24-Hour Double Strike: Boston Scientific and Stryker Launch Aggressive Moves, Challenging J&J's $13.1B IVL Dominance as Market Enters All-Out War

Stryker

Medical Device R&D, Production, and Sales Company

Johnson & Johnson

Medical Device R&D and Manufacturer

Shockwave Medical

Cardiovascular Disease Treatment Device Developer

May 18,StrykerAfter completing the acquisition of Amplitude Vascular Systems (AVS) earlier this month, the company announced the official launch of clinical research.

May 19,Boston ScientificInAt the core forum of the EuroPCR 2026 conference in Paris, France,Highlighted Positive Results of the FRACTURE Pivotal Clinical IDE Trial for SEISMIQ 4CE Coronary IVL System, with a Surgical Success Rate as High as93.7%。

Earlier, in 2024, Johnson & Johnson acquired Shockwave Medical for $13.1 billion, bringing this former "unicorn" into its fold.

Behind this series of actions, a deeper change is actually taking place in the global cardiovascular intervention industry:IVL, is evolving from an "innovative device" into the next generation of complexityPCI (Percutaneous Coronary Intervention) Era Infrastructure. What all the giants are competing for is not just a high-margin balloon, but the future complexity."Entrance Rights" for Coronary Intervention.

Coronary Intravascular Lithotripsy (IVL) Catheter Concept Diagram

01

"SurroundedJohnson & Johnson

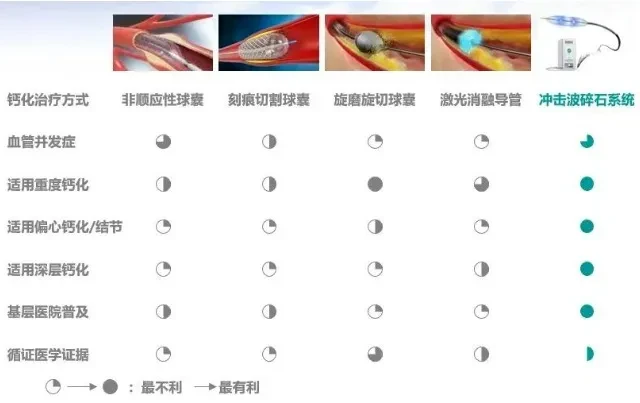

In the PCI operating room, severely calcified lesions have always been one of the most challenging types, often referred to as "the last tough nut to crack." In the past, doctors could only rely on high-risk and complex coronary rotational atherectomy, which has a steep learning curve and is associated with a significant rate of complications. The core principle of intravascular lithotripsy (IVL) is to adapt the acoustic wave technology used for breaking kidney stones in the body and apply it within the coronary arteries—delivering low-energy pulsatile acoustic waves through a catheter balloon to selectively target calcified plaques without damaging soft tissue.This "ability to strike from a distance" is considered by the industry as a generational disruption of traditional technology.

Global revenue in 2021 was only $230 million; Increased by 106% year-over-year to US$480 million in 2022, Climbed to 730 million U.S. dollars in 2023. On the eve of its acquisition, its trailing twelve months (TTM) revenue had broken through 780 million U.S. dollars, with gross margin consistently maintained at 86%-89% The Unparalleled Level.

This profit-making effect quickly caught the attention of industry giants. In June 2024, Johnson & Johnson acquired Shockwave Medical for $13.1 billion. This substantial investment brought significant performance dividends. Financial reports show that in 2025, Johnson & Johnson's medical technology segment generated $33.792 billion in revenue, with the cardiovascular department growing by 15.8%, and Shockwave contributing a remarkable 22.9% growth pull.This YearQ1, Shockwave Quarterly Revenue3.05Billion US dollars, year-on-year+18.5%Directly push the cardiovascular department to become the first growth curve of Johnson & Johnson Medical.

02

Controversy over Technical Routes

At the core of this IVL battle lies a dispute over physical mechanisms and engineering approaches. The industry has broadly formed three routes.

The first is the Electrohydraulic route represented by Shockwave.

The principle is that the electrode inside the catheter discharges to form a plasma bubble in the saline solution, releasing 360° circular pressure waves through the cavitation effect, simultaneously acting on both superficial and deep calcifications.

This is currently the most evidence-based mature route, with the longest clinical accumulation and the largest real-world data. However, due to the need for electrode structures inside the catheter, there are natural limitations in the catheter's outer diameter and compliance.

The second route is the laser-acoustic route represented by Boston Scientific's SEISMIQ (Laser-Acoustic).

It uses optical fibers to introduce laser energy into the balloon to excite the medium and generate pressure waves, rather than relying on electro-hydraulic discharge. There are three structural advantages: the catheter can operate at an extremely low inflation pressure (approximately 2 atm), offering significantly better deliverability compared to high-pressure balloons; it avoids the risk of high-voltage electric shock; and the pressure waves possess a certain directionality, enabling more precise targeting of calcified lesions in specific quadrants.

It is reported that the 4CE coronary version is currently in the pre-FDA submission stage, and the FRACTURE data will support the marketing application. Commercial scaling in the U.S. coronary market is expected as early as 2027.

The third route is the external mechanical power source route represented by Stryker (AVS).

The AVS Pulse system relocates the power source entirely outside the catheter, utilizing high-pressure CO₂ to drive hydraulic pulses, with no electrodes or optical fibers inside the catheter. This means the outer diameter of the catheter can be further reduced, theoretically improving its deliverability in complex calcified and tortuous lesions.Stronger.

03

The Unignorable Chinese Variable

If the global IVL race is a "free-for-all battle" unfolding in the main theaters of the U.S. and Europe, China has quietly evolved into the most noteworthy parallel battlefield. Not only does it have a vast patient population, but it has also given rise to a rare "domestic force" on the global stage.

"Report on Cardiovascular Health and Diseases in China 2023" shows,China's PCI surgery volume has exceeded 1.6 million cases, with about 30% experiencing diabetic calcification complications, among which severe calcification...Approximately 10%,Huge unmet needs.

In terms of imported products, Shockwave Medical, through a joint venture structure with CH Heart Rhythm Management, received NMPA approval in 2022 and achieved full commercialization in 2023. Regarding domestically produced coronary IVL, from 2023 to the present, there have been...6 sheetsThe registration certificate for domestically produced coronary IVL has been approved, respectively.Saihe Medical,Lepu Medical,Spectrum Medical, Zhonghui Medical, Blue Sail Boyuan, MicroPort Melody。

As expected, the rapid rise of Chinese manufacturers brought significant price impacts. In 2023, the local online listing price for Johnson & Johnson's Shockwave product wasRMB 29,800; while the corresponding price for domestically produced similar products isRMB 17,000-20,000Range, showcasing extremely strong cost-performance advantages.

At the same time, Johnson & Johnson has also begun "reverse localization."In December 2024, Johnson & Johnson, through localization, obtained the NMPA registration certificate for a single-use coronary intravascular shockwave catheter produced by JW Medical (Wuxi), directly receiving "Chinese production certification," enabling the establishment of ultimate price and channel defense in future centralized procurement.

According to incomplete statistics, there are alreadyMore than 20Companies have IVL-related pipelines, and 2026-2027 could be a密集 window period for the approval of domestically produced products. The industry believes that the next phase of differentiation for domestic IVL will focus on three directions:

1. The extreme optimization of physical outer diameter and passability, such as BlueSail 2.0mm diameter;

Second, the generational innovation of non-electrode discharge technology, such as the solid-state laser acoustic IVL and piezoelectric ceramic ultrasound being developed by Sino Medical, aims to bypass overseas patent blockades and reduce overall costs.

Third, the full workflow is system-level bound, with IVL products serving as a link in the "integrated diagnosis and treatment" of complex calcified lesions. By leveraging the solid foundation of domestic companies in conventional stents, guidewires, and intravascular imaging, an ecological leapfrogging can be achieved.

Over the past decade, China has reshaped the global landscape of several innovative medical device sectors, such as cardiac stents, TAVR, and electrophysiology, through its robust domestic innovation speed and intense competition. Today, IVL is likely entering a similar historical cycle.