White Paper on Neurosurgical Medical Devices (2023 Edition) Officially Launched

Preface

“This white paper systematically explores the innovation and development of neurosurgical medical devices, introducing a series of globally leading new technologies and products in neurosurgery. It aims to enhance surgical precision, mitigate risks in neurosurgical diagnosis and treatment, and provide valuable references for optimizing neurosurgical care pathways.”

December 2023

Recommended Institutions

From the perspective of capital markets, reviewing and studying industry-related materials is a crucial approach for conducting industry assessments, making investment decisions, and uncovering corporate value. The "White Paper on Neurosurgical Medical Devices" provides an in-depth exploration of the current landscape and future development trends of medical devices in the field of neurosurgery. It serves as a valuable reference for investors, medical device manufacturers, and healthcare institutions within the industry, offering critical insights for capital markets to grasp the direction of industry development. This document is a rare and invaluable resource for industry research.

Neurosurgery stands as a vital vessel in the grand course of modern medical history. Emerging from the distant horizon, it has navigated through the bustling currents of progress, carrying with it the rich discourse of diverse schools of thought. With great anticipation and forward-looking vision, we hereby present this white paper, hoping that its value will be fully realized and that it will shine brightly through the ages.

—Li Tianyu

Guosen Securities Co., Ltd. Investment Banking Division

Member of the Party Committee, General Manager of the Healthcare Business Headquarters

The release of the White Paper on Neurosurgical Medical Devices (2023 Edition) provides directional guidance for professionals in the neurosurgery industry, representing a valuable and meaningful contribution to the field. Objective, rational, and high-quality industry research reports can enhance the quality of strategic decision-making, thereby indirectly promoting industrial development and progress. The advancement of neurosurgical medicine relies on the joint efforts of clinicians, research institutes, and medical device companies. We extend our sincere appreciation to the Innovation and Translation Branch of Neurosurgery under the China Health Care Association for the Elderly and VCBeat for their contributions.

Legend Capital looks forward to working with industry partners to jointly drive technological innovation in neuroscience-related fields, promote industrial progress and social development, and make unremitting efforts to alleviate the suffering of patients.

——Wang Jianfei

Legend Capital, Managing Director

The release of the “White Paper on Innovative Development in the Neurosurgical Medical Device Industry” has had a highly positive impact on the sector. Innovation in neurosurgical medical devices is not merely about technological advancement; it also reflects the assumption of responsibility within the healthcare industry. We must continuously strive for more precise and safer treatment solutions to provide better medical services to patients.

As a professional healthcare investment firm, Danlu Capital has long focused on innovative products in the field of neuroscience. We hope this white paper will serve as a starting point for our collective efforts, providing guidance and momentum to promote the healthy development of the neurosurgical medical device industry.

——Liang Qiao

Danlu Capital, Investment Director

Crafted with the collective expertise of over 30 neurosurgery specialists from across China

Highlights and Insights of the White Paper

1. The First Panoramic Insight and Innovation Analysis of Neurosurgical Medical Devices in China.

2. An in-depth industry report, compiled over six months, that consolidates the academic achievements of numerous domestic neurosurgery experts and integrates multi-faceted research spanning clinical practice, industry, scientific research, and capital investment.

3. Five Major Sections: A Systematic Review of the Current Development, Innovation Progress, and Frontier Breakthroughs in China’s Neurosurgical Device Sector.

Part I: The Evolutionary Trajectories of East and West, Exploring the Future Path of Neurosurgical Medical Devices

1.1 Development History of the Neurosurgery Industry Globally and in China

The development of neuro-medical devices has undergone a century-long evolution, encompassing two key periods: from the late 19th century to the late 20th century, and since the early 21st century. From the late 19th century to the late 20th century, the emergence of specialized neurosurgical instruments and the nascent forms of cranial nerve stimulation devices laid the foundation for the growth and expansion of this field. Since the 1980s, China’s neurosurgery sector has experienced robust development, actively assimilating the essence of internationally leading technologies.

1.2 Development Environment for Neurosurgical Medical Devices

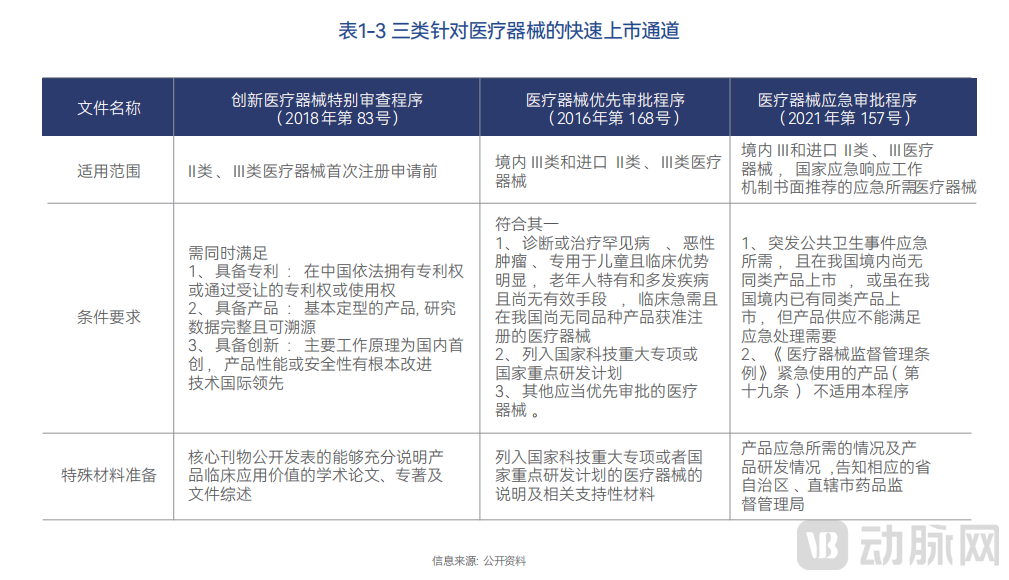

Regulatory Aspects. In terms of approval, China has successively introduced three fast-track pathways for the market launch of medical devices in recent years. The Special Review Procedure for Innovative Medical Devices provides a “green channel” for devices with high innovation and technical value; the Priority Review Procedure for Medical Devices offers a “green channel” for devices in short clinical supply; and the Emergency Review Procedure for Medical Devices establishes a “green channel” for devices required to address urgent public health needs. According to the 2022 Annual Report on Medical Device Registration released by the National Medical Products Administration (NMPA), the NMPA approved 55 innovative medical device products for market launch, representing a 57.1% increase compared to 2021. From 2014 to 2022, the NMPA approved a total of 189 innovative medical devices. Among these, domestically produced innovative medical devices involved 134 enterprises across 15 provinces, while imported innovative medical devices involved eight enterprises from two countries. Regarding market access, the Opinions of the National Development and Reform Commission and the Ministry of Commerce on Several Special Measures to Relax Market Access Restrictions for Shenzhen in Building a Pilot Demonstration Area of Socialism with Chinese Characteristics, issued in January 2022, explicitly mentioned relaxing market access restrictions for medical devices. These measures allow the acceptance of registration test reports for medical devices issued by certain third-party testing institutions and support the promotion of real-world data applications to accelerate the market launch of new products.

**Funding Support.** In October 2013, the *Several Opinions of the State Council on Promoting the Development of the Health Service Industry* pointed out that R&D and industrialization in fields such as medical devices should be supported through relevant construction funds and industrial funds. In December 2017, the *Three-Year Action Plan for Enhancing the Core Competitiveness of the Manufacturing Industry (2018–2020)* proposed increasing financial input to support the implementation of projects in manufacturing sectors, including medical devices. Under consultation between fund management institutions and project entities, funds such as the Advanced Manufacturing Industry Investment Fund can be actively utilized to support the development and industrialization of innovative products.**Medical Insurance Coverage.** In August 2018, the National Development and Reform Commission (NDRC), in its *Letter in Response to Proposal No. 437 (Economic Development Category No. 360) of the First Session of the 13th National Committee of the Chinese People’s Political Consultative Conference*, stated that registration management and regulatory systems for medical devices and other fields should be improved, and new insurance payment mechanisms should be explored to optimize the innovation environment and accelerate industry development.**R&D Support.** In September 2020, the NDRC, in its *Response to Proposal No. 9407 of the Third Session of the 13th National People’s Congress*, mentioned that significant tax incentives would be granted to key industrial projects introduced during the 14th Five-Year Plan period. These measures include reducing the corporate income tax rate to 15% for certified high-tech enterprises, raising the additional deduction ratio for enterprise R&D expenses to 75%, and removing restrictions that previously prohibited the additional deduction of R&D expenses entrusted to overseas entities. Such tax reduction and fee-cutting measures aim to support R&D in industries such as high-end medical devices.

Part II: Market Overview—Unveiling the Competitive Landscape and Commercial Prospects of Neurosurgical Medical Devices

2.1 Estimation of the Global and Chinese Market Size for Neurosurgical Medical Devices

● Imaging Equipment

Since 2016, the global market size for medical imaging equipment has continued to grow at an annual rate of approximately 3%, reaching USD 43 billion in 2020. By 2030, the global market size for medical imaging equipment is projected to exceed USD 60 billion. In China, although the medical imaging equipment sector is less mature than its overseas counterparts, it has experienced more rapid growth driven by increasing clinical demand and favorable policy support. In 2022, the total market size for medical imaging equipment in China reached approximately RMB 58.5 billion. Over the next five years, the overall market is expected to maintain a compound annual growth rate (CAGR) of over 7%, with the market size projected to surpass RMB 100 billion by 2029. By product category, CT holds the largest share, accounting for approximately 32% of the market, followed by X-ray (XR) systems at around 23%. Ultrasound and MRI rank next, capturing 19% and 17% of the market share, respectively.

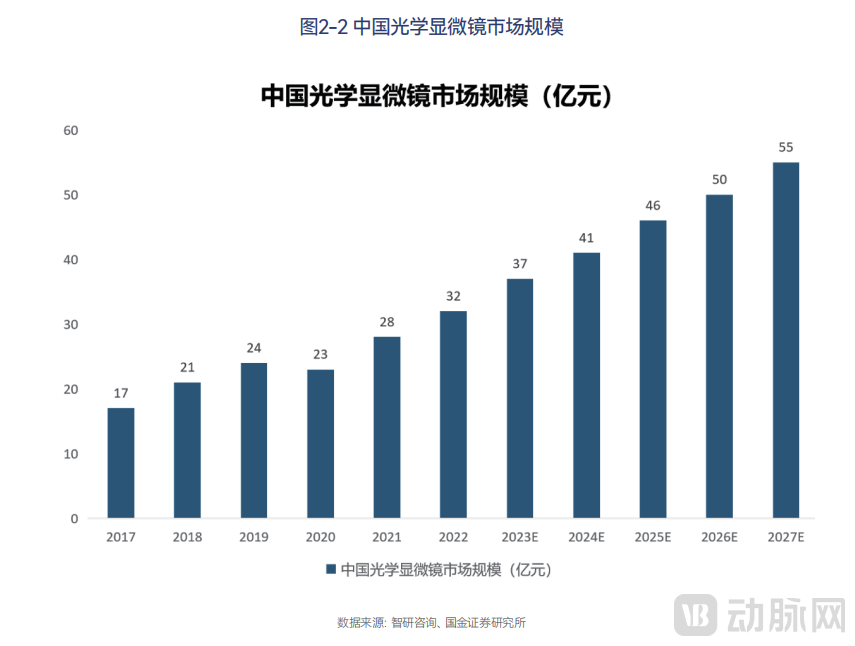

● Optical Microscope

Surgical microscopes are optical microscopes specifically designed for use in surgical environments and are now widely employed in neurosurgery, ophthalmology, dentistry, oncology, urology, and other fields. Neurosurgical microscopes are a specialized type of surgical microscope particularly suited for procedures involving the brain, spinal cord, and spine. The application of surgical microscopes in neurosurgery emerged slightly later than in otology and ophthalmology. According to QYResearch statistics, the global market size for surgical microscopes was approximately USD 2 billion in 2022 and is projected to exceed USD 3 billion by 2027. In comparison, the domestic market size for optical microscopes in China was around RMB 3.2 billion in 2022 and is expected to reach RMB 5.5 billion by 2027. Although China has gradually become a global manufacturing hub for optical microscopes since the 1970s and 1980s, domestic manufacturers currently have limited capacity for producing high-end microscopes, with the premium market still dominated by foreign companies.

● Medical Endoscope

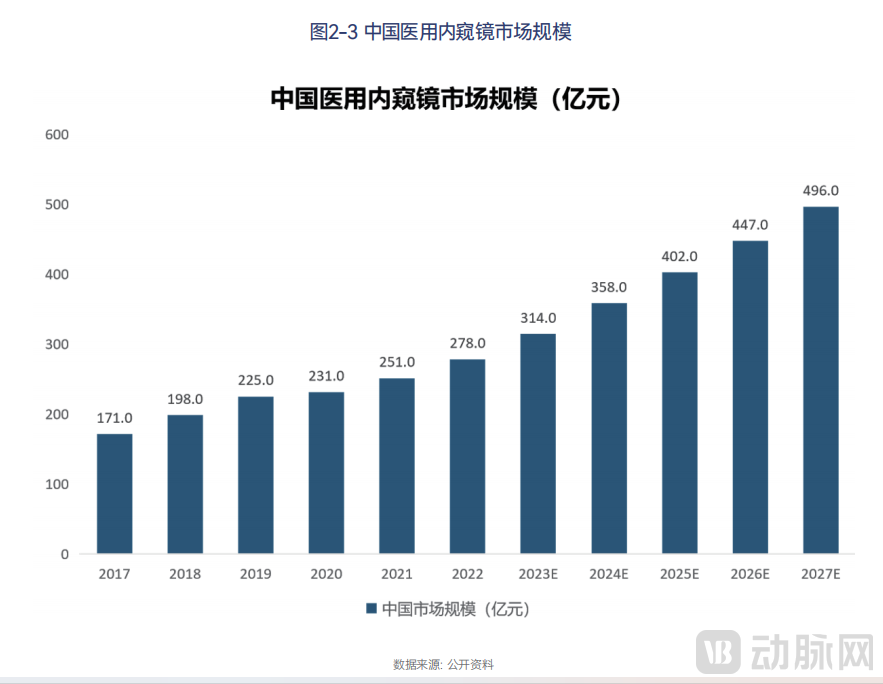

Medical endoscopy systems play a pivotal role in the healthcare sector. Clinically, endoscopes are primarily used for both diagnosis and treatment. For diagnostic purposes, physicians can utilize endoscopes to visualize internal structures or obtain biopsy samples from lesions for pathological analysis. For therapeutic purposes, endoscopic systems enable specific surgical procedures or assist in the implantation of therapeutic medical devices. Against the backdrop of supportive policies, an accelerating aging population, and rising per capita healthcare expenditures, both the global and Chinese medical endoscopy markets have experienced significant growth. In 2017, the global endoscopy market size was approximately USD 12 billion; by 2023, it is projected to reach around USD 17.2 billion, representing a compound annual growth rate (CAGR) of 7.25%. In comparison, although the domestic endoscopy market started later, it has developed rapidly, with a CAGR exceeding 10% in recent years, surpassing the global growth rate. Specifically, the size of China’s endoscopy market was approximately RMB 17.1 billion in 2017 and is expected to approach RMB 50 billion by 2027.

Endoscopes have extensive clinical applications. Among the major products categorized by medical specialty, neuroendoscopes account for a relatively small share. Statistics indicate that neuroendoscopes represent approximately 10% of the overall market size for medical endoscopes, with the market value reaching around RMB 3 billion in 2022.

● High-value consumables for neurosurgery

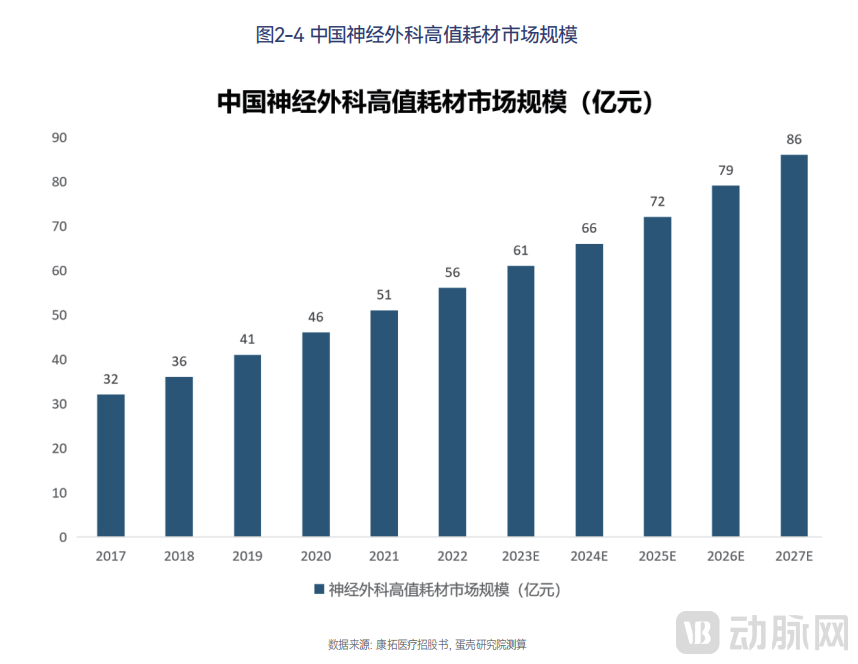

With the introduction of advanced overseas imaging equipment, neurosurgery has entered a period of rapid development, driving swift growth in the market size of high-value consumables used in this field. High-value neurosurgical consumables primarily include cranial materials, dural materials, drainage and suture materials, neuromodulation and electroencephalogram (EEG) monitoring materials, and related auxiliary tools. According to data from Evaluate Medtech, the global market size for neurosurgical medical devices is projected to reach $15.8 billion in 2023. Focusing on China, the market size for neurosurgical consumables reached approximately RMB 5.6 billion in 2022, with the cranial repair materials segment accounting for around RMB 1.5 billion and the artificial dura mater (spinal) membrane segment reaching approximately RMB 1 billion. By 2027, the market size for high-value neurosurgical consumables is expected to approach RMB 10 billion. The market for high-value neurosurgical consumables is relatively mature. In the future, the neurosurgery market will continue to grow, driven by the ongoing optimization and broader adoption of neurosurgical procedures across different tiers of healthcare institutions in China, upgrades in high-value consumable materials—such as the replacement of titanium with PEEK (polyether ether ketone) and synthetic materials with animal-derived ones—and rising consumer expenditure on medical care.

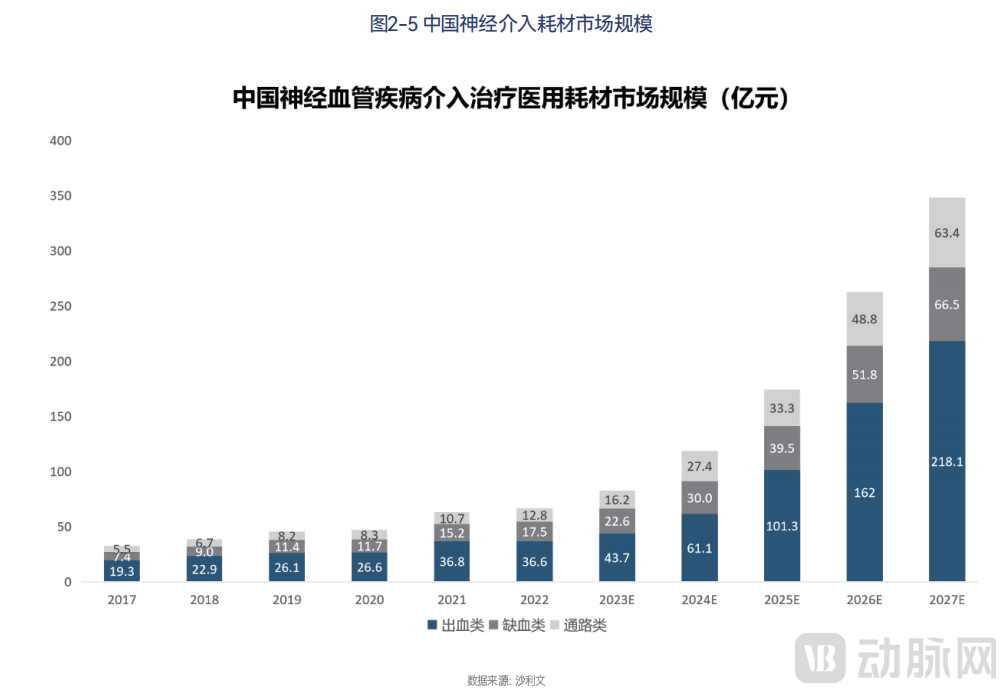

● Neurointerventional Consumables

In 2022, the market size of interventional consumables for neurovascular diseases reached RMB 6.68 billion, among which the market size for hemorrhagic neurointervention was RMB 3.68 billion, for ischemic neurointervention was RMB 1.75 billion, and for access devices was RMB 1.28 billion. By 2027, the neurointerventional market is projected to reach RMB 35 billion, with hemorrhagic neurointervention accounting for the largest share at approximately 62%, while ischemic and access device segments will have similar market sizes, accounting for around 20% and 18% respectively, with compound annual growth rates exceeding 30%. The rapid growth of the neurointerventional market is attributed to the rising incidence of stroke in China, the increasing number of neurologists, enhanced patient health awareness, and continuous innovation in domestically produced medical devices. However, the development of the neurointerventional industry also faces a series of challenges, such as price reduction pressures from centralized procurement policies, stringent requirements for manufacturers due to high technical barriers, and the first-mover advantage and strong influence of overseas giants in the industry.

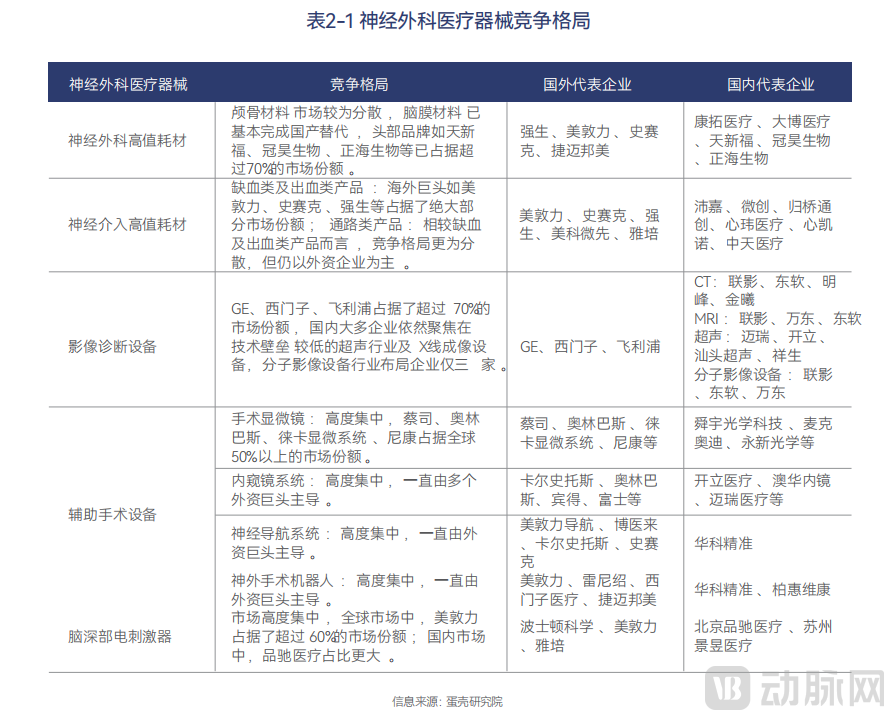

2.2 Competitive Landscape of Neurosurgical Medical Devices and Analysis of Representative Companies

Overall, the market for high-value neurosurgical consumables and medical devices is highly concentrated. In the field of neurointerventional consumables, overseas giants such as Medtronic, Stryker, and Johnson & Johnson dominate the majority of the market share. Compared to hemorrhagic and ischemic neurointerventional procedures, the competitive landscape for access-related neurointerventional products is relatively fragmented, although foreign companies still remain the primary players. Among imaging equipment, the localization rate of CT scanners continues to rise; however, domestic products are mainly focused on mid-to-low-end configurations, and there remains a certain gap between Chinese manufacturers and their overseas counterparts in the production of high-end models. In contrast, ultrasound equipment has achieved the highest localization rate, with domestic substitution largely realized. Currently, domestic manufacturers such as Mindray, Sonoscape, and Shantou Institute of Ultrasonic Instruments have secured significant market shares by leveraging the high cost-performance ratio of their products, and they have also achieved notable success in overseas markets.

A similar trend is observed in the field of auxiliary surgical equipment. In the rigid endoscope market, Karl Storz holds a market share of over 30%, firmly securing the top position. Due to higher technical barriers, the flexible endoscope market is predominantly monopolized by Japanese brands, with Olympus, Pentax, and Fujifilm collectively accounting for more than 80% of the market share. In the field of neurosurgery, Karl Storz is the primary supplier of endoscopes.

Part III: Comprehensive Overview of Medical Devices—An Analysis of Device Development Across Neurosurgery Subspecialties

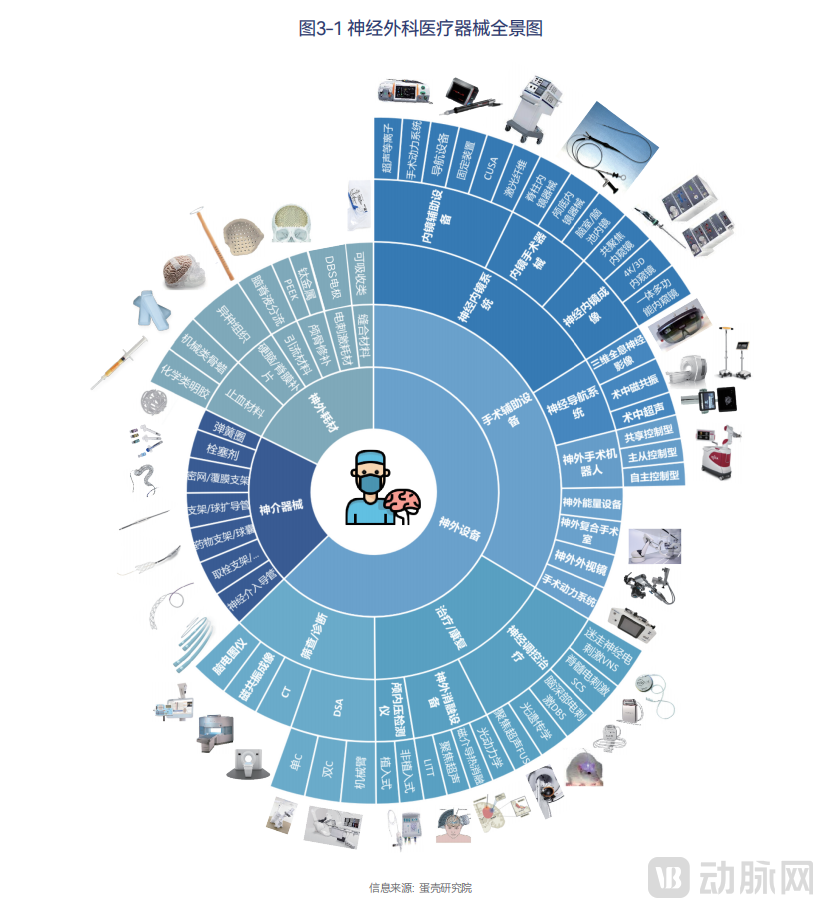

3.1 Overview of Neurosurgical Medical Devices

Neurosurgical medical devices refer to a series of specialized tools and equipment used for the diagnosis, treatment, and management of nervous system diseases.

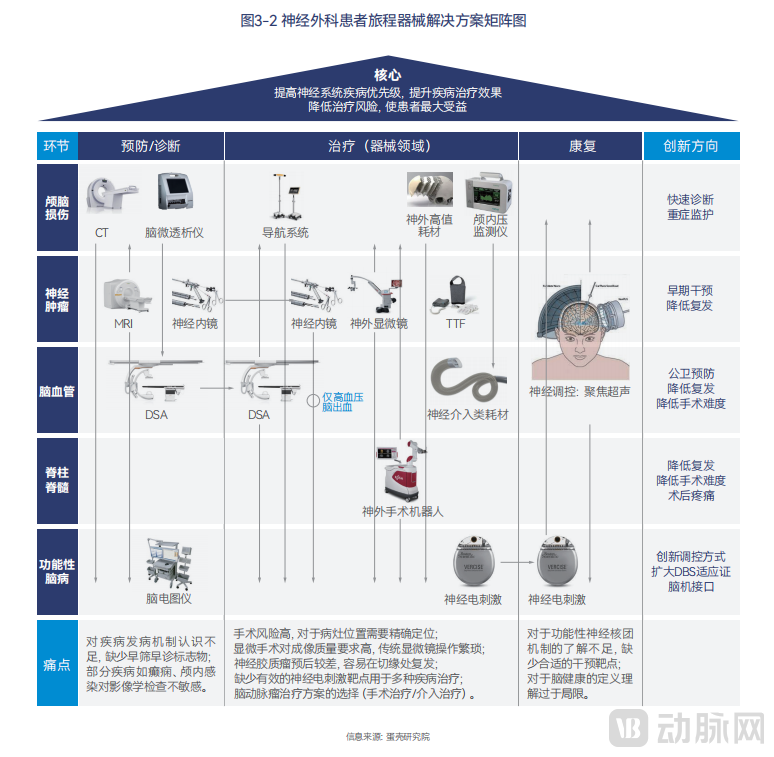

Indications for neurosurgery encompass five categories: traumatic brain injury, neurological tumors, cerebrovascular diseases, spinal and spinal cord disorders, and functional brain disorders. The patient journey varies depending on the specific indication. For instance, in cases of traumatic brain injury, the patient journey may include acute trauma management, imaging assessment, surgical intervention, and rehabilitation. For patients with neurological tumors, the journey involves tumor diagnosis, surgical planning, resection, and postoperative treatment. Patients with cerebrovascular diseases may undergo stroke diagnosis, vascular repair surgery, and rehabilitation. Those with spinal and spinal cord disorders typically experience spinal surgery followed by postoperative physical therapy. For functional brain disorders, the treatment journey generally includes evaluation, neuromodulation therapy, and rehabilitation.

3.2 Neurosurgical Medical Devices

● Digital Subtraction Angiography (DSA)

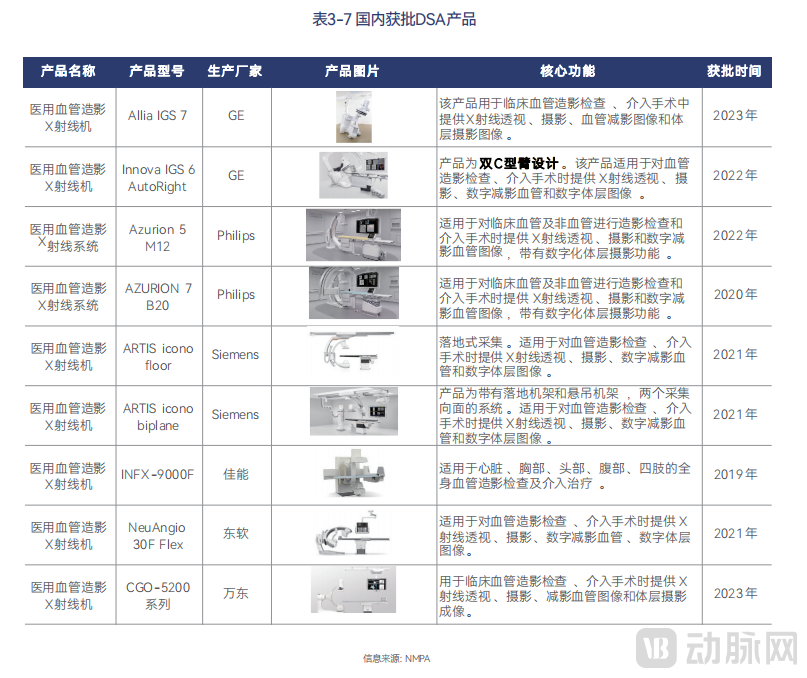

Digital Subtraction Angiography (DSA) consists of subsystems such as an X-ray generation system, image acquisition and processing system, C-arm and catheter table, and control devices, which are interconnected via a computer communication system to form a local area network. Based on the number of C-arms and the level of automation, DSA equipment can be classified into single-C, dual-C, and robotic arm systems; according to the C-arm mounting method, it can be further divided into ceiling-mounted and floor-mounted types. Among these, biplane systems significantly enhance 2D and 3D imaging and are specifically designed for neuroradiology and abdominal imaging, although they entail high installation costs. Ceiling-mounted DSA systems can be categorized into rail-mounted, free-moving (rail-free), and dual-isocenter ceiling-mounted types. Their advantages include a clean floor layout, a large range of motion, and greater C-arm arc depth, but they have relatively higher requirements for the facility. Floor-mounted DSA systems allow for the selection of the number of mechanical axes of movement based on needs and have relatively lower facility requirements, making them more suitable for retrofitting existing examination rooms. Robotic arm systems, represented by Siemens’ ARTIS pheno (as shown in Figure 3-8), are commonly used in hybrid operating rooms.

Due to the high technical barriers associated with Digital Subtraction Angiography (DSA), domestic brands have relatively weak competitiveness, and the market has remained heavily reliant on imports. Meanwhile, the high costs of purchasing and maintaining imported equipment mean that DSA is currently primarily used for interventional diagnosis and treatment in large, top-tier hospitals. Against the backdrop of increased investment in primary healthcare, DSA is experiencing rapid development in secondary hospitals, such as county-level hospitals. In this favorable environment, domestically produced DSA systems are gradually emerging; for instance, Neusoft’s NeuAngio 30 series, Wandong’s CGO-5200 series, and DSA systems from brands such as Weimai and Lepu have received approval from the National Medical Products Administration (NMPA) for market launch.

3.3 Neurosurgical Medical Consumables

Neurosurgical medical consumables mainly consist of six categories: cranial products, dural patches, hemostatic products, sutures, cerebrospinal fluid drainage catheters, and electrical stimulation products (as shown in Figure 3-18). Overall, China’s high-value neurosurgical consumables sector started relatively late and still exhibits a significant technological gap compared with imported brands. In terms of market size, the current market for high-value neurosurgical medical consumables in China is estimated at over RMB 6 billion.

From the perspective of the competitive landscape of neurosurgical medical consumables, the concentration in each sub-segment is currently high, with the majority of market share held by a few manufacturers. However, in China’s market for high-value neurosurgical medical consumables, import substitution has been achieved only in the artificial dura mater segment (where domestically produced products have attained an 80% market share, essentially realizing localization), while other segments remain dominated by imported products with a low level of import substitution. Therefore, overall, most sub-segments of China’s high-value neurosurgical consumables market hold significant growth potential.

3.4 Neurointerventional Consumables

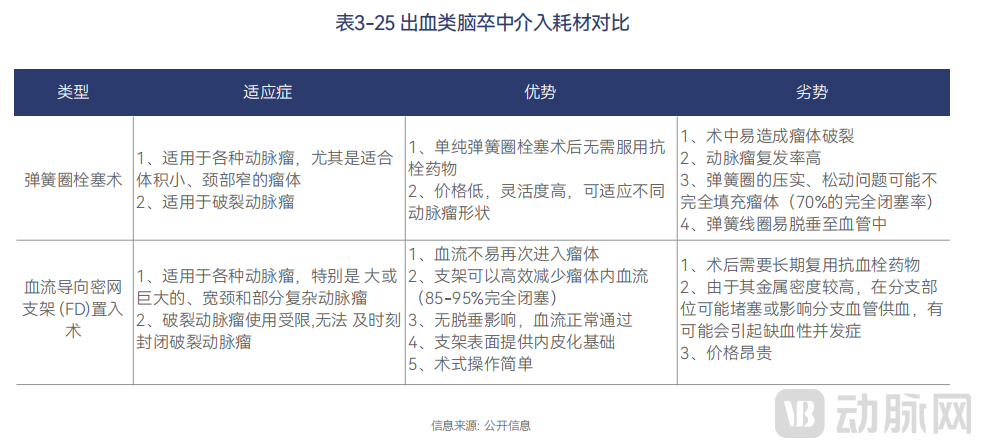

Neurointerventional medical devices (consumables) mainly comprise three categories: hemorrhagic devices, ischemic devices, and access devices. Hemorrhagic devices primarily include coils, flow diverters, covered stents, and liquid embolic agents. Ischemic devices mainly encompass intracranial angioplasty stents, intracranial angioplasty balloons, stent retrievers, and aspiration catheters. Access devices primarily consist of guiding catheters, balloon-guided catheters, distal access catheters, long and short sheaths, microcatheters, and microwires; these devices form the foundation for performing neurointerventional procedures.

In the treatment of hemorrhagic stroke, coil embolization and flow diversion are currently the more common technical approaches, each with its own optimal indications. Coils offer advantages in terms of cost and compliance, whereas dense-mesh stents demonstrate significant benefits in aneurysm occlusion, prevention of aneurysm recurrence, and endothelialization.

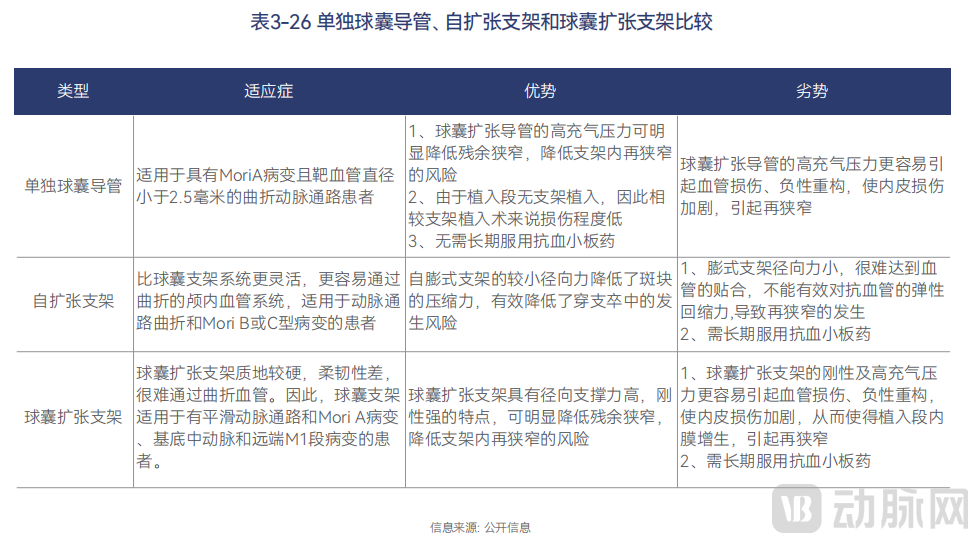

For intracranial atherosclerotic stenosis, standalone balloon angioplasty catheters, intracranial self-expanding stents, and balloon-expandable stents are the primary treatment options. Each of these three approaches has its own advantages and disadvantages.

For acute ischemic stroke, the currently common interventional approaches are stent retrievers or aspiration thrombectomy systems. Stent retrievers offer lower technical difficulty in thrombus removal but carry a higher risk of distal embolization. Aspiration thrombectomy, with its high suction power, minimizes the risk of fragmented clots migrating to and causing embolization in distal vessels; however, thrombus extraction is more challenging due to pressure gradients. Currently, a significant proportion of clinical interventions employ a combined approach using stent retrievers together with aspiration catheters to leverage the advantages of both techniques.

Part Four: Technological Leadership, Driving Innovation and Frontier Breakthroughs in Neurosurgical Medical Devices

4.1 Therapeutic Innovation

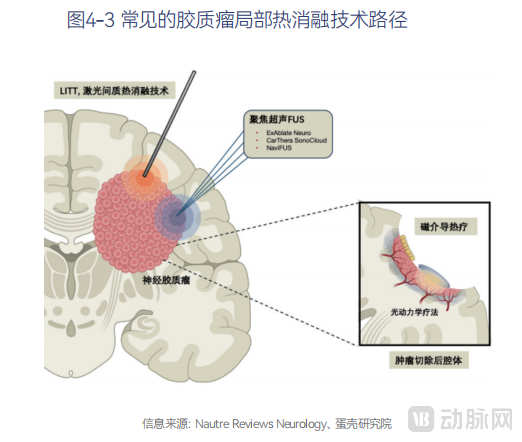

● Local Ablation Techniques Reduce Recurrence of Glioblastoma

Local Thermal Ablation (Local Thermal Therapy) is one of the local treatment modalities for gliomas, utilizing thermal energy to induce apoptosis and necrosis in glioma cells. Additionally, localized hyperthermia can increase the radiosensitivity of gliomas, enhance the efficacy of chemotherapy, trigger immune responses, and cause transient disruption of the blood-brain barrier (BBB).

● Innovative Treatment Options for Chronic Subdural Hematoma

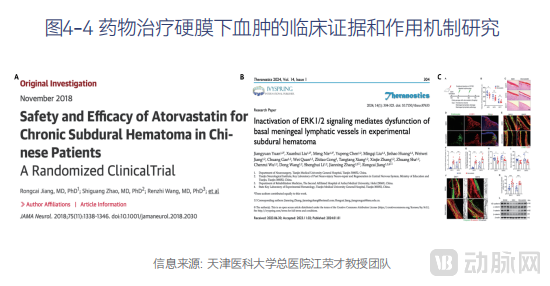

The original, multicenter, randomized, double-blind, controlled clinical trial on drug repurposing of atorvastatin calcium for the treatment of chronic subdural hematoma, initiated by Professor Zhang Jianning and Jiang Rongcai’s team at Tianjin Medical University General Hospital, yielded positive results. The study confirmed that atorvastatin calcium, a classic lipid metabolism inhibitor, can promote the resorption of chronic subdural hematoma. These findings were published as an original article in the internationally renowned journal JAMA Neurology in July 2018. This marks the first time since the disease was recognized that Chinese researchers have demonstrated, through original research, that a novel therapeutic approach using a classic medication can transform the traditional treatment paradigm for this condition.

4.2 Material Innovation

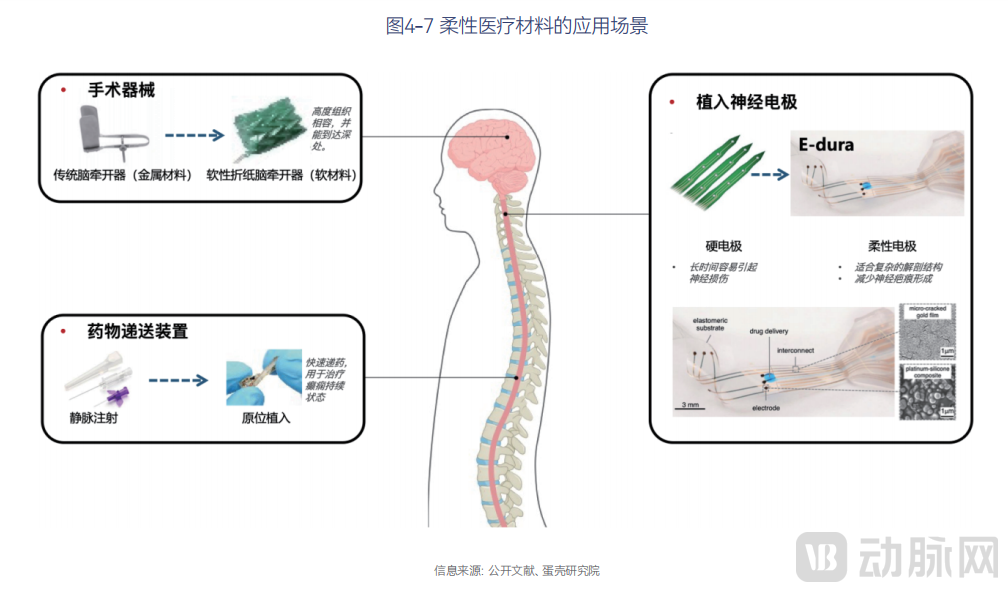

● Flexible medical materials improve biocompatibility with neural tissue

Unlike rigid instruments, soft medical devices (Soft Devices) offer the advantage of mechanical properties that closely match those of biological tissues, enabling minimally invasive surgery, precise drug delivery, and implantable neural monitoring and stimulation, thereby truly achieving revolutionary advances in neurosurgery.

4.3 Algorithmic Innovation

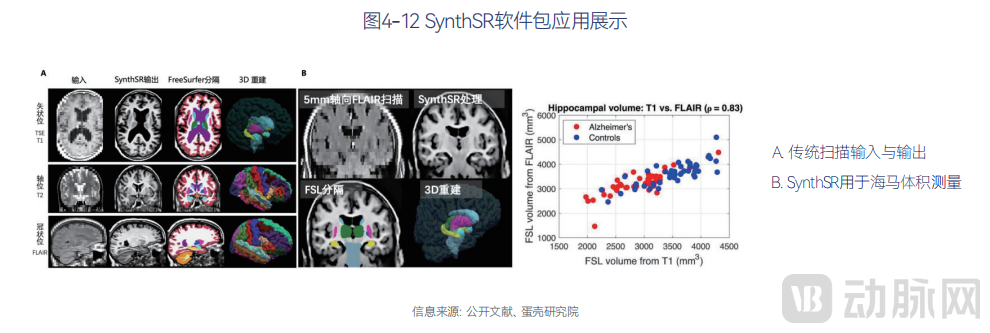

● SynthSR: An open-source AI tool for generating high-resolution T1 scans

There are currently approximately 36,000 magnetic resonance imaging (MRI) scanners in use worldwide, with the United States alone conducting around 40 million clinical scans annually. However, these hospital-based scans often suffer from low precision and inconsistent scanning sequences across different institutions, rendering them unsuitable for unified analysis and resulting in significant waste of clinical data. SynthSR is an open-source neuroimaging software package developed by the Iglesias team at Harvard Medical School. It integrates clinical brain MRI scans with any MR contrast (e.g., T1, T2), orientation (axial, coronal, or sagittal), and resolution, reconstructing them into high-resolution T1-weighted images compatible with nearly all existing human neuroimaging tools. This enables the secondary utilization of conventional clinical scan data.

Part V: Looking Ahead: Analyzing Development Trends in Neurosurgical Medical Devices

5.1 Rapid Development of Subspecialties: Disease-Specific Care Emerges as a New Development Model

Neurosurgery can be further subdivided into subspecialties such as neuro-oncology, cerebrovascular diseases, spinal and spinal cord disorders, craniocerebral trauma, and functional neurological disorders. Many hospitals in China are continuously advancing the development of neurosurgical subspecialties. The “14th Five-Year Plan” for National Clinical Specialty Capacity Building explicitly supports key specialty construction projects across provinces, with a particular emphasis on strengthening the management of neurological disorders, including surgical treatment of traumatic brain injury and comprehensive treatment of intracranial tumors (encompassing surgery, radiotherapy, chemotherapy, targeted therapy, immunotherapy, etc.).

5.2 Volume-Based Procurement Drives Enterprises Toward Platform-Based Innovation

Since 2019, China has conducted 62 rounds of centralized procurement in the medical device sector, covering approximately 17 product categories, including neurosurgical devices. Looking back at 2020, the capital market flourished, with more than 20 innovative enterprises emerging in the neurointerventional field alone. In 2021, domestically produced neurointerventional products experienced a wave of intensive market launches, with coils being the most popular product pipeline, leading to product homogenization. In 2021, Hebei Province implemented centralized procurement for coils, while Zhejiang Province carried out centralized procurement for microcatheters. As centralized procurement has advanced, the procurement model for high-value neurosurgical consumables has gradually matured.

Volume-based procurement has intensified competition in the market for highly homogeneous products, making single-product portfolios insufficient to meet diverse market and customer demands. An analysis of recent approvals for neurosurgical devices reveals that companies are extensively expanding their product portfolios. Leading enterprises such as Medtronic and Johnson & Johnson have achieved comprehensive coverage across major categories, including access, hemorrhagic, and ischemic products, with full coverage of mainstream subcategories such as coils, thrombectomy stents, and aspiration devices. Domestic brands tend to focus on specific product categories based on their respective capabilities, with approved products predominantly concentrated in the ischemic segment. By iterating on existing products and aggressively developing new pipelines, companies are continuously enhancing their competitiveness through multi-category coverage.

5.3 Surgical Robots Will Be the Landmark Achievement of Future Neurosurgical Medical Equipment

Since neurosurgery entered the era of robotic surgery in 1985, surgical robots have made significant progress over the past three decades. In the field of robot-assisted surgery, applications have gradually expanded from relatively simple procedures such as biopsy of intracranial lesions, hematoma puncture, cyst fluid aspiration, and ventriculostomy, to more advanced techniques including deep brain stimulation (DBS), stereoelectroencephalography (SEEG), transcranial magnetic stimulation (TMS), and even remote-controlled operations. Meanwhile, the precision and stability of these systems have steadily improved. With continuous technological development and maturation, autonomously controlled robots are expected to gradually replace master-slave and shared-control systems. These autonomous robots will operate under physician supervision, significantly reducing clinicians’ workload and extending benefits to a broader patient population.

5.4 Product Quality and Manufacturing Process Stability Will Become the Key to Success for Medical Device Manufacturers in Market Competition

According to data disclosed by the FDA, the number of Class I medical device recalls reached a 15-year high in 2022, with 70 recalls, compared to an average of only 47 recalls per year over the previous five years. Among the recalled products were numerous devices related to neurosurgery. For instance, in 2021, a certain flow diverter stent was urgently recalled due to the risk of occasional rupture and fracture of its delivery system; in 2022, a certain intracranial pressure monitor was recalled because equipment failure could cause serious injury or death to patients; and in 2023, a nuclear imaging device was recalled due to the risk of its detector falling and crushing patients.

Taking the neurointerventional industry as an example, it has experienced rapid growth in recent years due to strong interest from capital markets. However, given the market’s high barriers and low penetration rate, the industry remains in the 1.0 stage of competition. At this stage, most companies prioritize platform-based development and accelerating the acquisition of medical device registration certificates. Once products are launched and face market-driven competition, the focus shifts to product quality, clinical efficacy, and profitability, marking the transition to the 2.0 stage of competition. Currently, coils among neurointerventional consumables have already entered this developmental phase. Competition at this stage will be even more intense, particularly in the neurointerventional field characterized by extremely high technical barriers. Only companies that balance both the speed of regulatory approval and product quality will ultimately prevail.

Channels for Purchasing the Complete White Paper

Units or individuals with procurement needs are requested to contact the ITMNS Secretariat.

Contact

Teacher Wang 18992829981

Email Address

ITMNS Secretariat Email: itmns-secr@cawaorg.cn

For more information, please follow the ITMNS official account.