Medical Companies in 2026 No Longer Need to Obsess Over IPOs

The just-concluded Qingming Festival holiday, though only three days long, still saw a “bustling” healthcare industry,Four Medical Companies Have Failed in Their IPOs, with a focus on medical aesthetics, early cancer screening, innovative medical devices, and IVD.

However, this is not a phenomenon unique to the recent period. As early as the end of last year, a “wave of IPO withdrawals” had already swept extensively across the healthcare sector and has continued to the present. According to incomplete statistics from VCBeat,Over the past four months, nearly 50 healthcare companies have successively “terminated” their IPOs。

This is undoubtedly a rare sight, yet analyzing the underlying reasons is not particularly difficult. The two most critical factors are none other than the overall cooling of the market and the tightening of IPO policies at the regulatory level. However, this is not the whole story. On a deeper level, new changes and trends within the healthcare industry are also hidden amidst this cold wave of collective IPO setbacks.

IPO "Meltdown"

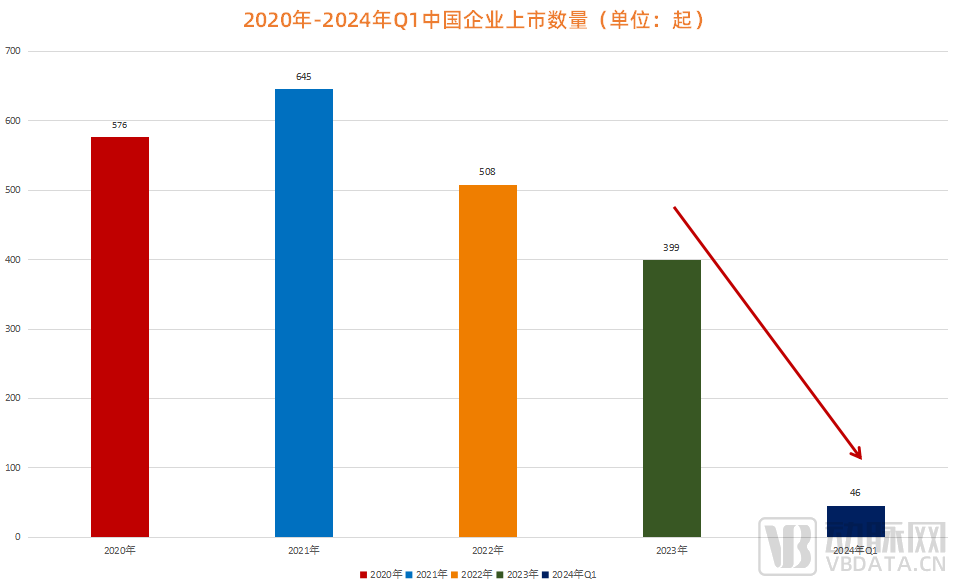

According to the statistical data from Zero2IPO Research Center,In the first quarter of 2024, 46 Chinese companies went public both domestically and overseas, representing year-on-year and quarter-on-quarter declines of 52.6% and 40.3%, respectively., with a total of 30 companies listed on the A-share market, representing year-on-year and month-on-month declines of 55.9% and 38.8%, respectively; meanwhile, 16 Chinese enterprises were listed in overseas markets, reflecting a year-on-year and month-on-month decrease of 44.8%.

Figure 1. Number of Chinese Enterprises Listed from 2020 to Q1 2024 (Data Source: Zero2IPO Research; Chart by VCBeat)

Figure 1. Number of Chinese Enterprises Listed from 2020 to Q1 2024 (Data Source: Zero2IPO Research; Chart by VCBeat)

Behind the sharp contraction in the number of IPOs lies the reality that a large number of companies have had their paths to public listing cut off. It is reported that,In the first quarter of 2024, 80 companies chose to voluntarily withdraw their filing materials, including as many as 23 healthcare and medical enterprises., with a primary focus on innovative drugs and the IVD sector.

Starting with in vitro diagnostics (IVD), which has been the “hardest-hit area” for IPO withdrawals, since Kangwei Century’s successful listing in October 2022,Over the past year and a half, no IVD company has listed on the A-share market.. Meanwhile, the IPO listings of nearly 16 IVD companies have been terminated in succession, with the most recent case occurring on April 8, when an IVD company voluntarily withdrew its IPO application from the STAR Market.

In fact, the main reason why IVD companies have fallen under the “IPO curse,” with zero listings over a period of 18 months, is their earnings instability. As is well known, the core businesses of IVD companies are largely closely tied to the pandemic. As the impact of the pandemic has gradually waned, demand for related testing has dropped significantly, leading to a precipitous decline in overall revenue. In this regard, an investor remarked, “Market gains driven by fortuitous events are not competitive. As the industry returns to its normal trajectory, the initial windfall will quickly transform into pressure on the company’s future performance, given that neither regulators nor the market look favorably upon companies that experience a sharp deterioration in performance shortly after their IPO.。”

Unlike IVD,The primary obstacle to the market launch of innovative drugs is their lack of profitability, meaning they are either operating at a loss or have not yet commercialized any products.. Taking as an example a certain innovative drug company that recently withdrew its marketing application, although it possesses multiple star pipelines and has completed Phase III clinical trials for several candidates and submitted New Drug Applications (NDAs) to the National Medical Products Administration (NMPA), none have yet been approved for market launch; consequently, no commercial production or sales activities have been initiated.

In this regard, a senior investor remarked, “Given the generally high technical barriers of innovative drugs, investors have correspondingly shown considerable tolerance. However, as time goes on,”Especially as the capital winter intensifies,Investor pressure has also mounted, necessitating a focus on the ‘financial statements’ of innovative drug companies and their ‘timelines’ for future profitability.“This means that it is now virtually impossible for innovative drug companies to ‘launch their products while still addressing unresolved issues.’”

Therefore, it is not difficult to see that, against the backdrop of tighter IPO regulations, healthcare professionals are increasingly concerned about “capital.” Consequently, since 2023, healthcare companies have been fiercely competing to boost their revenue. This trend is particularly evident in the innovative drug sector, where a review of numerous annual reports from the past two years clearly reveals thatTo present robust financial statements, Chinese pharmaceutical companies have largely converged on a consistent strategy: cost reduction, efficiency enhancement, and focus.。

“Cost reduction” is straightforward, encompassing measures such as layoffs, plant closures, and pipeline cuts. “Efficiency enhancement,” in this context, primarily refers to the development of new business growth curves. For instance, a large number of pharmaceutical companies have concentrated on lucrative, fast-return sectors—such as medical aesthetics and weight-loss treatments—in recent years, with many successfully establishing these as their second growth curve for revenue. Lastly, “focus” is more direct, referring to innovative drug companies concentrating on their core businesses to accelerate R&D and market commercialization.

The medical device sector is certainly no exception; however, its approach to generating cash flow differs slightly, with a particular emphasis on “global expansion.” According to authoritative statistical data,The overseas revenue of A-share listed medical device companies in China has rapidly increased from RMB 25.7 billion in 2018 to RMB 108.1 billion in 2022, with a compound annual growth rate (CAGR) of 43.2%.。

Furthermore,Transitioning into a “platform company” is also a major strategy for monetizing medical devices.In this regard, a medical device investor remarked, “Medical device products are inevitably affected by centralized procurement, which means you cannot rely on a single product to dominate the market. It is essential to have other innovative products to sustain high profit margins. This is precisely why investors currently favor platform-based companies.”

Therefore, an objective fact lies before all healthcare professionals:“The era of burning cash” has largely come to an end, and the entire healthcare industry is now striving aggressively to generate revenue, driven by an unprecedented momentum.。

IPO Is No Longer the Only Option

A senior healthcare investor told VCBeat, “"If a portfolio company approaches us now expressing interest in being acquired, we would be very welcoming of such an opportunity."”. Extending this logic further, namelyInvestors are no longer passively waiting for IPOs; instead, they have widely adopted a flexible “exit whenever possible” strategy.。

This is certainly attributable to capital market dynamics. Although going public remains the optimal choice for maximizing returns, in an environment where IPO channels are narrowing, investors who continue to rely heavily on IPOs at this stage are essentially engaging in a futile struggle. In the future, they are highly likely to face cutthroat competition within a constrained space.

Beyond this, significant changes across the entire healthcare industry are also indirectly driving investors to no longer view initial public offerings (IPOs) as the sole exit strategy. From an industry perspective, taking the innovative drug sector as an example, over the next five to ten years, more than a thousand domestic innovative pharmaceutical companies will undergo natural selection through upgrades, transformations, mergers, and acquisitions. Consequently, the proportion of companies that can truly stand out by going public will continue to shrink.

From a transactional perspective, on March 15, 2024, the China Securities Regulatory Commission (CSRC) formulated and issued the policy document “Guiding Opinions on Strengthening the Supervision of Listed Companies (Trial),” which explicitly supports listed companies in enhancing their investment value through mergers, acquisitions, and restructurings. Coupled with the rapid development of the healthcare industry in recent years and the gradual improvement of its industrial chain, the exit market—represented by mergers and acquisitions—has become increasingly mature, leading to a widespread surge in transaction activities.According to statistics from Zero2IPO Research, domestic IPOs in China fell by 13% year-on-year from January to October 2023, while mergers and acquisitions rose by 29.9% year-on-year.。

In this regard, a senior investor stated, “At present, if healthcare enterprises can actively prioritize cash flow, engage in diversified collaborations, and optimize their pipelines and asset allocation, this will undoubtedly be a crucial strategy for achieving sustainable operations at this stage. However, if none of these paths prove viable, exiting the market at an appropriate time may well be a prudent choice. From an industry perspective,”Integrating innovative projects with low viability into established enterprises can not only mitigate talent loss to a certain extent but also accelerate the metabolic turnover of the entire industrial ecosystem.。”

In other words,For the vast majority of healthcare companies today, maintaining a position that allows for either an IPO or, alternatively, business development (BD) partnerships or acquisition, is in fact the optimal strategy.。

Certainly, pursuing an initial public offering (IPO) is not out of the question if deemed necessary; however, it requires adopting the right approach. The selection of the listing venue, in particular, is critical. Over the past one to two years,The Beijing Stock Exchange, which is currently attracting significant attention, may be a promising listing target.On September 1, 2023, the Beijing Stock Exchange (BSE) officially released the “19 Measures for Deepening Reform,” explicitly allowing high-quality small and medium-sized enterprises (SMEs) that already meet listing requirements to conduct initial public offerings (IPOs) and list on the BSE, provided they align with the exchange’s market positioning. In short, amid rising IPO thresholds in the Shanghai and Shenzhen stock markets as well as overseas markets due to various factors, the BSE has emerged as a new listing option for a large number of innovative SMEs, characterized by its high inclusivity, compact and controllable timelines, and rapid review process.

In fact, the Beijing Stock Exchange already has numerous successful cases, includingJinbo Biopharm, Xinghao Pharma, Boxun Bio, Wuxi Jinghai, Heyi Pharmaceutical, Xin Ganjiang PharmaceuticalMedical companies such as these all successfully listed on the Beijing Stock Exchange in 2023, and their stock prices have shown an upward trend. Taking Jinbo Bio, a developer of collagen-based products, as an example, its share price reached RMB 226.84 on April 8, 2024, representing a 362.93% increase from its issue price of RMB 49. This performance is particularly remarkable amid the current capital winter.

Figure 2. Stock Performance of Selected Medical Companies Listed on the Beijing Stock Exchange in 2023 (Source: Public Information)

Figure 2. Stock Performance of Selected Medical Companies Listed on the Beijing Stock Exchange in 2023 (Source: Public Information)

In addition, ““Pivoting to the Hong Kong Stock Exchange” has also become a major breakthrough trend in the healthcare sector this year.. According to incomplete statistics, there have already beenHuahao Zhongtian, Taimei Medical, Lu Daopei Medical, iFlytek Medical, Tongyuankang Pharma, Health 160, Jiuyuan Gene...and other medical enterprises are making a sprint toward listing on the Hong Kong Stock Exchange.

A key reason for this is that the Hong Kong stock market’s “Chapter 18A listing requirements” allow pre-profit biotechnology companies to go public. In March 2023, the Hong Kong Stock Exchange further introduced the “Chapter 18C” listing rules, providing listing and financing opportunities for five categories of specialized and innovative technology companies that are not yet commercialized or are in the early stages of commercialization. This holds significant appeal for current innovative drug enterprises. According to Wind data, seven biotechnology companies newly listed on the Hong Kong stock exchange in 2023 under the Chapter 18A listing requirements, all of which reported net losses in 2022.

In retrospect, after the broader market cooled down, whether to persist with an IPO or to exit gracefully, the core strategy is to make flexible choices based on one’s own circumstances and market dynamics. For healthcare professionals, this is essentially the optimal “exit path.”

How Many More IPOs Can Healthcare Companies Achieve?

On March 15, 2024, the China Securities Regulatory Commission (CSRC) consecutively released four policy documents, once again signaling its regulatory stance of “strengthening fundamentals and foundations” and “strict supervision and regulation.” This implies that the IPO market will generally continue its trend of phased contraction, making the path to public listing even more challenging for healthcare companies.

However, this should not be viewed simply as a “bad thing”; from the perspective of seasoned investors, “A significant part of the significance of cold lies in ecological evolution.”

In this regard, he added, “The winter in the secondary market has, in fact, cleared out a significant portion of non-professional and non-industrial capital, as well as many healthcare projects with uncertain commercialization prospects. In the post-trial industry ecosystem, project owners will adopt more objective valuations and place greater emphasis on the innovativeness of their R&D pipelines, clinical value, and the progress and prospects of commercialization. Meanwhile, investment institutions will act more rationally, deepening their understanding of technological products, including the cyclicality and risk implications inherent to the healthcare industry. Isn’t this a positive signal that the healthcare industry is entering a new stage?”

Following this logic, healthcare professionals may need to return more to the essence of medical practice. Taking enterprises as an example, they must first accurately identify current unmet clinical needs; second, based on this foundation, they must continuously deepen their efforts and adhere to original innovation; finally, they need to balance R&D and marketing, prioritize cash flow, and possess the critical ability to deliver results on schedule.

Furthermore, as “co-founders,” investors must also step out of their comfort zones during industry downturns, standing shoulder to shoulder with their portfolio companies to jointly address the most pressing challenges at hand. This may include providing financing support, collaborating on strategic planning, executing marketing initiatives, and even assisting with workforce reductions to cut costs and increase revenue.

From a broader perspective, against the backdrop of deepening global expansion and import substitution, China’s future healthcare market will increasingly favor domestically produced enterprises with global competitiveness. Therefore, rather than merely observing the slump in the secondary market, we are witnessing the dawn of a new era and the rise of a new industry. This landscape presents both significant opportunities and formidable challenges.

1. “VC/PE Can No Longer Wait for IPOs” – FOFWEEKLY;

2. “Further Cooling! IPO Access Tightens in Q1” – Zero2IPO Research;

3. “After A-Share IPO Setbacks, Pivoting to Hong Kong! Strong Interest Among Such Enterprises in Listing in HK” — Securities Times China.