Local State-Owned Capital vs. University-Backed Funds: Which Is the Preferred Choice in the Current Investment Winter?

Since 2023, a joke has been circulating in the industry, roughly meaning that"If you haven’t dealt with state-owned capital yet, you’re basically still a novice."。

Although this may be somewhat exaggerated, what it actually seeks to convey is the current state-owned capital’s extremely high level of participation across the entire healthcare industry. According to incomplete statistics from the VCBeat Orange Database,In 2023, there were 388 investment events in China's healthcare sector with direct participation from state-owned capital., which is exactly double the figure from the previous year. This trend continued in 2024; as of March 28,In China, there were 69 investment deals in the healthcare sector with direct participation from state-owned capital, accounting for 31% of the total number of financing transactions.. However, this is only the tip of the iceberg; if indirect investments by state-owned capital in capacities such as fund-of-funds and limited partners (LPs) are included, this proportion would be even higher.

But this is not a unique landscape; on the other side, where state-owned capital has shown impressive performance, university-affiliated funds are also gradually gaining momentum. According to statistics from FOFWEEKLY, 2In 2023, a total of seven new funds were established by Chinese universities, with an aggregate scale of nearly RMB 5 billion., including Shanghai Jiao Tong University, Fudan University, Zhejiang University, Wuhan University, Central South University, and many other universities have participated. And earlier this year, Hong Kong University, Tianjin University, and many other domestic universities began to enter the market as LPs, with unprecedented investment strength.

This is truly a rare sight. In the past, both local state-owned assets and university-endowed funds mostly played supporting roles in the capital markets. Today, however, both have made significant strides onto the stage of China’s venture capital history, becoming vital sources of fresh capital in the current market.

It is precisely for this reason thatA question is now before all healthcare professionals: namely, the choice ofLocal State-Owned Assets or University Funds?Amid the current market winter, this choice has become particularly critical.

“Product” of the Times

Cast your mind back to early 2023, when the pandemic had just been declared over. Everything seemed like a fresh start, and everyone was filled with renewed energy.

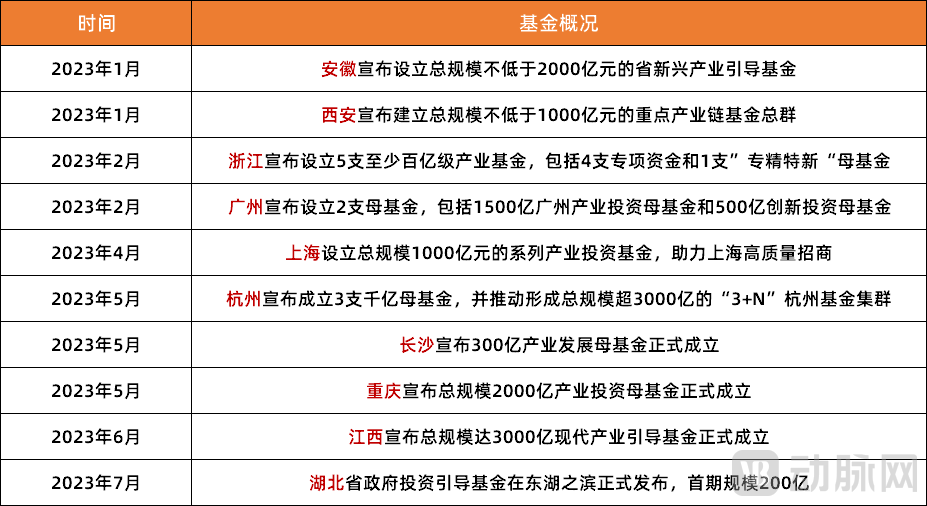

Figure 1. Local state-owned assets established in clusters in 2023 (Source: Public information)

Among them, local governments have been the most proactive. On January 16,Anhui Takes the Lead in Local State-Owned Capital Reform, Announces Establishment of Provincial Emerging Industries Guidance Fund with a Total Scale of No Less than RMB 200 Billion, soon after, cities such as Xi’an, Hangzhou, Guangzhou, Shanghai, and Chengdu also ramped up their efforts, successively launching large-scale guidance funds. Since then, hundreds of billions and even trillions of yuan in fund-of-funds have emerged one after another across various regions; it is reported thatAs early as August 2023,The Total Scale of Government Guidance Funds Established in Multiple Regions Has Exceeded RMB 1 Trillion, and is still growing exponentially.

This is no exaggeration; in fact, the trend of local state-owned capital increasing its investments has continued to unfold on a large scale recently. On March 20, the Suzhou Suchuang Biopharmaceutical and Greater Health Venture Capital Fund, led by Suzhou Venture Capital Group, was officially established with a total size of RMB 5 billion. On March 21, Xiamen Industrial Investment Co., Ltd., the municipal industrial investment platform of Xiamen City, was unveiled and established with a registered capital of RMB 20 billion. On March 22, the Beijing Pharmaceutical and Health Industry Investment Fund, with a total size of RMB 20 billion, was officially signed and established in Changping District.

Amid the current capital winter, the announcements of these funds’ establishment have been particularly resounding. So, what exactly is driving local state-owned assets to aggressively increase their investments?

There are multiple factors involved, butThe most critical point is undoubtedly “investment attraction.”. In the post-pandemic era, there has been a strong drive for economic growth across various regions; however, investment promotion has become increasingly challenging. The traditional, simplistic approach to attracting investment is no longer effective in securing high-quality enterprises, prompting local governments to widely adopt the new model of “investment-driven attraction.” In this process, the healthcare sector has emerged as a common priority for local state-owned capital. This is partly because healthcare is both a livelihood-critical industry and one with hard-tech attributes, and partly because its substantial market size is sufficient to support further advancements in local economies.

In this regard, a state-owned enterprise executive remarked, “For local economies to grow at present, they must rely on investment promotion, attracting more companies to establish operations locally so as to increase tax revenues. Therefore, over the past couple of years, even though some local governments have faced significant fiscal challenges, they have still been willing to allocate tens or even hundreds of billions of yuan toward this effort.”Since everyone is engaging in capital-driven investment promotion, if you do not follow suit, high-quality projects will certainly not settle in your region, making it difficult to stimulate economic development.。”

There are clear reasons for the strong focus on the healthcare sector. A project leader at a state-owned medical enterprise stated, “First, the healthcare industry is a national strategic priority, representing the broader direction of future industrial development. Second, from an industry perspective, the entire healthcare sector has experienced rapid growth in the post-pandemic era and is currently at a critical juncture of a new development cycle, with substantial market opportunities yet to be tapped. Finally, in terms of practical implementation and commercialization, the healthcare market is large in scale, capable of generating significant tax revenue for local governments. Moreover, it effectively drives local employment and promotes the horizontal development of other related industries.”

Therefore, in the eyes of many professionals,The “state-owned capital wave,” which has been fervently embraced by the healthcare sector over the past two years, is in fact a phenomenon specific to a particular historical period.. On one hand, against the backdrop of a cooling market, the industry requires local state-owned assets to take the lead; on the other hand, driven by the evolution of investment promotion models, state-owned capital has also become a powerful tool for local governments to seek new economic growth points.

However, it is not only local state-owned assets that are hailed as specific “products of the times”; university endowment funds are no exception.

Compared with their overseas counterparts, university endowment funds in China started later and, for a long period, primarily operated behind the scenes. In this regard, Yuan Wei, Secretary-General of the Tsinghua University Education Foundation, once stated, “Due to a lack of professional expertise and other various factors,”University endowments in China tend to be conservative; most prefer to act as qualified limited partners (LPs) without taking a leading role or interfering with general partner (GP) decisions, resulting in an overall low participation rate.。”

The heightened activity in the past year or two is largely attributable to the fact that technological innovation has become the central theme of contemporary healthcare venture capital investment.

In recent years, the healthcare industry has placed increasing emphasis on original innovative technologies and the commercialization of research outcomes. Against this backdrop, universities, as the primary sources of innovation, have naturally garnered greater attention. Initially, collaborations may have been limited to technical research partnerships. Over time, a wave of entrepreneurship gradually emerged within universities, with more scientists stepping out of their laboratories and into the entrepreneurial arena. In the past one to two years, university-affiliated funds have also gained momentum, assuming diverse roles such as acting directly as venture capital (VC) investors, investing as limited partners (LPs) in general partner (GP) firms, and establishing fund-of-funds structures.

In this regard, a university fund investor remarked, “Amid the current surge in the commercialization of scientific and technological achievements, universities—possessing inherent advantages in talent resources and R&D capabilities, as well as serving as vast resource pools—naturally aspire to establish an industrial closed loop. Therefore, investment and financing are indispensable components. Hence,”The growing activity of university endowment funds is, in essence, a microcosm of the era of technological innovation.。”

Same “Fate,” Different Paths

Currently,“Investing early, investing in small businesses, and investing in technology” is undoubtedly the prevailing trend in the entire investment community., and as the two hottest funds at this stage, local state-owned capital and university-affiliated funds are naturally unable to escape this law.

This is particularly true for local state-owned assets, which may feel the impact more acutely. In the past, they primarily focused on mid-to-late stage projects; however, they are now compelled to significantly shift their investment focus toward earlier stages. Commenting on this trend, a head of a state-owned asset platform in Chongqing stated, “In the healthcare sector, we rarely invested in early-stage projects in previous years due to generally high risks and limited industrial certainty. However, over the past few years, we have laid substantial groundwork for early-stage investments,”From an objective standpoint, this is an industry trend; only by getting involved early can you secure future opportunities. On a subjective level, it has become increasingly difficult to find high-quality mid-to-late-stage healthcare projects in the market.。”

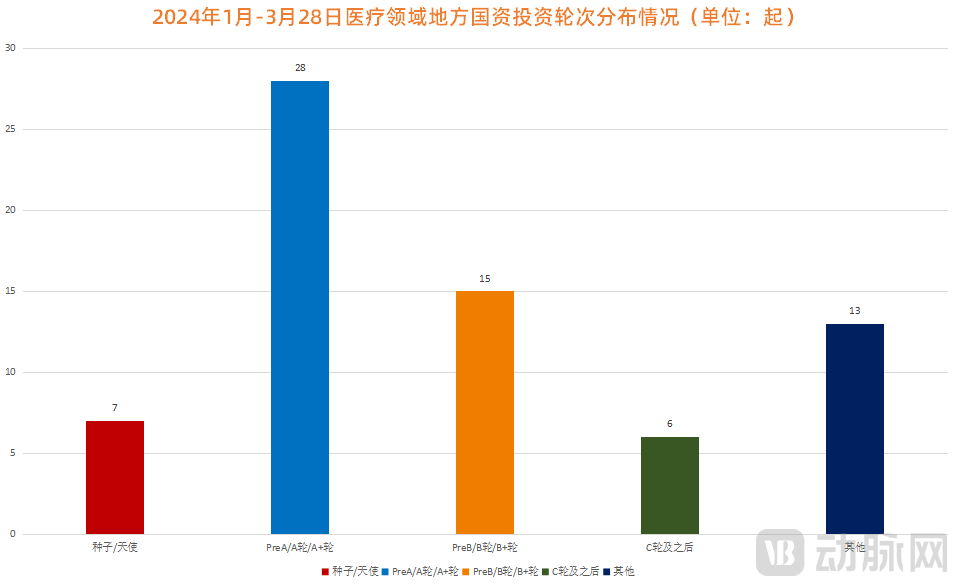

Figure 2. Distribution of Local State-Owned Capital Investment Rounds in the Healthcare Sector from January to March 28, 2024 (Data Source: VCBeat)

Figure 2. Distribution of Local State-Owned Capital Investment Rounds in the Healthcare Sector from January to March 28, 2024 (Data Source: VCBeat)

Consequently, there is a growing demand for funds to operate in a more market-oriented manner. In response, local state-owned assets and university-affiliated funds have been making concerted efforts in recent years, with their primary solution being the recruitment of a large number of professional investors from outside. Indeed, this has become a widespread phenomenon. An investor who joined a state-owned entity last year shared his personal experience, stating, “Nearly half of our team members have now moved to state-owned enterprises.。”

Of course, in addition to their similarities, local state-owned assets and university funds also exhibit certain differences due to their distinct attributes and missions.

For instance, in selecting early-stage healthcare projects, local state-owned capital is more inclined to introduce external ventures, as its core objective is investment promotion. In contrast, university-affiliated funds tend to focus on their own institutions. Taking Fudan University as an example, the “Fudan Sci-Tech Innovation Fund of Funds” was officially launched in December 2023 with an initial size of RMB 1 billion, explicitly stating that it would prioritize supporting the commercialization of Fudan’s scientific and technological achievements as well as alumni-led innovation and entrepreneurship initiatives.

Of course, beyond the source of projects, the two major funds also have their own preferences when it comes to selecting specific niche sectors. Taking local state-owned capital as an example, its reference criteria mainly include two aspects: either aligning with its own industrial advantages or complementing and strengthening the existing industrial chain. Taking Chengdu as an example, its current strategic focus is primarily on biomedicine, given that the city has multiple listed companies in the pharmaceutical sector, making it easier to establish a closed-loop industrial ecosystem.

University endowment funds are relatively “focused,” primarily centering on their own strengths in specific disciplines. Taking Shanghai Jiao Tong University as an example, it boasts a powerhouse team in medical robotics. On the public market side, it is associated with listed companies such as Runmai De and MicroPort MedBot. In the private equity market, it has invested in high-quality targets including Fourier Intelligence, Jingmai Medical, Huihe Medical, Timi Robot, and Zhuodao Medical. Therefore, it is hardly surprising that the university places greater emphasis on the medical robotics sector and has established dedicated funds for this purpose.

However, this is only part of the difference; the two funds also differ significantly in their post-investment value-added services.

For instance, local state-owned assets primarily provide empowerment at the policy level and through hard resources, mainly land.In this regard, a representative from a state-owned enterprise (SOE) remarked, “Given the direct alignment with government interests, land allocation and expedited regulatory approvals fall within the purview of benefits provided by local SOEs. For instance, in terms of land provision, numerous industrial parks have been established consecutively, with increasingly mature supporting infrastructure. Regarding regulatory approvals, local SOEs often tailor and optimize relevant policies to facilitate product approval or smooth corporate listings.”

In contrast, university-affiliated funds tend to focus more on the industry itself, such as by driving R&D and directly connecting with market resources. Taking the latter as an example, these funds can provide substantial empowerment by leveraging the large number of listed companies and leading capital firms clustered around them. Specifically, listed companies can facilitate business transactions and collaborations, while leading capital firms can offer support in subsequent financing rounds and IPO processes. For medical enterprises today, these are all critical sources of strength.

The Other Side of the Surge

Although frontier innovations and technological iterations in the healthcare sector are still ongoing, one of the primary tasks for most capital investors this year is to fulfill their local reinvestment obligations.

In fact, many institutions are currently grappling with this issue, as most performance indicators are difficult to meet. There are numerous reasons for this, one of which is the generally high requirement for local reinvestment ratios. It is reported that, in order to promote investment attraction, local state-owned assets have occasionally reduced reinvestment ratios and relaxed restrictions; however, such cases remain isolated. According to an investor, “Although the minimum reinvestment ratio can technically reach 1:1 on paper, this is uncommon and often subject to restrictions such as upfront reinvestment requirements, making it rather “hot to handle.”。”

In addition to high ratios and numerous restrictions, the weak local economies and industrial bases in certain regions also pose significant obstacles for many institutions in fulfilling their reinvestment obligations. It is reported that during the early stages of the market downturn, many institutions paid little heed to these concerns in their bid to secure funding. However, as time went on, they found the path increasingly difficult, particularly in third- and fourth-tier cities, where most reinvestment targets proved hard to meet. In this regard, a head of one institution remarked, “Before accepting government funding, we must first assess the local economy and industrial base; regions with weak foundations are typically excluded from consideration, as it is difficult to fulfill subsequent reinvestment requirements.。”

However, this is only one part of the picture. Setting aside “reverse investment,” local state-owned capital itself is also under significant pressure. The first challenge is how to endure the calm after the frenzy. It is reported that some medical enterprises’ current financiers,Nine out of ten are typically state-owned enterprises., which means that many projects have not undergone sufficient market assessment and validation, making exit increasingly difficult as these projects progress.

Furthermore, homogeneous competition is another source of pressure. A representative from a state-owned enterprise remarked, “Given that everyone shares the same investment promotion targets and is still in the exploratory phase,”There is actually little difference among local state-owned assets; the key factors to consider are the sector, underlying benefits, and hard metrics, which are largely similar.Amid the current market winter, everyone is forced to engage in cutthroat competition within a limited space.”

Having discussed local state-owned assets, we now turn our attention to university-affiliated funds, which are currently facing significant growth challenges, with the most pressing being the sudden demand for profitability. In the past, university-affiliated funds were not prominent players in the capital markets; their limited investments were primarily short-term or debt-oriented, rarely involving low-liquidity, high-risk long-term or equity investments. This stands in stark contrast to the current fervent market participation, a shift driven by the funds’ own profitability targets. It is reported that among the three core missions of the Tongji Alumni Fund, “revitalizing the existing assets of the university’s endowment fund to achieve long-term preservation and appreciation of wealth” ranks first.

Beyond this, another significant challenge lies in how university endowment funds can break through their insular circles and extend their reach outward. It is well known that while university endowment funds possess substantial industrial resources, their immediate ecosystem consists largely of “insiders”—either enterprises incubated by the universities themselves or capital firms founded by alumni. This limited degree of openness makes it difficult for these funds to expand externally, while also creating high barriers for “outsiders” to enter. Within such a relatively closed environment, it is considerably challenging for university endowment funds to transform into “patient capital” and “long-term capital.”

Therefore, in retrospect, the fact that both local state-owned assets and university-affiliated funds have quickly become the “protagonists” of the capital market is largely attributable to the times.Amid the capital winter, the winds of technological innovation have pushed both funds from behind the scenes to the forefront.. In the midst of this rapid identity transition, insufficient maturity has led to emerging challenges; those who can swiftly identify solutions will stand out. After all, survival of the fittest remains an enduring and unchanging principle in the venture capital industry.

On the other hand, many investors also believe that the current high-profile approach of local state-owned assets and university funds is not necessarily a good thing,A well-functioning and mature primary market should be stratified, encompassing projects that address employment, those that generate wealth, and those that pioneer the future; correspondingly, this requires support from institutions operating across different dimensions.. Therefore, as the industry returns to rationality, what belongs to the market will ultimately return to the market, state-owned assets will naturally revert to state ownership, and university-affiliated assets will return to universities.

1. “Why ‘Cash-Strapped’ Governments Are Making High-Stakes Bets on ‘Capital-Driven Investment Promotion’” — Qin Shuo’s Circle of Friends;

2. “How to View the Primary Market in 2024” — Brother Xing, the Star Counter;

3. “When VC/PE Despairs” – Fund of Funds Research Center.