Telehealth Giant Amwell Faces Delisting Risk Amid Strategic Struggles

Amwell

Internet Medical Service Platform

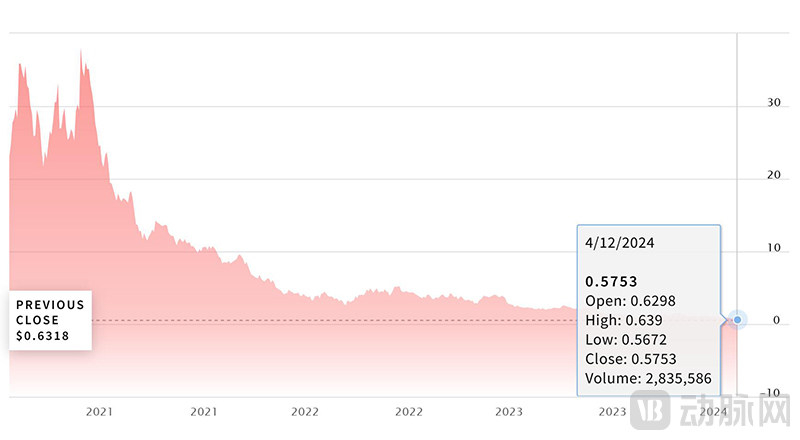

On April 2, the U.S. Securities and Exchange Commission issued a warning letter to Amwell, a well-known internet healthcare company, stating that its common stock had triggered a delisting warning because its average closing price over 30 consecutive days fell below the $1 threshold. If its share price does not improve within six months, it will be delisted from the New York Stock Exchange.

Amwell’s stock price has long hovered below $1.

This does not mean that Amwell is inevitably destined for delisting. After all, the six-month period spans two quarters, giving it ample time to improve its stock price. Nevertheless, for a company regarded as a leader in the U.S. telehealth industry, this constitutes a significant blemish on its record.

It is worth noting that just a few years ago, Amwell was on par with Teladoc, the pioneer of telemedicine. What exactly did Amwell do wrong in such a short span of time? What underlying trends does this reflect? This article summarizes the full context of these developments, hoping to provide reference insights for the industry.

Amwell, formerly known as American Well, was founded in 2006 by brothers Ido Schoenberg and Roy Schoenberg. Both brothers were born in Israel and attended medical school there. After gaining entrepreneurial experience by founding their respective companies, they joined forces to establish Amwell, venturing into the then-emerging field of telemedicine.

At that time, telemedicine was still in its infancy. Just one year earlier, in 2005, Teladoc, the pioneer of telemedicine, had officially launched its telemedicine services. Patients could access this telephone-based teleconsultation program by dialing a “1-800” number to seek medical advice from physicians, who would return their calls within three hours (with an average response time of 30–40 minutes). In addition to providing remote medical consultations, physicians sometimes prescribed medications directly. Teladoc would then place orders with the appropriate pharmacies on behalf of patients based on their needs.

Inspired by this, Amwell’s primary business is to provide 24/7 teleconferencing services for both patients and physicians. It sells its teleconferencing platform as a subscription service to healthcare institutions, enabling medical professionals to easily connect online.

As we entered the internet era, Amwell’s platform also evolved. It offers outstanding SDK (Software Development Kit) and API (Application Programming Interface), enabling its platform to be conveniently and seamlessly embedded into healthcare institutions’ workflows. Clients with certain development capabilities can even use the SDK and API provided by Amwell to embed, integrate, or customize the system themselves. With Amwell’s platform, healthcare institutions can directly launch internet-based medical services from their local Electronic Health Records (EHR) systems and seamlessly integrate them with their reimbursement systems.

To meet customer needs, Amwell also provides hardware such as surgical carts and medical service kiosks with integrated audio and video capabilities. Furthermore, when Amwell’s clients are unable to deliver telehealth services within their own capabilities, they can leverage Amwell’s affiliated AMG service to instantly access a network of more than 5,000 healthcare providers who deliver online remote care to patients.

It is not difficult to imagine that Amwell has received widespread acclaim from healthcare institutions. In 2014, Amwell’s downloads surpassed the 1 million mark. In March 2015, Amwell further obtained the American Telemedicine Association’s first certification for online patient consultations.

In 2015, Teladoc went public on the New York Stock Exchange, becoming the world’s first publicly listed internet healthcare company. Investors eagerly began searching for “the next Teladoc,” and Amwell consequently seized the opportunity for rapid growth.

From 2007 to 2020, Amwell completed a total of 10 financing rounds, raising a cumulative amount of $866 million. Notably, seven of these rounds occurred after December 2014, accounting for $801 million of the total. Among Amwell’s investors are insurance giant Allianz and multinational pharmaceutical company Takeda Pharmaceutical. Clearly, no one wants to miss out on the boom in internet healthcare.

Nevertheless, unlike its competitor Teladoc, which has pursued a more aggressive expansion strategy, Amwell has adopted a more conventional approach to business growth, acquiring only Avizia in 2018 and Aligned TeleHealth in 2019. The former acquisition primarily expanded its business model, while the latter enhanced its mental health service capabilities.

By 2020, Amwell had grown to a considerable scale. It provided telehealth solutions to more than 240 health systems, including 2,000 hospitals and 55 health plan partners, as well as over 36,000 employers, covering the lives of more than 80 million people across the United States. Each day, up to 45,000 virtual care visits were completed through its platform.

At this point, Amwell began its final preparations for the IPO sprint.

In March 2020, the company optimized its brand by changing its name from the somewhat lengthy “American Well” to the more concise “Amwell,” which also carries the phonetic connotation of “I am Well.” In May, it completed its Series C financing round, raising up to $194 million. Furthermore, Amwell partnered with Google Cloud to migrate its video capabilities to the Google Cloud platform. As part of this collaboration, Google Cloud invested $100 million in Amwell.

This has undoubtedly significantly bolstered investor confidence in Amwell. In August, Amwell filed a registration statement with the New York Stock Exchange.

On September 17, 2020, Amwell rang the opening bell and listed on the New York Stock Exchange, successfully raising $742 million. On its first day of trading, the stock opened at $25.51 per share, a 42% increase over its IPO price of $18. Within a month, Amwell’s share price had surged to $35.84.

Subsequently, in its first post-IPO financial report released in December, Amwell delivered strong results: Q3 revenue reached $62.6 million, representing a year-over-year increase of 80%. Revenue from long-term contracts amounted to $25.8 million, up 17% year over year. Online consultation revenue reached $28.5 million, marking a substantial 300% year-over-year increase from the $7.2 million recorded in the same period of 2019.

In terms of visit volume, Amwell’s growth rate was also staggering, with visits reaching 1.414 million in the quarter, a year-on-year increase of 455%. The number of active third-party healthcare providers (those who had provided at least one online consultation service on the platform within the year) reached 62,000, a surging 930% year-on-year increase.

At that moment, everyone believed it was merely the beginning of Amwell’s ascent, with a brighter future just around the corner. However, no one anticipated that this would prove to be Amwell’s peak moment to date.

Although Amwell is often regarded as the second Teladoc, there are notable differences in their business focus. While Teladoc relies primarily on online consultations, Amwell places greater emphasis on empowering clients through its proprietary technology platform behind the scenes. It generates revenue from both providers and patients through their use of its digital health platform, as well as hardware solutions such as community-based surgical carts and service kiosks.

After years of development, Amwell’s platform has achieved coverage across various clinical settings, including family physicians and healthcare institutions. It categorizes medical conditions into modular offerings, requiring clients to subscribe to specific modules to deliver targeted services. For instance, a health plan might initially select only the urgent care module, but as employer needs evolve, it may later add the behavioral health module. Subscription fees for these condition-specific modules constitute a significant portion of Amwell’s revenue.

Amwell’s in-house AMG division represents another value-added service. This division provides a clinical network comprising more than 5,000 healthcare providers, covering numerous fields such as emergency care, behavioral health, lactation consulting, and nutrition, and has earned accreditation from the National Committee for Quality Assurance (NCQA) and the Utilization Review Accreditation Commission (URAC) telehealth certification programs.

This service enables some of Amwell’s clients to deploy telemedicine solutions without employing dedicated physicians. Furthermore, AMG can serve as a supplemental resource when other clients exceed their own service capacity due to nighttime emergencies, weekend demands, or other reasons, or when cases fall outside their scope of medical expertise; naturally, an access fee applies for this service.

Prior to the pandemic, this B2B service consistently accounted for the majority of Amwell’s revenue. In 2019, Amwell reported annual revenue of $149 million, with over $100 million derived from empowering other institutions, while its own online consultation services contributed only $40.8 million in revenue.

Despite its steady development, this customer-empowerment-centric business model has constrained the growth of its revenue scale, as evidenced by its years of operations.

Furthermore, Amwell exhibits a high degree of customer concentration. As disclosed in its prospectus, Anthem, the second-largest health insurer in the United States, is not only a shareholder with a 3% equity stake but also its largest customer. Revenue from this single client accounted for as much as 22% of Amwell’s total revenue in the first half of 2020. Including Anthem, the top ten customers collectively contributed 44% of the company’s revenue.

From another perspective, the loss of any major client could lead to a sharp plunge in its performance.

No one anticipated that Amwell’s online consultation business would experience explosive growth in 2020, surpassing its long-dominant B2B segment to become the primary contributor to revenue.

Amwell’s high growth was certainly driven by the gradual maturation of digital health, but in retrospect, it also benefited significantly from the dividends brought by the COVID-19 pandemic. During the pandemic, regulatory and reimbursement barriers to telemedicine in the United States were substantially reduced. Healthcare systems also promoted virtual consultations to protect healthcare workers from infection and ensure that patients with other conditions could continue to receive care, which greatly accelerated the development of digital health.

The bad news is that as the pandemic recedes, patients still prefer face-to-face consultations with doctors. This is undoubtedly a major concern for Amwell.

In fact, such underlying concerns had already begun to surface in Amwell’s Q3 2020 financial report. Although Amwell’s telehealth visit volume in Q3 reached 1.414 million, representing a year-on-year increase of 455%, it actually declined by approximately one-third compared with the Q2 figure of 2 million visits.

Amwell itself has emphasized that since its founding in 2006, it has cumulatively provided 5.6 million online consultations, with 2.9 million consultations conducted in the first half of 2020 alone. Clearly, Amwell is also wary of this underlying concern, fearing that policies temporarily supporting the development of telemedicine may be rescinded.

Moreover, this surge in business expansion did not help boost profits. In the first half of 2019, Amwell generated $69 million in revenue and reported a net loss of $41 million. By the first half of 2020, its revenue had reached $122 million, but the net loss widened to $111 million—losses grew even faster than revenue.

Nevertheless, Amwell remained optimistic about the growth prospects of internet healthcare at that time, believing that once users embraced the concept of telemedicine, visit volumes and revenue would not experience a significant decline. Furthermore, as regulatory oversight tightened again, many other telemedicine platforms that had emerged during the pandemic would gradually exit the market, thereby reducing competition.

Amwell’s senior executives are well aware of the underlying concerns about slowing future growth, as evident from their consistently cautious statements. Therefore, after securing ample capital through its IPO, Amwell has embarked on a series of strategic initiatives, aiming to carve out its own path to sustainable success.

First, Amwell has made significant investments in technology research and development. In April 2021, Amwell launched the Converge telehealth platform. In layman’s terms, this platform functions more like an “app store for telehealth,” integrating all of Amwell’s proprietary products and third-party applications through a unified interface. This tight integration can greatly enhance the user experience.

For example, alongside the launch of its new platform, Amwell integrated Biobeat’s wearable monitoring solution into the system, enabling clinicians to continuously monitor patients’ vital signs via Amwell’s Converge platform and receive direct alerts on deterioration to their mobile phones through Biobeat’s AI-powered automated real-time early warning scoring system.

Amwell has made substantial investments in this platform, confident that it will become its core competitive advantage in the future. Frankly speaking, the new platform has indeed brought significant benefits to Amwell. For instance, in August 2022, Amwell won the favor of CVS, helping the pharmaceutical giant build its online primary care services.

This project is built on the Converge platform, aiming to integrate all service elements of the CVS ecosystem into a single platform with a unified user experience. Given that Teladoc had previously become the exclusive online healthcare provider for Aetna, a CVS-owned insurer, this partnership represents a bold move against a dominant competitor and holds significant importance for Amwell. Amwell’s senior management also regards it as a compelling demonstration of the Converge platform.

As recently as November 2023, Amwell secured a major contract from the U.S. Defense Health Agency (DHA). The deal, reportedly valued at up to $180 million, will deploy the Converge platform to replace existing video solutions within the U.S. military’s healthcare system.

In addition to the Converge platform, Amwell has invested heavily in R&D elsewhere. For instance, Amwell partnered with Solaborate and LG to leverage televisions as gateways to internet-based healthcare services. Furthermore, Amwell collaborated with the Israeli startup TytoCare to integrate and distribute its FDA-cleared remote diagnostic devices, including digital stethoscopes, otoscopes, and tongue depressors.

In addition to heavy investment in technology, Amwell has also spared no expense in rapidly scaling its business operations. After raising sufficient “ammunition” through its IPO, Amwell quickly acquired SilverCloud Health and Conversa Health in July 2021 for a total consideration of $320 million. The former helped Amwell expand its digital cognitive behavioral health offerings and European presence, while the latter specializes in automated text-based conversational technologies, enhancing service efficiency by covering the entire care continuum from pre-admission patient education to post-acute monitoring and chronic care management.

Furthermore, rumors suggest that Amwell made two separate attempts to acquire the online mental health service provider Talkspace in 2022. However, it is reported that Talkspace rejected Amwell’s offers.

Regrettably, despite numerous strategic moves, Amwell’s performance hit a ceiling after a brief period of rapid business growth, with its financial reports and stock price deteriorating year after year.

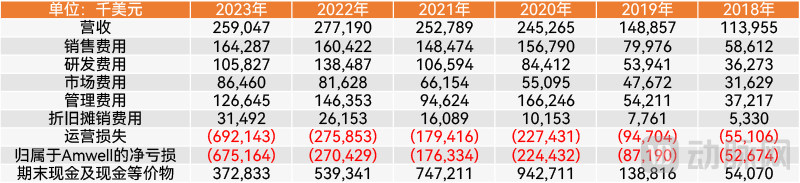

In its full-year 2023 financial report released in February, the company reported annual revenue of $259 million, a 6% year-on-year decrease from $277 million in 2022. The full-year net loss surged significantly from $272 million to $679 million, primarily due to a $436 million goodwill impairment charge triggered by a decline in its stock price.

Perhaps the only good news is that the large contract recently awarded by the U.S. Defense Health Agency, as mentioned earlier, is expected to significantly improve financial statements in the future. Amwell anticipates its 2024 net loss will narrow to between $155 million and $160 million, with the 2025 net loss further reducing to a range of $35 million to $45 million.

Amwell’s Historical Performance (Chart by VCBeat)

According to foreign media reports based on insights from former Amwell employees and other insiders, the company’s consistently lackluster performance may be attributed to the following reasons.

On one hand, Amwell’s business is overly fragmented, failing to concentrate its limited resources on key areas for breakthrough improvements, which gives the impression of a scattered and unfocused approach. Although Amwell initially built its foundation by empowering B2B clients, the short-term high growth of its B2C online consultation business has made it difficult for the company to disengage. Consequently, there is no clear strategic roadmap regarding its future direction.

On the other hand, while Amwell appears to have partnered with numerous enterprises, the implementation of these collaborations has largely been fraught with difficulties. Anyone with even a basic understanding of healthcare IT implementation knows that deploying even a single-point solution is an extremely cumbersome delivery process. In comparison, the complexity of Amwell’s proposed unified platform for seamless integration is on an entirely different level. When coupled with the necessity of ensuring uninterrupted business operations, the implementation challenges become self-evident.

Its R&D expenses have also surged, rising from approximately $54 million in 2019, prior to its IPO, to over $80 million, and subsequently surpassing the $100 million mark. The proportion of R&D expenses to revenue has also increased from 36% to a peak of nearly 50%. However, at least for now, these investments do not appear to have yielded sufficient returns.

Amwell may have been overly confident in its technology, making excessive technical promises that resulted in product delivery falling far short of expectations, which appears to have significantly impacted its performance.

Finally, the unfavorable macroeconomic environment is likely another reason for Amwell’s decline. In fact, digital health companies have faced significant challenges in recent times. Take Teladoc, a leader in the digital health sector, as an example: its fiscal year 2023 performance also fell short of expectations, with fourth-quarter revenue reaching $660 million, below the market consensus of $671 million.

Furthermore, its full-year revenue for fiscal 2023 was $2.6 billion, representing a year-on-year increase of only 8% from $2.4 billion in 2022, indicating a significant slowdown in growth. For fiscal 2024, the company also provided a relatively pessimistic forecast, projecting Q1 2024 revenue to be between $630 million and $645 million, below analysts' consensus estimate of $673 million. Full-year revenue is expected to range from $2.635 billion to $2.735 billion, also falling short of analysts' expectation of $2.77 billion.

Following the release of its financial report, Teladoc’s stock price plummeted by 22%. This also led Jason Gorevic, who had served as CEO for 15 years, to announce his resignation. This is undoubtedly a significant blow to Teladoc. However, compared to Amwell, which is facing tight cash flow, Teladoc’s substantial scale and revenue still enable it to weather the storm and make a comeback.

In fact, not only has internet healthcare in the United States faced challenges, but China’s internet healthcare industry has also undergone difficult adjustments in recent times. The declining performance reflected in annual reports and rumors of acquisitions are both concentrated manifestations of this downturn.

It is easy to imagine the difficulty Amwell faces in achieving counter-trend growth in such an environment.

Although Amwell is in a difficult situation, it still has $370 million in cash on its balance sheet. Given its current revenue and order backlog, extricating itself from trouble within six months should not be a challenge. However, as one of the representative models of telehealth, its future trajectory is arguably more worthy of attention.

Interestingly, as the new generation surpasses the old, we have also observed the growth and expansion of emerging, distinctive internet healthcare companies. For instance, Hims & Hers, which specifically targets the younger generation (for details, see“Revenue Surges Nearly 70% to Approach $1 Billion: The Sector Behind This Company Is Not to Be Missed”) Although it went public nearly a year later than Amwell, with comparable performance at the time of its IPO, it achieved a fourfold increase in revenue over several years following consecutive quarters of rapid growth, with annual revenue poised to surpass $1 billion. Perhaps this strategic direction also represents a potential possibility.

How Internet Healthcare Will Evolve in the Future: Let’s Wait and See.

References:

Heather Landi,Fiercehealthcare.com:Telehealth company Amwell spikes in public debut with outsized $742M IPO

Dave Muoio,Fiercehealthcare.com:NYSE tells Amwell to increase share prices or be delisted