Performance Divergence and the Restructuring of CDMO Industry Rules

WuXi AppTec

New Drug R&D and Production Service Provider

Tot Biopharm

Developer and Producer of Anti-Tumor New Drugs

ASYMCHEM

Pharmaceutical R&D and Production Outsourcing Service Provider

PORTON

Customized R&D and Manufacturing Service Provider in Pharmaceutical Industry

WuXi XDC

End-to-End CDMO Service Provider for Biologics Conjugation Drugs

Haoyuan Chemexpress

Small Molecule Drug Developer

CMS

Professional Drug Developer

Over the past year, the CDMO industry has been in a state of turmoil, grappling with overcapacity and declining orders on one front, while facing targeted scrutiny against industry leader WuXi AppTec on the other.

On March 29, Reuters exclusively reported details regarding the controversy surrounding WuXi AppTec. The article pointed out that during a previous closed-door briefing, WuXi AppTec was accused of engaging in activities in the United States that violated U.S. national security and illegally transferring clients’ intellectual property (IP). IP is the foundation of development in the pharmaceutical industry, and CDMO services, in particular, rely heavily on it. Such accusations have undoubtedly brought undeserved trouble to WuXi AppTec and cast a shadow over the industry’s future prospects.

As industry leaders face headwinds overseas, intensifying competition in the domestic market is inevitable. Yet, against this backdrop, some small and mid-sized CDMOs, such as Tot Biopharm, have bucked the trend. By leveraging differentiated advantages in niche segments, they have achieved divergent performance outcomes even in this challenging environment. Their strategies for breaking through may offer valuable insights for the future development of the CDMO industry.

The starkly contrasting hiring trends reflect the current turbulence in China’s CDMO industry.

On March 18, WuXi AppTec, recently at the center of controversy, released its 2023 financial results. Revenue surpassed RMB 40 billion for the first time, with net profit exceeding RMB 10 billion. Excluding revenue from commercialized COVID-19 projects, income grew by 25.6% year-on-year. However, the market remained unconvinced, and the stock price showed no signs of recovery.

Customer Data Hidden Behind Revenue Figures: The Market’s Concerns About WuXi AppTec

According to financial report data, WuXi AppTec’s 2023 revenue structure comprised income from U.S. customers (RMB 26.13 billion), European customers (RMB 4.70 billion), domestic customers (RMB 7.37 billion), and customers in other regions (RMB 2.14 billion), all of which experienced varying degrees of growth compared to 2022.

In other words, overseas revenue accounts for more than 80% of WuXi AppTec’s total revenue, with U.S. clients contributing over 65% of the overseas portion. Meanwhile, the financial report also reveals that 98% of its revenue comes from existing customers, while new customers generated only RMB 710 million in revenue.

Although an absolute increase of 1,200 new clients is not insignificant, in these turbulent times the market is more concerned about the decline of approximately 200 clients compared with the 1,400 new clients added in 2022, and whether this downward trend will become the new normal. Meanwhile, the 25.08% year-on-year decline in the company’s domestic new drug R&D business segment in 2023 has further fueled market skepticism that, even if the Biosecure Act does not escalate further, the company’s long-term high-growth trajectory may be slowing down.

The reduction in headcount also, to some extent, corroborates market concerns regarding the company.

Financial reports show that as of the end of 2023, WuXi AppTec had 41,116 employees, a decrease of 3,245 from the 44,361 employees at the end of 2022. The largest reduction was in Asia, with 2,962 fewer employees. Although employee turnover is normal in the industry, the current environment, characterized by fewer hires and more departures, reflects the turbulence that companies are currently experiencing.

In contrast, Tot Biopharm, a newcomer to the CDMO industry, announced a 34% increase in its CDMO team size despite the prevailing market downturn. Following this expansion, the headcount of Tot Biopharm’s CDMO business segment reached 464, accounting for 84% of the company’s total workforce, while the retention rate of its core CDMO talent stood at 95%. The confidence behind Tot Biopharm’s team expansion stems from the substantial growth of its CDMO business. According to financial report data, Tot Biopharm’s CDMO revenue increased by 94% year-on-year.

WuXi AppTec’s workforce reductions and conservative guidance for its 2024 performance underscore the ongoing challenges facing the CDMO industry. In contrast, Tot Biopharm’s counter-trend growth in its CDMO business and expansion of its team demonstrate that, in the current climate, small and medium-sized enterprises (SMEs) must proactively adapt and identify breakthrough strategies to carve out a distinct path amid widespread industry downturn.

As small-molecule CDMO business weakens, high-barrier large-molecule CDMO services have become the strategic focus for CDMO companies.

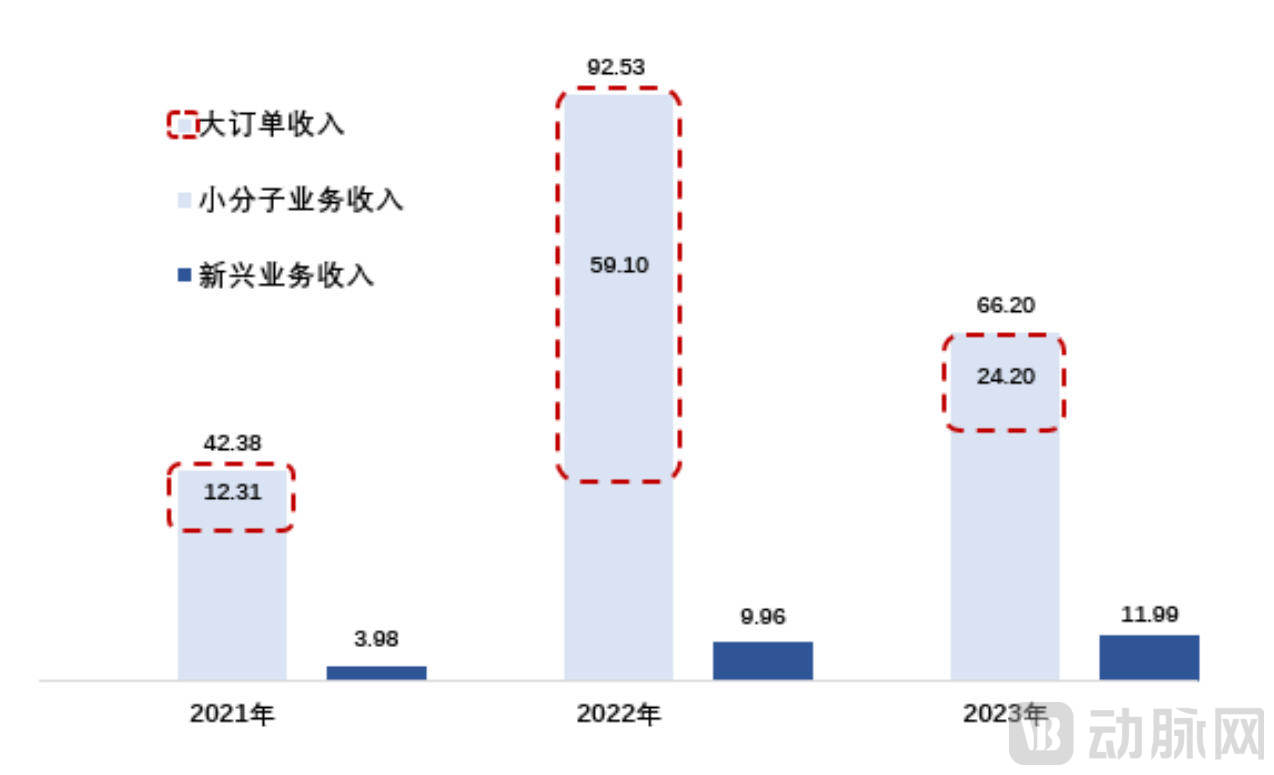

The technical barriers for small-molecule CDMO are not high, with numerous participants and existing overcapacity. In 2023, the small-molecule businesses of leading CDMO companies, including ASYMCHEM and PORTON, experienced significant declines. The former reported small-molecule business revenue of RMB 6.62 billion, a year-on-year decrease of 28.5%, while the latter disclosed in its earnings forecast that its total revenue had dropped by 45%–50% year on year.

ASYMCHEM's Revenue by Business Segment Over the Past Three Years, Source: Annual Report

In contrast, the large-molecule sector faces higher technical barriers in GMP-compliant drug manufacturing due to complex structures, stringent development standards, and increasingly challenging formulation analysis technologies, leading to greater reliance on professional CDMO services. This is particularly evident for antibody-drug conjugate (ADC) drugs, which gained significant traction last year; as these products gradually enter the commercialization phase, their demand for CDMO services is expected to further expand.

On the evening of March 25, WuXi XDC, a leading Chinese ADC CDMO company, released its first annual report since going public. During the reporting period, WuXi XDC achieved revenue of RMB 2.124 billion, representing a year-on-year increase of 114%; adjusted net profit reached RMB 412 million, up 112% year on year.

The financial reports of WuXi XDC and Tot Biopharm clearly demonstrate that deep specialization in the CDMO niche can also yield high performance returns.

Previously, the market generally believed that the era of high growth for domestic CDMOs had passed, but the ADC CDMO segment appears to be an exception, even within the WuXi ecosystem.

Whether it is WuXi AppTec, which has already released its annual report, or WuXi Biologics, whose 2023 revenue increased by only 11.6% year-on-year, both serve to corroborate the market view that the growth rate of the CDMO industry has slowed down. WuXi XDC’s impressive performance is attributable not only to the high prosperity of the ADC sector but also to its continuous efforts in building one-stop ADC CDMO service capabilities.

In 2023, WuXi XDC secured 50 new projects, bringing its total project portfolio to 143. This included 84 preclinical (pre-IND) projects, 38 Phase I projects, and 21 Phase II and III clinical projects, among which five were Process Performance Qualification (PPQ) projects. As of 2023, the company had served a cumulative total of 345 high-quality clients, including international pharmaceutical companies and innovative biotechnology firms, and had supported clients in submitting 55 Investigational New Drug (IND) applications.

With the addition of new projects and the advancement of existing projects to later stages, WuXi XDC’s pre-IND and post-IND service revenues reached RMB 927 million and RMB 1.197 billion, respectively, representing year-on-year increases of 143.20% and 96.47% compared to 2022, with strong expectations for future commercial growth. Furthermore, as of the end of 2023, the backlog order value grew by 82% to USD 579 million, laying a solid foundation for sustaining high-speed growth in the future.

Not only WuXi XDC, but also Tot Biopharm, another company fully committed to the ADC CDMO business, has achieved strong performance growth.

In 2023, Tot Biopharm’s CDMO business generated RMB 141 million in revenue, representing a year-on-year increase of 94%. Excluding the impact of non-recurring items, full-year revenue grew by 101% year-on-year, effectively doubling. Meanwhile, the growth rate of its CDMO business outpaced the industry average, demonstrating strong momentum. Of the 65 projects on hand, both revenue and project count from ADC programs rose to account for 65%. The company added 39 new projects throughout the year, including 30 ADC projects, and established long-term, stable collaborations with multiple biotech firms such as Akeso, Duality Biologics, Zhihe Biotechnology, Shijian Biopharma, and Yilian Biopharma.

Currently, among the ADC CDM projects developed by Tot Biopharm, four have successfully reached the pre-BLA (pre-Biologics License Application) stage, bringing the cumulative total to six pre-BLA projects and securing future commercial production. Tot Biopharm initially built its foundation on ADC drug development and strategically transformed to provide ADC CDMO services starting in 2020. In just three years, the company achieved annual revenue exceeding RMB 100 million and accumulated nearly 100 projects, demonstrating a precise capture of this emerging market opportunity.

In 2023, when the overall industry environment was sluggish, CDMO companies that could still maintain a 100% growth rate were rare. With the industrial development and upgrading, structural adjustments in the CDMO industry will be inevitable.

If leading enterprises have leveraged their first-mover advantage to address various weaknesses in line with the “wooden bucket theory” and thereby capture market share, then latecomers like Tot Biopharm have opted for a strategy of building strengths in specific areas to achieve breakthroughs in niche segments.

Winning orders through low pricing is not sustainable; specialized capabilities are the key to building lasting competitiveness.

If WuXi XDC benefits from the strong backing of the WuXi ecosystem, then Tot Biopharm’s counter-trend growth in the CDMO sector serves as a classic case study of how a latecomer can break through in the current domestic market environment.

As a pharmaceutical company, Tot Biopharm, like other domestic biotech firms, harbors a “Pharma dream,” making factory construction and capacity expansion an inevitable stage in its development. However, as the capital market has gradually cooled, this excess capacity has become a burden for the company. Whether to halt production, sell off the assets, or pivot to becoming a CDMO, each path presents significant challenges that need to be addressed.

At that time, as ADCs emerged as a new track, there were few CDMOs capable of providing related services. Tot Biopharm believed that a high-quality ADC service system had not yet been established in China, and its prior investments in ADC R&D offered certain differentiated advantages for its transition into a CDMO.

Tot Biopharm first gradually divested its self-developed pipeline, selling or discontinuing various assets, including the near-launch ADC product TAA013. The company then redirected its resources to focus on CDMO services, continuously expanding CDMO capacity while investing in the construction of R&D centers and ADC production lines.

Nowadays, the R&D center has been in operation since 2023. In terms of ADC production lines, Tot Biopharm already owns two ADC production lines and two antibody production lines; the annual bulk drug substance capacity for antibodies is 300,000 liters, with an annual finished product capacity of 20 million units; the annual bulk drug substance capacity for ADCs is 960 kilograms, with an annual finished product capacity reaching 5.3 million vials.

Since deciding to transform into a CDMO in 2020, Tot Biopharm’s CDMO revenue stood at merely RMB 6.42 million that year; by 2022, CDMO revenue had risen to RMB 72.54 million, representing more than a tenfold increase compared with 2020. In 2023, it grew another 94% year on year, reaching RMB 140 million. Just three years later, the transformed Tot Biopharm has become a key player in China’s ADC CDMO industry.

Tot Biopharm’s successful transformation is not an isolated case; a number of other companies are also targeting ADC CDMO as a key area for breakthrough.

Haoyuan Chemexpress, which initially focused on small-molecule drugs, was also one of the first companies in China to conduct research on ADC payload-linkers. It subsequently established an integrated CDMO service platform for ADC payload-linkers, providing related ADC CDMO services.

As of the first half of 2023, Haoyuan Chemexpress maintained an inventory of over 80 payloads and more than 400 linkers, accumulated experience in synthesizing over 1,000 payload-linker conjugates, advanced the R&D of multiple high-difficulty ADC small-molecule toxins, and completed the preliminary establishment of its ADC conjugation and testing platform. In the first half of 2023 alone, Haoyuan Chemexpress undertook more than 60 ADC projects and collaborated with over 570 clients, representing a year-on-year increase of 48.32%.

In 2023, the fourth new ADC production line commenced operations, significantly enhancing Haoyuan Chemexpress’s GMP manufacturing capacity for ADCs. As a result, the company achieved revenue of RMB 1.879 billion, representing a year-on-year increase of 38.36%. Furthermore, Haoyuan Chemexpress established its Chongqing subsidiary to build an integrated commercial platform for ADC antibody–linker conjugation and fill-finish processes, offering one-stop CDMO services covering the entire R&D and manufacturing lifecycle.

Another startup, Healsun Biopharm, completed a Series B+ financing round of nearly RMB 200 million in October 2023. The investor consortium included CMS, while Lepu Biopharma had also participated in its previous funding rounds. What attracted these investors was Healsun Biopharm’s persistent focus on the CDMO sector for large-molecule biologics and its continuous refinement of core competitive capabilities. In November 2023, Healsun Biopharm completed the upgrade of its ADC production facility, achieving an annual production capacity of up to 50 batches.

In 2023, Healsun Biopharm delivered over 350 ADC development projects. Its Hangzhou headquarters features proprietary, commercially licensable platforms for high-expression stable cell line development and process development, along with fully equipped GMP production lines for drug substance and drug product at 250 L and 500 L scales. Meanwhile, Healsun Biopharm plans to construct six 2,000 L commercial-scale production lines, which are expected to become operational in phases by the end of 2024.

No enterprise’s achievements can be separated from the opportunities bestowed by the times, and at this current juncture, antibody-drug conjugates (ADCs) represent the most powerful tailwind. Among the many contract development and manufacturing organizations (CDMOs) offering ADC services, although overall performance has declined, the ADC segment has generally made significant contributions. Leading CDMOs, including ASYMCHEM and PORTON, are also actively leveraging external resources to accelerate the expansion of their ADC production capacity.

The robust rise of ADC CDMOs has demonstrated that, in the face of macroeconomic uncertainty, only by maximizing strengths in niche segments and leveraging significant competitive advantages can companies deeply bind customers and navigate through market cycles.

Despite the interdependence between European and American markets and the risk of decoupling, Chinese CDMO companies continued to see growth in their European performance in 2023. For instance, WuXi Biologics’ revenue from the European market increased by 101.9% year-on-year; ASYMCHEM’s European revenue rose by 57.1%; Pharmaron’s European revenue grew by 24.4%; and even WuXi AppTec, which has faced significant pressure, saw its European revenue increase by 12% year-on-year.

Beyond the high-quality delivery of past orders, what attracts clients to continue their partnerships is the proactive strategic positioning of Chinese enterprises in emerging sectors. For instance, the global sales surge of semaglutide has directly ignited a rise in demand for peptide drug manufacturing and R&D services, enabling CDMOs with prior investments in this area to start securing orders.

Taking ASYMCHEM as an example, although its historically dominant small-molecule CDMO business grew by 25.6% year-on-year after excluding large orders, the more noteworthy development is the over 20% year-on-year growth in its emerging services. Among these, peptide/GLP-1-related businesses represent ASYMCHEM’s future strategic focus.

On one hand, ASYMCHEM is accelerating the expansion of its commercial-scale peptide production capacity, which is expected to reach 14,250 liters in the first half of 2024 to meet project demands. On the other hand, it is continuously strengthening its team’s delivery capabilities in analysis and separation/purification, which involve higher technical requirements in the peptide field. Meanwhile, in terms of new technologies, ASYMCHEM has embarked on research into efficient technological pathways such as liquid-phase synthesis, enzymatic synthesis, and hybrid approaches combining enzymatic and liquid-phase synthesis.

It is not only ASYMCHEM, but also companies including Nuotai Biology, Onbo Pharmaceutical, Sinopep, and Jiuzhou Pharmaceutical that are working to build their technical capabilities in peptide CDMO.

The surge in high-barrier niche sectors, such as antibody-drug conjugates (ADCs) and peptides, has, to some extent, presented new opportunities for contract development and manufacturing organization (CDMO) companies. For established players, building technical capabilities in these emerging niches, while leveraging their accumulated qualifications and collaborative experience from years in the industry, can rapidly unlock a second growth curve. For emerging small and medium-sized CDMOs, establishing distinctive competitive advantages in specific niches and integrating them into the collaborative industrial chain enables rapid co-growth with other enterprises. As the industry has matured, hardware costs and the engineer dividend have become largely homogeneous across competitors. Only those with sufficiently pronounced strengths can attract more partners and stand out during this period of industry adjustment.