Is Now the Best Time to Invest in Biotech?

In the first quarter of 2024, capital in the market began to flow back into the biopharmaceutical sector.

In the primary market, biotech financing in North America and Europe saw a significant year-on-year increase in the first quarter, with 20 large-scale deals exceeding $100 million each, representing a 66% year-on-year growth.

The most notable development remains the wave of U.S. biotech IPOs. Since the first quarter, nine companies have gone public, with CG Oncology, the first company to launch an IPO this year and a developer of oncolytic virus therapies, surging 95% on its debut and gaining more than 130% to date.

Furthermore, U.S.-listed biotech companies raised over $4 billion in refinancing this year. Several biotech firms announced follow-on offerings, triggering a surge in their stock prices. In March alone, iBio’s stock soared by 192% on the day it announced its follow-on offering, while Avalo’s stock jumped by 400% on the day of its announcement.

From a global market perspective, the biopharmaceutical sector has finally “turned a corner” this year, compared to the chilly start of 2023. However, a close examination of capital inflows in the first quarter reveals that the overarching theme remains risk aversion.

Primary Market: Embracing Innovation with Conditions

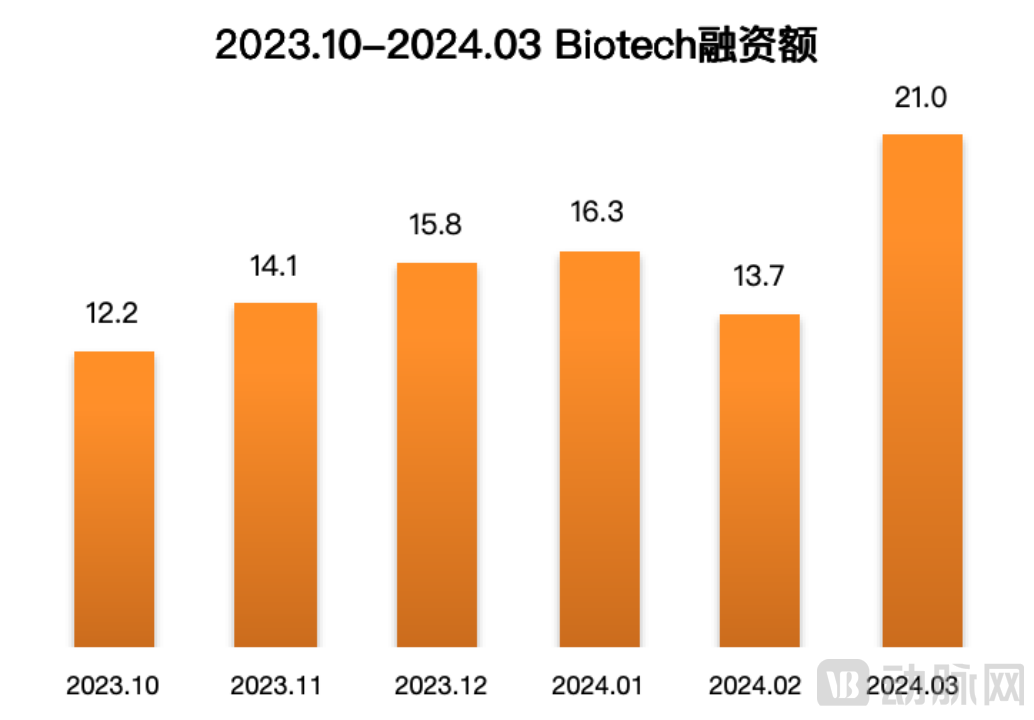

The biotech primary market experienced a long-awaited “small peak” in financing this March, with total funding exceeding $2.1 billion.This is primarily due to two star companies securing large rounds of financing: Alumis, a best-in-class competitor in TYK2 inhibitors, raised $259 million in Series C funding, and Mirador Therapeutics, an autoimmune disease company founded by the founder of Prometheus, raised $400 million in Series A funding.

Statistical Scope: Primary Market Financing in North America and Europe (Unit: USD 100 Million)

Large-scale financing plays a significant role in boosting the biopharmaceutical industry.After years of sluggishness in biotech venture capital and financing, the industry is finally showing signs of recovery. Notably, Mirador Therapeutics, a newly established company with its pipeline yet to be disclosed, has secured an oversubscribed Series A funding round.

Q1 2024 Primary Market Financing Events, Covering North America and Europe

In the first quarter of this year, among more than 60 financing deals, the average financing amount was $80 million, with as many as 39 deals exceeding $50 million. However, in terms of financing stages, early-stage investments still dominated: Seed/Angel and Series A/A+ rounds accounted for nearly 60%.

Capital has demonstrated inclusivity toward various innovative therapies and drug modalities. Companies across fields ranging from cutting-edge cell and gene therapy (CGT) and RNA therapeutics to protein degraders, radiopharmaceuticals, photoimmunotherapy, microbiome-based therapies, and AI-driven drug screening have all secured financing. However, as the market environment recovers, biotech companies are returning to a pipeline-centric logic—streamlining and focusing their efforts to advance products into clinical trials as quickly as possible. Purely platform-type companies are nearly absent from the financing lists, while those securing significant funding (the top 20 by financing amount in the first quarter) have an average of no more than five publicly disclosed pipeline assets.

IPO: Thresholds Quietly Rise

Biotech companies are particularly reliant on the stock market, as they often require substantial capital to fund drug development before generating sufficient revenue to service their debt. This is why the reopening of the U.S. IPO market for biotech firms this year has drawn significant attention from investors.

Since the first quarter, nine U.S. biotech companies have gone public through traditional IPOs, compared with just 19 for the full year of 2023 and 21 in 2022. Even more encouraging is the amount raised: the nine IPOs in the first quarter of this year collectively raised approximately $1.3 billion, whereas the total amount raised for all of 2022 was less than $1.6 billion.

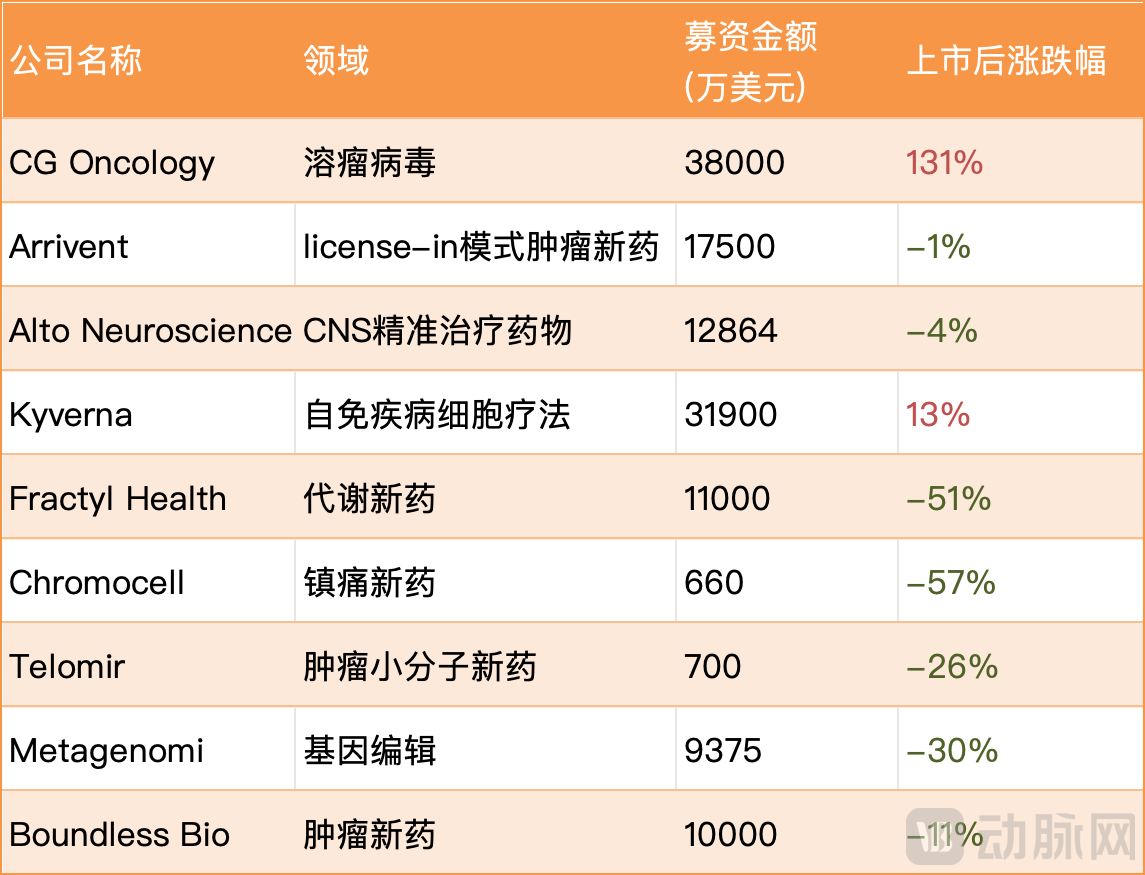

2024 Q1 U.S. Biotech IPOs: Post-listing price changes calculated based on the offering price and the stock price on the last trading day of March

However, the threshold for IPOs has quietly risen. Since early 2023, the profile of companies successfully going public has shifted. Data from BioPharma Dive shows that among the top ten largest IPOs from 2023 to date, nine companies had product pipelines in the mid-to-late stages of clinical development. Among all companies that went public, those that had not yet entered clinical trials raised an average of no more than $90 million at listing.

Looking back at 2020 and 2021, most publicly listed companies were either in preclinical or Phase I clinical trials. This means that companies with early-stage pipelines or those possessing only technology platforms are facing a more challenging period than before.

Among this year’s IPOs, gene-editing company Metagenomi is a typical early-stage biotech firm. This young company, which collaborates with Ionis and Moderna, currently has no drug candidates in its pipeline. Its listing has drawn significant attention from industry insiders, with its stock performance viewed as a bellwether for whether the IPO market is opening up to early-stage companies. However, Metagenomi’s IPO was priced at the low end of its expected range, and its shares subsequently fell 30% after listing, as widely anticipated.

Metagenomi’s post-listing decline does not rank as the largest; Chromocell, a novel analgesic developer, and Fractyl Health, a metabolic disease therapeutics company, have both dropped by more than 50%. Chromocell is a typical early-stage company with its core pipeline in Phase I clinical trials. Meanwhile, Fractyl Health is developing an AAV gene therapy candidate targeting GLP-1. In contrast, CG Oncology surged 131%, as its core product, cretostimogene, for treating high-risk, BCG-unresponsive non-muscle-invasive bladder cancer (NMIBC), has received both FDA Breakthrough Therapy Designation and Fast Track designation. Investor preferences are evident.

“Investors’ patience for larger-scale, longer-duration narratives is not what it was a few years ago,” said a representative from Silicon Valley Bank.

Moreover, some industry insiders believe that many biotech companies considering an IPO are doing so under pressure from investors who have yet to achieve a successful exit. In the past two years, numerous companies have been acquired or faced near-elimination, freeing up capital to support new biotech ventures. Therefore, it is premature to declare a resurgence of robust U.S. IPO activity in the biotech sector.

Post-Listing Refinancing: Capital Flowing Toward Certainty

Post-IPO biotech companies continue to burn cash before achieving commercial viability, making refinancing a critical imperative for their success. In the first quarter of this year, numerous U.S.-listed biotech firms opted for secondary offerings.

In late February, after Viking announced Phase 2 data for VK2735 in the indication of weight loss, its stock price surged more than 120% in a single day. Subsequently, Viking swiftly announced a $350 million follow-on offering to fund the further development of its pipeline, which was met with an enthusiastic response. Before deducting underwriting discounts and commissions as well as offering expenses, the total gross proceeds from this issuance amounted to approximately $632.5 million.

In late March, autoimmune disease-focused biopharmaceutical company Avalo Therapeutics announced the acquisition of Almata Bio, thereby securing AVTX-009, an IL-1β-targeting monoclonal antibody that has entered Phase II clinical trials. The company also announced the completion of a $185 million private placement financing, with its stock price surging by as much as 625% on the same day.

Another biotech that secured substantial funding through a PIPE is Denali. This rare-disease company raised $500 million via private placement in late February. Earlier this year, Denali announced the divestiture of its small-molecule therapy portfolio and implemented workforce reductions, subsequently refocusing its efforts on large-molecule therapeutics research.

Additional share issuances help inject substantial capital into companies, highlighting the biotechnology sector’s appeal to investors. However, these biotech firms undertaking secondary offerings have all released sufficiently positive catalysts—either through impressive clinical data or compelling strategic developments—and their offering prices are typically no lower than the prevailing market price. This demonstrates that capital in the market continues to flow toward certainty. In contrast, the approach seen a few years ago with companies like Fate Therapeutics, which repeatedly raised operating capital through low-priced private placements while incurring significant losses, now appears out of step with current market dynamics.

Now May Be the Best Time to Invest in Biotech

Recently, Jefferies, the most specialized investment bank in the biopharmaceutical sector, stated that the IPO fundraising scale for U.S. biotech companies remains far below pre-crash levels, and current preliminary signs of improvement may not indicate that the biotech sector has fully emerged from its difficulties. As interest rate cuts this year are expected to be slower than anticipated, market sentiment could shift.

The biotechnology industry is characterized by nonlinearity, making the innovation process difficult to predict. The performance of biotech companies is particularly binary, as clinical trial outcomes often determine the success or failure of drug developers. Typically, compared with other industries, biotech represents the most challenging asset class to manage and the “poorest” business model, due to its high complexity, lengthy R&D cycles, and stringent regulatory environment.

Over the past year, the market has witnessed robust growth in the research, development, and commercialization of antibody-drug conjugates (ADCs) and glucagon-like peptide-1 (GLP-1) receptor agonists. For the first time, a pharmaceutical company—Eli Lilly—has entered the top ten U.S. stocks by market capitalization. Furthermore, as patents for previous blockbuster drugs expire sequentially, major multinational corporations (MNCs) have embarked on a new round of “arms race.” The vital lifeline fueling these MNCs is the vast number of biotech companies across both primary and secondary markets.

This is why capital is showing interest in biotech companies with late-stage and commercialized assets. Although funding flowing into the biopharmaceutical sector remains cautious, the XBI Index’s 32% rise over the past six months, coupled with various financing activities, suggests that the current sentiment can at least be described as “cautiously optimistic.” The optimal time to invest in biotech is often precisely during such periods of “cautious optimism”—a middle ground between market downturns and bubbles.

Although the North American biotech market and China’s innovative drug sector have not yet moved in lockstep, the United States, as the engine of biotech innovation, serves as a critical bellwether for Chinese biotech firms in terms of market sentiment, R&D trends, and commercialization outcomes. Moving forward, both U.S. and Chinese biotech companies will unlock greater potential in disease-specific therapeutic areas and technological domains through First-in-Class and Best-in-Class innovations. This new chapter of the future belongs to the global biotech community and the investors who believe in it.