East China Medicine Reports Revenue Surge Beyond RMB 40 Billion, Announces RMB 1 Billion Dividend Plan

Huadong Medicine

Large Comprehensive Pharmaceutical Product Developer

Recently, Huadong Medicine issued an announcement,Announced a cash dividend of RMB 5.8 for every 10 shares to all shareholders, with a total distribution of RMB 1.018 billion.。

The announcement immediately sparked intense debate within the industry. After all, in recent years, amid a market winter, the sector has been dominated by negative news such as bankruptcies, layoffs, and losses, with the term “dividends” rarely seen—except perhaps as a strategic goal. Recently, Zhu Xiaohu, Managing Partner at GSR Ventures, remarked in an interview with media outlets, “Times have changed; today, demanding dividends has basically become the consensus among the vast majority of early-stage VCs.。”

Figure 1.Ranking of 14 Pharmaceutical Companies with Dividend Plans Exceeding RMB 1 Billion (Data Source: China Newsweek)

Figure 1.Ranking of 14 Pharmaceutical Companies with Dividend Plans Exceeding RMB 1 Billion (Data Source: China Newsweek)

This is undoubtedly correct, but achieving immediate dividend payouts is no easy feat. According to data statistics from Wind,As of April 25, only 14 listed pharmaceutical companies had proposed dividend distributions exceeding RMB 1 billion., and among these 14 pharmaceutical companies, three saw their dividend payouts decline year-on-year by more than 50%. Nevertheless, the fact that they are still distributing dividends is considered favorable; many other pharmaceutical firms have explicitly stated they will not pay dividends this year, with their last dividend distributions dating back to the pre-pandemic era.

Without comparison, there is no harm. Amid the market winter, Huadong Medicine has managed to significantly increase its dividend payout by two-fold this year, breaking through the 1 billion yuan mark for the first time, which is truly commendable. However, amidst the excitement, a question arises:What Exactly Does Huadong Medicine Rely on to Make Money?

Breaking the 40 Billion Mark for the First Time, Quietly Claiming the Crown

The confidence in “dividend distribution” naturally stems from business performance.

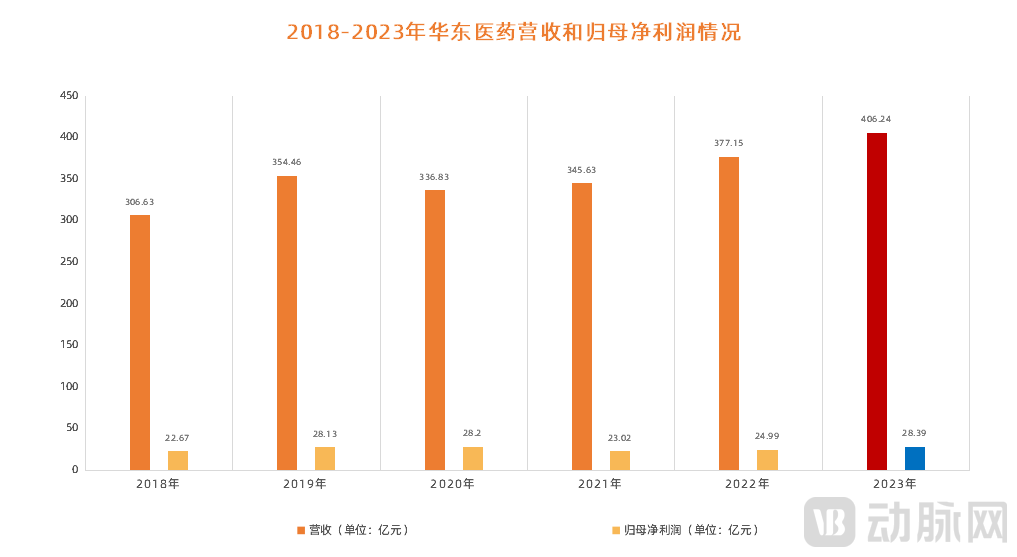

Figure 2. Revenue and Net Profit Attributable to Shareholders of Huadong Medicine, 2018–2023 (Source: Huadong Medicine Annual Reports)

Figure 2. Revenue and Net Profit Attributable to Shareholders of Huadong Medicine, 2018–2023 (Source: Huadong Medicine Annual Reports)

According to the annual report, Huadong Medicine achieved a total revenue of RMB 40.624 billion in 2023, a year-on-year increase of 7.71%; the net profit attributable to shareholders of the parent company was RMB 2.839 billion, up 13.59% year on year; and the net profit attributable to shareholders of the parent company after deducting non-recurring gains and losses was RMB 2.737 billion, representing a year-on-year increase of 13.55%.The company described this annual report, which showed growth in both revenue and net profit, as its “best performance in history.”。

So, where does the “money” come from?

It is reported that Huadong Medicine has four major business segments: pharmaceutical manufacturing, pharmaceutical distribution, medical aesthetics, and industrial microbiology. In 2023, their respective revenues were RMB 12.217 billion, RMB 26.981 billion, RMB 2.447 billion, and RMB 525 million. It is evident from these figures that pharmaceutical distribution is the largest revenue contributor, accounting for more than half of the total revenue. However, its net profit was only RMB 431 million, contributing modestly to the overall profitability. AndIt is the pharmaceutical manufacturing segment that truly shoulders the burden of profitability. According to the annual report, this business segment achieved a net profit attributable to shareholders of RMB 2.33 billion in 2023, accounting for as high as 85% of the total profit.。

Specifically, within the pharmaceutical industry segment, Huadong Medicine focuses on three core therapeutic areas: oncology, endocrinology, and autoimmune diseases. In the field of oncology, Huadong Medicine has established a portfolio of more than 30 innovative drug products, including targeted small-molecule chemical drugs, antibody-drug conjugates (ADCs), antibodies, and PROTACs. Many of these products received successful approval in 2023. For instance, the marketing authorization application in China for mirvetuximab soravtansine for injection, a first-in-class ADC novel drug licensed from ImmunoGen, was formally accepted in October 2023. Additionally, mivociclib, a Class 1 new drug, was included in the Breakthrough Therapy Designation program in May 2023.

Huadong Medicine has also demonstrated strong performance in the endocrinology sector. On March 30, 2023, the marketing authorization application for Liruluping®, indicated for glycemic control in adults with type 2 diabetes mellitus, was officially approved. As a result, Liruluping® became the first domestically produced liraglutide injection approved for the treatment of diabetes in China. In addition, several GLP-1 products achieved breakthrough progress in 2023; for instance, HDM1002, an orally administered small-molecule GLP-1 receptor agonist independently developed by the company, received Investigational New Drug (IND) approval from both Chinese and U.S. regulatory authorities in May 2023 for the indication of diabetes.

Lastly, mention must be made of the autoimmune disease sector, which has been Huadong Medicine’s most rewarding business segment. In March this year,“China’s No. 1 Autoimmune IPO” Quanxin Biologics Officially Lists on the HKEX; Prior to Its Listing, Huadong Medicine Was Its Second-Largest Shareholder with a 17.09% Stake. In addition to equity investment, Quanxin Bio has also licensed the domestic commercialization rights of QX001S, its clinical candidate with the most advanced development progress, to Huadong Medicine. Reportedly, QX001S is the first domestically produced ustekinumab biosimilar for which a marketing authorization application has been submitted in China, indicating considerable commercial potential.

Therefore, in retrospect, the logic behind Huadong Medicine’s ability to rapidly monetize its pharmaceutical manufacturing segment boils down to two points:First, it has seized opportunities in the field of major diseases; second, it is capable of rapidly entering the market through various means, including but not limited to in-licensing, mergers and acquisitions, equity investment, or licensing commercialization rights.。

However, what has truly propelled Huadong Medicine into the spotlight in recent years is its medical aesthetics segment, which has indeed become a significant revenue growth driver for the company in recent years.

According to the annual report, Huadong Medicine’s medical aesthetics segment achieved a total revenue of RMB 2.447 billion in 2023, representing a year-on-year increase of 27.79%. Among this, Sinclair Aesthetics, its wholly-owned subsidiary in China, recorded cumulative revenue of RMB 1.051 billion, up 67.83% year on year. In the international market, its wholly-owned UK subsidiary, Sinclair, generated sales revenue of approximately RMB 1.304 billion, a year-on-year increase of 14.49%.

At the product level, Huadong Medicine currently offers 38 high-end international aesthetic medical products featuring “minimally invasive and non-invasive” technologies. Among these, 24 products have been launched both domestically and internationally, while 14 global innovative products are under development. The product portfolio covers mainstream non-surgical aesthetic medical fields, including facial fillers, facial cleansing, and thread lifting. Notably, Ellansé (commonly known as “Girl’s Needle”), a poly-ε-caprolactone microsphere-based facial filler for injection, has made a significant contribution to performance. By the end of 2023, the number of officially partnered hospitals for this product had exceeded 600.

Of course, the story of Huadong Medicine’s performance growth is far from over. Specifically, in its traditional business segment, most of Huadong Medicine’s core products have already undergone price reductions under the centralized procurement program. In the coming years, market pressures on existing products and those not yet included in centralized procurement will gradually ease. Furthermore, the two emerging business segments—innovative drugs and medical aesthetics—hold substantial growth potential. Taking innovative drugs as an example, by the end of 2023,Huadong Medicine’s Innovative Product Pipeline Exceeds 60 Items, among which six innovative products are expected to achieve commercial success in 2024; additionally, in the medical aesthetics segment, the company’s current revenue is nearly on par with Imeik, the market leader in China. Furthermore, its domestically self-operated medical aesthetic products achieved profitability for the first time in 2023 and are poised to enter a harvest phase in the near future.

Amid the Wave of Transformation in the Pharmaceutical Industry, Why Did Huadong Medicine Take the Lead?

In recent years, driven by the triple forces of technological advancement, intensifying competition, and policy guidance, many domestic pharmaceutical companies have joined the wave of innovative transformation. A typical manifestation of this trend is that the number of new drug clinical trial applications has repeatedly hit record highs. Moreover, a review of the annual reports of major pharmaceutical companies readily reveals that“Transformation” has now become the common choice for the sustainable development of domestic pharmaceutical companies。

However, the path of “transformation” is not easy, with numerous cases of companies becoming trapped instead. The reasons are manifold, such as choosing the wrong direction, implementing an incomplete transformation, or allowing corporate ambitions to outstrip actual capabilities. When a “diversification” strategy fails to deliver tangible performance results, it inevitably leads to continuous profit margin compression, and even dire straits such as losses or bankruptcy.

So, as a typical success story, what exactly did Huadong Medicine do right on its transformation journey?

First and foremost, one must possess a keen sense of smell to stay closely aligned with industry hotspots.It is reported that Huadong Medicine had already made strategic moves in the medical aesthetics sector before its explosive growth. With the rising popularity of GLP-1 therapies, which align perfectly with Huadong Medicine’s core focus, the company swiftly secured approval for the first liraglutide injection in China. In 2023, as antibody-drug conjugates (ADCs) gained global prominence, Huadong Medicine remained highly active, obtaining NMPA approval for an investigational new drug (IND) application for a new indication of its globally first-in-class ADC, mirvetuximab soravtansine injection. Currently, as the autoimmune disease therapeutic sector is on the verge of rapid expansion, Huadong Medicine has long been positioned within this space, having invested in Quanxin Biopharma, known as “China’s leading autoimmune-focused public company,” and acquired commercialization rights to its flagship product.

It can be said that,Wherever the market hotspots are, there is Huadong Medicine., but this is not due to luck; it largely relies on Huadong Medicine’s strong resources in the out-of-hospital market. As is well known, Huadong Medicine has a sales-driven background and has established a robust presence in primary care, out-of-hospital, and retail channels. Its sales personnel maintain direct, long-term engagement with communities, pharmacies, and private hospitals, enabling them to identify clinical needs at the earliest stage. In this regard, a senior industry expert stated, “Although the gross margin of Huadong Medicine’s pharmaceutical commercial segment is not high, the process of distributing and delivering products to various hospitals allows the company to monitor real-time changes in supply and demand for different types of drugs, thereby empowering its marketing team.”

However, Huadong Medicine has not blindly followed trends in chasing hotspots. For instance, during the pandemic, the company adopted a highly cautious approach toward COVID-19, taking virtually no action. In hindsight, many pharmaceutical companies have stumbled in their strategic layouts for COVID-19-related products; after the reclassification of COVID-19 as a Class B infectious disease under Class B management, these heavily invested projects have rapidly become negative assets.

The second point is the ability to rapidly monetize, converting captured market hotspots into value at the earliest opportunity.In 2002, Huadong Medicine acquired the new drug certificate and exclusive rights to the relevant technology for acarbose active pharmaceutical ingredient (API) and tablets at a price of RMB 24.5 million. Within just ten years, sales of acarbose surpassed RMB 1 billion, exceeding those of the originator drug, Glucobay. This successful business development (BD) experience enabled Huadong Medicine to quickly identify a strategic path suited to its strengths:Compared with building an R&D system from scratch, leveraging capital to acquire pipelines or platforms is undoubtedly more efficient.。

Thus, during the rapid transformation period from 2019 to 2021, Huadong Medicine aggressively closed nearly 20 business development (BD) deals, earning it the industry moniker of “BD Maniac.”. Taking the medical aesthetics segment as an example, Huadong Medicine spent $220 million to acquire Sinclair in 2018; in 2019, it invested $20 million to acquire approximately 26.60% of the shares in R2, a U.S.-based medical aesthetics company; in 2020, it successfully acquired a 20% equity stake in Kylane; in 2021, it acquired High Tech, a medical aesthetics device company; and in 2022, it acquired Viora, a light- and energy-based device company. In just four years, through aggressive acquisitions, Huadong Medicine rapidly evolved from having no presence to becoming one of the companies with the most comprehensive pipeline of medical aesthetics products in China.

Currently, Huadong Medicine continues to pursue an aggressive inorganic growth strategy through business development (BD), introducing a series of highly promising, mature products—including zevor-cel from CARsgen Therapeutics, roflumilast cream, Wynzora cream, and senaparib—thereby establishing its “four pillars” of weight management, antibody-drug conjugates (ADCs), autoimmune diseases, and medical aesthetics.

The final point is its strong commercialization capability; it excels in marketing and has a proven track record of creating blockbuster products.Across the entire pharmaceutical industry, cases where generic drugs surpass originator drugs are rare, yet Huadong Medicine has achieved this feat more than once. In addition to the aforementioned acarbose, its generic cyclosporine has also captured a larger market share than Novartis’ originator product. These two typical cases clearly demonstrate Huadong Medicine’s strong capability in product commercialization.

In fact, Huadong Medicine has long been renowned for its “sales iron army.” Taking acarbose as an example, after the company failed to win bids in the national volume-based procurement (VBP) program, it remarkably managed to offset the substantial losses incurred in the hospital market by aggressively expanding into the out-of-hospital market. While many pharmaceutical companies responded to the impact of VBP by reducing their sales forces to cut costs and redirect resources toward R&D, Huadong Medicine took the opposite approach. From 2018 to 2021, its number of sales personnel steadily increased from 5,463 to 6,608, and further rose to 8,496 in 2022. Among these, the “specialized pharmaceutical care and market development team” under its pharmaceutical industrial segment alone comprised a massive workforce of 7,000 employees.

In this regard, Li Bangliang, former chairman of Huadong Medicine, once stated, “If marketing fails to keep pace, even the best products will not sell.”. This remains applicable in the current environment that emphasizes technological innovation, as innovation is a journey without a finish line. It consistently requires efforts from the marketing side to mitigate and hedge against the pressures of economic downturns, thereby buying time and capital for further innovation.

Therefore, in retrospect, Huadong Medicine has actually established a closed loop on its transformation path.First, by leveraging the vast out-of-hospital market and staying closely aligned with frontline clinical needs, it consistently captures business opportunities. Second, through its business development (BD) capabilities, it secures early-mover advantages in emerging market hotspots. Finally, via effective marketing, it rapidly monetizes products and reinvests the resulting cash flow into further BD initiatives.. This has also laid the foundation for Huadong Medicine’s advancement path, namelyFrom marketing to generics, then to business development (BD), and finally to independent innovation。

Can the “Huadong Model” Be Replicated?

In fact, like many domestic pharmaceutical companies, Huadong Medicine’s transformation was also “forced.”

In January 2020, one of Huadong Medicine’s flagship products, acarbose, unexpectedly failed to win a bid in the centralized volume-based procurement program. Following the announcement, its stock price plummeted instantly, hitting the daily limit down and wiping out more than RMB 4.3 billion in market capitalization. This reaction is hardly surprising: in 2019, Huadong Medicine’s sales revenue from acarbose exceeded RMB 3 billion, while the total revenue of its entire pharmaceutical manufacturing segment had just surpassed RMB 10 billion. This meant an immediate loss of 30% of sales revenue. Moreover, given that Huadong Medicine’s product portfolio was historically very streamlined and heavily reliant on a few flagship products to drive sales, it was inevitable that the company would face skepticism from secondary market investors.

Although Huadong Medicine ultimately retained its market share by leveraging its strong out-of-hospital market,However, this has also made it acutely aware of the drawbacks associated with a heavy reliance on a single product.Since then, Huadong Medicine has accelerated its transformation, making significant strides into the fields of innovative drugs and medical aesthetics.

Based on the preceding analysis, Huadong Medicine has many replicable aspects in its transformation journey, such as in track selection.Either focus on areas with established technical expertise and high success rates, or explore untapped markets with significant growth potential.. In terms of commercialization strategy, Huadong Medicine did not choose to go “all in” on R&D; instead, it pinned its hopes on in-licensing, essentially aiming to further leverage the advantages of its formidable sales force.

Of course, there are certain aspects that cannot be replicated. This primarily refers to Huadong Medicine’s inherent foundational advantages, such as its extensive resources in the out-of-hospital market, strong sales capabilities, and even its business development (BD) experience. These strengths have been accumulated through long-term practice, making it difficult for other pharmaceutical companies to achieve them through short-term, intensive efforts.

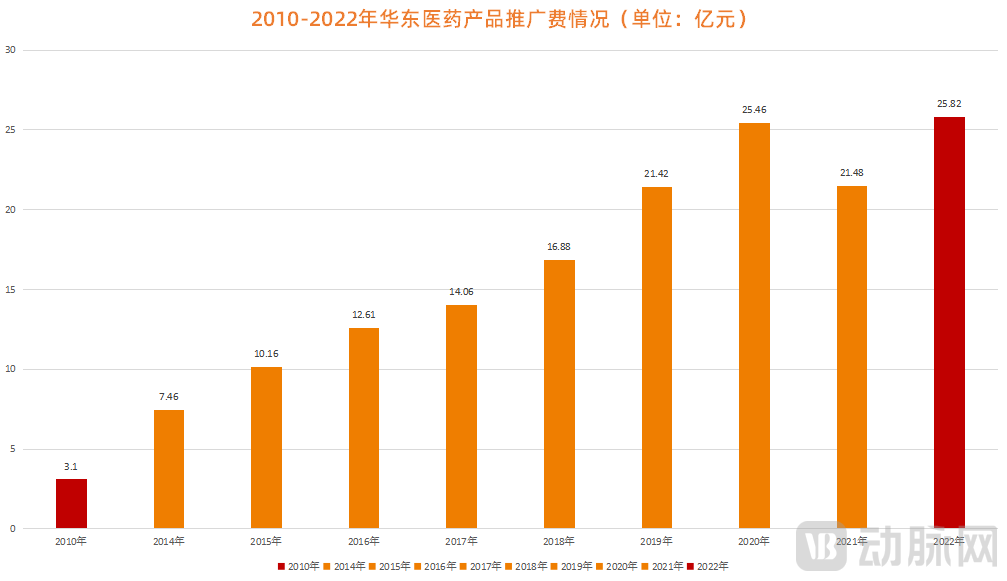

Figure 3. Huadong Medicine’s Product Promotion Expenses, 2010–2022 (Source: Huadong Medicine Annual Reports)

Figure 3. Huadong Medicine’s Product Promotion Expenses, 2010–2022 (Source: Huadong Medicine Annual Reports)

Beyond this, Huadong Medicine's determination to transform is something that other pharmaceutical companies would find difficult to sustain, for example, in marketing,Huadong Medicine is highly willing to invest a higher proportion of promotional expenses to consolidate its advantage in sales.. It is reported that since 2010, product promotion expenses have become the largest single item in Huadong Medicine's sales expenses, rapidly increasing from RMB 310 million initially to RMB 2.582 billion in 2022, representing a 7.3-fold growth over twelve years.

Of course, Huadong Medicine’s success is just one example; other traditional pharmaceutical companies, such as Simcere Pharmaceutical and Luye Pharma, are also typical cases of transformation in the current wave. Taking Simcere Pharmaceutical as an example, since 2020, it has shifted away from relying solely on its generic drug base and has intensified its transition into an innovation-driven pharmaceutical enterprise. Over the past three years, its R&D expenditure accounted for 25.3%–28.3% of total revenue. According to its latest annual report, innovative drugs now contribute more than 70% of its revenue, indicating that its “generic-to-innovation” strategy has entered a phase of performance realization. In contrast to Simcere’s focus on first-in-class (FIC) drugs, Luye Pharma has not chased short-term research hotspots. Instead, it has pursued targeted innovation based on its existing business foundation, building a robust pipeline centered on two core therapeutic areas: oncology and the central nervous system.

In fact, with the intensive implementation of volume-based procurement and the deepening capital winter, pharmaceutical companies’ transformation has become urgent. Through numerous successful cases, their transformation paths have gradually become clear:Prioritize marketing, then proceed with imitation, followed by business development (BD), and only as a last resort embark on genuine in-house R&D and innovation.. However, this is only a general roadmap. When translating it into concrete strategies, one must act according to one’s own capabilities. The underlying logic remains unchanged: leverage your core strengths to seize first-mover advantage in the market as quickly as possible.

Therefore, in a sense, this marks another new watershed moment in the development of China’s pharmaceutical industry.

1. “Huadong Medicine Is Quietly Becoming the King” — Yaodu Daily;

2. “Huadong Medicine: Are ‘Good Times’ Coming?” — Miaotou APP;

3. “Huadong Medicine’s Bull Stock Gone Astray” — Jin Duan.

4. “Cost Reduction, Efficiency Enhancement, and Focus: As More Pharmaceutical Companies Enter a New Phase of Transformation” – Amino Observation.