Not All Biotechs Need to Survive: Industry Reset Amid Wave of Failures and Strategic Exits

Walking Fish Therapeutics

B Cell Therapy Developer

Rubius Therapeutics

Developer of Novel Therapeutics

Impel

Drug Delivery Device and Drug Developer

Bankruptcy has always been a taboo subject. News of a biotech company’s bankruptcy often spreads first through private channels in veiled terms. Even with the specific company name redacted, details such as its business focus and location quickly reveal which biotech firm has reached its breaking point, sparking a wave of lamentation alongside mentions of liquidation, layoffs, and asset sales.

Jeremy Jonker, co-founder of Infinity Ventures, once stated that business failure is the most opaque aspect of the current commercial landscape: “More than one million businesses fail in the United States each year, yet this topic remains a taboo.”

Data from S&P Global Market Intelligence shows that the number of U.S. biotech companies filing for bankruptcy in 2023 reached a new high since 2010. According to data from the U.S. Securities and Exchange Commission (SEC), as many as 41 biotech companies declared bankruptcy in 2023.

In China, the first biotech company to file for bankruptcy liquidation this year emerged: on January 12, Boji Biologics formally submitted a bankruptcy liquidation application to the Yuhang District People’s Court in Hangzhou. Subsequently, on February 13, LianBio (LIAN.US), a biotech firm listed in the United States, announced that it would begin scaling back its operations and delisting, with all activities related to its cessation of operations to be completed by the end of 2024. Then, in March, CGT company Landun Biologics publicly solicited appraisal agencies to formally advance the bankruptcy liquidation process, despite having received approval for Phase I clinical trials of its CAR-T pipeline just last year.

Since last year, major domestic biotech parks have seen a surge in vacancy rates. Parks that once struggled to meet demand are now lowering rents to retain tenants. Amid a decline in new company formations and downsizing among existing firms, a leasing manager at one biotech park described the previously bustling hub as “having been hollowed out,” adding that “KPI pressures are also significant.” Companies that have left did so in large groups, often involving dozens of employees, yet under the current climate, it is difficult to attract new tenants of comparable scale.

This also suggests that bankruptcy or cessation of operations among biotech firms will not be an isolated incident. Although there are early signs of improvement in the current biotech financing market, active capital remains limited, and many companies are still struggling to survive.However, we should not view the successive bankruptcies of biotech companies as a collapse of the industry.

Bankruptcy Is a Necessary Component of the Biotech Ecosystem

The biotechnology industry is characterized by nonlinearity, making the innovation process difficult to predict. The performance of biotech companies is particularly binary, as clinical trial outcomes often determine the success or failure of drug developers. Typically, compared with other industries, biotech represents the most challenging asset class to manage and boasts the “poorest” business model, owing to its high complexity, lengthy R&D cycles, and stringent regulatory environment.

In recent years, competition in biotech innovation has intensified, with the “low-hanging fruit” becoming increasingly scarce. Taking cancer as an example, many challenges have become more difficult to overcome than in the past, and similar situations are emerging in fields such as autoimmune diseases. Biotech companies must continuously develop innovative technologies to address increasingly complex medical challenges and compete against a growing number of rivals.

If the technology validation process encounters setbacks, a biotech company may face a dead end.

Just days ago, Walking Fish Therapeutics, a biotech company specializing in engineered B-cell therapies, filed for bankruptcy and ceased operations. The founder stated that a key reason for the bankruptcy was “the sudden withdrawal of major investors, which left the company insufficient time to secure new funding, while prior financing rounds were inadequate to sustain future operations.” With its most advanced pipeline asset still only at the Investigational New Drug (IND) stage, it is both an unfortunate yet understandable outcome that this biotech firm, lacking near-term prospects for clinical translation, was abandoned by investors.

For another example, Rubius Therapeutics set a record for the largest IPO at the time of its public listing in 2018. The company developed multiple red blood cell therapy candidates targeting cancer, autoimmune diseases, and inherited metabolic disorders. However, due to unconvincing clinical data, red blood cell therapy was questioned as an ineffective technological approach, ultimately leading to Rubius’s shutdown in early 2023.

Even biotech companies that have entered the commercialization stage cannot afford to relax.

Earlier this year, Impel Pharmaceuticals filed for bankruptcy. Its acute treatment for adult migraine, Trudhesa, received FDA approval and generated tens of thousands of prescriptions. However, Trudhesa failed to meet its commercial expectations, leaving the company without sufficient funding to support its subsequent pipeline. Despite Impel’s efforts to explore various alternatives—including the sale of assets, a full company sale, mergers, or other strategic transactions—the biotech ultimately sought Chapter 11 bankruptcy protection.

And normal clearance.Just as the TMT era once saw a surge of startups claiming they would become the next major platform, the rise of China’s biotech boom has likewise spawned countless companies aspiring to lead the innovative drug industry.

“At that time, many companies claimed they were aiming to develop First-in-Class drugs. Later, it became clear that achieving Best-in-Class status was already a remarkable feat. Now, looking back, many companies have ended up producing Me-Worse products,” said an investor.

Some projections suggest that the survival rate of biotech companies in China’s primary market will be approximately 5–10%.

This is not necessarily a bad thing. From a macro perspective, bankruptcy acts as a “purifier” within the entrepreneurial ecosystem. By eliminating uncompetitive enterprises, it creates space for the development of new companies, reallocates resources and talent to more productive uses, and provides warnings or insights for the operations of other firms. Although bankruptcy is an undesirable outcome for all parties involved, it does not entail exclusively negative consequences in terms of maintaining the vitality of the biotech ecosystem.

Dignified Bankruptcy: A Technical Skill

Recent business registration information for a bankrupt domestic biotech company reveals that it is embroiled in over 110 judicial cases, with causes of action including disputes over sales contracts, construction project contracts, service contracts, and labor disputes. Meanwhile, the company’s legal representative has been subject to 30 orders restricting high-level consumption.

Moreover, shareholder accountability claims and the triggering of valuation adjustment mechanisms (VAMs) can plunge founders into an abyss.

This state of “chaotic entanglement” and the panic over “unlimited personal joint and several liability” will leave other biotech companies and the entire industry feeling uneasy.

When facing bankruptcy, U.S. biotech companies may undergo a scenario known as a "quick life-or-death decision." This approach primarily involves an expedited liquidation procedure under the U.S. Bankruptcy Code, wherein the company filing for bankruptcy first petitions the court for Chapter 11 bankruptcy protection.。

Chapter 11 allows companies to restructure their debts while continuing operations, and also triggers an “automatic stay” to prevent creditors from taking action to seize the company’s assets. This provides the company with a breathing space, free from the concern that key assets will be stripped away.

Once the assets are sold and the debts repaid, the company may declare its legal “death,” i.e., dissolution, or, in some cases, continue to survive through restructuring if economic conditions permit.

This expedited liquidation process is typically swift, with asset valuation, asset sales, and debt repayment usually completed within months of the bankruptcy filing. It reduces legal and administrative costs, facilitates rapid corporate restructuring or liquidation, and minimizes the impact on creditors and investors to the greatest extent possible. This approach is suitable for biotech companies experiencing severe cash flow disruptions, unable to maintain normal operations, and in need of a prompt resolution to their debt issues.

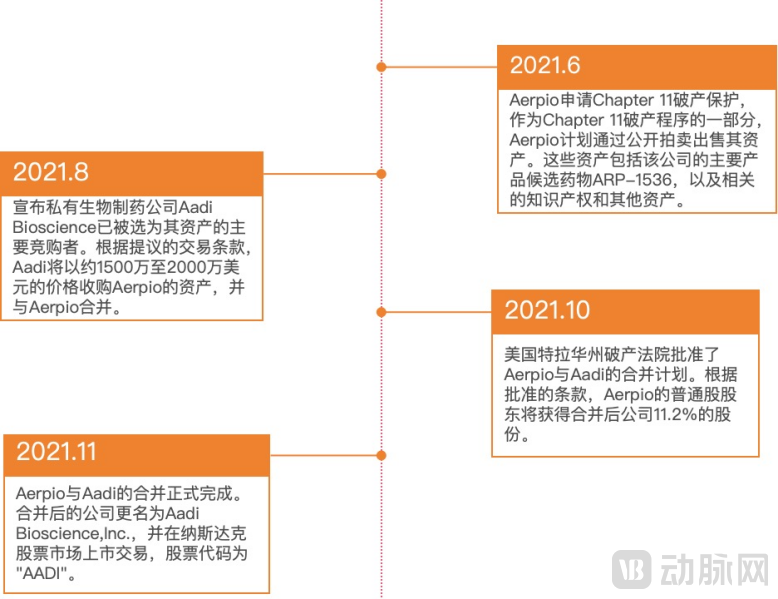

In this way, companies can quickly “save themselves” or make an orderly “exit,” minimizing the impact of bankruptcy on all stakeholders. Impel Pharmaceuticals, mentioned earlier, filed for Chapter 11 bankruptcy protection. In fact, since the pandemic, several U.S. biotech companies have opted for Chapter 11 bankruptcy protection due to unsustainable debt accumulation, including rare disease therapy company Permeon Biologics, metabolic disorder therapy company Vivus, and vascular disease drug company Aerpio Pharmaceuticals.

Aerpio Files for Chapter 11 Bankruptcy Protection | Graphic by VCBeat

From the perspective of Aerpio’s bankruptcy protection proceedings, although Aerpio no longer exists as an independent company, its assets and technology have continued to develop through the newly merged entity. For Aerpio’s shareholders, the value of their original shares has significantly diminished; while this outcome is far from ideal, they have received a certain equity stake in the post-merger company.

Some biotech companies that still hold certain assets may be eligible for state-law “out-of-court bankruptcy” procedures—specifically, an Assignment for the Benefit of Creditors (ABC)—whereby the company’s assets are transferred to creditors for disposition.

The ABC process generally does not involve restructuring and is not subject to federal court supervision, offering a more agile and streamlined approach. More importantly, the ABC process is confidential, whereas bankruptcy is often associated in the public mind with failure and financial distress. Therefore, opting for an ABC may have a lesser impact on the company’s reputation and impose a lighter burden on the management and board of directors of the biotech firm.

When Biotech startups fail, a well-functioning bankruptcy system is crucial.Entrepreneurs can exit quickly, decently, and at low cost, allowing them to devote their time and energy to new career opportunities. A protracted and complex bankruptcy process not only excessively drains entrepreneurs’ resources but also risks labeling them as “failures.”

Meanwhile, fast and efficient bankruptcy proceedings also serve as an important safeguard for biotech investors.If bankruptcy proceedings are protracted, investors’ losses could widen further, exacerbating risk aversion toward the biotech industry and creating a vicious cycle.

Furthermore, one of the defining characteristics of the biotech industry is that its patents and pipeline assets may still regain vitality following restructuring or change of ownership. Proper disposition of bankrupt companies can provide more promising projects with the opportunity to continue development, which is crucial to the new drug R&D ecosystem.

Not All Biotech Companies Need to Survive

Last year, four companies incubated under the Flagship model went bankrupt in succession, leading the market to believe that this approach to pursuing biotech innovation was “no longer effective.” However, Flagship itself does not expect all of its portfolio companies to survive. Like most venture capital firms, its logic—centered on identifying cutting-edge technologies, assembling teams, and applying rigorous funnel-style screening—is predicated on the expectation that the majority of biotech startups will ultimately fail.

Flagship also provides a sufficient sense of security when persuading talent to join or lead startup biotechs: it paints an appealing vision of entrepreneurship while ensuring a safety net, so that even in the event of failure, their successful career trajectories will not come to an abrupt halt.

By leveraging adept financing strategies, Flagship often exits its positions entirely before a biotech company encounters difficulties. This is how Flagship generates profits and how it enables science to deliver value.

Therefore, the market need not demand that every biotech company carry a major life sciences mission and persevere through the winter.

The unique characteristics of the biopharmaceutical industry place greater moral and ethical pressures on Biotech entrepreneurs compared to those in other sectors. With a shortage of long-term capital on the funding side and limited options on the payment side, it is exceedingly difficult for Chinese Biotech companies to deliver more, better, and newer products under such dual constraints. Companies and founders who struggle to survive despite diligent efforts under these challenging conditions should not be subjected to excessive criticism, nor should their plight be met with lamentations accompanied by the dismissive remark that “the industry is failing.”

Companies that seek to profit from chaos and founders who use entrepreneurship as a pretext for rampant cash-grabbing should be acceleratedly eliminated, or even blacklisted by the industry. Fortunately, as China’s biopharmaceutical sector gradually gets on track, the true nature of many “shoddy operators” has been exposed.

Chinese biopharmaceuticals are at their best in history. The company’s gradual clearing out is not a defeat of Biotech, but the beginning of a new chapter for Chinese Biotech.