Medical VCs in 2026 Double Down on Category Leaders Amid Market Consolidation

Since the beginning of the year, many investment institutions have been changing their investment strategies.

“This year, we will strive to secure the top position in our niche sector.“During VCBeat’s recent interactions with numerous healthcare venture capital firms, many investment institutions have explicitly expressed this view.”

Compared with the red-hot healthcare venture capital market in 2020 and 2021, institutional investors now have an intense appetite for absolute top-tier companies. Previously, investment firms would prioritize betting on the top three players; if competition was fierce and they failed to secure a stake, they would consider the fourth or fifth-ranked companies as alternatives.

Wang Haijiao, Deputy General Manager of GTJA InvestmentInIn an interview with IPO Early Know at the beginning of this year, it was mentioned that for mature sectors, the goal is to invest in the company ranked first in terms of scale; secondly, if the sector is still in its growth and development phase, the preference is generally to invest in the company that is first or unique in terms of technology.

“In the current market environment, resources are converging on the top-tier companies. If the valuation is not excessively inflated, the leader in a niche segment has the greatest chance of success. The second-place player may also be worth considering if it demonstrates meaningful differentiation from the leader. However, companies ranked third or lower have virtually no chance,” Yang Junhao, a healthcare investor, told VCBeat.In the past, some large funds tended to pour capital all at once into the top players in a specific niche sector. That era of “machine-gun” investing is long gone. In this winter chill, investors must improve the hit rate of every bullet they fire.”

Amid the Rotation of Investment Strategies, How Will the Logic of the Healthcare Venture Capital Industry Evolve?

A mounting pressure is spreading across investment institutions.

“The market is currently under significant liquidity pressure, with many investment institutions facing fundraising and exit challenges, as well as intense scrutiny from LPs regarding investment returns,” Yang Junhao, a healthcare investor, told VCBeat.

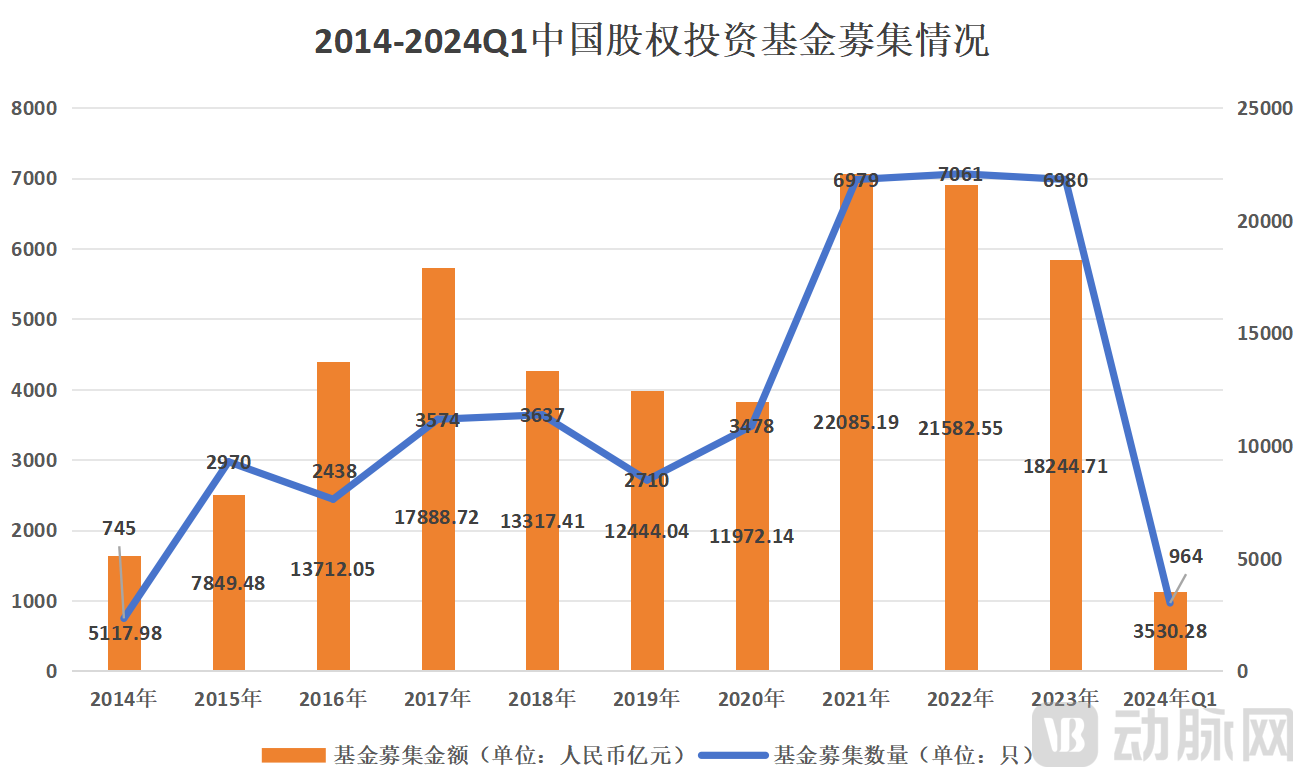

For instance, the pace of fundraising has slowed. According to data from Zero2IPO Research, the number and size of newly raised funds in China in the first quarter of 2024 were 964 and RMB 353.028 billion, respectively, representing year-on-year declines of 43.9% and 5%, continuing the downward trend.

(Data source: Zero2IPO Research; graphic by VCBeat)

Another example is the exit landscape. A recent research report on exits in the venture capital and private equity sector, released by the Beijing Fund Town Research Institute, shows that exit transaction activity in the primary market further declined in 2023. In the first three quarters of the year, there were a total of 2,251 exit cases in China’s equity investment market, representing a year-on-year decrease of 35.8%.

“At this time,The venture capital industry’s desire to bet on absolute top-tier companies is growing increasingly strong. These companies offer relatively certain and actionable prospects, enable faster exits, and provide substantial endorsement value for current funds.“Yang Junhao added, ‘Based on our observations,’In the broader biopharmaceutical sector, top-tier companies command substantial valuation premiums.“The resulting phenomenon is that once a company becomes the leader in a specific niche segment, its valuation is often higher than that of all its competitors.”

At an industry-specific conference, a managing partner of an investment group also expressed similar views. He believes that the pharmaceutical and healthcare industry comprises 40 to 50 niche segments, where leading companies in each segment enjoy valuation premiums; however, non-leading firms face valuation discounts.

For the aforementioned reasons, a growing number of healthcare investors are paying greater attention to and seeking out the leading companies in niche sectors, willing to incur higher investment costs to do so. A partner at a financial advisory firm stated,To secure the leading enterprise in process design within the cell and gene therapy (CGT) sector, four prominent institutions engaged in fierce competition, repeatedly driving up the valuation.。

“Growth potential and scarcity are the core focus of current investments in healthcare innovation enterprises. As long as a company’s technology is sufficiently advanced, its market ceiling is high enough, and its profitability is strong, its value will inevitably be realized; time will prove that the high valuations of such companies are justified,” said Yang Junhao, a healthcare industry investor.

A healthcare investor also mentioned,The most critical aspect of investment is to back the absolute market leaders; the risk of missing out on a potential industry giant far outweighs the risk of making incorrect investments in 100 companies.

As can be seen, the strategy of “investing in the number-one player in a niche segment” aligns with the current realities facing the healthcare venture capital industry.

As previously mentioned, it is both necessary and urgent for VC/PE firms to invest in “leaders of niche segments.” However, the challenge lies in determining, from a practical standpoint, how to assess whether a target company holds a position in its respective niche segment—and whether it ranks first.

When VCBeat inquired about this issue with numerous investment firms,Many healthcare investors have questioned the reliability of the “invest in the leader” criterion and expressed curiosity about the challenges of its practical implementation; on the other hand, some healthcare investors have shared their own reasoning behind “investing in the leader,” along with the perspectives and methodologies of certain institutions.. Given that certain information pertains to the core strategies of institutions, this article will present a simplified account in its exposition.

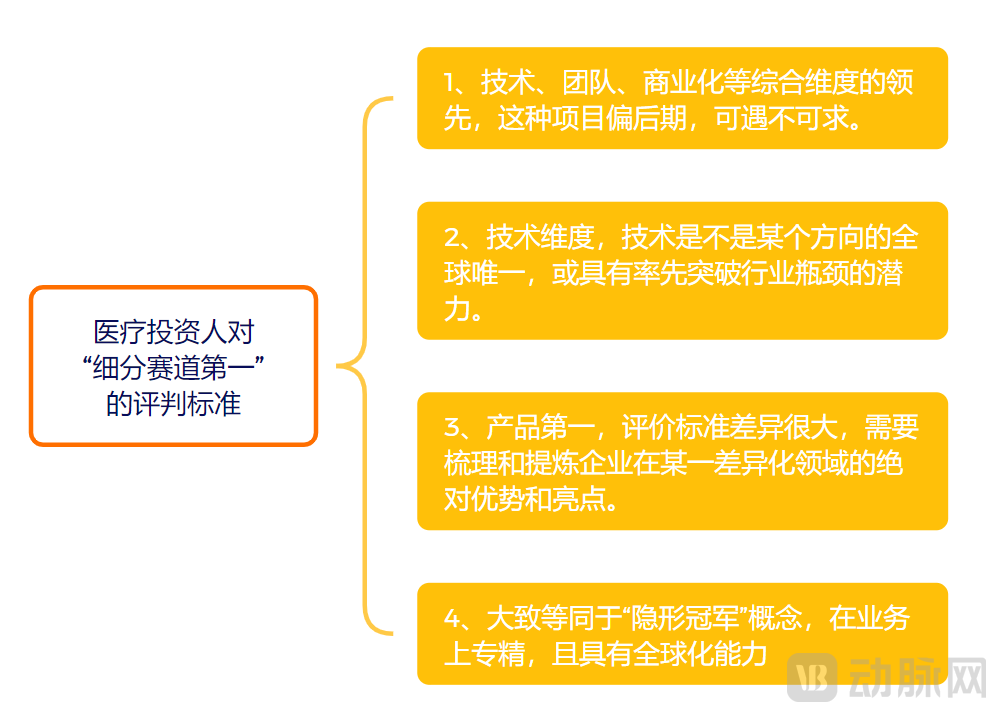

First, from the perspective of some investment firms, the ideal “number one” is a company that leads across comprehensive dimensions such as technology, team, and commercialization. However, such companies are rare and often only reach this stage in their later development phases, particularly when they already have data-backed market share. By that time, however, the valuation of these target companies has become exceedingly high, making it difficult for most institutions to enter.

Therefore, the criterion of being “first” applies more to early- and mid-stage enterprises, referring to being “first” in a specific dimension—such as technology, product, or team—rather than being “first” across comprehensive dimensions.

During VCBeat's research process,The dimension most frequently discussed by institutions, and with the least controversy, is technical standards: at the current stage, whether the technology of medical innovation enterprises is sufficiently robust, whether it is the only one globally in a particular direction, or whether it has the potential to take the lead in breaking through industry bottlenecks.

“In fact, for many domestic companies that claim to have original technologies, we conduct global source tracing and find that many of these technologies are not as robust as claimed, nor are they industry-leading,” said Yang Junhao, a healthcare investor. He noted that evaluating healthcare startups based on technological merit places exceptionally high demands on investors, who must not only understand technical details but also possess sound judgment regarding industry development cycles.

So, how can one identify companies that rank first in the “technological dimension”? Institutions generally consider the most efficient approach to be engaging with universities and research institutes.

A healthcare investor told VCBeat that when their firm previously anticipated the imminent surge in medical AI, they compiled a comprehensive list of global talent in AI-driven healthcare and academic institutions with deep expertise in this field. They identified each scientist and their specific technical focus, prioritizing visits to those with proprietary technological advantages. The firm then invested in companies founded by these individuals or provided startup funding to scientists who had not yet established their own ventures.

In addition, some institutions actively seek out underwater companies with proprietary technologies and compile lists of healthcare enterprises that have secured seed or angel funding in the past two years. They monitor these companies’ technological progress and, upon identifying any breakthroughs—particularly those leading the industry—they promptly engage to secure an allocation in their next round of financing.

Beyond technology, “product-first” has become the focal point for more institutions, yet “how to evaluate a product-first approach” remains a difficult question, on which the vast majority of institutions hold divergent views.

Some institutions consider the speed of regulatory approval (e.g., fastest to obtain certification) or clinical efficacy (significantly superior to others) as key benchmarks; others note that if a product is the first drug or therapy targeting a specific patient population, it truly addresses unmet clinical needs and operates in a blue-ocean market from a commercialization perspective; still others conduct a comprehensive analysis of a product’s competitiveness in the market based on its overall product strength.

It is not difficult to see that reaching a consensus at the product level is extremely challenging. “For investors,, whether to establish a unified evaluation standard is not actually important; the most crucial aspect is to systematically organize and distill the company’s absolute advantages and highlights in a specific area of differentiation.“The aforementioned FA partner summarized to VCBeat, ‘This is similar to how many healthcare companies, prior to their IPOs, strive to emphasize the uniqueness of their market and the innovativeness of their business operations. As a result, the market has seen the emergence of so-called “the first listed company in a specific niche” or “the leader in a particular segment.”’”

Taking the currently booming weight-loss sector as an example, companies can differentiate themselves by claiming titles such as “the leading publicly traded weight-loss drug company,” “the leading publicly traded weight-management company,” or “the leading publicly traded weight-loss device company.” More specific qualifiers can also be added, such as “the leading publicly traded weight-loss drug company focused on adult weight loss” or “the leading publicly traded health-management company focused on pediatric weight loss.” In other words, investment institutions currently favor targets that anchor a niche market, offer truly innovative products or solutions, and maintain an absolute leading position.

(Graphic by VCBeat)

(Graphic by VCBeat)

Additionally,Some healthcare investors believe that being “number one in a niche segment” can also be aligned with the concept of “hidden champions,” a term frequently cited in the venture capital community.According to the definition provided by renowned German author Hermann Simon in his book Hidden Champions: The Pioneers of Future Globalization, hidden champions are enterprises that are not widely known to the public but hold a leading position in a specific niche industry or market. They possess clear strategic positioning and core competencies, with products and services that are difficult to surpass or imitate. These companies rank among the top, or even first, globally within their respective industrial chains (more often upstream) or niche sectors.

Hermann Simon believes that,Only by specializing can one reach world-class standards, but specialization shrinks the market, necessitating globalization to expand it.Leveraging globalization, niche markets can enable mid-sized companies to achieve substantial scale. These are the most critical guiding principles for “Hidden Champions,” and also serve as key criteria for many investment institutions to assess whether a target company is the absolute leader in its specialized segment.

The book mentions numerous “hidden champion” enterprises, such as Dräger, a manufacturer of ventilators; Fresenius, a manufacturer of hemodialysis products; Brainlab, a provider of surgical navigation software; Otto Bock, a prosthetics and orthotics company; and International SOS, a Singapore-based enterprise that provides medical rescue services.

In addition to medical investors actively seeking out hidden champions, stakeholders across the industry are also looking for innovative healthcare products and solutions—and the innovative companies behind them—that represent technological advancement, high potential for domestic substitution in China, fulfillment of unmet clinical needs, global competitiveness, and prominent industry-leading effects within China’s and even the global healthcare sector.

For instance, at the recently held 8th Future Healthcare Ecosystem Expo, the “Innovative Products List for the Medical and Health Industry” was released to the industry for the first time. Two hundred representative innovative medical products and solutions attracted significant industry attention, with up to 80% of them being global debuts or pioneering medical innovations.

Whether investors are targeting the absolute top-tier players or engaging in the aforementioned industry activities, these trends provide high-potential projects with genuine original innovation more opportunities to showcase themselves, thereby allowing the entire industry to take notice of them.

Of course,Amid rapid industry shifts, healthcare investors have no choice but to concentrate their firepower on “category leaders in niche segments.” Despite the controversy and ambiguity surrounding implementation criteria, the amplification effect of absolute market leaders—whether in terms of fund endorsement or exit return probability—is unmistakable, making it imperative for VC/PE firms to include such targets in their portfolios.

And this will ultimately feed back into the investment ecosystem of the primary market, intensifying the Matthew effect.

As healthcare investors increasingly focus on absolute market leaders, capital is inevitably concentrating toward them, making fundraising more difficult for mid-tier and smaller enterprises.

Taking innovative drug developers as an example, some investors predict that half of these companies will disappear over the next three years as the current wave of venture capital investment recedes. The vast majority of those affected will be mid- to lower-tier players in various subsectors, as difficulties in securing financing will accelerate this process and intensify industry polarization.

At this time,Healthcare founders caught in the midst of this major trend must not focus solely on securing financing for survival; they must also pay attention to and refine their company’s positioning, anticipate future outcomes, and devise strategic responses.

“We often tell the companies we have invested in,”It is equally important to find a new way of ‘living’ and a dignified way of ‘dying’.“Yang Junhao, a healthcare investor, told VCBeat that the pace at which medical innovation startups are failing has accelerated in recent years, representing normal industry turnover,”Therefore, companies must either strive to rapidly advance from the lower or middle tiers to the top tier, or identify their core strengths and pivot to a differentiated niche segment; otherwise, they must accept being acquired or eliminated.

For instance, some innovative pharmaceutical companies positioned in cutting-edge technological fields may begin engaging with large multinational corporations (MNCs) if their commercialization progress lags behind after the release of Phase I clinical trial data. Once favorable Phase II clinical trial results are achieved, these companies can opt to sell directly to MNCs, rather than necessarily pursuing further financing or an independent initial public offering (IPO).

It should be noted that,The intrinsic quality of a company’s assets and their strategic value to the acquirer are key factors determining the successful execution of a merger or acquisition.Therefore, healthcare founders should not merely ponder the question of “to sell or not to sell,” but must instead refocus on the intrinsic value of their enterprises.

Taking the largest merger and acquisition in the ophthalmology industry since the beginning of this year as an example, Zeiss Medical’s acquisition of the Dutch ophthalmic company DORC hinges on DORC’s leading position in the combined phacoemulsification and vitrectomy system segment, as well as its strategic complementarity with Zeiss’s ophthalmic equipment ecosystem.

However,Projects that can exit via mergers and acquisitions are ultimately the minority; the majority will be directly eliminated.VCBeat's Recently Published Articles"Not Every Biotech Needs to Survive"It points out that, due to the unique nature of the biopharmaceutical industry, entrepreneurs face greater moral and ethical pressures compared to those in other sectors. Therefore, companies and founders who struggle to survive despite diligent management under challenging conditions should not be subjected to excessive criticism.

Like two sides of the same coin, industry differentiation has indeed posed challenges for many healthcare entrepreneurs, but a significant opportunity has also emerged: as more capital and resources flow toward companies that are truly innovative and sustainably leading, they will experience greater growth.

This process will inevitably involve challenges and growing pains, but once the dust settles, the healthcare innovation industry is bound to emerge stronger, paving the way for more sustainable and healthy development.