Greater Bay Area Generates 36 Medical Device IPOs, with More in the Pipeline

DaAn Gene

Clinical Laboratory Reagents and Instruments R&D, Production, and Sales

Mindray

Medical Device R&D Manufacturer

Snibe

In Vitro Diagnostics (IVD) Product Developer, Manufacturer, and Supplier

Yhlo

Developer, Manufacturer, and Seller of In Vitro Diagnostic Instruments and Matching Reagents

MGI

Gene Sequencing Instruments and Related Reagent & Consumables R&D Manufacturer

Edan Instruments

Developer, manufacturer, and service provider of medical electronic equipment products

Biolight

Medical Device R&D Manufacturer

Guanhao Biotech

Regenerative Medical Product Provider

LifeTech

Suppliers of Congenital Heart Defect Occluders

Wondfo Biotech

In Vitro Diagnostics (IVD) Product Development, Manufacturing, and Sales

Well Lead Medical

Medical Catheter Research, Development, Production, and Sales

KingMed Diagnostics

Third-Party Medical Testing and Pathological Diagnosis Service Provider

The Guangdong-Hong Kong-Macao Greater Bay Area has become one of China's three major medical device industry clusters.

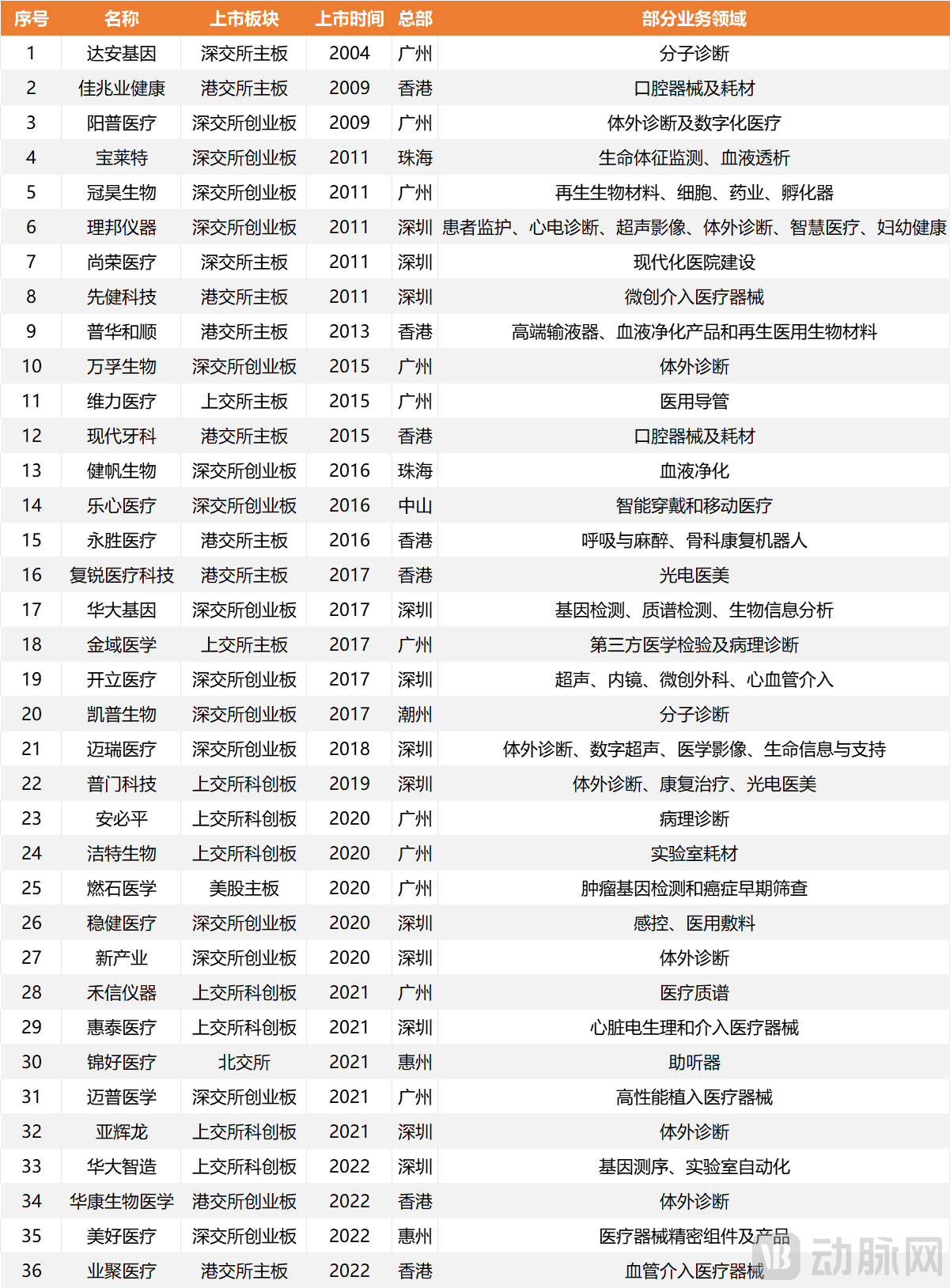

As of December 31, 2023, the number of listed medical device companies in China reached 172. Among them, 36 were from the Guangdong-Hong Kong-Macao Greater Bay Area, accounting for 20.93% of the total number of listed medical device companies in China.

In addition, medical device companies such as Bokang Shiyun from Guangzhou, Kentuo Fluid and Dakewe from Shenzhen, Shantou Ultrasound, and Zhuhai Keyu Biology are queuing for initial public offerings (IPOs), with the number of listed medical device enterprises in the Guangdong-Hong Kong-Macao Greater Bay Area expected to surpass 40.

A glance reveals a thriving landscape of listed medical device companies in the Guangdong-Hong Kong-Macao Greater Bay Area. This region has nurtured a large number of renowned domestic and international listed medical device enterprises, including DaAn Gene, Mindray, BGI, Medprin, Edan Instruments, and Snibe, while also gathering more than 8,000 innovative companies specializing in niche segments of the medical device industry.

In the primary market, more than 10 companies, including Baishi Medical, Ruipai Medical, Hongji Medical, Shenyuan Biology, Weiguang Medical, and Qiaojieli Medical, completed substantial financing rounds in the first quarter of 2024, attracting investment from over 20 renowned institutions such as Qiming Venture Partners, Cowin Capital, and Fortune Capital.

This land is witnessing a continuous stream of entrepreneurial legends in the medical device industry.

The Guangdong-Hong Kong-Macao Greater Bay Area is a city cluster comprising the two Special Administrative Regions of Hong Kong and Macao, along with nine cities in the Pearl River Delta region of Guangdong Province. On February 18, 2019, the state issued the Outline Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area, formally elevating the region to a national strategic priority. The Outline proposes that the Greater Bay Area will focus on building a “Healthy Bay Area.” Medical devices serve as a critical foundation and technical support for this initiative.

Listed companies are a key indicator for evaluating regional industrial clusters. Of the 172 listed medical device companies in China, one-fifth are from the Guangdong-Hong Kong-Macao Greater Bay Area.

First, let's look at the listing date.The IPO pace of listed medical device companies in the Greater Bay Area has largely synchronized with the overall development of China’s medical device industry, which can be divided into three phases. Before 2009, only DaAn Gene successfully went public. Following the official launch of the ChiNext board in 2009, there were IPOs every year, with six companies listing on the Shenzhen Stock Exchange in 2011. The third phase began in 2018, when the registration-based IPO system reform was initiated, leading to a significant increase in listing activity among medical device enterprises. After 2020, the pandemic drove rapid growth in the in vitro diagnostics (IVD) sector; among the 14 IPOs from 2020 to 2022, more than half were IVD companies.

Then, examine the product sub-sectors., among the 36 listed medical device companies, 17 have businesses that include in vitro diagnostics.

Leveraging its rich and mature industrial supply chain system, the Greater Bay Area has established a solid foundation for the in vitro diagnostics (IVD) industry. This has fostered the emergence of a large cohort of IVD enterprises represented by DaAn Gene, Mindray, Snibe, Yhlo, BGI, and Edan Instruments. By capitalizing on the talent and supply chain advantages of these leading companies, the region is gradually forming a complete IVD industrial chain.

Furthermore, leveraging Guangdong Province’s robust foundation in the electronics industry, niche market leaders have emerged in sectors such as diagnostic imaging, clinical devices, minimally invasive surgical instruments, endoscopic equipment, and blood purification.

Regional DistributionThe medical device industry in the Guangdong-Hong Kong-Macao Greater Bay Area generally presents a development pattern with Hong Kong, Macao, Guangzhou, and Shenzhen as the four core engines driving regional growth, radiating to and stimulating development in surrounding areas. A breakdown of the healthcare industries in these three central cities reveals a relationship of complementary synergy.

Guangzhou and Shenzhen are two core clusters of the medical device industry in Guangdong Province, exhibiting distinct development trajectories based on their respective intrinsic industrial foundations.

Leveraging its advanced medical resources and trade systems, Guangzhou initiated its export business at an early stage, initially focusing on medical consumables. Driven by favorable policies and the leadership of local industry giants, the city has since strategically prioritized the high-end medical device sector, cultivating a distinctive cluster of specialized enterprises represented by DaAn Gene, Wondfo Biotech, KingMed Diagnostics, Well Lead Medical, and MicroPort Medtech.Has established significant advantages in the fields of in vitro diagnostics and clinical devices.

As a vanguard of China’s reform and opening-up, Shenzhen boasts a highly developed and concentrated mechatronics industry, establishing an integrated R&D, production, and sales chain that spans upstream raw material supply, midstream product development and manufacturing, and downstream foreign trade exports. Driven by market demand, pioneers in Shenzhen began transitioning into the medical device sector, which shares the same electronic and mechanical technological foundation, giving rise to a host of industry leaders such as Mindray, SonoScape, Lifetech Scientific, and Edan Instruments.Focus on the development of medical electronic equipment and medical imaging equipment。

Expanding the scope to Guangdong Province, the medical device industry radiates from Guangzhou and Shenzhen to surrounding cities. It is worth noting that,Surrounding cities such as Zhuhai, Foshan, Huizhou, and Zhongshan will also focus on specific niche areas based on their respective locations, talent pools, and scientific research capabilities, thereby pursuing differentiated development.. For instance, Foshan City intends to develop the dental instrument industry by investing heavily in building the South China (International) Dental Medical Equipment Industrial City, thereby solidifying the foundation of its characteristic industries.

Among the 36 listed medical device companies, seven are headquartered in Hong Kong. Their business operations primarily target the consumer healthcare market, including dental instruments, aesthetic medical devices, and consumables.

Finally focusing on the listed sector, the number of listed companies on the Shenzhen Stock Exchange (SZSE), Shanghai Stock Exchange (SSE), and Hong Kong Stock Exchange (HKEX) stood at 17, 11, and 8, respectively. Prior to 2020, the ChiNext board was the primary channel for initial public offerings (IPOs) in the medical device sector, with all 15 SZSE-listed companies having completed their listings before 2020. Following the introduction of the “Fifth Set of Listing Standards” on the SSE’s STAR Market and the “Chapter 18A Listing Rules” on the HKEX, medical device enterprises have received greater support from more inclusive regulatory frameworks, leading to an increase in the number of medical device companies listed on the STAR Market and the HKEX.

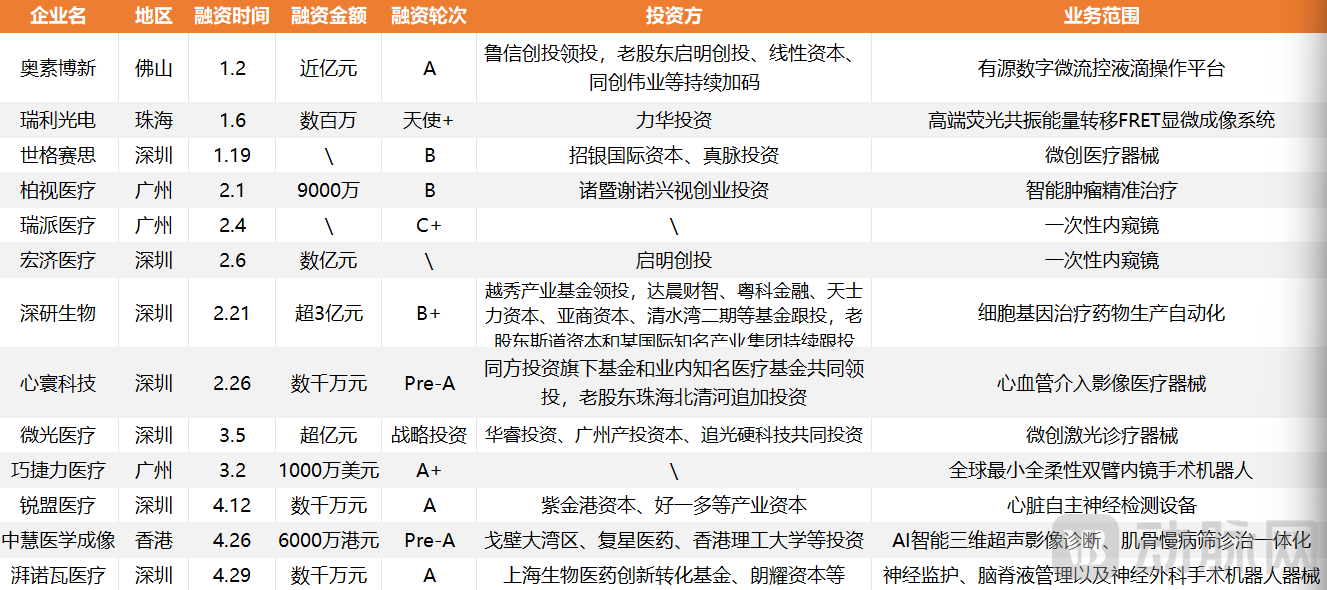

In 2024, the healthcare investment climate cooled slightly, yet medical device enterprises in the Greater Bay Area continued to secure financing frequently. According to incomplete statistics from VCBeat, as of April 2024, 13 financing rounds had been completed in the medical device sector within the Greater Bay Area, concentrating on fields such as medical imaging and minimally invasive surgical instruments, which aligns with Shenzhen’s areas of advantage mentioned earlier.

From the perspective of investor composition, state-owned capital participation is relatively high. Since 2023, state-owned entities have been actively investing. According to VCBeat’s observations, state-owned capital tends to invest in early-stage, small-scale, and innovative ventures, while also covering mid-to-late stage healthcare projects. It focuses on frontier fields such as imaging equipment, AI-driven healthcare, and medical robotics, and leverages local industrial advantages to layout upstream and downstream sectors, thereby building a complete regional industry chain.

Currently, the listed medical device companies in the Guangdong-Hong Kong-Macao Greater Bay Area have not only stimulated the region's economy but also provided a fertile ground for the entrepreneurship and development of more innovative medical device enterprises, thereby accelerating the improvement of the medical device industry chain. This aligns with the tiered cultivation strategy for medical device enterprises implemented in the Greater Bay Area.

Leading Enterprises Target Key Links in the Industrial Chain to Establish Top-Level Advantages for Industrial Clusters

In terms of leading the development of industry leaders, the government encourages these key enterprises to focus on critical links in the industrial chain and core technologies, engage in joint ventures, cooperation, mergers, and acquisitions, integrate resources, leverage complementary advantages, strengthen brand cultivation, and continuously enhance their core competitiveness and ability to drive the industry.

First,Economic growth has fueled the continuous expansion of the M&A market. Through mergers and acquisitions, integration, and industry restructuring, companies can secure greater market resources, thereby creating enhanced market value.

In January 2024, Mindray invested RMB 6.65 billion to acquire controlling interest in Huitai Medical, a company listed on the STAR Market. Through this collaboration, Mindray has rapidly entered the cardiovascular consumables market, including electrophysiology; meanwhile, Huitai Medical’s product performance and its relatively weak presence in overseas markets are expected to see significant improvement.

This acquisition represents a powerful alliance between two major local innovators in Shenzhen. Their union will strengthen Shenzhen’s medical device sector and accelerate the city’s development into a globally renowned R&D hub for high-end medical devices.

Among the 36 listed medical device companies mentioned earlier, Kaisa Group acquired Meijia Medicine, a leading provider of dental instruments and consumables, to enter the broader healthcare sector. Puhua Heshun acquired Volute, a high-end infusion set manufacturer; Ruijian Medical, a leading domestic producer of hemodialysis consumables; Ruijian Gaoke, an innovator in regenerative materials; and a private medical industrial park, thereby completing the establishment of its four major business systems. Furui Medical Technology acquired Fosun Dental for RMB 312 million to accelerate its digital transformation. Biolight acquired Junkang Medical to achieve synergy with its existing operations.

Secondly,The relentless pursuit of innovative technologies is the key determinant of whether an industrial cluster can achieve long-term success and sustain its competitive edge in the market.

Innovative medical devices serve as an indicator of a region’s technological capabilities. As of 2023, the National Medical Products Administration (NMPA) had approved a total of 251 innovative medical device products. Among these, Guangdong Province had 36 innovative medical device products on the market, ranking fourth nationwide.

Listed medical device companies are also increasing their R&D investment to continuously strengthen their competitive moats. For instance, Mindray’s R&D expenses reached RMB 2.811 billion in the first three quarters of 2023, approaching its full-year level in 2022; Lifetech Scientific invested RMB 2.979 billion in 2023 to enhance its R&D and innovation efforts; and DaAn Gene’s R&D expenditure accounted for 44.9% of its total operating revenue in 2023.

SMEs Pursue the "Specialized, Refined, Differential, and Innovative" Development Path to Solidify the Foundational Basis for Industrial Clusters

In fostering the growth of small and medium-sized enterprises (SMEs), the government guides SMEs in the medical device sector to adopt a clinical value-oriented approach, focus on key core technologies, enhance innovation capabilities and market share, and pursue a development path characterized by “specialization, refinement, differentiation, and innovation.”

“Little Giant” firms specializing in refinement, innovation, and niche markets are the elite among specialized and sophisticated SMEs, representing internationally leading production technologies or processes and ranking among the top globally in market share for their individual products.As of the end of 2023, Guangdong Province had a total of 80 specialized, refined, distinctive, and innovative “Little Giant” enterprises with medical devices as their core business, ranking first in China, including 36 newly added enterprises in 2023.

The Medical Device Registration Certificate is also a key indicator for assessing the R&D capabilities of medical device companies. According to the Guangdong Province Medical Device Industry Development Report (2023), as of January 2024, the total number of product registrations in Guangdong Province reached 19,690, and the total number of filings reached 22,873, accounting for 14.7% and 12.3% of the national totals, respectively. In 2023, Guangdong Province registered 379 Class III medical devices, representing 14% of the national total (2,706 items). The Greater Bay Area is also encouraging corporate innovation through various preferential policies. For instance, Guangzhou City provides subsidies of up to RMB 5 million to enterprises that obtain their first registration certificates for Class II and Class III medical device products.

“Leading the Small with the Large”: Building Advanced Manufacturing Clusters

In the development of advanced manufacturing clusters, government departments have proposed enhancing the driving role of leading backbone enterprises, supporting cluster promotion agencies, and vigorously advancing the construction of the "Shenzhen-Guangzhou High-End Medical Devices" national-level advanced manufacturing cluster.

After these pioneering enterprises develop into industry leaders, their demand for upstream and downstream supply chains will drive the growth of other small and medium-sized enterprises; meanwhile, their mature corporate systems will also cultivate a large number of innovative and entrepreneurial talents for the market. For instance, Shenzhen Anke and BGI Genomics, hailed as the “Whampoa Military Academy” of the industry, have nurtured many leading figures in the field of high-end medical device equipment.

The Greater Bay Area has established a competitive medical device industry chain. According to data from Yaozhi Medical Devices, as of August 2023, Guangdong Province ranked first in China in the number of medical device manufacturers, with 8,493 enterprises; there were 28,600 distributors of Class II and III medical devices, placing the region at the forefront of the country in research and development, manufacturing, and distribution capabilities.

These enterprises are primarily concentrated in the core areas of the Greater Bay Area, which boast robust economic development and advanced manufacturing industries. Key clusters include Guangzhou Science City, Sino-Singapore Guangzhou Knowledge City, Nanshan District and Pingshan District in Shenzhen, the National Health Technology Industrial Base in Zhongshan, Songshan Lake in Dongguan, and the China Medical Device (Sanshui) Industrial Base.

In 2019, the total output value of the medical device industry in the Guangdong-Hong Kong-Macao Greater Bay Area exceeded RMB 125 billion, accounting for 16.67% of China's total medical device industry output value and ranking first nationwide.

The remarkable achievements of the Greater Bay Area in the medical device industry are attributable to its mature market environment and economic development, as well as being closely linked to factors such as policy support, financial backing, and industrial foundation.

The Greater Bay Area, as a frontier of reform and opening-up, exhibits distinct characteristics of an export-oriented economy.In 2023, the total import and export value of the nine mainland cities in the Greater Bay Area reached RMB 795 million, accounting for 19% of the national total. The international market is also a primary target market for Guangdong Province’s medical device industry. Among the listed medical device companies within the region, leveraging natural geographical advantages and the traditional outward-oriented mindset of South China, GBA-based listed medical device enterprises have demonstrated significant progress in commercial globalization. For instance, Mindray reported revenue of RMB 18.476 billion in the first half of 2023, with overseas sales contributing 40% of its total revenue. Snibe generated RMB 1.321 billion in overseas business revenue in 2023, representing a year-on-year increase of 36.23%, a growth rate that exceeded its overall revenue growth for the same year.

In terms of the industrial environment, the government provides proactive services and allocates comprehensive public resources for innovation and entrepreneurship., such as platform carriers and policy environments. The Greater Bay Area High-Performance Medical Device Innovation Center, located on Guangzhou International Bio Island, is establishing an integrated innovation consortium covering basic research, applied basic research, industrial translation, and registration and approval.In terms of industrial structure, the healthcare services in the Hong Kong and Macao Special Administrative Regions are highly developed, while the nine cities of the Pearl River Delta boast a robust manufacturing foundation. Guangdong Province also has a strong manufacturing base, offering significant advantages in regional synergy and complementarity.

Capital Elements Required for Industrial DevelopmentShenzhen Capital Group, Shenzhen High-Tech Investment Group, and Songhe Capital, which were established in the 1990s, as well as outstanding domestic investment institutions founded in the early 21st century—including Fortune Capital, Oriental Fortune Capital, Cowin Capital, Fenxiang Investment, and Keytone Capital—have become leaders in China’s venture capital industry, creating over a hundred star investment cases in the healthcare sector. The Greater Bay Area has established sci-tech innovation industry investment funds totaling hundreds of billions of yuan, which, combined with highly active private capital, provides substantial capital support and significant market potential for the region.

Extensive Clinical Resources and Research Capabilities, which is sufficient to demonstrate that the Greater Bay Area has ample clinical and technical foundations to support and foster the implementation of new technologies. The Greater Bay Area boasts over 100 Grade A tertiary hospitals, Hong Kong’s rigorous and robust healthcare management system and nursing workforce, Macau’s highly refined community medical services, as well as a number of influential higher education institutions such as Sun Yat-sen University, South China University of Technology, Southern Medical University, and Guangzhou Medical University.

Furthermore,A batch of influential research institutes, hospitals, testing agencies, and other application-side entities, with a solid foundation in the innovation, translation, manufacturing, and trade of medical devices. The Shenzhen Institute of Advanced Technology, Chinese Academy of Sciences, has optimized its layout in six key areas: life and health, medical devices, biomedicine, electronic materials, marine science and technology, and artificial intelligence and robotics. In addition, by the end of 2020, the Greater Bay Area had 181 animal experimentation institutions, 90 clinical trial institutions, and 33 medical device testing institutions, among others.

Based on this, the Greater Bay Area has also become the preferred destination for the implementation of numerous high-quality medical device projects and the flow of overseas talent resources. With the development of China's medical device industry,China has formed three major medical device industry clusters in the Guangdong-Hong Kong-Macao Greater Bay Area, the Yangtze River Delta, and the Beijing-Tianjin-Bohai Rim region. The total output value and sales revenue of medical devices in these three regions account for more than 80% of the national total.and exhibit distinct regional characteristics. For instance, the Yangtze River Delta is led by Shanghai’s high-end medical devices, with Jiangsu and Zhejiang featuring clustered industries specializing in disposable medical devices and consumables. The Beijing-Tianjin-Bohai Rim region, centered on Beijing, boasts a competitive cluster in digital medical equipment such as MRI systems, digital ultrasound, accelerators, and computer-navigated positioning devices for medical use.

In addition,Central China, represented by Henan and Hubei provinces, is absorbing industrial spillovers from the three major clusters and has already established a certain overall scale advantage.Henan boasts prominent advantages in medical hygiene materials and rehabilitation equipment. Changyuan is home to China’s largest production base for sanitary materials, while Zhengzhou hosts China’s largest production base for in vitro diagnostic products. In Hubei, the birthplace of China’s laser industry and pathology equipment, Xiantao and Zhijiang hold leading positions in the fields of medical protective supplies and medical dressings.

Close-quarters competition is inevitable. To develop local medical device industry clusters, it is essential to fully understand the strengths and weaknesses of the existing local industrial chain, achieve deep integration with the healthcare sector, and ultimately transform these advantages into differentiated core competitiveness. The path for the development of China’s medical device industry is arduous and long; breaking through the encirclement requires continuous exploration by all stakeholders in the industry.

Reference Article:

Hyjoy Capital’s “Three Soul-Searching Questions: What Defines Healthcare Venture Capital in the Greater Bay Area, What Are Its Strengths, and Where Is It Headed?”

Yaozhi Medical Devices “Guangdong Province Medical Device Industry Development Report (2030)”

Caixin Health: “Why Are Over 20% of Listed Medical Device Companies in Guangdong?”

IHM MedTech Planet: “The Medical Device Industry Is Accelerating—Why the Guangdong-Hong Kong-Macao Greater Bay Area?”

ChanYe JiaJia “Map of China’s Trillion-Yuan Medical Device Industry Clusters: How Can Emerging Regions Seize the Momentum to Precisely Connect with Leading Medical Device Hubs?”