Smart Healthcare Enters the Era of Medical Data Value Application: Transitioning from Data Collection and Governance to Commercialization

Building upon existing information infrastructure, against the backdrop of continuously upgrading demands for medical services, and driven by the ongoing integration of innovative technologies such as big data and artificial intelligence, the scope and definition of healthcare informatization are constantly expanding. It has evolved from standalone, hospital-based systems to interconnected data sharing and collaborative applications across regions and diverse institutions. Furthermore, it has extended beyond patients’ electronic medical records to encompass full-lifecycle health data of residents and environment-related factors closely linked to health, thereby fostering a more comprehensive and digitally intelligent framework for smart healthcare development.

This report seeks to explore the current status, pain points, and industry-leading solutions at each stage of development, through collaborative discussions with enterprises working together in the same sector.

Key Points:

Traditional information systems suffer from severe homogenization, prompting enterprises to seek breakthroughs through new products, technologies, and services, such as developing cloud-based systems, integrating AI application tools into healthcare IT, and exploring collaborative opportunities in scientific research and drug development.

Data silos are an inevitable stage in the development of informatization. Currently, various stakeholders in the industry are joining forces to actively break down these silos and unlock the value of data. Policies continue to encourage data interoperability and refine standards, while enterprises govern multi-source heterogeneous data through integration platforms and database construction. Medical institutions are also actively embracing digital transformation.

The smart healthcare industry has progressed through the stages of data collection and governance, and is now advancing into a phase of digital-intelligent application development. Built upon high-quality databases, digital-intelligent applications have achieved commercial implementation in scenarios such as clinical research, disease-specific studies, drug development, real-world evidence (RWE) research, and digital marketing.

1Policy-Driven Three Waves of Development Surge, Leading the Upgrade of Healthcare Informatics

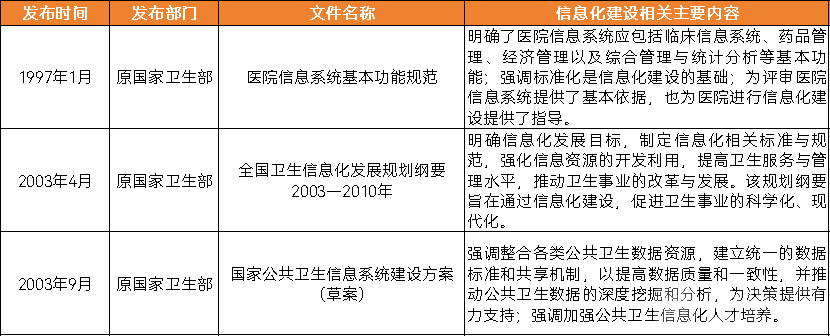

The first wave of development boom focused on clinical informatics.In September 1995, the “Military Project No. 1” was officially initiated and deployed in over 200 military hospitals and more than 100 civilian hospitals. At that time, China’s healthcare informatization was in its nascent stage, focusing on hospital internal management. The Hospital Information System (HIS) served as the primary application system during this period, marking the first wave of development centered on the construction of in-hospital medical information systems in China.

Key National Policies Driving the First Wave of Development Boom (Source: VBInsight)

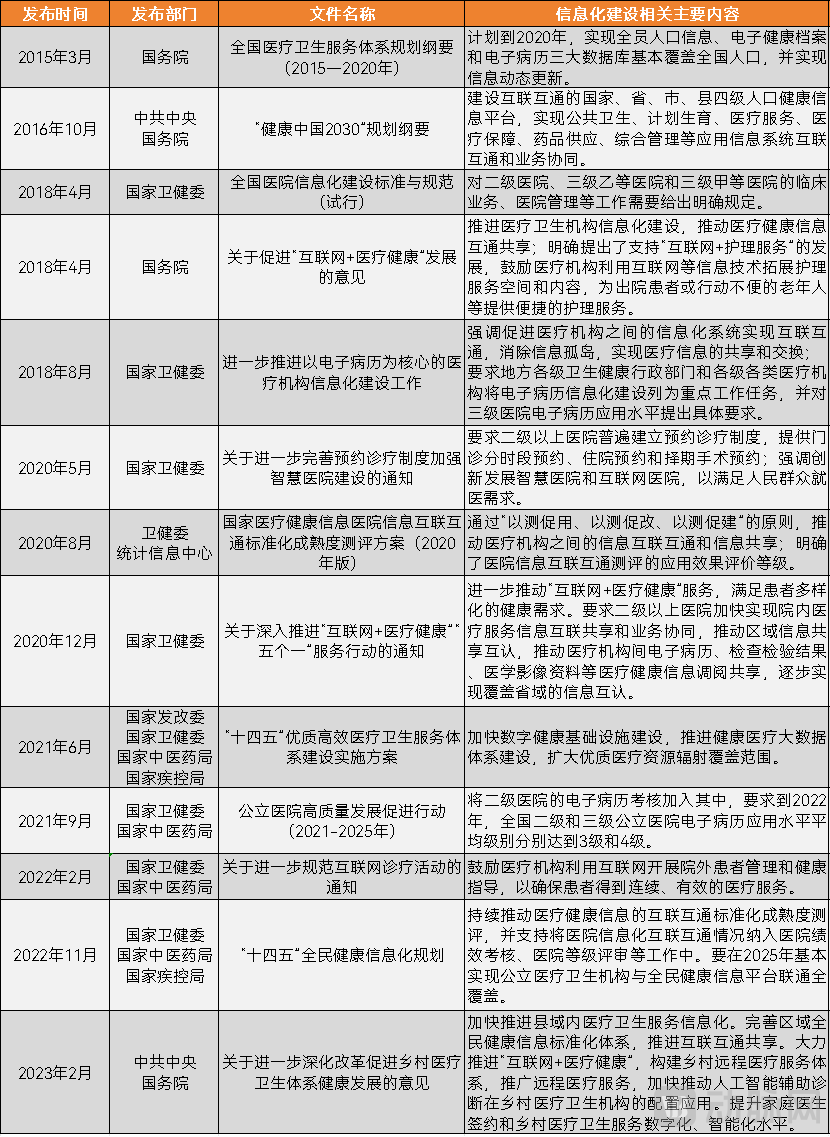

The EMR Grading System Sparks a Second Wave of Development, with Digital Technologies Widely Adopted.In December 2009, the former Ministry of Health and the State Administration of Traditional Chinese Medicine jointly issued the “Basic Architecture and Data Standards for Electronic Medical Records (Trial),” which defined the overall framework, data structure, and data exchange standards for electronic medical records, laying the foundation for information sharing and interoperability among healthcare institutions.

The standardization of electronic medical records (EMRs), in conjunction with relevant graded evaluation methodologies, has robustly and efficiently promoted interoperability among various systems within healthcare information infrastructure. At present, China’s healthcare informatization is no longer confined to the digitization and storage of medical data and processes via hospital-based information systems; instead, it focuses on identifying, retrieving, and applying the accumulated stored data. Consequently, China’s healthcare informatization is advancing toward healthcare digitalization, ushering in a second wave of development momentum.

Key National Policies Driving the Second Wave of Development Boom (Source: VBInsight)

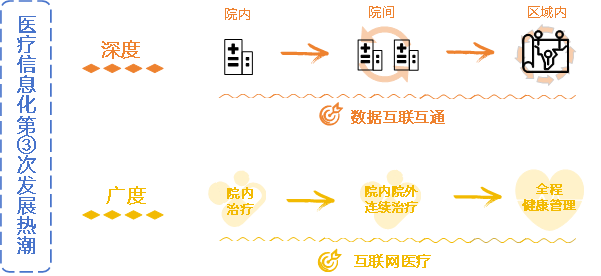

The Third Wave of Development: Building Smart Healthcare.In August 2018, the National Health Commission issued the "Guidelines on Further Promoting Informationization in Medical Institutions with Electronic Medical Records at the Core," emphasizing the need to promote interconnectivity among information systems across medical institutions, eliminate information silos, and achieve sharing and exchange of medical information both between institutions and within regions. At this point, digital intelligence was placed on the agenda, leveraging artificial intelligence technologies to efficiently facilitate mutual recognition of data, ushering in the third wave of development boom focused on data applications and the growth of internet hospitals.

Policies Spark a Development Boom Across Both Depth and Breadth

Defining Smart Healthcare from a Data Perspective.From a data perspective, the informatization, digitalization, and data-intelligence development of smart healthcare respectively focus on data generation, governance, and application, with an emphasis on full-lifecycle personal health record data.

Scope of Research on Smart Healthcare Development

Defining Smart Healthcare from the Perspective of Service Scope.The development of healthcare informatization continues to evolve, moving beyond the narrow scope of digitizing only medical service delivery. It now encompasses medical services, healthcare payment, pharmaceutical enterprise services, health management, and other sectors related to national population health. This broader ecosystem includes the construction and provision of services leveraging informatization, digitalization, and data-driven intelligence applications. In this report, our research covers this expansive definition of healthcare informatization, which we term “Smart Healthcare.”

Cloudification is the prevailing trend, and lower-tier markets may drive a second growth curve.

1High Homogeneity in Medical Information System Functions and Fierce Industry Competition

Under the rigid demand "guidance" of hospitals, product homogenization is high.For years, the Chinese government has attached great importance to the level of informatization in medical institutions, continuously issuing policies to clarify the direction of informatization development and specify concrete requirements. Medical institutions have actively responded to these policies by enhancing their informatization capabilities to meet grading and rating standards, and have diligently advanced their informatization initiatives in accordance with policy guidelines. In this context, the services and functionalities required of “essential” informatization application systems in medical institutions are transparent and increasingly standardized.

At that time, driven by demand, a large number of healthcare IT service companies flooded into the sector. To secure market positioning more rapidly, it became an obvious and advantageous development strategy to focus R&D efforts on addressing the common “essential needs” of medical institutions and bring these products to market. Consequently, core information systems applied to medical institution management have become highly homogeneous.

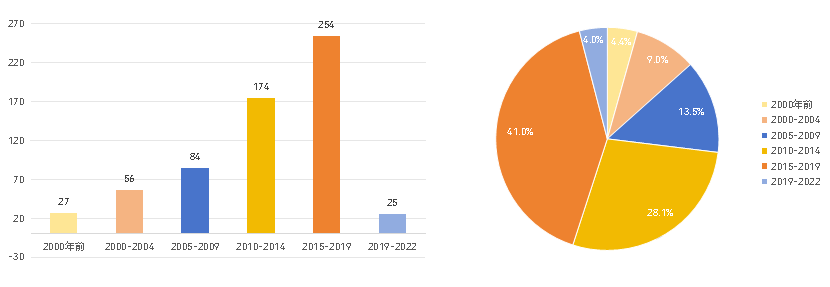

Channels Are King; Industry Competition Is Fierce.As of the end of 2022, there were 620 medical informatization service enterprises, according to incomplete statistics from the database.

Number and Proportion of Healthcare IT Service Enterprises Established in Each Year Interval (Data Source: VBInsight)

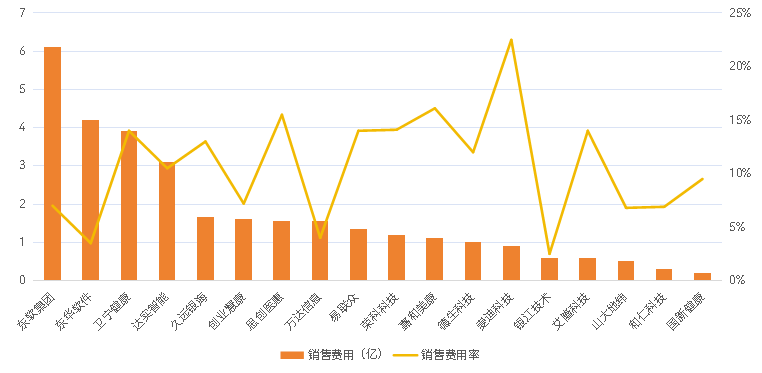

With a large number of enterprises and serious product homogenization, competition in China’s healthcare IT sector is fierce, with distribution channels playing a dominant role. This forces companies to increase their spending on marketing and sales. According to data from a report published by Great Wall Guorui Securities, enterprises focusing on information systems for medical institutions had an average sales expense ratio of approximately 12.50% in 2021, which is higher than the average level of the software and computer industry.

Analysis of Sales Expenses of Healthcare IT System Companies (Source: Wind, Company Announcements)

Amid intense industry competition, enterprises face rising sales costs and shrinking profit margins due to price wars, which will inevitably affect their sustained R&D investment and hinder the process of building product differentiation, thereby undermining their long-term development.

3Cloud Adoption Trends Are Clear and Increasingly Critical, Unlocking the Market Potential of Grassroots Healthcare Institutions

To break through the intense competition within the healthcare IT industry, enterprises should shift their service model from merely “meeting functional requirements for related applications” to a strategy focused on “tangible cost reduction and efficiency improvement for institutions,” with an emphasis on building product differentiation.

Aligning with the demands of smart healthcare development, leveraging innovative technologies to address critical implementation challenges.Currently, large healthcare institutions typically operate over one hundred information systems. This proliferation of systems entails substantial maintenance costs and poses the challenge of periodic, comprehensive system upgrades approximately every decade, which require construction investments ranging from tens of millions to hundreds of millions of yuan. Furthermore, as information systems expand, the dimensions of patient data increase and the overall data volume surges dramatically, necessitating significant additional investment in storage infrastructure for healthcare institutions.

In addition to costs, data security is another key challenge in infrastructure development, as equipment failures may lead to data corruption or loss. As the construction of smart hospitals continues to advance, such pain points will become increasingly prominent.

Cloud migration of information systems is an irreversible trend, with its importance continually growing.Against this backdrop, enterprises are closely aligning with the demands of smart healthcare development. While addressing the pain points of medical institutions, they are also seizing the opportunity to differentiate their products. Consequently, the industry is actively engaged in the research and development of next-generation information systems: cloud-based information systems.

Information systems deployed on public, private, or hybrid clouds significantly reduce maintenance costs compared to traditional information systems, while also saving on space and construction expenses for offline storage equipment. Moreover, the risks of data loss and corruption are substantially mitigated. Currently, as cloud infrastructure continues to improve, many enterprises have not only launched comprehensive cloud-based information systems but have also successfully implemented them, entering a phase of iterative upgrades.

Secondary and lower-level medical institutions are being gradually included in the scope of interoperability requirements.As China advances its healthcare informatization initiatives, the requirements for secondary and lower-tier medical institutions have become increasingly clear. Emphasis on data interoperability and sharing continues to clarify these requirements, thereby unlocking the market potential for informatization in secondary and lower-tier medical institutions. According to the *Statistical Bulletin on the Development of Health and Wellness Services in China 2022*, by the end of 2022, there were 11,145 secondary hospitals, 12,815 primary hospitals, 9,493 unclassified hospitals, and 979,768 grassroots medical and health institutions in China, indicating a vast market space for informatization.

SMEs Join the Construction of Grassroots Information Infrastructure.The surge in demand for IT infrastructure development among lower-tier medical institutions is not only creating a second growth curve for traditional healthcare IT enterprises but also presenting greater opportunities for local small and medium-sized IT firms. Notably, due to limited IT maturity and weak foundational infrastructure, grassroots digitalization efforts rely more heavily on vendors delivering tangible “outcomes” rather than merely supplying software systems. In other words, these institutions are more willing to pay for SaaS-based services that fulfill their digitalization requirements through the use of software, rather than simply purchasing licenses for software usage.

Therefore, localized enterprises that thoroughly understand local policies on information technology infrastructure and integrate them into their SaaS service delivery standards have gained certain advantages. For instance, Chongqing Tongbu Yuanfang, after completing system interface integration with the regional “Health Cloud” coordinated by the Health Commission, developed an integrated medical and public health platform tailored to the operational habits of primary care institutions. This platform encompasses software systems such as cloud-based HIS, LIS, PACS, electronic medical records, public health services, and family doctor contracts. Leveraging a highly standardized cloud platform as a bridge, it provides primary care institutions with medical informatics SaaS services that fully comply with policy requirements for data storage, governance, and application.

In the future, the industry will continue to closely align with policy directives and the evolving demands of healthcare institutions for informatization. By developing new products, iterating on existing ones, and innovating service models, it will establish differentiated advantages and competitive barriers, thereby better supporting the development of smart healthcare in China.

1Low Interoperability Maturity of Healthcare Institutions, Low Enterprise Concentration, and Prominent Medical Data Silos

The participation rate in the Interconnectivity Assessment has increased, but remains low overall.Hospital Interconnectivity builds upon the application of electronic medical records (EMRs) to break down information silos both among internal hospital systems and between different hospitals. As EMR adoption becomes increasingly widespread and mature, hospital interconnectivity has also been placed on the agenda.

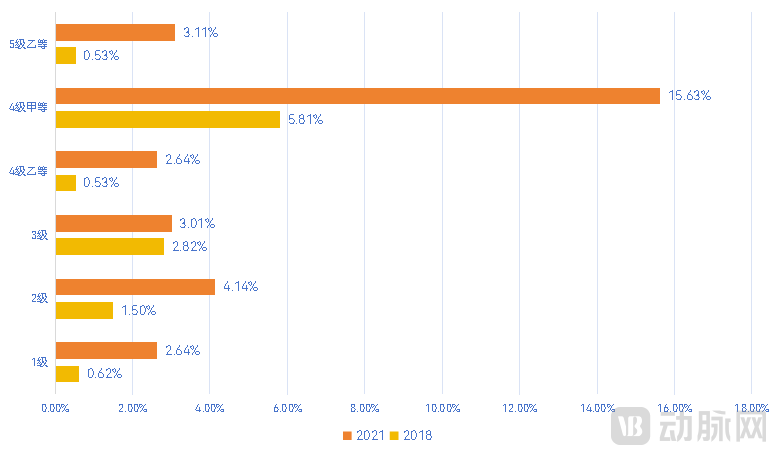

According to CHIMA’s survey, approximately 40% of hospitals participated in the Interconnectivity Maturity Assessment during the 2021–2022 period, compared to only about 12% in 2018. Excluding hospitals that did not participate or for which results were not yet available, the majority of hospitals with assessment results achieved Level 4 Grade A, with this proportion increasing year by year. The combined proportion of hospitals rated at Level 4 Grade B and above was 7.31%, 11.90%, and 21.37% in 2018, 2019, and 2021, respectively.

Hospital Participation in the Interconnectivity Standardization Maturity Assessment (Source: CHIMA)

Hospital Interconnectivity Assessment has been conducted since 2013, with ten batches completed to date. According to the National Health Commission, as of April 2024 (public announcement of the results of the 2022 National Medical and Health Information Interconnectivity Standardization Maturity Assessment), a total of 94 hospitals across China have been rated at Level 5 Grade B for interconnectivity, and 857 hospitals have achieved Level 4 Grade A or higher.

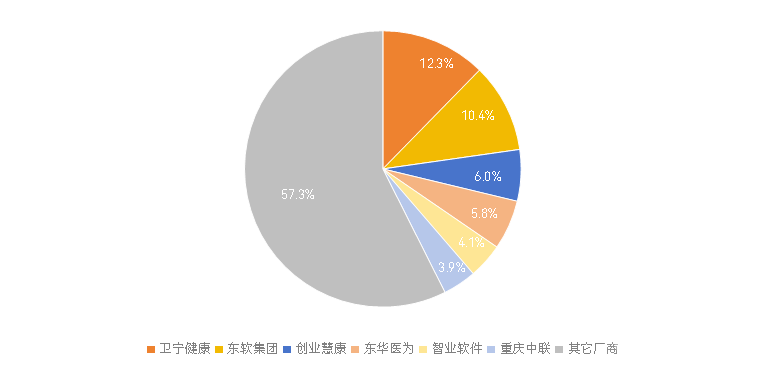

The overall corporate concentration is lower than the concentration in specific segments.From the perspective of market competition, the overall industry concentration is relatively low. According to IDC data, in China’s healthcare informatization sector in 2022, the market landscape among leading vendors providing core hospital information management systems is as shown in the figure: Winning Health, ranking first, held a 12.3% market share, and Neusoft held 10.4%. The combined market share of the top three players approached 30%, while that of the top six amounted to only 42.7%, less than half.

Market Share of Core Clinical System Vendors in Chinese Hospitals in 2022

The market concentration in key sub-sectors, such as medical big data, health insurance, and electronic medical records (EMR), is slightly higher than the overall industry average.In the field of medical big data solutions, represented by Yidu Tech, the market share of the top six companies stands at 45.3%; in the health insurance information systems sector, represented by Neusoft Group, the top six companies account for 59.9% of the market; and in the electronic medical records (EMR) domain, represented by Jiahe Meikang, the market share of the top six companies reaches as high as 69.1%.

The problem of information silos is prominent, and interoperability is the bottleneck.Achieving interoperability to break down "information silos" is a crucial measure for addressing the difficulties and high costs associated with accessing medical care. Realizing information sharing among hospitals can reduce redundant examinations, conserve social resources, lower medical expenses, and facilitate mutual referrals between medical institutions, with patients being the primary beneficiaries. However, due to the late introduction of national standards, hospitals lacked standardized guidance during the development of their information systems, resulting in severe "information silo" problems. Currently, numerous vendors have emerged in the healthcare informatics industry, creating a highly fragmented landscape characterized by a large overall market but dominated by many small enterprises.

2Interconnectivity Is Gradually Becoming a Mandatory Requirement, and Mutual Recognition of Medical Test Results Is Beginning to Be Implemented in Practice

Eliminating information silos and achieving interoperability of regional patient-provider data is not solely the responsibility of individual hospitals, nor is it merely a task for system vendors or software developers; rather, it requires concerted efforts from national health authorities, system providers, and hospital administrators.

Hospitals should strengthen top-level design to establish a comprehensive information system.In terms of medical interoperability and data application, if there is a lack of top-level planning during the process of connecting and integrating various systems, it will be difficult to effectively improve the level of system connectivity and data utilization. Furthermore, in addition to ensuring medical quality, hospitals need to support functions such as intelligent patient guidance, point-of-care settlement, mobile payments, and sharing of laboratory test results. The implementation of internet hospitals, which have rapidly emerged in recent years, also relies on more robust information systems.

In the process of digital transformation, mature solutions have emerged in the industry to help medical institutions leverage internet hospitals to implement functions such as appointment scheduling, intelligent triage, mobile payments, and sharing of laboratory test results, thereby enhancing their digital service capabilities. For instance, Naiterui, a company specializing in the development of internet hospitals and providing digital solutions for the broader health industry, has created an internet hospital solution integrated with various artificial intelligence tools. This solution enables medical institutions and enterprises across all segments of the health industry value chain to easily train and deploy specialized systems for online medical services, intelligent triage, rational drug use, and chronic disease follow-up. Furthermore, a variety of other solutions—including medical research platforms, online traditional Chinese medicine (TCM) consultation services, physician education programs, prescription circulation platforms, medical e-commerce, and AI-driven medical applications—have been widely adopted by more than 300 enterprises, facilitating their digital transformation.

Interoperability and data sharing are mandatory requirements in multiple provinces and municipalities, with some regions establishing incentive and penalty mechanisms.. Following the issuance of the “Opinions on Further Improving the Healthcare Service System” by the General Office of the Communist Party of China Central Committee and the General Office of the State Council, provinces and municipalities across China have successively formulated their local implementation plans. Among these, the implementation plans for further improving the healthcare service system in 17 provinces/municipalities/autonomous regions—namely Jiangxi, Yunnan, Fujian, Ningxia, Hunan, Chongqing, Guangxi, Qinghai, Guangdong, Hebei, Henan, Heilongjiang, Jilin, Inner Mongolia, Tianjin, Shanxi, and Sichuan—have frequently highlighted the interoperability and sharing of medical data. Under policy guidance and driven jointly by enterprises engaged in smart healthcare development, interoperability is accelerating into the practical implementation phase.

1High-quality data is the foundation of all applications, and the capitalization of data assets is gradually becoming a necessity.

The process of applying intelligent digitalization to medical data encompasses data ingestion, data governance, model training, application development, and application services. For different types of data, the governance process often presents distinct challenges and technical requirements.

Key to Imaging Data Governance: Identifying Imaging FeaturesIn 2023, Meta released the Segment Anything Model (SAM), which demonstrated robust image segmentation capabilities on natural images. However, due to characteristics such as indistinct object boundaries and high segmentation difficulty inherent in medical imaging, SAM’s performance in medical image segmentation has been unsatisfactory. Numerous research institutions both domestically and internationally have conducted in-depth academic studies based on SAM, aiming to apply it to the field of medical imaging. Models such as Medical SAM, SAM-Med2D, and MedSAM have achieved certain research breakthroughs, yet practical clinical deployment remains scarce. This is largely attributable to limitations in the quality of training data.

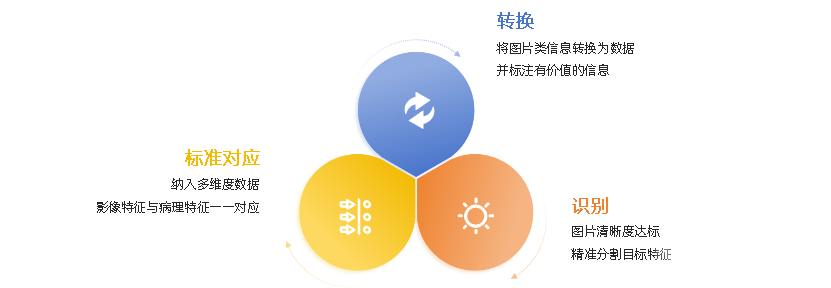

For imaging data, the standards for data storage formats are unified, making extraction and aggregation relatively straightforward. The primary challenge lies in transforming the features of image-based information into quantifiable metrics and then marking valuable features using standardized data to facilitate model training. Furthermore, the clarity of the images themselves is a critical factor influencing imaging quality. Additionally, a significant difficulty in imaging data governance is establishing precise one-to-one correlations between fragmented imaging data and other physiological indicators to extract valuable features and assess health status.

Challenges in Medical Image Data Processing

To address this pain point, the industry has made numerous attempts at solutions, and mature offerings have already emerged. For instance, Neusoft Group began by ensuring image clarity through quality control systems for imaging equipment. It then integrated expert consensus and incorporated hospital-wide data for comparative analysis to create its own high-quality, annotated medical image database. Leveraging SAM as the foundational large model and adopting a “pre-trained large model + task-specific fine-tuning” approach, Neusoft developed the Medical Image Segmentation Model (MISM) in April 2023. MISM improved medical image segmentation accuracy by more than 30% compared to SAM and helped healthcare professionals increase their work efficiency by 30 to 40 times.

Challenges in Text Data Governance: Terminology Alignment.In addition to imaging data, another major category of clinical data is textual data. Unlike imaging data, textual data lacks a uniform format and is unstructured in nature; individual healthcare providers often have their own preferred expressions for the same medical terms, resulting in medical records that primarily exist as large blocks of unstructured text. Therefore, the key challenges in governing textual data lie in identifying and normalizing varying expressions of the same term into a standardized representation, as well as extracting structured information from extensive unstructured medical records. Among these tasks, establishing terminology standards and rapidly identifying and mapping textual content to the corresponding standards constitute the core components.

In the process of establishing terminology standards, close collaboration with experts from various clinical specialties is essential. It is necessary to fully understand the language usage habits of clinical healthcare professionals and distill a common terminology database from them, thereby creating industry-recognized terminology standards that serve as the foundation for data cleaning and classification. Meanwhile, the rapid text identification phase tests the ability to leverage artificial intelligence technologies to enhance both the accuracy and speed of recognition.

Text data governance requires technological prowess, accumulated experience, and clinical expertise, all of which are indispensable. As one of the first companies to enter the text data governance arena leveraging artificial intelligence technologies such as natural language processing and knowledge graphs, Yidu Tech has collaborated with industry experts and disease alliances to establish and publish 19 disease data standards, addressing the issue of non-standardized data. Furthermore, based on its self-developed vertical-domain large language models and validation through high-quality real-world studies, the company continuously iterates and enhances its technical capabilities in medical record understanding. As of September 2023, YiduCore had been authorized to process and analyze over 4 billion medical records for more than 900 million patients.

It is evident that the challenges in governing different types of medical data vary significantly in the process of assetizing medical data. This requires an organic integration of technology and domain expertise, and there is no one-size-fits-all solution. Therefore, a common development model for enterprises is to focus on achieving breakthroughs in specific niche areas, whereas a comprehensive, all-encompassing approach poses greater tests to a team’s financial resources and R&D capabilities. Currently, the assetization of medical data, namely the establishment of high-quality medical databases, has gradually become a critical necessity for healthcare institutions, research societies, pharmaceutical and medical device companies, and public health regulatory authorities.

2Keeping pace with market demand, an increasing number of AI-driven commercial application scenarios are being validated.

Currently, the digital and intelligent application of medical data has gradually completed market validation across multiple scenarios, with healthcare institutions and pharmaceutical companies being the two most mature areas.

Addressing the requirements for scientific research and high-quality development in healthcare institutions from multiple perspectives.For healthcare institutions, the most critical demand for high-quality data stems from the research needs of physicians and specialists, as well as the institutional requirements to meet evaluation criteria for electronic medical record (EMR) grading and smart hospital development. To address these two prominent demands, the construction of databases at both the departmental and hospital-wide levels serves as the foundational solution. Building on this foundation, digital-intelligence applications powered by artificial intelligence and large language models will assist hospital experts and administrative leaders in fulfilling their research and management objectives.

Currently, mature service providers in the field of digital intelligence applications can be broadly categorized into two types. The first type leverages its robust foundation in traditional information system construction to vertically expand its capabilities in smart healthcare development, covering the entire spectrum from data collection and governance to final digital-intelligent applications. Benefiting from the establishment of comprehensive data collection systems, these companies possess a thorough understanding of physicians’ usage patterns, diagnostic and treatment habits, and their requirements for research data applications. They are also intimately familiar with the management processes and application needs of medical institutions. These insights constitute a key advantage in guiding data governance and digital-intelligent applications, enabling the distillation of common needs across various scenarios into standardized application products. This approach significantly reduces detours in product research and design, better meets clinical demands, shortens product delivery cycles, and substantially enhances product competitiveness.

As a leading enterprise in healthcare IT, Neusoft Group has consistently enhanced its product capabilities guided by clinical needs and is committed to driving reforms in healthcare delivery models through AI within an innovative ecosystem for monetizing medical data. The company’s solutions for unlocking the value of medical data meet the integrated data requirements of “three-in-one” smart hospitals, facilitating high-quality development for large medical institutions, closely integrated medical consortia, and healthcare groups. Furthermore, by proactively positioning itself in the sector of innovative health insurance payment mechanisms, Neusoft leverages AI to promote comprehensive patient screening and management, shifting the focus from “treatment” to “prevention,” thereby helping health insurance funds address cost containment at its root.

Furthermore, another highly representative service provider has entered the field of intelligent digital applications for medical data by leveraging advanced artificial intelligence technologies. Capitalizing on their robust technical capabilities, these companies possess inherent advantages in processing and identifying multi-source heterogeneous data from healthcare institutions. They rapidly master the storage and upgrade logic of data originating from diverse medical information systems through AI, thereby enabling the precise and efficient construction of high-quality databases. Moreover, grounded in a deep understanding of data applications, they can swiftly translate descriptive requirements from clients into “technical language,” guiding the development of specific digital-intelligence products and meeting the needs for intelligent digital applications of medical data with superior user interaction experiences.

As a leading enterprise in this sector, Yidu Tech has consolidated its top-tier position in the development of high-quality medical databases and continues to explore a commercial closed-loop for AI-driven data applications. Currently, in the field of intelligent medical data applications, its scientific research and smart hospital construction services cover more than 1,700 medical institutions. It has also built regional platforms, public health systems, urban “Health Brains,” and electronic health records for residents for 38 regulatory agencies and policymakers. The Huiminbao (inclusive supplementary medical insurance) services developed by Yidu Tech have cumulatively covered 12 cities across 4 provinces. Furthermore, in the field of drug R&D, the company serves 131 active life sciences clients, helping them achieve significant cost reductions and efficiency improvements.

Pharmaceutical companies represent a prime scenario for commercialization, with R&D and marketing being the key components.Beyond healthcare institutions, another advantageous scenario for the commercialization and implementation of data assets is within pharmaceutical companies. As is well known, drug development is characterized by high investment, high risk, long cycles, and low success rates. Consequently, there is a strong demand for the intelligent application of medical data in the R&D phase. Coupled with their substantial financial capacity, this makes drug R&D a prime area for practical implementation.

Currently, smart healthcare construction service enterprises are leveraging technology to promote the application of high-quality databases, assisting pharmaceutical companies in reducing costs and improving efficiency across the entire drug R&D process—including drug design, clinical trial protocol design, feasibility validation, clinical trials, and data analysis. These efforts have already yielded significant results. Such applications are rapidly maturing and have become a key source of revenue and cash flow, constituting a competitive advantage for medical data service providers.

Furthermore, under the combined pressures of centralized drug procurement, codes of conduct for pharmaceutical sales representatives, and anti-corruption campaigns in the healthcare sector, pharmaceutical companies face an imperative need to reduce costs and enhance efficiency in their marketing operations. In addition to leveraging technology to optimize traditional sales processes, the maturation of online prescription issuance, medication delivery, and digital marketing via internet hospitals has given rise to emerging direct-to-consumer (DTC) health product marketing models, offering pharmaceutical enterprises new pathways to achieve cost reduction and efficiency gains.

In this field, Knightree, leveraging its expertise in internet healthcare and artificial intelligence, offers digital-intelligence solutions. By serving as a bridge through its independently developed internet hospital service system with full intellectual property rights, it provides connectivity services for the broader health industry. It builds new digital infrastructure for pharmaceutical and medical device companies, insurance firms, and other stakeholders, shaping new online marketing models, facilitating expansion into lower-tier markets, and ultimately boosting product sales. Furthermore, as an industrial middle platform, Knightree enables deep B2B industrial resource linkage, comprehensively helping enterprises reduce costs and improve efficiency.

In the future, the application value of medical data assets will be continuously explored, and commercial implementation scenarios will gradually increase. This will revolve around dimensions such as helping healthcare institutions operate more efficiently and with higher quality, enabling patients to access medical care more conveniently and precisely, assisting enterprises in achieving extreme cost reduction and efficiency improvement, and allowing relevant regulatory authorities to monitor situations in real time and make informed decisions.

Three Breakthrough Directions for the Dilemmas of Traditional Informatization: New Products, New Technologies, and New Services

Reward and penalty mechanisms related to interoperability will continue to improve, with industry associations potentially playing a key role in their promotion.

Technology-Driven, Demand-Guided: The Practical Application of High-Quality Database Value Is Gradually Being Realized

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1: Policy, Demand, and Technology Drive the Evolution of Medical Informatics Toward Smart Healthcare

1.1 Policy-Driven Three Waves of Development Surge, Leading the Upgrade of Healthcare Informatics

1.2 Rising Demand for Healthcare Services Drives the Development of Smart Healthcare

1.3 Continuous Integration of Innovative Technologies Lays the Foundation for Smart Healthcare Development

Chapter 2: Cloud Adoption Is an Irreversible Trend, with the Lower-Tier Market Potentially Driving a Second Growth Curve

2.1 High Degree of Functional Homogenization in Medical Information Systems and Fierce Industry Competition

2.2 Insufficient Motivation Among Healthcare Institutions and Sluggish Corporate Innovation Are Key Causes

2.3 Cloud Adoption Trends Are Clear and Increasingly Important, Unlocking the Market Potential of Lower-Tier Healthcare Institutions

Chapter 3: Data Silos Are the Key Bottleneck, Making Interconnectivity Increasingly Urgent

3.1 Low Interoperability Maturity of Healthcare Institutions and Low Enterprise Concentration, Highlighting the Prominence of Medical Data Silos

3.2 The Lack of Standards for Multi-Source Heterogeneous Data and the Significant Advantages of Enterprise Localization Are Key Reasons

3.3 Interconnectivity Is Gradually Becoming a Mandatory Requirement, and Mutual Recognition of Medical Test Results Is Beginning to Be Implemented in Practice

Chapter 4: Data Assetization Becomes a Necessity, with Value-Driven Applications Achieving Commercial Deployment Across Multiple Scenarios

4.1 Artificial intelligence and big data technologies are the core technologies of digital-intelligent transformation, currently in the early stages of application

4.2 High-quality data is the foundation of all applications, and data assetization is gradually becoming an essential requirement

4.3 Keeping Pace with Market Demand: An Increasing Number of Digital and Intelligent Commercial Application Scenarios Are Being Validated

Chapter 5 Future Trends

5.1 Three Major Breakthrough Directions for the Dilemmas of Traditional Informatization: New Products, New Technologies, and New Services

5.2 Incentive and Penalty Mechanisms for Interconnectivity Will Be Further Refined; Industry Associations May Leverage Their Influence to Promote Adoption

5.3 Technology-Driven, Demand-Guided: Value-Added Applications of High-Quality Databases Are Gradually Being Implemented

Chapter 6 Enterprise Cases

6.1 Naiterui: Leveraging Internet Hospitals as a Service Bridge to Become a Connector in the Big Health Industry

6.2 Yidu Tech – Continuously Improving the Commercial Closed Loop of Data Applications Based on Leading Data Processing Technology

6.3 Neusoft Group: AI-Driven Transformation of Healthcare Models, Leading an Innovative Ecosystem for the Valorization of Medical Data

Special Acknowledgments (in order of interviews):

Mr. Qu Yi, Chairman and CEO of Naiterui; Ms. Zheng Xinlan, Strategic Expert at Yidu Tech; Mr. Xia Ruobing, Head of the Real-World Insights and Consulting Business Department at Yidu Tech; Dr. Li Linfeng, Vice President of Technological Innovation and AI Architect at Yidu Cloud, a subsidiary of Yidu Tech; Dr. Zhang Xia, Dean of the Neusoft Intelligent Medical Technology Research Institute; Mr. Peng Chengbao, Deputy Dean of the Neusoft Intelligent Medical Technology Research Institute and Director of the Platform Engineering Research Center; and Dr. Cai Wei, Director of the Medical Information Engineering Laboratory at the Neusoft Intelligent Medical Technology Research Institute.

Please scan the QR code to add our assistant and obtain the full report. If you have already added the assistant, please proactively reach out to request it.

The report will be released on-site at the Internet Hospital and Smart Hospital Forum of VCBeat’s “8th Future Healthcare Ecosystem Expo.”