Beyond Class 1 Innovative Drugs: The Rising Opportunity in Transdermal Drug Delivery

Competition for Class 1 innovative drugs has always been fierce. Although Class 1 innovative drugs represent the highest level of China’s biopharmaceutical industry, blind pursuit of original innovation and excessive competition within the same target space can drive companies to their demise—a fact already evidenced by numerous biotech firms struggling with weak financing or clinical development challenges.

Following the previous wave of biotech investment fervor, an increasing number of investors and companies have come to recognize the costs and risks associated with first-in-class innovation.Since 2020, innovative formulations and novel drug delivery systems in China have undergone rapid development, driven by policy support and market demand.

Innovative formulations are improvements based on a thorough understanding of drug molecular properties, particularly those demonstrated in clinical practice. They can circumvent the inherent defects of drug molecules, reduce toxic side effects, and enable more prolonged and stable therapeutic efficacy.Compared with new molecular entities, the development of innovative formulations requires lower investment;It also makes significant contributions to addressing unmet clinical needs.

Even in the United States, the global pinnacle of innovative drug development, regulators and the market alike recognize this form of innovation, which features shorter cycles and lower risks. Since 2016, the number of new drugs approved by the U.S. FDA under Section 505(b)(2) (innovative formulation new drugs) has exceeded that under Section 505(b)(1) (innovative compound new drugs).

In recent years, innovative formulations such as nano-delivery systems and inhalation preparations have become a major focus in China.However, there remains a largely untapped blue ocean: transdermal drug delivery.Currently, the sales revenue of transdermal preparations in the Chinese market is approximately RMB 13 billion.Only chemical drug patch varieties were accepted from 2021 to 2023.18.

This is a field where even intense competition has yet to take hold: transdermal formulations are subject to stringent clinical evaluation requirements, entailing high time and financial investments. With only a limited number of such products currently marketed in China, many patients are compelled to source them from abroad.

Recently, the 2024 China Pharmaceutical Full Industry Chain New Resources Conference was held in Nanjing. Drawing on expert insights from the special session on R&D and innovative collaborative applications of transdermal technologies, VCBeat seeks to discuss: Is it time to enter this blue-ocean market?

A Paradoxical Blue Ocean

As the third major drug delivery system beyond oral and injectable routes, transdermal drug delivery has always been characterized by its "paradoxical nature."

On the one hand, transdermal formulations were developed early but have not yet achieved widespread adoption.

Since the 1970s, modern transdermal formulations have pioneered their development in the Japanese and U.S. markets. To date, hundreds of transdermal products have been launched globally, yet the sector has not experienced the widespread boom that was anticipated. In 2004, the U.S. prescription patch market exceeded $3 billion; however, transdermal drug delivery subsequently failed to maintain its high-growth momentum or witness a surge in new product launches. According to Research and Markets, the global transdermal drug delivery market is projected to reach $10.67 billion by 2026—a figure dwarfed by Keytruda’s annual revenue of $25.011 billion in 2023.

On the other hand, while transdermal drug delivery offers significant advantages, its therapeutic efficacy remains limited due to technical bottlenecks and other constraints.

For decades, transdermal formulations have been successively launched across multiple therapeutic areas, including cardiovascular diseases, central nervous system disorders, anti-inflammatory and analgesic treatments, and allergic conditions. Transdermal drug delivery offers flexibility and high patient compliance, particularly for topical administration or in special populations such as infants and the elderly. For instance, Novartis’s rivastigmine transdermal patch, introduced in 2007 for Alzheimer’s disease (AD), significantly reduced the gastrointestinal adverse effects associated with the original oral formulation and decreased dosing frequency. Its indications were expanded to include mild-to-moderate AD, ultimately achieving peak sales of approximately $900 million.

However, since rivastigmine transdermal patches, no other single transdermal patch product has achieved such high sales revenue, largely due to limited clinical benefits. For instance, many active ingredients fail to reach effective therapeutic concentrations; ionized drugs cannot be administered via the transdermal route; and certain components struggle to penetrate the stratum corneum, resulting in a delayed onset of action.

Another aspect is that although traditional plasters have a long history in China, the domestic market remains unfamiliar with transdermal drug delivery itself. In other words, China has not yet transitioned from traditional formulation methods to modern pharmaceutical formulations in the field of transdermal drug delivery systems.

In China's transdermal drug delivery system (TDDS) market, novel transdermal formulations account for 13%, while traditional Chinese medicine (TCM) transdermal formulations comprise 87%. Currently, the representative chemical drug-based transdermal products in China are Jiudian Pharmaceutical's Loxoprofen Sodium Gel and Tide Pharmaceutical's Flurbiprofen Gel, both of which provide anti-inflammatory and analgesic effects.

Data show that in 2022, Jiudian’s Loxoprofen Sodium Gel and Tide’s Flurbiprofen Gel ranked first and second, respectively, in hospital market sales of topical patches, with sales exceeding RMB 1.5 billion and RMB 2.5 billion. As of the first half of 2023, their three-year compound annual growth rates (CAGRs) were 45.5% and 38.8%, respectively.

Beneath the rapidly growing sales figures of these two major products lies the fact that annual domestic patch sales in China amount to less than 300 million units, compared to over 5 billion units sold annually in Japan, indicating enormous potential for market growth.

Therefore, it is evident that leading pharmaceutical companies such as Hengrui Medicine and Kanion Pharmaceutical are strategically positioning themselves in this field, while specialized transdermal formulation companies have also attracted significant attention from investment institutions in recent years.

Transdermal Drug Delivery System Companies That Secured Investment in Recent Years

Boom May Arrive “Late but Sure”

Around the year 2000, due to the rapid growth of the U.S. prescription patch market, many predictions suggested that within 10 to 15 years, one-third of currently used medications might be formulated as transdermal preparations. However, the global transdermal preparation market has not continued to thrive.

Especially after 2010, the number of new transdermal drug registrations worldwide has sharply declined. The core reason is that with existing mainstream technologies, only a small fraction of small-molecule compounds can penetrate the skin barrier, resulting in a limited selection of eligible drugs; currently, only about 30 compounds have been developed into transdermal formulations.

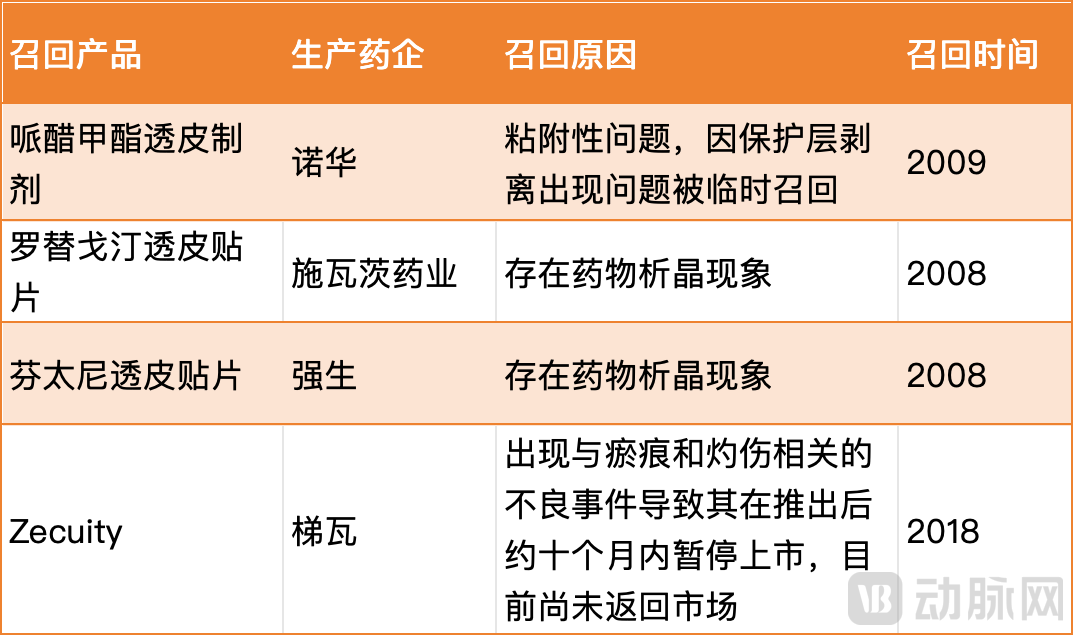

Furthermore, since the first transdermal patch was launched in 1979, the number of transdermal patches and similar dosage forms recalled by the FDA has been steadily increasing. The majority of these recalls were due to quality-related issues, which have undermined market confidence in transdermal formulations.

Partial FDA Recall Information on Transdermal Preparations

An analysis of recall reasons—including adhesion issues, drug crystallization, and adverse events—highlights the bottlenecks encountered by transdermal formulations in materials and penetration-enhancement technologies. For instance, Zecuity, the sumatriptan transdermal patch utilizing iontophoresis (the third product based on this technology), was withdrawn from the market due to safety concerns, despite high expectations from Teva.

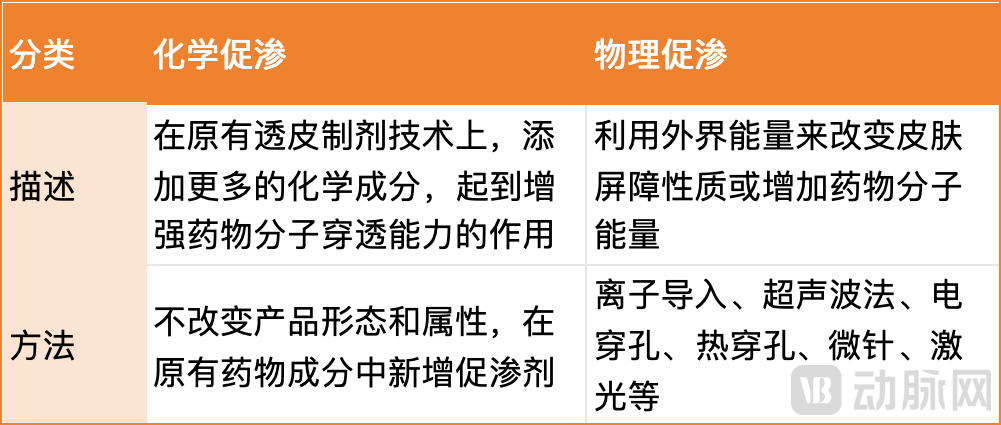

Therefore, overcoming the penetration enhancement challenges of transdermal formulations is a key focus for the entire industry. One approach involves traditional chemical penetration enhancers, while the other encompasses physical enhancement techniques represented by microneedles, iontophoresis, and electroporation.

Both face challenges in R&D implementation and commercialization. For physical penetration enhancement, issues may include system complexity, limited efficacy, and high treatment costs. For instance, the development of microneedle products, which have gained significant attention in the past two years, has progressed relatively slowly. The core reason lies in the complex manufacturing processes and high costs of microneedles, making short-term commercialization considerably difficult.

For chemical permeation enhancement, it is necessary to address technical challenges while seizing the appropriate window of opportunity: the accelerated development of new molecular entities for innovative drugs may bring about qualitative leaps in treatment, rendering some older molecule modification technologies obsolete or meaningless.

However, with the continuous advancement of technology and materials, the prosperity of transdermal formulations may be “late but inevitable.” Wu Xuetao, Secretary-General of the Transdermal Technology Innovation Alliance, pointed out that the variety of new patch types is currently increasing at an annual rate of 11.2%, and domestic Chinese teams are also rapidly growing in the areas of penetration enhancement technologies and excipients.

Transdermal formulation excipient manufacturers, represented by New Saint Era and Shanghai Cisen, have already advanced multiple excipients to the “Investigational” stage, with more than 10 collaborative products in development. Just a few days ago, China’s first drug microneedle patch—the dexmedetomidine hydrochloride microneedle patch submitted by Guangzhou Xinji Pharmaceutical—received clinical trial approval, ushering in a new phase for microneedle-based drug delivery in China.

A worthy entry point has arrived.

Another major factor that hindered the development of transdermal formulations at the time was the withdrawal of capital investment; a large number of U.S. drug-delivery technology companies disappeared, making it increasingly difficult to see the emergence of highly innovative products with significant clinical advantages as witnessed in the past.

However, in recent years, resources and policies have once again begun to favor innovative formulations, including transdermal preparations.In China, the tightening of biomedical funding and the declining tolerance for the risks associated with innovative drugs are highly evident. Improved new drugs, classified as Class 2 innovative drugs, have garnered increasing policy support and market attention as a more affordable innovation pathway for domestic enterprises.

According to data from the National Medical Products Administration, a total of 40 improved new drugs were approved for marketing in China from 2019 to 2023. An analysis of the number of approvals shows that 1, 2, 15, 15, and 7 improved new drugs were launched in 2019, 2020, 2021, 2022, and 2023, respectively, demonstrating an overall upward trend.

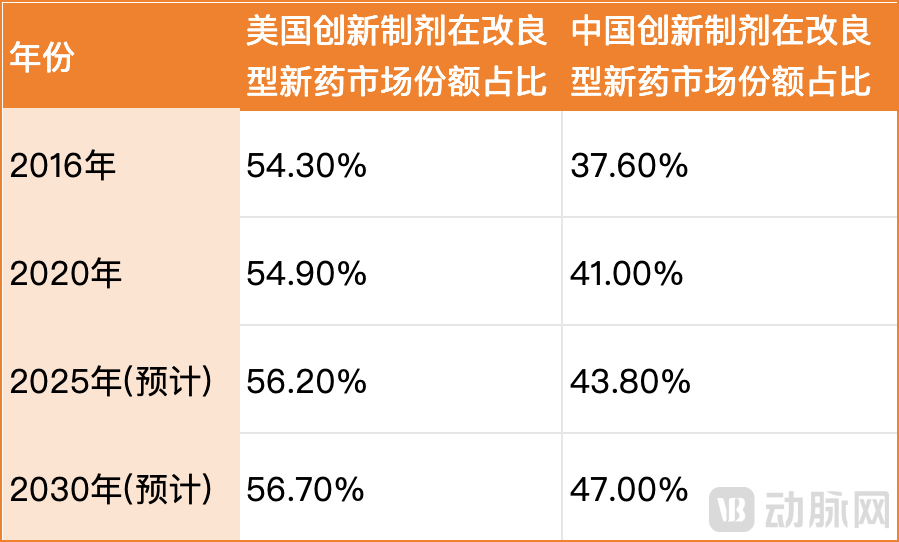

Among these factors, the successful development of innovative formulations is of significant importance to the growth of the modified new drug market size. In the mature U.S. market, the share of innovative formulations within the modified new drug sector has been increasing year by year; this proportion is also expected to rise annually in China, reaching 47% by 2030.

Data Source: Frost & Sullivan

Currently, newly launched innovative formulations are predominantly concentrated in orally disintegrating films, injectables, and injectable microspheres. In contrast, the competitive landscape for transdermal formulations is relatively less intense. It is precisely this market gap that endows companies specializing in transdermal formulations with substantial growth potential.

Given the limited number of domestically marketed products and patents related to transdermal formulations, the Chinese government has begun to prioritize and support the development of transdermal drug delivery systems, thereby creating a favorable policy environment for future growth in this field. For instance, the “13th Five-Year Plan for the Development of Strategic Emerging Industries” explicitly listed “technologies for novel dosage forms such as transdermal and mucosal drug delivery systems” within the biomedical and biopharmaceutical sectors.

Not long ago, the proposed biopharmaceutical promotion measures in Zhuhai also mentioned that a reward of RMB 1 million would be granted for the first registration certificate of each innovative high-end formulation (including innovative dosage forms such as nanoparticles, microspheres, liposomes, controlled-release and sustained-release formulations, and microneedles).

Compared with “injections and oral medications,” transdermal formulations offer more distinct advantages in improving convenience and adherence, as well as reducing adverse reactions; once they capture market share, they will generate substantial revenue.

In addition to the visibly surging sales of loxoprofen sodium gel and Taiho Pharmaceutical’s flurbiprofen gel mentioned earlier, transdermal formulations have already demonstrated considerable revenue-generating potential in transactions within the field of improved new drugs:In 2021, Luye Pharma licensed the commercialization rights in China for its rivastigmine transdermal patch, indicated for the treatment of mild to moderate Alzheimer’s disease, to GeneScience Pharmaceuticals for a maximum consideration of RMB 216 million. Subsequently, Luye Pharma launched the world’s first twice-weekly rivastigmine transdermal patch and granted Myungin Pharmaceutical exclusive commercialization rights in South Korea in 2024.

Therefore, although the transdermal drug delivery sector has not yet formed a complete and clearly defined track, it is currently in an optimal window for investment or market entry.

The Chinese Market Is Larger Than Expected

The transdermal drug delivery market in China is still in its early stages, with few approved products currently available and low industry maturity. The domestic market potential can initially be realized by closing the gap between China and mature markets such as Europe, the United States, and Japan.

As of 2022, data from PatSnap shows that the United States had a total of 157 innovative patches and 198 generic patches, while China had 59 chemical drug patches, predominantly generics. Many marketed products lag behind those in Europe and the United States by “several decades.” Therefore, if transdermal formulation manufacturers can develop superior product technologies and launch products with favorable pharmacoeconomic profiles, they can stimulate the growth of the transdermal drug delivery market.

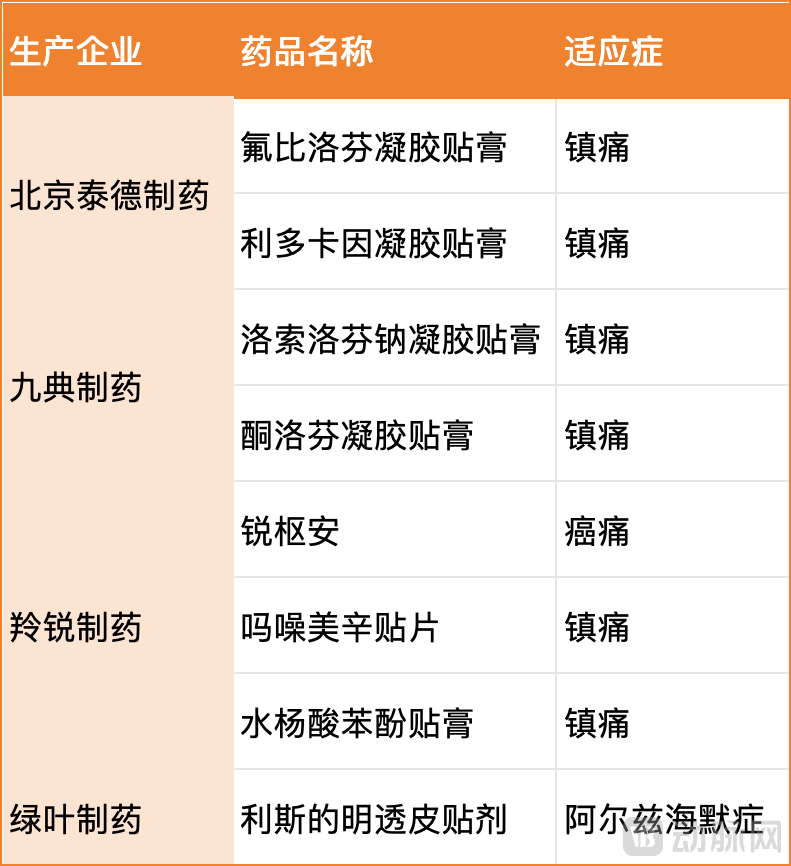

Some Transdermal Formulation Products Marketed in China

In terms of indications, transdermal drug delivery is often targeted at chronic diseases. With the aging population in China and the continuous improvement in quality of life, the disease spectrum and therapeutic approaches need to be adjusted accordingly. Medications for chronic diseases require more patient-friendly administration methods, creating substantial clinical demand for transdermal drug delivery. Taking analgesic needs as an example, if we assume that 20% of patients with chronic pain receive treatment, with an average annual treatment cost of RMB 2,000 per patient, the market size for analgesics in China would reach RMB 50 billion.

A sufficiently large market size means that the transdermal drug delivery market is not a winner-takes-all scenario; both early entrants leveraging generic drugs and more innovative latecomers have opportunities.

However, the reason why many companies are currently adopting a wait-and-see approach toward transdermal drug delivery is due to the high barriers and numerous challenges within the industry.

First are patent and technological barriers.Transdermal drug delivery presents high technical barriers, involving multidisciplinary approaches spanning polymer science, chemistry, biology, and pharmaceutical formulation. The FDA classifies transdermal formulations as complex products within the category of complex dosage forms, characterized by significant R&D challenges and substantial technical hurdles. Notably, many suitable and advantageous non-active ingredients or excipients remain monopolized by foreign companies. Collective efforts across the entire industry value chain are required to achieve domestic production of equipment, excipients, and packaging materials in China.

Next is the talent barrier.As transdermal drug delivery is an interdisciplinary field, clarifying its intrinsic logical connections poses a significant challenge to R&D professionals. Currently, in ChinaTalent is scarce in the transdermal formulation industry,Talent with R&D experience across the entire lifecycle of transdermal patches—including development, evaluation, and manufacturing—is extremely scarce. It was not until 2020, amid consolidation and restructuring among domestic and international enterprises, that such professionals began to enter the job market in succession.

Then, there are still relatively few clinical policies and guidelines.Professor Liu Yali, Deputy Director of the Institution and Director of the Phase I Clinical Trial Ward at the First Affiliated Hospital of Shantou University Medical College, pointed out: “In China, guidelines for transdermal drug delivery—namely, the Technical Guidelines for Research on Topical Chemical Generic Drugs and the Technical Guidelines for Clinical Trials of Locally Administered and Locally Acting Drugs—have already been issued. However, compared with mature markets, there is still a relative lack of relevant regulations and product-specific guidelines.”

Finally, there are commercialization challenges.Currently, hundreds of transdermal formulation varieties in China have entered the clinical trial stage and are highly likely to be launched centrally between 2025 and 2026, thereby expanding the overall market size. However, they also face challenges in promoting innovative formulations, specifically regarding how to conduct market education to replace existing products, as well as the need for advance layout and planning for either building in-house sales teams or selecting distribution agents. On the other hand, the launch of more varieties makes inclusion in volume-based procurement (VBP) possible. The resulting decline in unit prices due to VBP will also test the cost-control capabilities of pharmaceutical companies.

Nevertheless, China’s emerging market for novel transdermal formulations holds greater potential than anticipated, offering ample room for numerous enterprises to thrive.

References

2024 China Pharmaceutical Full Industry Chain New Resources Conference - On-site Discussion of the Special Session on R&D and Application Innovation Cooperation in Transdermal Technology

Huge Development Potential for the Improved New Chemical Drug Industry - China Pharmaceutical News, http://bk.cnpharm.com/zgyyb/2024/03/14/app_316582.html

Current Industry Status and Development Prospects of Transdermal Preparations - Yaoshi Zongheng, https://mp.weixin.qq.com/s/_ZyHZ0__wp5U5v-SrbBOjA

A Preliminary Exploration of the Transdermal Drug Delivery Industry - Chuangjing Capital, https://mp.weixin.qq.com/s/BRLcW20ms-OfuBoP3NYcrg

China’s First Transdermal Drug Delivery Technology Research Institute Established: How to Break the Impasse of Shortage in High-End Formulation Talent? - 21st Century Business Herald, https://www.21jingji.com/article/20230227/herald/2a4467ba0352a5bbdb919ad6f5983543.html