Tencent-Backed Zhuzheng Medical Files for Hong Kong IPO, Igniting the Premium Healthcare Sector

Distinct HealthCare

High-Quality, Digital Medical Service Provider

On May 16, Distinct HealthCare, a private mid-to-high-end integrated medical service provider, filed its prospectus with the Hong Kong Stock Exchange for an initial public offering.

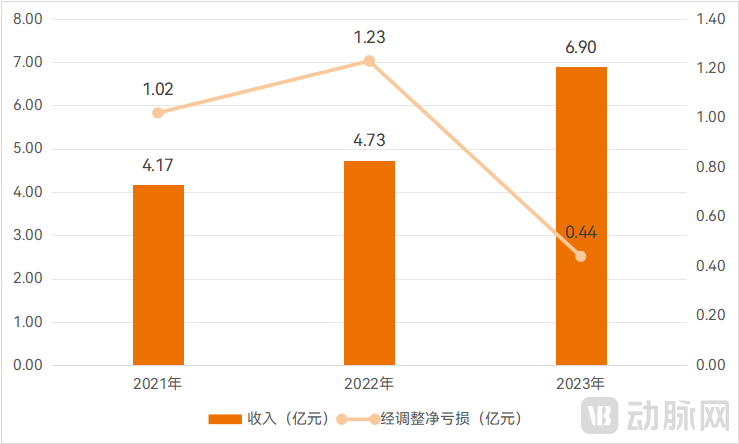

Since its establishment in 2012, Distinct HealthCare has operated 21 medical service institutions across 11 cities in China, including 19 clinics and two hospitals. In recent years, the company has achieved steady growth in its operational performance, with total revenue increasing from RMB 417 million in 2021 to RMB 690 million in 2023.

Medical services is a capital-intensive industry characterized by high upfront investment and long payback periods. Currently, Distinct HealthCare remains in a loss-making position, although its losses are gradually narrowing. Its adjusted net loss decreased from RMB 102 million in 2021 to RMB 44 million in 2023.

Distinct HealthCare: Key Performance Metrics, Source: Prospectus

As a star enterprise in the mid-to-high-end medical services sector, Distinct HealthCare has previously secured investments from renowned institutions including Tencent, Tiantu Capital, CICC, Qianhai Fund of Funds, Matrix Partners China, and Shuimu Fund.

In recent years, a number of specialized medical service providers have gone public or filed for initial public offerings, spanning fields such as ophthalmology, dentistry, oncology, and assisted reproduction. These institutions cater to consumer-driven healthcare demands in their respective specialties or complement the public specialized medical service system, with the majority continuing to provide inclusive, affordable medical services.

Distinct HealthCare’s IPO Application Reignites Industry Focus on Mid-to-High-End Medical Services

Compared with standard medical services, a prominent feature of mid-to-high-end medical services is the high consultation fees, ranging from hundreds to thousands of yuan, while examination costs are several times higher than those at ordinary medical institutions, or even more. However, medical demand is inherently low-frequency, and the target population for mid-to-high-end medical services is smaller than that for standard care. Therefore, despite the high average transaction value, mid-to-high-end medical services cannot rely solely on single-visit consultations.

"In recent years, mid-to-high-end medical services have continuously built their core service model through 'home-style medical care'."

Taking Distinct HealthCare as an example, its medical institutions offer departments in pediatrics, dentistry, ophthalmology, dermatology, otolaryngology and surgery, gynecology, and internal medicine. By establishing a family-centered care model and fostering close collaboration among specialists across these disciplines, the company addresses the diverse healthcare needs of patients and their entire families, continuously improves patient satisfaction, and creates opportunities for cross-departmental referrals.

Specifically, Distinct HealthCare focuses on the holistic health of the individual rather than isolated organs or body systems, comprehensively considering patients’ physical, mental, and social well-being. It also provides selected subspecialty services and targeted care for specific familial conditions based on patient needs, including pediatric asthma management, allergen immunotherapy, pediatric endocrinology, pediatric developmental-behavioral pediatrics, gastrointestinal endoscopy, weight management, and dry eye treatment.

Annual membership serves as the product vehicle for the “family-style healthcare service” model. Since 2020, Distinct HealthCare has launched a membership program across all its medical service institutions, allowing up to six members per account to enjoy various benefits offered by the program.

It is not just Distinct HealthCare; membership-based “family-style medical services” have become a standard offering among mid-to-high-end healthcare institutions.

In March 2024, Shanghai Ward Medical Center, under Meihua Ward Healthcare, upgraded its “Family Membership Card” to comprehensively cover healthcare services ranging from dentistry to ophthalmology, and from pediatrics to general practice.

In April 2024, Jiahui Health launched its Family Combined Health Management Service, providing tailored health management assessments for middle-aged and young adults, the elderly, and children.

Furthermore, Shengzhong Medical has even proposed the concept of “managing family life assets like corporate assets,” providing entrepreneurs’ entire families with a full-chain service ranging from risk management to diagnosis, treatment, and rehabilitation. By continuously collecting, organizing, and analyzing medical and various lifestyle-related health data of family members, the company delivers proactive, high-frequency services for disease prevention.

“Home-style medical services” shift healthcare demand from single, low-frequency encounters to multi-person, higher-frequency engagements, enabling healthcare institutions to increase service volume while achieving higher revenue per customer. Meanwhile, inter-specialty collaboration and referrals facilitate more efficient allocation of medical resources.

This model has also gained a certain degree of market recognition. Taking the operational data of Distinct HealthCare as an example, its member renewal rate has shown steady growth. In the four quarters of 2022, the member renewal rates were 40%, 36%, 38%, and 48%, respectively; in 2023, they reached 47%, 57%, 55%, and 63%, respectively.

In the future, “family-style medical services” will continue to deepen within the mid-to-high-end healthcare sector. On one hand, they will address the diverse medical needs of family members across different life stages and roles; on the other hand, based on the overall lifestyle of the family unit, they will provide full-cycle services ranging from disease prevention to diagnosis, treatment, and rehabilitation, thereby safeguarding family health.

Payers are an indispensable component of the healthcare service system. Mid-to-high-end medical services cater to middle- and high-income populations. In addition to out-of-pocket payments, commercial insurance is one of the primary payers, particularly mid-to-high-end medical insurance products characterized by direct billing.

In recent years, the development of mid-to-high-end medical insurance has driven the growth of mid-to-high-end medical services.

On the one hand, various insurance companies are continuously launching diverse new products, expanding their covered populations, and incorporating more private medical institutions. For instance, Fosun United Health Insurance has established a comprehensive product portfolio encompassing million-yuan medical insurance, mid-end medical insurance, and high-end medical insurance, thereby carving out a distinctive niche in the mid-to-high-end medical insurance sector. As the scale of its insurance business expands, its direct-billing medical network has also grown steadily. Currently, its direct-billing network in mainland China includes over 800 medical institutions, such as renowned Grade A tertiary hospitals, international hospitals, private clinics, and dental clinics. This network features mid-to-high-end medical chains including Distinct HealthCare, SinoUnited Health, and ParkwayHealth.

On the other hand, amid intensifying competition and increasing market saturation, some million-yuan medical insurance products are transitioning toward mid-to-high-end medical insurance. Leading companies that once dominated the “million-yuan medical insurance” sector, such as ZhongAn Insurance, Ant Insurance, PICC, and Ping An Health, have also successively launched medical insurance products targeted at mid-to-high-end customers.

Furthermore, healthcare service providers are also participating in the development and promotion of insurance products. In February 2024, Jiahui Health, together with China Continent Property & Casualty Insurance Company and MSH China, jointly launched a Jiahui-exclusive high-end medical insurance plan—the “Hejia Ankang” Individual Medical Insurance.

Overall, the ecosystem of the mid-to-high-end medical insurance market has become increasingly diverse, encouraging more patients to utilize mid-to-high-end medical services.

According to Distinct HealthCare’s prospectus, as of the end of 2023, the company had signed agreements with more than 50 commercial insurance companies and third-party administrators (TPAs) for medical expense settlement. In 2021, 2022, and 2023, revenue from direct billing through commercial medical insurance accounted for 7.2%, 8.4%, and 10.3% of total revenue for the respective years.

Meanwhile, Distinct HealthCare will also collaborate with more commercial insurance companies and third-party administrators (TPAs) to develop and promote insurance products, aiming to provide broader medical coverage and more convenient settlement methods, help commercial insurers and TPAs manage costs, and increase the proportion of revenue from direct billing through commercial medical insurance, thereby further diversifying its revenue streams.

Currently, China’s new healthcare reform has entered a critical phase. Measures for reforming medical insurance payment methods are being accelerated and institutionalized. As initiatives such as centralized drug procurement and DRG/DIP payment systems are implemented, the positioning of medical insurance to cover basic needs and the public-welfare nature of public medical institutions have become more clearly defined.From another perspective, mid-to-high-end medical services and insurance can meet patients' demands for high-quality healthcare and high-value pharmaceuticals and consumables, and will feature more clearly defined target groups and market positioning in the future.

In recent years, internet healthcare has developed rapidly. If the online medical services of public healthcare institutions are mainly policy-driven, those of non-public healthcare institutions are primarily demand-driven, a trend that is also evident in the mid-to-high-end healthcare services sector.

Distinct HealthCare provides patients with health consultations, prescription services for follow-up visits, and other offerings through its online medical service platform, forming an integrated service model in combination with its physical facilities. The platform also offers free follow-up care initiated by physicians, enabling multiple rounds of communication between doctors and patients. Additionally, as part of membership benefits, members can enjoy a specified number of free online nursing guidance sessions via the online medical service platform.

Since November 2023, Distinct HealthCare has piloted an online cloud membership program in regions without physical medical facilities, allowing users to access certain online service benefits for a low annual fee. Among Distinct HealthCare’s paying patients, online patients account for more than 20%.

Internet healthcare has played a significant role in addressing the uneven distribution of medical resources, improving the efficiency of medical services, and enhancing the effectiveness of chronic disease management. Distinct HealthCare is not the only institution placing high priority on online medical services; in recent years, nearly all mid-to-high-end healthcare providers have actively invested in developing online platforms. This strategic initiative aims to expand patient access to care across China, streamline service processes, improve operational efficiency, and promote the coordinated development of both physical and online medical services.

As of the end of 2023, United Family Healthcare (UFH) has established a comprehensive healthcare ecosystem across China, integrating general hospitals, specialty hospitals, a clinic network, and internet hospitals. The hospitals and clinics within this system maintain differentiated positioning while achieving resource synergy. Meanwhile, UFH provides all-around intelligent support for medical services through online services, clinical care, middle-office operations, back-office management, and a suite of BI products. By centering online product upgrades on patient experience, UFH enhances the accessibility of high-quality medical care.

Recently, Noah Healthcare upgraded its internet hospital platform. In addition to integrating functions such as online consultations for follow-up visits, report inquiries, appointments with renowned specialists, and green-channel referrals, the platform now incorporates select features from its membership program.

In January 2024, Parkway Healthcare launched the New Hongqiao Parkway Health Cloud Internet Hospital, integrating the medical and technical resources of the Shanghai New Hongqiao International Medical Center, Shanghai Parkway Hospital, and Health Cloud to meet the multi-level and diverse healthcare needs of various populations.

Shanghai United Family Healthcare also features its internet hospital as a key service, with general practitioners and specialists providing 24/7 online consultations. Leveraging its digital platform, Shanghai United Family Healthcare has launched “Yao Health,” a digital chronic disease management service that integrates wearable devices, patient management services, and patient management SaaS solutions to deliver chronic care support to families in need. Additionally, through customized partnership models, it provides workplace health management services for large enterprises.

For mid-to-high-end healthcare service providers, internet-based healthcare offers dual value: first, it enhances service accessibility and improves patient experience; second, institutions can analyze the distribution characteristics of supply and demand based on physician and patient activity levels on online platforms, thereby strategically selecting offline markets for expansion and increasing the success rate of newly established medical facilities.

Distinct HealthCare has presented performance data that reflects ongoing growth and continued potential, offering insights into the current state and trends of the mid-to-high-end medical services market.

According to Frost & Sullivan data, the number of mid-to-high-end private healthcare institutions in China has grown rapidly, increasing from 6,993 in 2019 to 10,007 in 2023, representing a compound annual growth rate (CAGR) of 9.6%. This sector is projected to continue growing at a CAGR of 7.4% from 2023 to 2028, reaching 14,326 institutions by 2028.

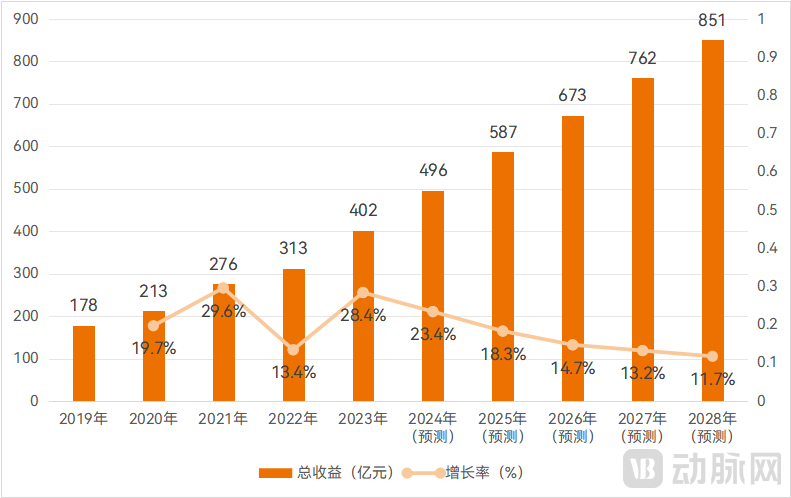

Based on the definition of private mid-to-high-end comprehensive healthcare service providers as institutions covering at least five specialties, with revenue from any single specialty accounting for no more than 50% of total revenue, the total revenue of such providers in China grew from RMB 17.8 billion in 2019 to RMB 40.2 billion in 2023, and is projected to reach RMB 85.1 billion by 2028.

Revenue Growth of Private Mid-to-High-End Comprehensive Medical Service Providers, Data Source: Frost & Sullivan

The growth trend is evident, as are the many challenges facing mid-to-high-end medical services. Internally, high service quality comes with high operating costs; externally, payers face thin margins and sluggish growth. Further development of the mid-to-high-end medical services market requires directly addressing these challenges.

Internally, to reduce costs, fully leverage digital tools to enhance operational efficiency.

Digitalization is increasingly penetrating the healthcare services sector, enhancing efficiency across the entire patient journey—pre-consultation, during consultation, and post-consultation. It also serves as a valuable aid to physicians in clinical tasks such as electronic medical record (EMR) management and assisted diagnosis, while leveraging large-scale data to support managerial decision-making.

High-level digitalization can promote the standardization of medical services and operational management. The synergy between digitalization and standardization enables effective management of existing institutions and facilitates the expansion into new ones.

In terms of external collaborations, more effectively maintain customers' health status and reduce payers' claim costs.

In 2023, Bupa, a global giant in high-end medical insurance, announced its withdrawal from the Chinese market, ceasing all insurance operations within China, including new policies and renewals, effective December 1, 2023. A major reason for Bupa’s exit was sustained operational losses. Both foreign-funded and Chinese-funded insurers face profitability pressures in the high-end medical insurance sector.

Unlike public medical institutions, which are subject to regulatory oversight under national health insurance policies, private medical institutions collaborate individually with various insurance companies and are not bound by unified, cost-containment regulations. This lack of standardized oversight may lead to over-treatment. While over-treatment may generate higher short-term revenues, it is ultimately counterproductive, akin to killing the goose that lays the golden eggs. Premium healthcare services and high-end medical insurance must be mutually reinforcing. To foster a virtuous cycle in the premium healthcare market, service providers must focus on enhancing medical technology, disease prevention, and health maintenance, while also collaborating with upstream pharmaceutical and medical device manufacturers to collectively reduce payout costs for payers.

References:

Jiemian News: Can Mid-to-High-End Medical Insurance Plans in the Thousand-Yuan Range, Advertised with “Zero Deductible,” Tap into the Middle-Class Market?

VBInsight: Intensifying Competition and Exit of Major Players, High-End Medical Insurance Urgently Needs “Rebalancing”