After Five Years of Policy Implementation, Medical Insurance Is Not the Primary Payer for Online Healthcare Services

The National Healthcare Security Administration recently disclosed in public information that,Currently, all provinces across China have issued policy documents on pricing for “Internet+” medical services. Teleconsultations, prenatal diagnostics, and follow-up visits for certain common and chronic diseases conducted via “Internet+” platforms have played a significant role in addressing routine healthcare access and medication needs.。

Since the National Healthcare Security Administration issued the "Guiding Opinions on Improving Price and Medical Insurance Payment Policies for 'Internet+' Medical Services" in 2019, the new policies have been implemented for nearly five years. From including internet medical services in medical insurance coverage to pricing of service items and actual reimbursement, payment for internet medical services under medical insurance has long moved from institutional design to practical implementation.

With policy documents already in place across China, we cannot help but ask: How much revenue has medical insurance actually generated for online healthcare over the years?

Since 2019, the National Healthcare Security Administration has repeatedly taken the lead in issuing policies related to medical insurance reimbursement for internet-based healthcare. In fact, after the first new policy was introduced in 2019, there was limited progress in implementing medical insurance reimbursement; it was the occurrence of special events in 2020 that significantly accelerated this process. Since then,Internet-based medical care has played a positive role in health insurance payments, which is also an important reason for its rapid nationwide promotion over the past two years.

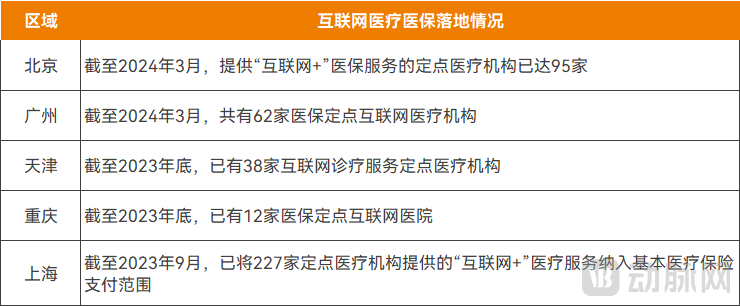

It is reported that after Shanghai’s first batch of tertiary general hospitals piloted the inclusion of “Internet+” medical services in medical insurance reimbursement in 2020, the average monthly service volume at most hospitals showed an upward trend in 2021. As of September 2023, Shanghai had included “Internet+” medical services provided by 227 designated medical institutions within the scope of basic medical insurance coverage. Furthermore, internet hospitals established by primary healthcare institutions are supported for inclusion in the network of designated medical insurance providers, encouraging these primary institutions to offer online follow-up consultations for certain common and chronic diseases.

Beijing implemented health insurance payment for internet-based medical consultations at its first hospital in March 2020. By July 2020, 15 hospitals across six districts had completed interface integration with the health insurance information system, recording RMB 1.686 million in medical expenses incurred through internet-based consultations, with nearly RMB 1 million covered by health insurance. As of March 2024, the number of designated medical institutions providing “Internet+” health insurance services in Beijing had reached 95.

In 2023, cities in Shanxi Province, including Datong, Yuncheng, and Taiyuan, actively explored and launched “Internet + Outpatient Pooling for Employees” medical insurance settlement and payment services, serving over 300,000 person-times cumulatively within nearly a year. The Shanxi Provincial Healthcare Security Administration issued a document to fully implement the “Internet + Outpatient Pooling for Employees” medical insurance payment system starting from December 1.

Status of Medical Insurance Reimbursement Implementation for Internet Healthcare Services in Selected Regions, Source: Official Websites of Local Medical Security Bureaus

Over time, as of now, all provinces across China have issued policy documents on pricing for “Internet+” medical services, thereby establishing enforceable standards for local online medical service pricing, reimbursement coverage, and pharmaceutical services.

Meanwhile, various payment models have emerged across different regions. The most basic model allows patients to directly complete insurance settlements and out-of-pocket payments for follow-up consultation fees and medication costs through the internet hospital system during their medical visits, or to be redirected to the local official medical insurance service platform for settlement. For instance, in Beijing, internet-based follow-up services for common and chronic diseases provided by designated medical institutions are covered by the medical insurance fund and settled in real time for insured individuals.

Some regions have also integrated internet-based healthcare services, designated pharmacies, medical insurance payments, and other convenient health services into public service platforms, allowing local patients to complete the entire process of follow-up consultations, prescription issuance, medication purchases, and online medical insurance payments on a single platform.

Recently, the Shaanxi Medical Insurance APP and mini-program have launched a dual-channel prescription service. Patients can now conduct online follow-up consultations and prescription renewals, compare drug prices at designated pharmacies within the province, purchase medications online, and settle payments through the medical insurance pooled fund. To ensure robust fund supervision, complete traceability is maintained for patient diagnosis and treatment data, prescription details, pooled fund settlement records, medication purchase histories, delivery information, and patient medication usage.

Following the nationwide implementation of medical insurance policies for “Internet Plus” healthcare services, a portion of the medical insurance quota has essentially been shifted to online platforms, rather than generating new incremental funds. Moreover, as online consultations account for a low proportion of total service volume, the amount of insurance quota transferred remains limited. Nevertheless, the inclusion of online services in medical insurance reimbursement has promoted the growth of internet-based diagnosis and treatment volumes, playing a positive role in enhancing public convenience.

Among the institutions designated as medical insurance providers are also non-public medical institutions, such as internet diagnosis and treatment services provided by private medical institutions or enterprise-led internet hospitals.

As one of the earliest regions to pilot medical insurance payments for internet hospitals, Yinchuan has continuously adjusted its policies in recent years based on actual conditions. As of February 2024, there were 14 internet hospitals designated by the Yinchuan Medical Insurance Bureau, including those operated by Ping An Health, Baidu Health, WeDoctor, Yuanxin Technology, Medlinker, Zhiyun Health, and JD Health in Yinchuan. Meanwhile, the scope of medical insurance coverage for internet hospital services has expanded to include 17 types of major outpatient diseases.

In Tianjin, among the 38 designated medical institutions providing internet diagnosis and treatment services as of the end of 2023, 24 were private entities, including outpatient clinics and private hospitals. In Beijing, private chain institutions such as Gushengtang have been included in the “Internet+” medical insurance designated providers.

In June 2023, Guangzhou Yishengkang Internet Hospital launched Mobile Medical Insurance 2.0 payment services. Local patients can enjoy pooled medical insurance fund coverage by selecting the medical insurance payment option after completing an online consultation, obtaining an electronic prescription, and submitting the required information.

Furthermore, WeDoctor has multiple internet hospitals included in the medical insurance payment system in Tianjin, Shandong, Fujian, Shanghai, and other regions, where it also conducts in-depth business operations.

A review of corporate prospectuses, financial reports, and other public data reveals that, in most cases, national medical insurance has not yet generated substantial revenue for companies.

First, even with medical insurance reimbursement, the out-of-pocket cost per visit for patients is not high.Statistical data show that among the first batch of internet hospitals in Shanghai piloting medical insurance payments, the average cost per online outpatient visit was lower than that of offline visits, ranging from tens to over 200 yuan. Online consultations are predominantly outpatient-based, and the scope of medical services covered by medical insurance is narrower than that for offline services, resulting in generally lower average costs per visit. Furthermore, stricter requirements for rational drug use and prescription review under medical insurance regulations clearly preclude any pursuit of higher “revenue per user.”

Second, the volume of services covered by medical insurance reimbursement is limited.An internet hospital can provide consultations to patients across China, whereas health insurance is strongly localized; even if a service is covered by a local health insurance scheme, it remains valid only for patients in that specific region.

The 53rd Statistical Report on China’s Internet Development stated that by the end of 2023, China had 414 million users of internet-based healthcare services, a figure that continues to grow steadily. While this is already a substantial number, it becomes relatively small when distributed across various medical insurance pooling regions; furthermore, even fewer regions have incorporated corporate-owned internet hospitals into their medical insurance reimbursement schemes.

Offline, policies for cross-regional reimbursement of medical insurance are being advanced, and raising the pooling level of medical insurance has become a definitive direction. Both developments help internet hospitals serve medical insurance patients on a broader scale. However, these two initiatives are massive undertakings. Considerable effort and time have already been devoted to untangling the complexities of offline payments, so it will take even longer for their impact to fully materialize in the online realm.

Overall, private medical institutions are similar to public ones in that their internet hospital medical insurance funding primarily comes from existing quotas, with the only difference being the payment channels. Although it is no longer rare for corporate-owned internet hospitals to be included in the medical insurance system, they still rely on offline medical institutions, and data indicates that their share of the medical insurance quota remains limited.

Internet healthcare is strongly correlated with online pharmaceuticals,The trend of using medical insurance for online drug purchases has also arrived,Rapid Expansion of Scope Since 2023。

In August 2023, the Shenyang Municipal Healthcare Security Administration partnered with Meituan to launch a compliant medical insurance pharmacy purchasing service. Insured residents in Shenyang can use their personal medical insurance accounts to purchase medications online via the Shenyang Smart Healthcare Security APP, with fast home delivery.

Since October 2023, Shanghai has also launched a pilot program for medical insurance payment for online drug purchases. Through collaboration among medical insurance authorities, internet platforms, and pharmacies, users can use their personal medical insurance accounts to pay for medications at online pharmacies marked with “Medical Insurance Payment” and have them delivered via food-delivery services.

According to the Shanghai Municipal Healthcare Security Administration, since the launch of this feature, 774 pharmacies have been integrated into the online medical insurance payment system. As of February 29, 2024, a total of 741,600 transactions were completed via online medical insurance payments, averaging over 5,000 transactions per day over the 130-day period, indicating rapid growth.

Meanwhile, Shanghai will further strengthen the integration between internet hospitals and pharmacies, enabling prescriptions for common chronic disease medications and prescription drugs to be issued through multiple channels, including internet hospitals, and transferred to pharmacies for quick medication purchase and payment.

In 2024, Ping An Health enabled online medical insurance payments for prescription drug purchases in two cities within a single month. In March, Ping An Health fully launched its online medical insurance payment service for drug purchases in Dongguan, allowing customers to use their medical insurance accounts for online payments at O2O pharmacies in the area. Local patients can place orders via the Ping An Health APP or its WeChat mini-program of the same name, paying through their personal medical insurance accounts online and having medications delivered directly to their homes.

In April, Ping An Health launched online medication purchasing in Guangzhou, supporting payments from both the pooled fund and individual accounts of medical insurance. By connecting with designated local pharmacies, the service enhances convenience for patients when purchasing medications. It is reported that Ping An Health has already covered O2O medication purchasing in more than 200 cities across China, and will continue to roll out online medical insurance-covered medication purchasing services in other cities in the future.

Across China’s online retail pharmaceutical market, O2O medication purchases with medical insurance payment have been implemented in multiple cities in provinces such as Zhejiang and Shandong, in addition to the aforementioned regions.

In recent years, the pharmaceutical O2O sector has experienced rapid growth, with its share of the pharmaceutical retail market continuously increasing. Online medication purchases are closely integrated with medical consultations; in particular, compliant prescriptions are required for buying prescription drugs. Most internet healthcare platforms have also established O2O medication purchasing services, and the inclusion of medical insurance reimbursement for drug purchases has provided a certain boost to these platforms.

However, it is crucial to recognize that in the currently rapidly expanding model of online medication purchases covered by medical insurance, the entity responsible for billing is the offline pharmacy. Internet platforms serve merely as intermediaries, providing pharmacies with traffic access and technical support, while offering patients medication delivery services and, when needed, online consultation and diagnostic services. Apart from their self-operated pharmacies, these platforms do not supply the medications themselves.

In such cases, the platform’s revenue is derived primarily from service commissions rather than pharmaceutical retail.Under the trend of medical insurance payments for O2O pharmaceutical purchases, platforms cannot directly share in the medical insurance fund; instead, they generate higher platform service fees as medical insurance coverage drives an increase in O2O medication orders.

Under the current policy framework, internet-based medical consultations are limited to follow-up visits, primarily for prescribing refills for patients with common or chronic conditions whose status is relatively stable. The corresponding fees are charged at the same rate as standard outpatient services.

The National Healthcare Security Administration also stated in its public information,Should future industry regulators expand the scope of internet-based medical consultations from follow-up visits to include initial consultations and pharmaceutical care clinics, the healthcare security authorities will promptly implement policies for tiered pricing of initial consultations based on healthcare provider qualifications and establish fee schedules for “Internet + Pharmaceutical Care Clinics,” in accordance with the principle of parity between online and offline services.

Furthermore, “Internet + Nursing Services” primarily involve online appointment scheduling, with hospitals dispatching nurses to provide medical services at patients’ homes.The healthcare security authorities have directed localities to accelerate the improvement of pricing policies for in-home medical services, adopting a fee structure of “medical service price + in-home service fee.”, with charges for medical services, pharmaceuticals, and medical consumables subject to the drug price policies implemented by this medical institution. Public medical institutions may independently determine home visit service fees.

Overall, the scope of medical insurance coverage for internet-based healthcare services is expected to continue expanding. Against this backdrop, should corporate-run internet hospitals and online healthcare platforms strive vigorously to secure inclusion in the medical insurance system?

Based on the preceding analysis, apart from specific models, the direct financial gains from medical insurance are limited. Currently, most regions have adopted a fee-for-service payment model for online consultations. Given the broader context of medical insurance cost containment, continuing with fee-for-service payments in the future is unlikely to drive significant revenue growth.

However, the authoritative endorsement provided by health insurance reimbursement can help internet healthcare companies gain greater patient trust. On this basis of attracting more patients, these companies can offer other reasonable, compliant, fee-based services that contribute to the maintenance of patients’ health.From the perspective of platform influence, internet healthcare companies should enhance the standardization of their operations and strive to integrate with medical insurance payment systems.

From another perspective, the opposite is true. In recent years, financial reports of publicly listed healthcare service providers have frequently featured similar statements: the proportion of revenue derived from medical insurance has been declining year by year, indicating a gradual reduction in reliance on such income. This sends a clear signal that, as oversight and cost-containment measures for medical insurance funds become increasingly stringent, a high share of revenue from medical insurance is not necessarily advantageous.

In this regard,Internet healthcare platforms should also draw appropriate insights from this; from the perspectives of business model and revenue, they should strive to “de-link” from medical insurance reimbursement and establish other sustainable, scalable revenue streams.

Of course, exceptions apply when the business model is inherently built around controlling healthcare insurance expenditures. For instance, WeDoctor’s Digital Health Community model is closely aligned with the direction of healthcare insurance payment reforms. In Tianjin, WeDoctor has successfully achieved scaled revenue through an innovative performance-based payment reform model, with a single smart hospital generating revenue comparable to that of a large Grade A tertiary hospital.

In summary, whether or not an internet healthcare enterprise is integrated into the national health insurance system is merely an outcome; the foundation for long-term development lies in standardized operations. While health insurance policies supporting internet medical services are certainly favorable, the most critical factor remains the enterprise’s comprehensive management and utilization of both internal and external factors.

References:

Pan Yi, Yang Yuqing, Xia Yun. Analysis of the Effect of Including Pilot “Internet+” Medical Services in Medical Insurance Payment in Tertiary General Hospitals in Shanghai [J]. Modern Hospitals, 2023, 23(1): 18-20.