Daoyuan Capital Research Report: Analysis and Outlook of the Nucleic Acid Therapeutics Industry

Editor’s Note: This article is from KinghandCapital, and VCBeat has been authorized to republish it.

This article offers insights from the three dimensions of points, lines, and planes, aiming to address three key questions in the nucleic acid therapeutics industry:

1. What is the current development status of nucleic acid therapeutics?

2. Are nucleic acid drugs the mainstream trend in future pharmaceutical innovation, and can they lead the way in ushering in the third wave of drug development?

3. What are the bottlenecks in the development of the nucleic acid drug industry, and where lie the breakthroughs for future innovation and industrialization?

(2023–2024)

Examining Trading Hotspots in Innovative Drugs

1、Macro Background of the Pharmaceutical Industry: Robust Cross-Border Transactions and Profound Shifts in Capital Landscape

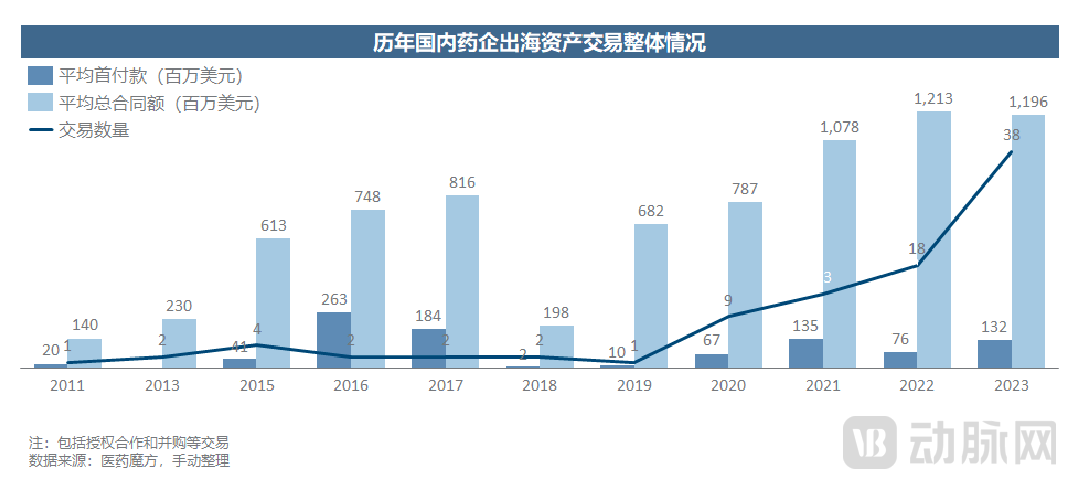

Background 1:Two nucleic acid drug deals in 2024 pioneered the global expansion of nucleic acid therapeutics.The number of overseas licensing deals by Chinese biotech companies rose rapidly from 2020 to 2023. Molecular modalities such as ADCs, CAR-T therapies, and bispecific antibodies are favored.

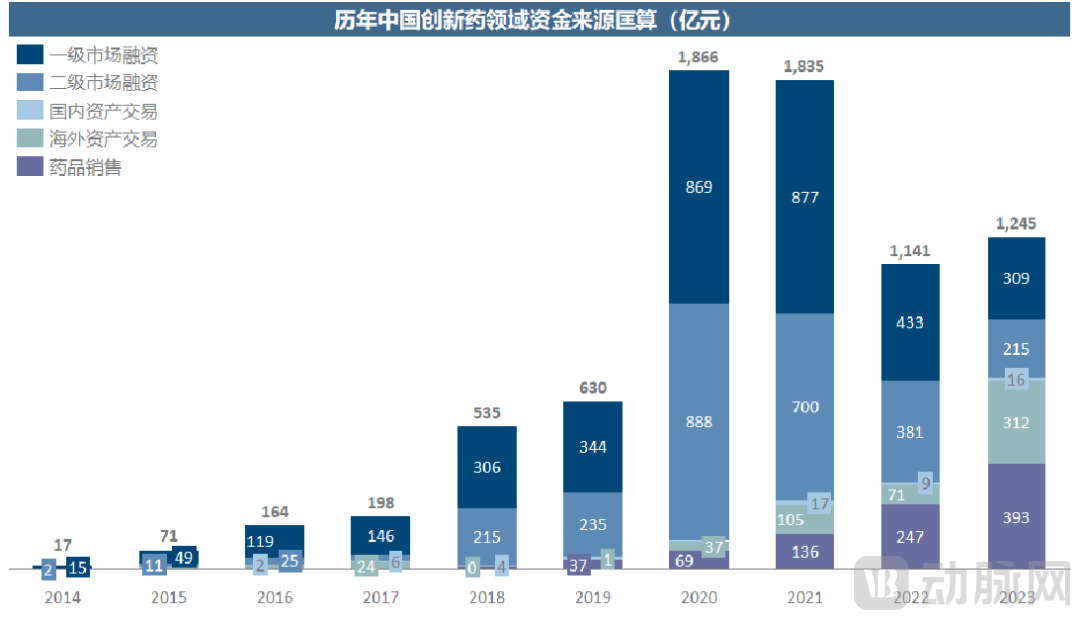

Background 2: Structurally, the funding sources for biotech companies have undergone a profound transformation. Over a mere one to two years, the landscape has shifted from one where equity financing provided more than 90% of capital for many consecutive years,By 2023, a tripartite balance had emerged among equity financing, asset transactions, and drug sales.

2、Global BD Deal Analysis 2023–2024: Small Nucleic Acid Pipelines Are One of the Hotspots in Global BD Deals in Recent Years

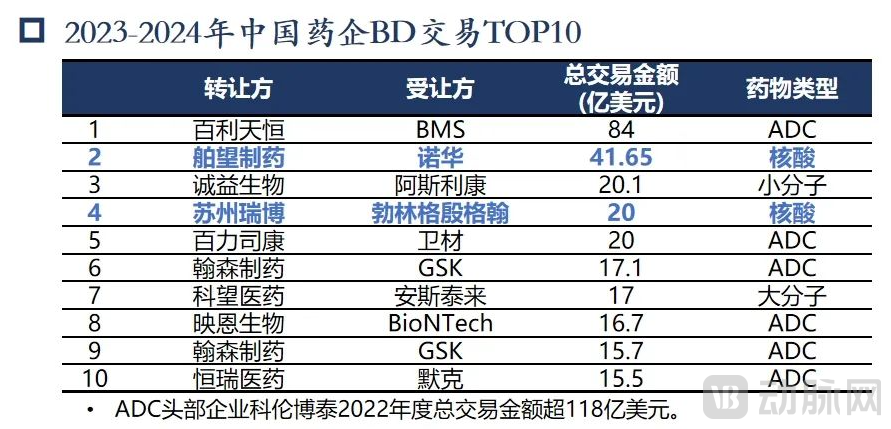

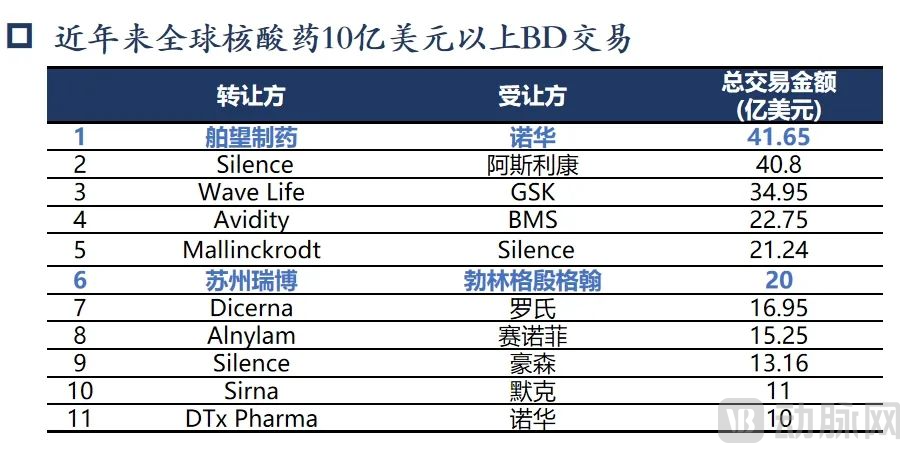

The total value of these two nucleic acid drug transactions ranks among the top tier both in China and globally, with both deals securing spots in the top 10 nucleic acid drug transactions worldwide across all years. Following ADCs, China’s nucleic acid drug pipeline is poised to become the next area of intense focus for multinational corporations (MNCs).

Kinghand Capital reviewed global innovative drug pipeline deals with total transaction values exceeding USD 300 million from 2023 to 2024, and the number of transactions is ranked as follows:

Nucleic acid therapeutics ranked among the hot areas in innovative drug pipeline transactions during 2023–2024, alongside other fields such as antibody-drug conjugates (ADCs), artificial intelligence (AI), adeno-associated virus (AAV) delivery, gene editing, and bispecific antibodies.

In 2024, Ribo Life Science and Boehringer Ingelheim, as well as WaveLife Therapeutics’ Chinese partner (Bowang Pharmaceuticals) and Novartis, completed two pipeline business development (BD) deals, marking a breakthrough in the global expansion of China’s oligonucleotide therapeutics sector. Nucleic acid-based drugs have thus become the next niche area of innovative medicines developed in China to gain global recognition, following the success of antibody-drug conjugates (ADCs). In that year, five of the top ten global pharmaceutical companies engaged in BD transactions in the nucleic acid therapeutics space, and to date, only two of the top ten global pharmaceutical companies have not yet entered this field. Nucleic acid therapeutics have become a strategically critical battleground for multinational pharmaceutical companies.

Kinghand Capital has long prioritized nucleic acid therapeutics as a key investment focus. Its funds invested nearly RMB 60 million in Bowang Pharma across two rounds during the Series A stage. Moving forward, Kinghand Capital will continue to collaborate with Bowang Pharma and actively position itself across the upstream and downstream segments of the nucleic acid therapeutics industry chain.

3、Why Are Nucleic Acid Drugs Favored by Multinational Pharmaceutical Giants?

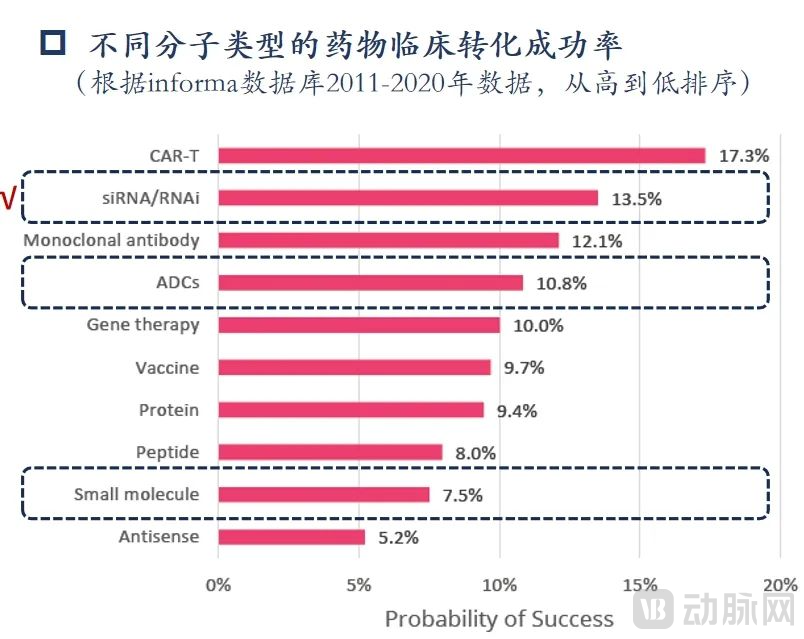

Point 1: Nucleic acid drugs exhibit high druggability, with a higher clinical translation success rate than ADCs and small molecules. Due to their favorable safety profile, their Phase I clinical trial success rate is significantly higher than that of other molecular types.

Second, nucleic acid drugs offer significant advantages over small-molecule and antibody drugs in three aspects: patient compliance (with dosing as infrequent as once every six months), drug safety, and target selection.

Third: Nucleic acid therapeutics have been clinically validated. Currently, 14 nucleic acid drugs are on the market. In the future, their applications will expand from rare diseases to common and major conditions such as cardiovascular disorders, establishing them as a major class of therapeutic molecules.

From a Timeline Perspective

The Historical Development and Trends of Nucleic Acid Therapeutics

1、The development trajectory of nucleic acid drugs is similar to that of ADCs,The Industry Is Poised for an Imminent Boom

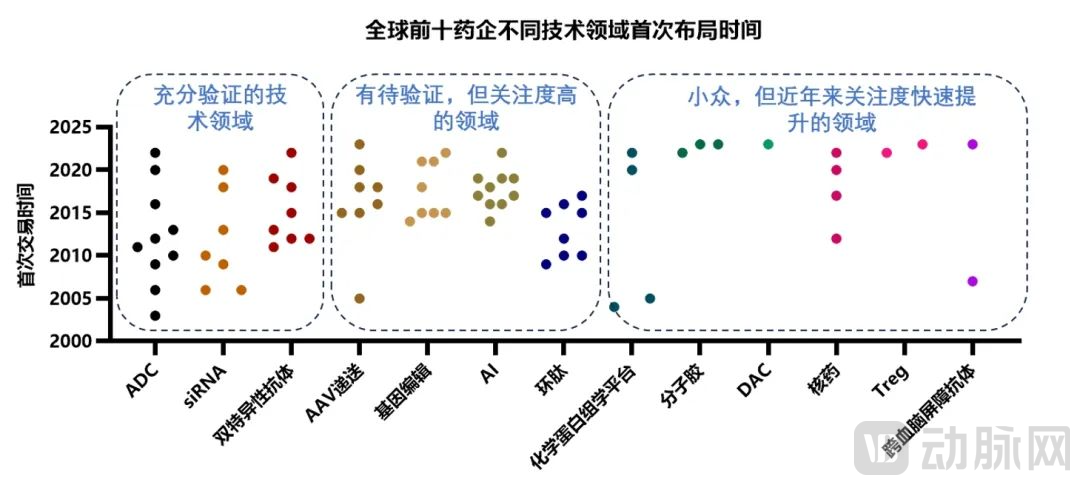

The development timeline of nucleic acid therapeutics mirrors that of antibody-drug conjugates (ADCs): ADC-related transactions heated up rapidly in 2023. However, it is evident that major pharmaceutical companies had already made their initial strategic moves around 2010. It may take a decade from the time when the top ten pharmaceutical companies begin to lay out their strategies to the explosion of transactions involving this molecular type. Small nucleic acid therapeutics follow a similar development trajectory to ADCs, having undergone a decade of technological iteration; the industry is poised for rapid expansion in the coming years.

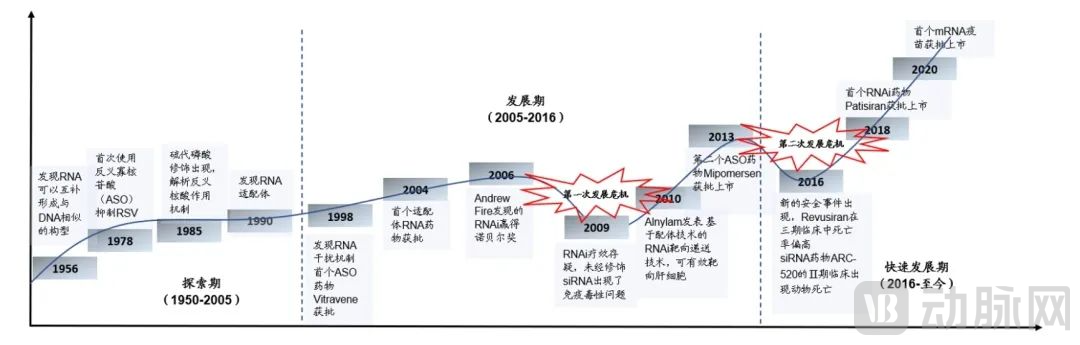

Nucleic acid therapeutics have undergone two leapfrog developments, resolving the challenge of hepatic delivery and entering a phase of rapid growth. In 2009, serious safety incidents emerged during clinical trials using unmodified siRNA; subsequent advances in chemical modification technologies enabled continued development. The second major challenge for the nucleic acid therapeutics industry arose around 2016, when new safety concerns surfaced in clinical settings. Once again, the advent of novel delivery systems propelled the field forward. In 2014, Alnylam published literature on GalNAc-related technology, and in 2018, Patisiran, the world’s first RNAi therapeutic, received FDA approval, ushering small nucleic acid drug development into a new era.

Starting from a Comprehensive Overview of the Current State of Nucleic Acid Drug R&D

# Future Directions

1、Nucleic Acid Drugs: Diverse Types and Functions, with siRNA as the Mainstream Development Focus

Based on their mechanisms of action, RNA therapies can be categorized into three major classes:

1) Small nucleic acid therapies: targeting nucleic acids, such as ASOs (antisense oligonucleotides) and siRNA;

2) Aptamers: Targeting proteins and modulating protein activity;

3) mRNA drugs or vaccines: targeting encoded proteins or antigens.

siRNA is currently a focal point in drug development due to its high druggability, while other types of nucleic acid therapeutics serve as robust complements to siRNA. Most domestic nucleic acid therapeutic companies at the clinical stage in China currently employ technology platforms based on siRNA.

2、The Overseas Landscape of Nucleic Acid Therapeutics Is Set, with Leading Chinese Companies Emerging

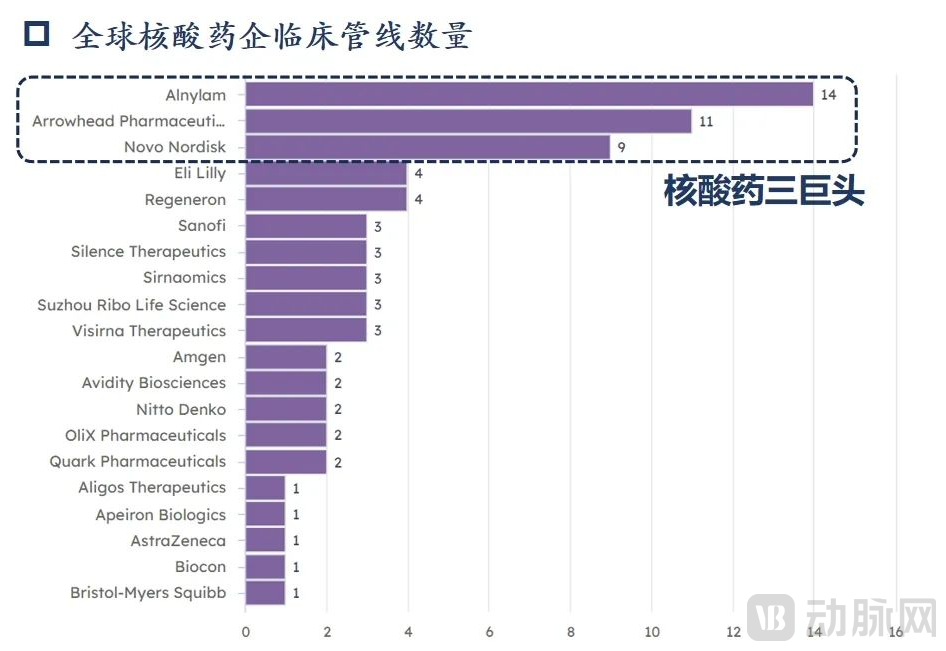

Overseas Industry Landscape:The siRNA sector is currently characterized by a pronounced consolidation among leading players, with clinical pipelines primarily concentrated in three companies: Alnylam, Arrowhead, and Novo Nordisk (which previously acquired Dicerna).

China's Industry Landscape:Currently, approximately 10 companies in the siRNA field have nucleic acid drug pipelines entering clinical trials. Most of their self-developed pipelines are in Phase I clinical trials, among which Bowang, Shengnuo, and Ribo Life Science have more advanced and rapidly progressing clinical-stage pipelines. The competitive landscape of the nucleic acid drug industry has not yet been fully established.

3、Five Factors Constituting Barriers to Nucleic Acid Drug Development

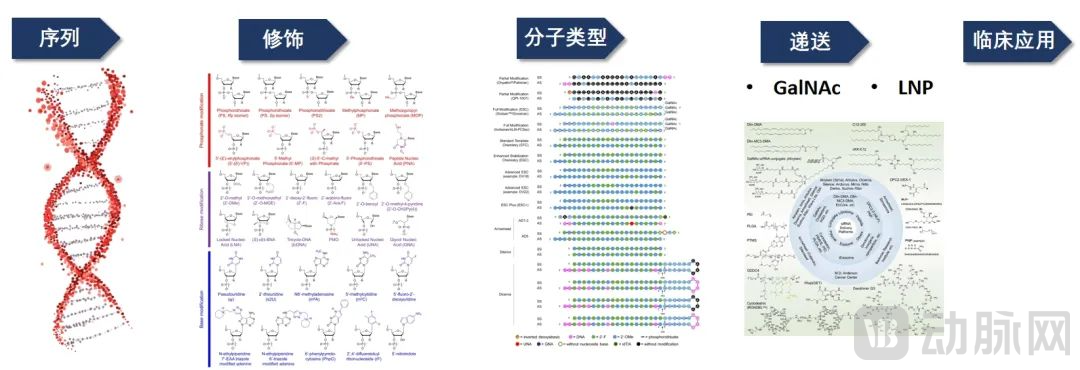

Nucleic acid therapeutics differ significantly from small-molecule drugs and antibody-based therapies across all aspects of design, testing, and manufacturing. Consequently, substantial bottlenecks persist in five key areas: nucleic acid sequence optimization, chemical modifications, exploration of nucleic acid molecular types, innovation in delivery systems, and expansion of clinical applications. Sequence design and chemical modifications determine drug efficacy and stability, granting leading companies a significant first-mover advantage and enabling them to establish robust patent barriers. The exploration of nucleic acid molecular types and innovations in delivery systems dictate the prospects for clinical application expansion, making them focal points for future breakthroughs in nucleic acid therapeutic development.

Need for Technological Innovation:

1. Delivery Technology: Currently, extrahepatic delivery technology remains a bottleneck in the development of nucleic acid therapeutics, limiting the expansion of their indications.

2. Homogenized Competition: The domestic nucleic acid drug industry in China is currently exhibiting a pronounced trend of homogenized competition in delivery technologies and target selection. Companies lacking independent intellectual property rights that merely follow trends may face future risks related to patents on sequences, modifications, and other aspects.

3. Indications and Market: Nucleic acid therapeutics urgently need to expand from rare diseases to common diseases, further enlarging the market size.

Need for Industrial Agglomeration:

4. Talent Scarcity: Nucleic acid drug R&D differs significantly from small-molecule and antibody drugs in design, testing, and manufacturing. Consequently, there is a scarcity of professionals specializing in the design, evaluation, and production of nucleic acid drugs, particularly those with experience in industrial-scale manufacturing.

5. Industry Chain: Nucleic acid drug companies and their upstream and downstream enterprises are still in a stage of rapid development, with no industrial clustering formed yet. In the nucleic acid drug industry chain, there is still significant demand for domestic substitution, technological iteration, and cost optimization in segments such as CROs, CDMOs, and production equipment.

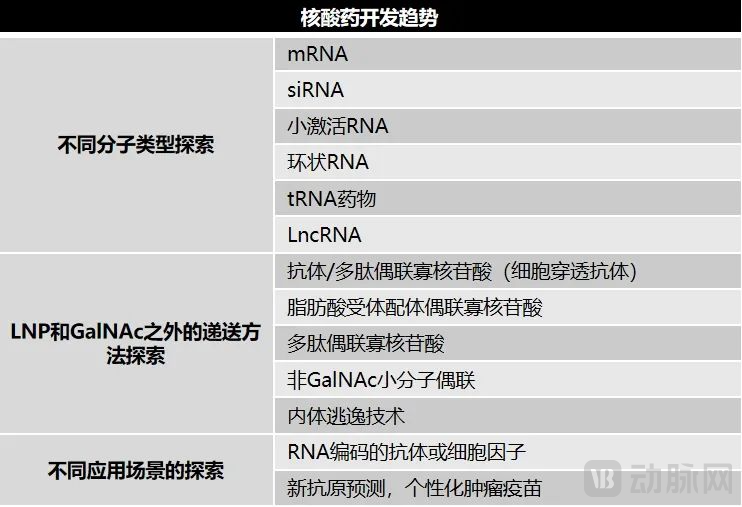

4、Future Innovation Trends in Nucleic Acid Therapeutics

GalNAc-based hepatic delivery technology for nucleic acid therapeutics has now matured. Future breakthroughs in extrahepatic delivery, which will further expand the clinical applications of these therapeutics, will require sustained advancements in three key areas: exploration of molecular types, innovation in delivery systems, and expansion of application scenarios.

About Kinghand Capital

Kinghand Capital is a leading private equity investment firm focused on the healthcare sector, dedicated to leveraging capital and industry resources to accelerate the growth of outstanding healthcare enterprises, deliver superior medical products and services to society, and advance human health.

Currently, Kinghand Capital manages 16 RMB-denominated funds and three USD-denominated funds. Its portfolio includes investments in 84 high-quality projects, with 16 companies having completed initial public offerings (IPOs), including one that has received registration approval from the China Securities Regulatory Commission (CSRC). These listed companies include Aier Eye Hospital’s competitor Puri Ophthalmology (SZSE: 301239), Jinxin Fertility Group (HKEX: 1951), Sino Medical Sciences Technology (SSE STAR Market: 688108), Tinavi Medical Technologies (SSE STAR Market: 688277), Viva Biotech Holdings (HKEX: 1873), Innotest Diagnostics (SSE STAR Market: 688253), Labpioneer Medical Technology (SSE STAR Market: 688393), Clover Biopharmaceuticals (HKEX: 2197), and Angios (SSE STAR Market: 688581). As of the current date in 2023, one portfolio company has filed for an IPO on the SSE STAR Market and had its application accepted. Kinghand Capital expects more than ten of its investee companies to list on major domestic and international stock exchanges within the next two years.