Commercial Nursing Care Services White Paper: A RMB 5 Trillion Market with 330,000 Enterprises—'Nursing + Insurance' Emerges as the Innovation Theme

The sunrise industries of the future are inevitably those closely tied to population aging.

High-quality, inclusive care services are key to addressing population aging. The rapidly accelerating aging society is driving a swift rise in demand for commercial care services.

In recent years, the Chinese government has issued multiple key policies related to nursing and elderly care, while the long-term care insurance (LTCI) system has become increasingly refined after several years of exploration. Driven by both policy support and growing demand, commercial nursing services are ushering in a period of robust growth, emerging as a critical measure to address the shortage of medical resources and the challenges of population aging.

On the other hand, the robust demand for commercial nursing services has strained the supply of professional care, while payment issues remain unresolved. How can the supply gap in commercial nursing services be bridged? How can traditional nursing services achieve a qualitative leap? Can insurance become the primary payer for nursing services? To address these questions, VCBeat Research surveyed eight companies and interviewed eleven industry experts, producing the “2023 White Paper on the Commercial Nursing Services Industry.”

Core Viewpoints:

The commercial care services market is fragmented with low concentration, necessitating a more vibrant financing environment.Currently, there are 330,000 enterprises in China involved in commercial nursing services. Over the past decade, the annual number of newly registered companies in this sector has shown a year-on-year upward trend. However, the industry’s market landscape exhibits significant fragmentation, indicating substantial room for improvement in market concentration. Among the 330,000 existing enterprises, only 130 have disclosed financing information in the primary market, with total financing amounting to RMB 6.475 billion.

Commercial nursing services are continuously expanding their service boundaries, evolving toward greater specialization and refinement.Nursing care is an integral component of medical services. Therefore, the commercial nursing care industry should transcend the narrow scope of basic caregiving and complement it with urgently needed services such as health management and family physician care. Enterprises should not only provide nursing care but also offer ancillary services, including health guidance and medical accompaniment, thereby serving customers throughout their entire life cycle and enhancing their overall experience.

Insurance channels will become the primary payers for commercial nursing services.Affordability is the most significant challenge facing China’s commercial long-term care services industry. Currently, consumer-side (C-end) payment capacity in this sector remains weak, while government-side (G-end) coverage is limited. Given the high alignment between insurance companies and commercial long-term care service providers in terms of target customer segments, the “insurance + long-term care services” model has emerged as a new trend, with business-side (B-end) payment mechanisms holding considerable promise. In particular, embedding long-term care benefits into insurance products has demonstrated greater market acceptance.

The following is an excerpt from the white paper:

According to data from Qichacha, there are currently 330,000 enterprises in China involved in commercial nursing care services, primarily concentrated in Jiangsu Province, Shandong Province, Guangdong Province, Sichuan Province, and other regions. In terms of registration volume, the number of new registrations for companies related to commercial nursing care services has shown a year-on-year upward trend over the past decade. The peak was reached in 2021, with as many as 58,000 new registrations, representing a year-on-year increase of 12.39%. As of October 2023, a total of 54,000 new enterprises related to commercial nursing care services were registered.

Financing Insights: Capital Favors Home Care

The market landscape of China’s commercial nursing services industry is characterized by small scale, fragmentation, high player count, and weak competitiveness, indicating significant room for improvement in market concentration. Among the 330,000 existing enterprises, only 130 have disclosed financing information in the primary market, completing a total of 206 financing rounds with an aggregate amount of RMB 6.475 billion. These companies are predominantly concentrated in economically developed regions such as Beijing, Shanghai, Guangdong, and Zhejiang.

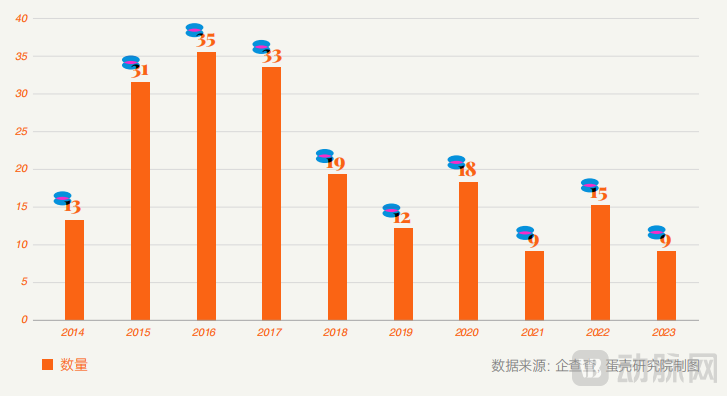

Distribution of Financing Years for Commercial Nursing Service Enterprises in China

From the perspective of financing years, the boom in internet healthcare has significantly raised capital market expectations for commercial nursing services.2015–2017 was a period of relatively active financing in the commercial nursing services industry. During this time, most companies that secured funding were those providing home-based nursing care services leveraging internet information technology, which closely coincided with the boom in China’s internet healthcare sector. Around 2015, internet technology became deeply integrated into the healthcare field, giving rise to a plethora of new business models such as online consultations, pharmaceutical e-commerce, O2O medication delivery, and O2O medical accompaniment services. As a blue-ocean market with rigid demand, nursing services naturally experienced rapid growth.

After 2018, the commercial nursing services market entered a period of stable development. Internet-based nursing service companies underwent a round of consolidation, with firms placing greater emphasis on strengthening their service capabilities and refining their operational models. During this period, the types of companies securing financing became more diverse and balanced, as capital paid substantial attention to in-hospital nursing, community-based home care, and institutional nursing.

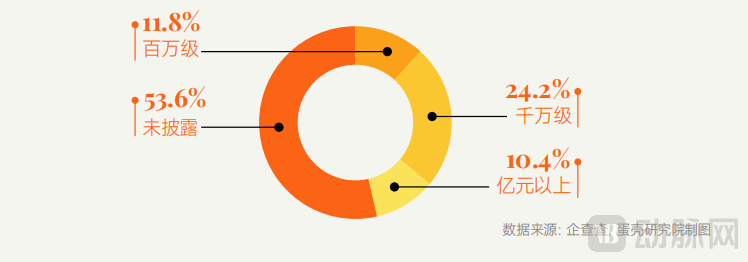

From the perspective of enterprise types, among the companies that have secured financing, the majority adopt a home care business model, which is generally more "asset-light." The financing amounts are predominantly in the tens of millions.

Domestic Commercial Nursing Service Financing Amounts

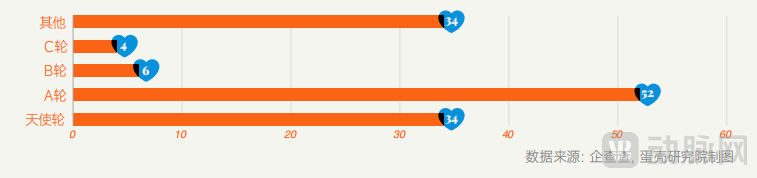

From the perspective of funding rounds, the commercial nursing care service industry is in its early stages, with seed and growth-stage companies representing the mainstream investment focus. Among the 130 companies that disclosed financing information, most were at the angel or Series A stage: there were 34 angel-round deals (accounting for 26%) and 52 Series A deals (accounting for 40%). Very few companies had reached Series B, Series C, or later stages.

Distribution of Financing Rounds for Commercial Nursing Services in China

Commercial care services align with capital’s investment objectives of “inelastic demand,” “high frequency,” and “long-term demand,” making them a key focus for investors. To continue attracting capital, commercial care service providers must demonstrate compelling operational capabilities and sustainable profitability models.

Enterprise Landscape Insight: Commercial Nursing Has Attracted Leading Internet Healthcare and Insurance Companies to Enter the Market

VCBeat has compiled statistics on enterprises involved in the commercial nursing services industry, which can be primarily categorized into four types: leading internet healthcare companies, firms backed by insurance giants, third-party professional nursing service providers, and traditional domestic housekeeping enterprises.

Internet Healthcare Giants

In the commercial nursing services sector, internet healthcare companies typically opt for collaborations with hospitals or government entities. By adopting the “hospital + platform” partnership model, they ensure the competence of nursing staff and the quality of care, while facilitating regulatory oversight.

For internet healthcare companies, a chain-based layout is the prevailing trend. Commercial nursing services serve as an important complement to their business, helping them establish a comprehensive operational framework that covers pre-consultation health management and family doctor services, online consultations and prescription circulation during consultation, and post-consultation nursing and rehabilitation. This creates a closed-loop system for whole-course disease management.

Third-Party Nursing Service Enterprise

Third-party nursing service providers tend to offer customized and standardized services, which can be further divided into two types: the first comprises enterprises with physical facilities and their own nursing teams; the second consists of internet-based nursing O2O platforms.

Enterprises with physical sites and in-house teams generally have a broader business layout, covering two or more settings among hospitals, homes, communities, and institutions, and providing one-stop nursing care services. In addition to nursing care, some companies have also ventured into caregiver training, sales of nursing products, and digital platforms, enhancing their competitiveness through a diversified business portfolio.

Internet-based nursing O2O platforms primarily focus on home care scenarios, with a few enterprises also covering in-hospital nursing services. These platforms integrate patient needs with nursing resources, connecting patients with caregivers. The business model of Internet-based nursing O2O platforms is still in an exploratory phase. Currently, the more promising platforms are mostly those collaborating with hospitals to leverage hospital resources, helping hospitals increase revenue, enhance patient satisfaction and loyalty, and strengthen their brand image.

Nursing Enterprises Backed by Insurance Companies

The integrated development of commercial insurance and health management has long attracted significant attention, prompting some insurers to establish their own health management companies and enter the commercial nursing care sector. While insurer-affiliated enterprises inherently possess channel advantages, this approach is asset-heavy, requires substantial investment, and involves a long payback period, thereby demanding that insurers have a thorough understanding of commercial nursing care services.

Taiyi Steward (Shanghai Shantai Health Technology Co., Ltd.) was jointly established by China Pacific Insurance and Sequoia China. Leveraging the advantages of insurance channels, it connects to a customer base of tens of millions within the CPIC system, ensuring precise matching between nursing care products and the needs of policyholders. The company also possesses professional expertise and insights in health management and the commercial nursing care industry. Its nursing service team comprises insurance product managers, health management product managers, big data experts, medical experts, operations specialists, and nursing care service experts. Through offerings such as in-hospital caregiver services and family doctor services, the company addresses customers’ health management needs across their entire life cycle.

Traditional Domestic Service Companies

Most traditional nursing service companies have evolved from domestic housekeeping firms, property management companies, or human resources agencies. These enterprises face low entry barriers, operate within a fragmented market landscape, and are predominantly regional in nature, serving specific areas or designated hospitals. Characterized by small revenue scales, they are generally positioned in the mid-to-low-end segment. The prevailing trend is for these traditional providers to be replaced by more specialized, standardized, and digitalized nursing service enterprises.

Characteristics of Different Types of Participants in Commercial Care Services

Nursing Scenario Insights: Significant Potential in Home-Based Care, While In-Hospital Nursing Requires Transformation and Upgrading

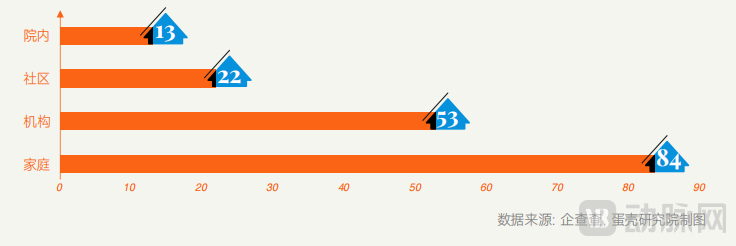

Commercial care service settings can be categorized into in-hospital, home-based, community-based, and institutional care. While there is overlap in the services provided, a single enterprise may simultaneously operate across in-hospital, home-based, community-based, and institutional care sectors, subject to its operational capabilities.

Distribution of Commercial Care Service Providers (Financed Companies Only)

In-Hospital Nursing

In-hospital nursing generally refers to bedside caregiving for inpatients, providing care and medical assistance services through bidding, labor dispatch, or O2O models. With concentrated clientele and higher demand density, in-hospital nursing allows for better control over service processes and quality. Commercial nursing service enterprises can prioritize in-hospital nursing as their initial entry point to build user reputation, before expanding from hospital-based care into the long-tail market of home-based nursing.

In-hospital nursing has a long development history and may appear to have a saturated market; in reality, it is undergoing a phase of service upgrading and transformation, with significant opportunities for reform in service processes and quality. Currently, the in-hospital nursing sector is dominated by domestic housekeeping companies, characterized by low entry barriers, a mixed-quality landscape, and substantial challenges in consolidation. Services tend to be standardized and assembly-line-like, failing to meet personalized needs, while service quality varies widely and regulatory oversight is lacking, making urgent innovation and upgrading imperative.

In the future, the in-hospital nursing sector must undergo innovation and upgrading in two key areas: first, regulation, by establishing internal corporate self-regulatory systems and evaluation mechanisms, potentially supplemented by hospital-based regulatory oversight; second, enterprises should achieve standardization, refinement, and personalization of services while building a reserve of high-quality talent.

Home Care

Home-based care is seeing increased participation from market-driven forces.

Participants in home-based care fall into two categories: one comprises enterprises operating under the “on-demand nurse” model, providing professional medical nursing services such as home visits for dressing changes, wound care, and infusion therapy; the other consists of domestic service companies that focus on daily living assistance, with relatively low barriers to entry.

The home-based nursing care market boasts a high ceiling and significant growth flexibility, positioning it as the dominant model within the nursing care sector. However, its limitations include constraints imposed by the setting, resulting in a relatively narrow scope of services; many highly technical and specialized medical nursing procedures cannot be performed in this environment. Furthermore, compared to in-hospital settings, the home environment is more complex, making standardization more difficult and quality control more challenging, thereby entailing compliance risks. The entire home-based nursing care segment remains in its nascent stage, with no successfully replicable business model yet established, and issues related to patient perceptions and payment mechanisms remain unresolved.

Community Nursing

Community nursing services are primarily supported by the government, which procures care services through government purchasing, medical insurance procurement, and long-term care insurance schemes. Government purchases and various subsidies constitute the core revenue sources for community nursing. According to surveys, most community nursing stations that have survived market competition are enterprises designated as approved providers under the long-term care insurance program. Under this government-funded model, community nursing service processes are standardized and risks are controllable; however, only relatively basic nursing services can be provided.

Institutional Care

Institutional care typically serves patients with disabilities or partial disabilities. Many elderly care institutions have made the care of patients with dementia and disabilities a key selling point, offering specialized supporting nursing services that provide 24/7 professional care, representing the highest tier within commercial nursing services.

Overall, relying on a single care setting is insufficient to address the complex, multidimensional needs of patients regarding services, financing, and facilities. Care settings will vary based on patients’ physical conditions and financial burdens. In the future, the boundaries between different care settings will gradually blur, giving rise to more integrated commercial nursing service enterprises.

Comparison of Characteristics Across Different Care Settings

The greatest obstacle to the commercial nursing care industry lies in payment. Patients lack the ability to pay, and commercial nursing enterprises lack viable profit models. The ultimate challenge for the industry is to clarify who the payers are for commercial nursing services and to resolve the payment issue.

This chapter provides a comprehensive analysis of the commercialization channels for commercial nursing services, covering the G-side (government), B-side (business), C-side (consumer), and H-side (hospital) sectors, and explores the industry’s profit models.

To G: The Largest Traffic Entry Point for Current Commercial Care Services

G-end refers to government payment, primarily through the social security-based long-term care insurance (LTCI). Social security LTCI represents the first breakthrough in the business model for nursing care services, as it not only initially addresses the payment issue but also serves as an endorsement of corporate qualifications and capabilities. Currently, social security LTCI has become a key customer acquisition channel fiercely contested by commercial nursing care service providers.

Social insurance-based long-term care insurance (LTCI) has stimulated the rigid demand for home-based elderly care among disabled individuals, serving as a springboard for commercial care enterprises to refine their service systems. At present, the profitability of most community-based home care providers is heavily reliant on government procurement, laying a solid foundation for the development of commercial care services. Under these circumstances, the implementation status of social insurance LTCI profoundly influences the growth of commercial care services. In cities where social insurance LTCI has not yet been implemented, the inherent conditions for developing commercial care services are inadequate, resulting in slow progress.

It is difficult for commercial nursing service enterprises to sustain long-term development by relying solely on the government sector.On one hand, there is payment pressure. The pooled funds of basic medical insurance constitute a major funding source for the social long-term care insurance (LTCI). However, as the pressure on maintaining the收支 balance of medical insurance funds intensifies, the payout burden of social LTCI will continue to expand. Relying solely on medical insurance funds is insufficient to fully cover costs or meet the enrollment needs of the covered population. Meanwhile, commercial LTCI has developed slowly and remains a niche product, failing to play its anticipated pivotal role.

On the other hand, a large number of companies are vying for government-sector channels, leading to severe service homogenization, low-price bidding, and disordered competition. Brand competition in the government sector has become intensely fierce, often leaving companies in a passive position during collaborations. Furthermore, the duration and frequency of nursing services funded by the government are insufficient, requiring patients to purchase additional services through other channels. Consequently, an increasing number of commercial nursing service enterprises have realized that relying solely on the government sector is unsustainable, necessitating the exploration of additional commercial channels.

To B: Poised to Become the Fastest-Growing Channel

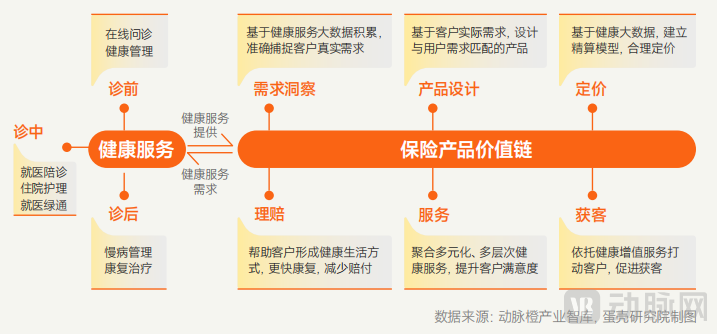

B-end clients mainly include insurance companies, health management enterprises, and internet companies. Among them, insurance companies paying for services represent a new growth point for profitability in commercial nursing care services within the B-end market.

Insurance-side payments can be further divided into two categories: one is commercial long-term care insurance, and the other is insurance products embedded with long-term care service guarantees. Currently, commercial long-term care insurance products lack substantial operational experience, making long-term risks difficult to manage and resulting in low market acceptance. In contrast, integrating long-term care services as part of life or pension insurance enjoys higher market acceptance.

Therefore, this section primarily explores the model of “embedding value-added nursing services into insurance products” within the insurance segment.

The integrated development of insurance with health management services, such as nursing care, has become an inevitable trend.Health management services, such as insurance and nursing care, align in terms of target customer base and strategic objectives, and can create a closed-loop data ecosystem, thereby enhancing the health protection level of policyholders. This collaboration offers a win-win opportunity for insurance companies, policyholders, and commercial nursing care service providers.

From the perspective of insurance companies, value-added health services can help insurers acquire customers, reduce claims payouts, and reshape the value chain of insurance products.

On one hand, customers’ demand for full-lifecycle services—such as health protection and diagnosis and treatment for pre-existing conditions—is growing steadily, making health management services a primary driver of customer acquisition in the insurance sector. By integrating health management services, insurers can enhance their marketing and customer acquisition efforts; beyond the policy terms and coverage scope of insurance products themselves, they can attract users through value-added health services.

On the other hand, through health management services, insurance companies can gain a more comprehensive understanding of customer profiles, thereby enhancing business quality control in underwriting and risk management. Leveraging these services, customers can better manage their daily lifestyle and dietary habits, fostering healthier lifestyles and facilitating faster recovery, which ultimately reduces claim payouts for insurers.

Overall, value-added health services are becoming deeply integrated into the insurance sector, reshaping key processes such as product marketing, design, claims settlement, pricing, and underwriting. There is an urgent demand among insurers to strengthen their health management offerings, making the “insurance + health management” model a strategic priority for many insurance companies.

Insurance Products + Value-Added Health Services Create a Closed-Loop Value System

For commercial nursing care service providers, insurance channels serve as a powerful tool for market expansion in the early to mid-stages. Compared with government (G-end) channels, which require navigating multiple layers of regulatory oversight and procurement processes, insurance channels offer simpler entry procedures. Moreover, relative to the highly fragmented consumer (C-end) channels, insurance-based customers exhibit higher density.

So, what kind of health value-added services are competitive? At this stage, the core element is customer acquisition. Customers need to have a high perception of these value-added services and a sense of gain, thereby enhancing their recognition of the value of insurance products.

Comparison of the Characteristics of Common Value-Added Health Services

In recent years, health value-added services have become increasingly comprehensive, encompassing online consultations, specialty drug services, inpatient nursing care, and green-channel access for critical illnesses. Among these, services such as nursing care and family physician programs offer higher perceived value. Taking nursing care as an example, first, its utilization rate is high. In the era of increased longevity, rising hospitalization rates among residents have spurred substantial demand for elderly care nursing. In contrast, while services like green-channel access for critical illnesses and specialty drug provisions carry high value, their incidence of use is relatively low. Second, customers often lack sufficient awareness of specialty drugs and tumor genetic testing services. Nursing care services, however, are straightforward and easy to understand, resulting in higher customer recognition and lower education costs.

In other words,Nursing services, characterized by high incidence rates and strong market awareness, better align with customers’ health protection needs, enhance their sense of value, and significantly boost the appeal of insurance products.

Driven by the superior performance of nursing services in customer acquisition, insurance companies have demonstrated unprecedented activity in the commercial nursing care sector.In 2023, China Pacific Insurance (CPIC) partnered with Taiyi Guanjia to establish a Caregiver Services Alliance, reaching cooperation agreements with eight nursing service enterprises. Among these initiatives, Taiyi Guanjia launched two key offerings: “In-Hospital and Post-Discharge Nursing Services” and “Baisuiju,” developed in collaboration with CPIC Life Insurance. These products provide customers with multi-tiered, high-quality in-hospital and post-discharge nursing care as well as home-based elderly care services. According to surveys, customer satisfaction among insurance policyholders has significantly improved thanks to the nursing services provided by Taiyi Guanjia.

To C: Insufficient payment capacity is a critical weakness on the consumer side.

C-end directly faces consumers. Although the demand for care is strong, it is not easy to get C-end users to pay directly. Three key challenges need to be addressed: affordability, trust, and customer acquisition costs.

Key Challenges in C-End Payments

Commercial nursing services face significant challenges in direct-to-consumer (C-end) implementation, making government (G-end) and business (B-end) channels currently more favorable. In the future, by leveraging empowerment from G-end and B-end partners, companies can, on one hand, facilitate more frequent consumer exposure to commercial nursing services, fostering habits and trust while strengthening market education, thereby driving traffic to the C-end. On the other hand, enterprises can utilize G-end and B-end channels to uncover consumers’ actual and unmet needs, identifying strategic entry points and breakthrough opportunities for penetrating the C-end market.

To H: Low willingness to pay, slow growth

The “H” end refers to hospital-funded services. Hospitals procure nursing services with the aim of supplementing registered nurses’ care, alleviating their workload, and enhancing both the quality of nursing care and patient satisfaction. Hospital-funded nursing services are generally generic in nature, meeting only patients’ most basic care needs. Currently, hospitals exhibit low willingness to pay, and future growth drivers for such willingness remain insufficient; consequently, the prevailing model is increasingly shifting toward a 2H2C (Hospital-to-Home-to-Consumer) approach.

Characteristics of Different Commercial Channels for Commercial Nursing Services

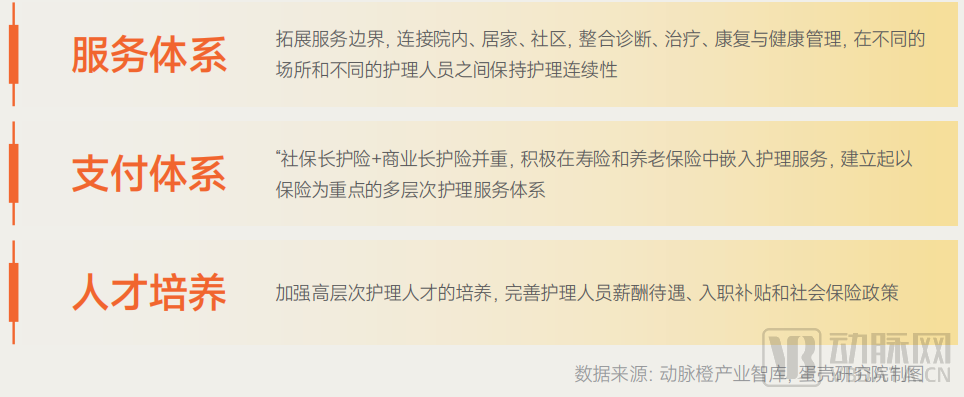

Service System: Establishing Continuous Care and Expanding Service Boundaries

In their commercial long-term care systems, both Japan and the United States have undergone a transition from extensive to intensive management and from passive to proactive service delivery. They have established relatively comprehensive service loops in terms of coverage settings and service offerings, with increasing emphasis on patients’ subjective and personalized needs.

The closed-loop service model is primarily reflected in the continuity of nursing care.Historically, nursing care has been fragmented, whereas overseas nursing systems have evolved toward continuity by linking in-hospital, home-based, and community settings. These systems integrate diagnosis, treatment, rehabilitation, and health management, maintaining care continuity across different settings and among various healthcare providers. They enable contextual transfer of patient information while safeguarding privacy, ensuring that patients receive continuous care services across different settings and preventing gaps in care. In China, nursing care has predominantly been hospital-based, focusing on acute-phase medical care for inpatients. Guided by the concept of continuous care, both home-based and community nursing are now experiencing significant opportunities for development.

Achieving continuity of care: family physician services are the key link.The challenge of continuous care lies in how to connect in-hospital, home-based, and community services; family doctors may offer a viable solution. Taking the family doctor services provided by Taiyi Guanjia as an example, the company’s family doctors deliver proactive, long-term management for users, encompassing pre-consultation health management, disease prevention, regular follow-ups during hospitalization, and post-consultation rehabilitation management. This approach covers the entire continuum of care—from disease prevention and diagnosis/treatment to rehabilitation—and establishes dynamic health records. Leveraging family doctor services that span hospitals, homes, and communities helps enhance the quality of nursing care.

China’s commercial nursing care services are in a phase of upgrading, with an urgent need to expand service boundaries and enhance granularity.Patients’ demand for specialized and personalized nursing services is emerging. For instance, in hospital settings, beyond basic nursing care, there is a high frequency of demand for medical accompaniment and off-campus housing. In home-based scenarios, there is strong demand for services such as remote rehabilitation consultations, purchasing assistance, errand running, and social companionship. This requires Chinese commercial nursing service enterprises to implement refined operations, enhance the quality and professional competencies of nursing staff, deeply explore patient need scenarios, provide composite services, and ensure precise matching between supply and demand.

In terms of nursing service offerings, Taiyi Guanjia’s strategic layout is quite innovative, having expanded from basic nursing services to comprehensive care covering the entire patient journey from medical consultation to rehabilitation.Established an online-to-offline closed-loop system, integrating medical consultation accompaniment, caregiver nursing, wellness accommodation, and family doctor services.

Taiyi Guanjia’s nursing service products boast both breadth and depth, with prominent differentiated advantages. The company focuses on addressing multiple pain points in the patient care journey, including the lack of companionship during medical visits, the absence of professional caregivers during hospitalization, off-site accommodation challenges for patients and their families, and the lack of professional rehabilitation guidance during the recovery period. To address these four key pain points, Taiyi Guanjia integrates medical visit accompaniment services, professional caregiver nursing services, comfortable lodging services, and family doctor services, achieving the promise of “companionship during medical visits, professional care within the hospital, accommodation outside the hospital, and medical consultation for rehabilitation.” In essence, Taiyi Guanjia provides not just standalone nursing services, but comprehensive, end-to-end health guidance.

Taiyi Guanjia Product Matrix

Payment System: Equal Emphasis on Social Security Long-Term Care Insurance and Commercial Long-Term Care Insurance

For China, a model that gives equal weight to social long-term care insurance and commercial long-term care insurance should be adopted to establish a multi-tiered care service system with insurance as the core, while actively integrating care services into life insurance and pension insurance products. First, social and commercial long-term care insurance have distinct positioning and target populations; they complement each other to comprehensively cover basic care protection and high-end care services, thereby avoiding any crowding-out effect. Second, insurance products combined with care coverage have performed well in overseas markets, demonstrating significant effectiveness in customer acquisition and claims reduction. As a high-value added service, care services warrant focused promotion in China.

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1: Aging Population Drives Demand for Care Services, with Market Size Approaching RMB 5 Trillion

1.1 The Connotation and Definition of Commercial Care Services Are Evolving

1.2 Drivers of the Commercial Nursing Services Industry

1.3 Vast Market with a Scale Approaching 5 Trillion

Chapter 2: 330,000 Enterprises with Prominent Characteristics of Being Small, Fragmented, and Weak

2.1 Breaking the Constraints on Talent, Services, and Regulation to Reverse the Industry’s “Low-Barrier” Image

2.1.1 The industry urgently needs to extend its service reach and establish a comprehensive service system

2.1.2 Significant Shortage of Nursing Staff Requires Enhancement of Professional Skills

2.1.3 Regulation: Policy regulation lags behind, with greater reliance on corporate self-regulation

2.2 Home Care Is Seen as Promising

2.2.1 Financing Insights: Capital Favors Community-Based Home Care

2.2.2 Insights into Enterprise Types: Commercial Nursing Has Attracted Leading Internet Healthcare and Insurance Companies to Enter the Market

2.2.3 Insights into Nursing Scenarios: Significant Potential in Home-Based Care, While In-Hospital Nursing Requires Transformation and Upgrading

2.2.4 Insights into Service Offerings: Severe Homogenization Necessitates the Establishment of a Closed-Loop Ecosystem

Chapter 3: Multiple Factors Influencing the Monetization of Commercial Nursing Services

3.1 To G: The Largest Traffic Gateway for Current Commercial Nursing Services

3.2 To B: Poised to Become the Fastest-Growing Channel

3.3 To C: Insufficient Payment Capacity Is a Critical Weakness on the Consumer Side

3.4 To H: Low willingness to pay, slow growth

Chapter 4 Analysis of Innovation Directions in Commercial Nursing Services

4.1 Insights from Overseas: The Commercial Nursing Care Services Industry

4.2 Analysis of Innovation Directions in China’s Commercial Nursing Services

4.3 Analysis of Innovative Forces in China’s Commercial Nursing Services: Taiyi Guanjia

Chapter 5: Future Trends

5.1 Transition from Domestic-Oriented Services to Integrated Medical and Elderly Care Services

5.2 Capital Drives Industry Scaling and Fosters a Nursing Ecosystem

5.3 Establishing a Business Model Primarily Focused on the B2B Sector

Please scan the QR code to add our assistant and access the full report. If you have already added the assistant, please proactively request the document.