two perspectives,First and foremost, policy-driven initiatives have been key, primarily due to the substantial dividends released by the out-of-hospital market and the accelerated coverage of primary healthcare.. Taking pharmacies as an example, the advancement of comprehensive supporting reforms for the “separation of prescribing and dispensing” in recent years has led to an increasing outflow of prescription drugs from hospitals, which has, to some extent, driven the development of retail pharmacies. In terms of primary healthcare, ten government ministries and commissions jointly issued a document in April 2022, mandating that traditional Chinese medicine (TCM) clinics at the primary care level achieve 100% coverage by 2025. This implies that tens of thousands of TCM clinics will rapidly emerge over the next three years.

Beyond policy, the race for industry leadership has now entered its final sprint.. As is well known, scalability is the core of chain operations; only by ranking among the industry leaders can one secure a share of the “cake” amidst fierce market competition. Therefore, opening new clinics will remain an enduring theme for chain medical institutions. In this regard, a professional investor remarked, “In certain segments of the chain medical care sector, market competition is relatively open at this stage. Consequently, industry players are eager to gain a first-mover advantage and emerge as the ultimate winners once the dust settles, as no one wishes to be the ‘small fish’ that gets swallowed up in the end.。”

To run faster, in terms of expansion strategy,Chain medical institutions prioritize mergers and acquisitions, as this approach offers higher store-opening efficiency compared to building new locations from scratch or franchising.. Taking Aier Eye Hospital as an example, it acquired 30 ophthalmic medical institutions in a single transaction for RMB 1.871 billion in 2020, and in September 2023, it acquired another 19 medical institutions in one go for RMB 860 million. The same trend is seen among chain pharmacies; according to annual report data, the four major pharmacy chains spent nearly RMB 2 billion on mergers and acquisitions during the first three quarters of 2023.

However, high-quality acquisition targets remain a scarce resource. In the race to secure them, chain medical institutions have always been willing to spend lavishly, making capital-intensive expansion inevitable. This is understandable, as premium targets not only enhance brand influence but also ensure economic returns, given their broader service radius and ability to reach a larger patient base.

Expansion, currently only hype

Although the ultimate goal of expansion is to capture market share, this cannot be simply equated; for chain medical institutions, the risks behind expansion also exist.

In fact,Many chain medical institutions are currently mired in the quagmire of expansion.. For instance, in the pharmacy sector, annual report data indicate that while revenue scales achieved slight growth following expansion, gross profit margins generally declined. Taking Laobaixing Pharmacy as an example, the gross profit margin for Chinese and Western proprietary medicines decreased by 0.12 percentage points year-on-year in the first three quarters of 2023, while that for traditional Chinese medicine products dropped by 1.21 percentage points compared to the same period last year.

This is not an isolated case; other chain healthcare sectors are currently facing similar challenges. Taking a leading chain institution as an example, although its expansion efforts have continuously intensified over the past one to two years, the growth rates of its overall revenue and net profit have been rapidly narrowing. The underlying “trigger” for this trend is the high administrative and marketing expenses incurred following expansion. According to financial reports, in 2022, its administrative expenses and marketing expenses were RMB 2.293 billion and RMB 1.556 billion, respectively, representing a several-fold increase from RMB 380 million and RMB 270 million in 2014.

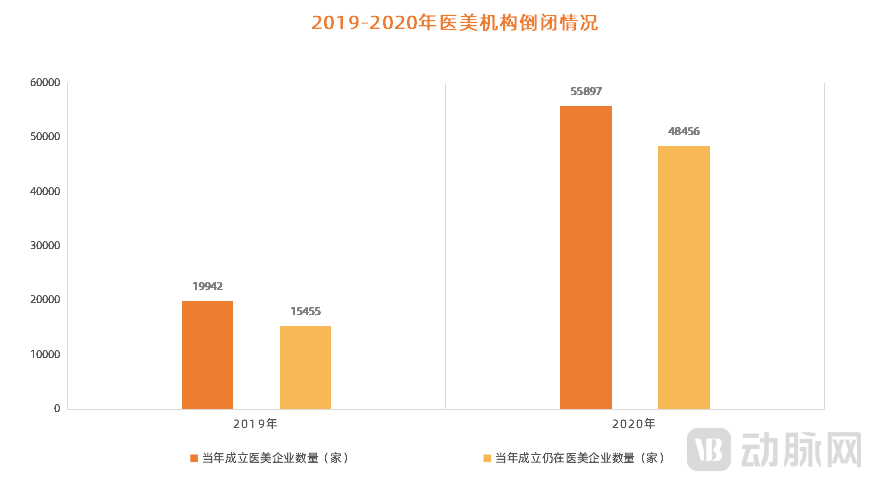

Thus, it is not difficult to see that in recent years,The frenzied expansion of chain medical institutions has failed to deliver the desired incremental performance; instead, it has pushed them into an abyss., namely, a large number of stores have closed down one after another. Taking the medical aesthetics sector, a “hard-hit area,” as an example, according to the “Meituan Research Institute: 2020 Report on the Development of China’s Life Beauty Service Industry,” the average store closure rate in the medical aesthetics industry was 20% in 2020, and by 2022, this figure had climbed to 31%.

Figure 2. Closures of Medical Aesthetic Institutions in 2019–2020 (Data Source: iiMedia Research)

Figure 2. Closures of Medical Aesthetic Institutions in 2019–2020 (Data Source: iiMedia Research)

So, what exactly is holding back expansion?

First, from a personal perspective,As store scale expands, overall operating costs rise significantly; in the absence of substantial revenue growth, this inevitably leads to a continuous decline in daily “labor productivity” and “sales per square foot.”On the other hand, standardization poses a significant challenge. As the number of outlets surges, maintaining standardized operations across these locations becomes increasingly difficult. For most chain medical institutions, systematic operational mechanisms have not yet been established, and their overall maturity remains insufficient. Consequently, medical disputes occur from time to time, inflicting substantial negative impacts on their brands.

Secondly, from a market perspective,Following a period of aggressive expansion, the market gradually approaches saturation, forcing most chain organizations to bear the cost of “ultra-low pricing” for survival.In the case of chain pharmacies, China currently has more than 640,000 pharmacies in total. Based on a population of 1.4 billion, the average number of people served per pharmacy is less than 2,200, which represents a gap of over 4,000 compared to the U.S. average of 6,250 people per pharmacy. Against this backdrop of oversupply, price competition among chain medical retail outlets has become inevitable, leading directly to a sharp decline in gross profit margins.

Finally, there is the massive impact of e-commerce on the expansion of physical medical stores.. In recent years, as e-commerce has extensively penetrated the chain healthcare sector, it has not only opened up certain revenue growth opportunities but also indirectly intensified market competition. This is reflected in the direct pressure exerted on brick-and-mortar stores. In this regard, industry experts note, “Compared with offline channels, online platforms may better meet the healthcare needs of the vast majority of users today. For instance, prices are generally slightly lower than those in physical stores, and users can easily compare offerings across different vendors. Most importantly, they can avoid the awkwardness of being subjected to sales pitches from store staff.”

Meanwhile, as online channels capture a segment of the customer base, the proliferation of substandard products on these platforms is also exerting significant negative effects on the entire industry. Taking hearing aids as an example, the founder of one company stated, “On certain e-commerce platforms, hearing aids can be purchased for just over 100 yuan, with remarkably high sales volumes. It is not that they should not be affordable; rather, such products are often ‘unlicensed’—lacking manufacturer names, production addresses, and quality certificates. Not only do they offer limited efficacy, but in severe cases, they may even cause secondary harm to users.”

Therefore,The pressures encountered during expansion may outweigh the returns yielded thereafter; to withstand such strain, ample “ammunition” from the rear is essential, and the capital chain must remain intact without any lapse.. So, against the backdrop of the current market winter and tight funding, where will chain medical institutions obtain their “ammunition”?

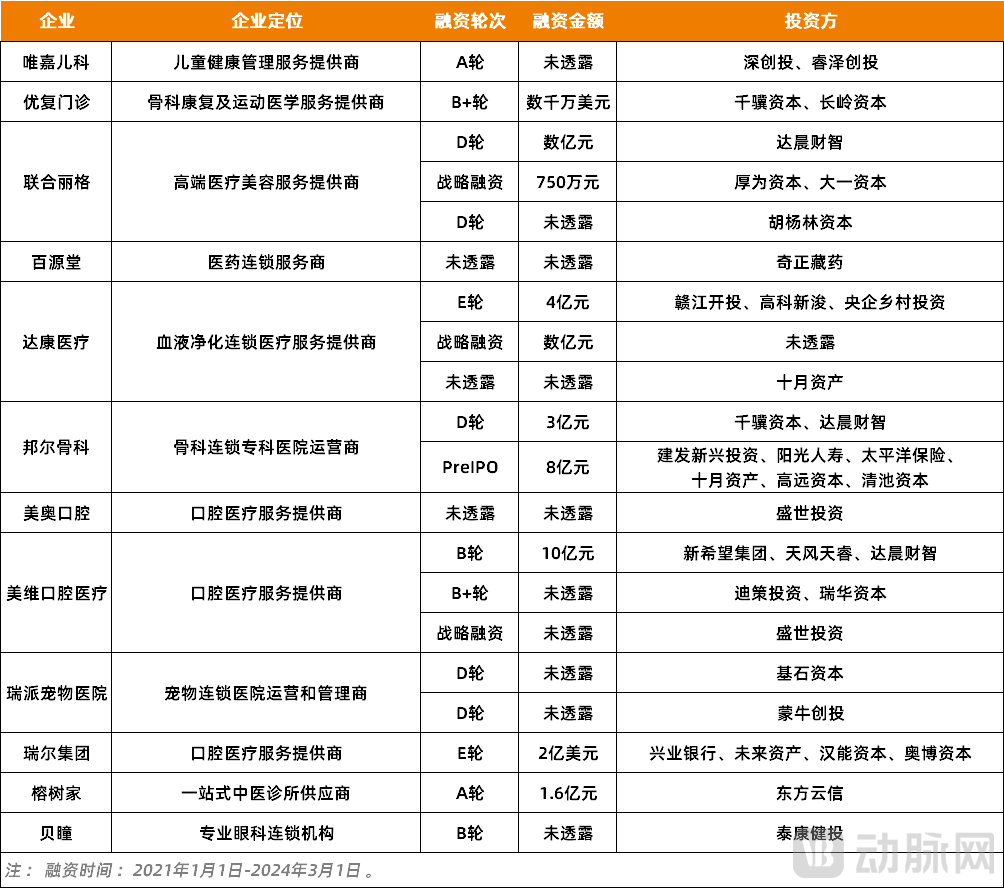

HeadFirst and foremost, it relies on internal resources, namely the cash flow generated through business operations.;Second is financing from the primary market, according to incomplete statistics from the VCBeat database, a total of 17 chain medical institutions in China completed financing over the past two years, with as many as 40 financing events;Finally, it relies on fundraising., according to an investor, “an increasing amount of state-owned capital is now getting involved; for instance, Sinopharm Group, China Resources, and Shanghai Pharmaceuticals are all actively expanding their investments in the chain medical market.”

Figure 3. Selected Financing Cases of Chain Medical Institutions from 2021 to March 2024 (Data Source: VCBeat Orange)

Among these three methods of replenishing “capital ammunition,” fundraising is the more common and mature approach. It is reported that in the past few years, each of the four major pharmacy chains has raised over RMB 5 billion from the market. Notably, Laobaixing Pharmacy has raised a total of RMB 8.64 billion since its IPO in 2015. Aier Eye Hospital followed a similar path; in October 2022, it completed its largest fundraising round since going public, raising RMB 3.536 billion, which will be primarily used for market expansion.

However, it is still difficult to determine the ultimate conversion rate of these funds.However, at the current stage, the aggressive expansion of chain medical institutions is, in most cases, a case of “losing money to gain visibility.”。

To Keep Racing or Wait for the Storm to Pass: How to Decide?

For the vast majority of chain institutions, expansion at this juncture is essentially inevitable. After all, driven by both policy and industry forces, the market space for chain healthcare is gradually expanding, although competition is intensifying as a result, andExpansion is indeed a key strategy for maintaining competitiveness.。

However, expansion is itself a discipline: moving too quickly can lead to instability, while moving too slowly may cause missed opportunities for growth. So, how should one make the right choice? By analyzing real-world cases and synthesizing interviews with industry experts, VCBeat has distilled a set of methodological insights.

First and foremost, a clear expansion strategy is essential., including how many new stores to add each year and which regions to prioritize. For instance, regarding expansion regions, many chain medical institutions have highlighted in their expansion strategies over the past one to two years the need to “focus on provinces where they hold a competitive advantage and accelerate their presence in lower-tier markets.” The underlying logic is straightforward: “provinces with competitive advantages” form the foundation of performance and must be stabilized, while “lower-tier markets” represent the second growth curve.

The second point is to leverage digital technologies to empower expansion., including the enhancement of overall medical services and the rapid establishment of store standardization. Taking standardization as an example, digital technologies can quickly consolidate experience and replicate it in newly opened stores. In subsequent operations, digitalization will continue to support these new stores, including service improvement and customer acquisition. In this regard, a head of a chain medical institution stated, “The purpose of expansion is essentially to create group advantages, and the integration of digital technology can effectively link all stores together.”

Third, while expanding, it is also essential to continuously improve the supply chain.For the chain medical industry, economies of scale are inevitably one of its core competitive advantages, while another major core competitive advantage stems from the supply chain, which reflects operational efficiency, including warehousing, logistics, and management capabilities.

The final point is to look beyond the individual store, realign supply with demand, and maximize the value of each single store.Currently, many chain pharmacies have begun engaging in “supermarket-style” operations, including selling fruits, eggs, rice, and cooking oil. While this model may not be applicable to all chain medical institutions, the underlying industry logic it reveals is that the transformation of revenue structures for chain medical outlets has officially been placed on the agenda.

For instance, Qingdao Bohou Medical, which initially positioned itself in community-based general practice, has gradually transitioned toward services such as community chronic disease management, geriatric care, home-based medical care, and physical therapy and rehabilitation, achieving favorable returns. Similarly, Chengdu Ande General Practice Clinic, originally focused on pediatrics and common adult conditions, has now shifted its business focus to sub-specialties including “child growth and development, minimally invasive aesthetic medicine, and pediatric dentistry,” while establishing collaborations with multiple public and private healthcare institutions. In the field of medical aesthetics, many traditional aesthetic clinics have also begun transitioning toward minimally invasive aesthetic procedures, which have already become their primary revenue stream.

In this regard, industry experts have analyzed that, “In the future, consolidation in the chain healthcare industry will accelerate further. As scaling becomes increasingly challenging, only by maximizing the value of individual stores can companies hope to alleviate the profitability dilemmas caused by expansion.。”

Currently, the development of chain healthcare in China has entered a “deep-water zone,” making expansion more significant at this stage. However, high-quality acquisition targets are becoming increasingly scarce, and industry competition is intensifying, leading to a gradual decline in the overall marginal benefits of expansion. Therefore, while this presents an unprecedented opportunity, it also poses substantial challenges. To stand out, chain healthcare institutions must not only demonstrate greater “hard power” but also deeply understand the market and adjust their expansion strategies in response to market changes, which is particularly crucial.

1. “Chain Pharmacies with ‘No Cash Crunch’ Are Burning Money to Expand Aggressively” — Times Finance;

2. “Behind Yixintang’s Cash Pooling Operations: Aggressive Expansion Alongside Close Monitoring of Capital Chains” — TMTPost;

3. “When Pharmacies Start Running ‘Supermarket’ Businesses?” — Chaoxi Business Review.