Shanghai Changzheng Hospital Unveils Novel Spinal Facet Joint Prosthesis in New Patent Filing

Recently, Shanghai Changzheng HospitalA new orthopedic joint patent has been published. This patent is aArtificial Spinal Facet Joint, which can be used for internal fixation in spinal artificial facet joint systems to alleviate and treat various spinal disorders, including spinal fractures, lumbar disc herniation, and lumbar spinal stenosis.

Currently, the primary surgical treatments for spinal disorders are simple decompression surgery and decompression with fusion surgery. Both procedures inevitably require partial resection of the laminae, facet joints, and other structures. While these interventions alleviate the symptoms of spinal disease, they also create potential risks for future complications.The incidence of complications such as spinal instability and adjacent segment disc degeneration may increase.

Therefore, there is an urgent clinical need for a spinal artificial facet joint to reduce the probability of postoperative recurrence and complications.

And this patentCapable of simulating the physiological and biomechanical structure of spinal facet joints, implantation into the patient's body not only does not compromise spinal flexibility but also prevents a series of complications arising from spinal instability.

I. Spinal implants account for the largest share of the orthopedics market

With the intensification of population aging, the incidence of spinal disorders and the prevalence of osteoporosis are rising.Spinal implants have also become the largest segment within China’s orthopedic implant market.

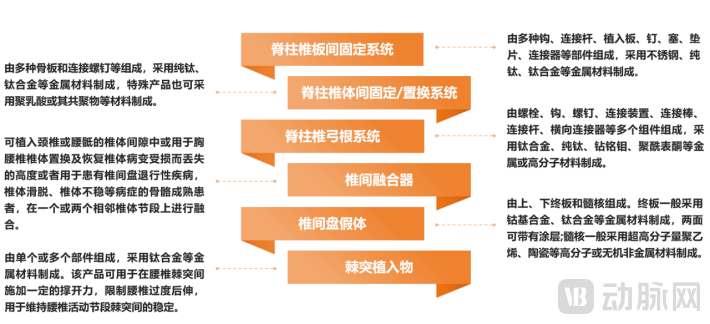

Due to the varying pathogenesis of spinal disorders, there is a diverse range of implantable devices, primarily categorized into spinal laminar fixation systems, intervertebral body fixation/replacement systems, pedicle screw systems, interbody fusion cages, disc prostheses, and spinous process implants.Six Types, with varying emphasis on the materials used.

Types of Spinal Implants

Types of Spinal Implants

The underlying design logic for spinal implants is largely similar, with product competitiveness primarily concentrated in technological processes such as surface finish, performance, and bone-contact surface treatment. In this field, the capabilities of Chinese manufacturers are significant, thereby driving a continuous rise in the substitution of domestic spinal implant products. According to statistics, the market size of China’s artificial spine industry in 2022Year-on-year increase of 13.1%, reachingRMB 13.06 billion。

such asWeigao, Zhengtian, Chunli, KailitaiThe market share of domestically produced orthopedic implant manufacturers is rapidly increasing. Of course, established medical device companies such as Johnson & Johnson, Stryker, and Medtronic still hold a significant position in the Chinese market. As of 2022, Johnson & Johnson and Zimmer Biomet remained the leading companies in China’s spinal implant market.

II. Post-VBP, the Market Landscape is Reshuffled

Since 2022, the national volume-based procurement (VBP) program for orthopedic spinal consumables has been officially launched, a policy that has also influenced changes in China’s market landscape.

From the perspective of bid-winning results,Major Domestic Manufacturers All Win Bids, some imported manufacturers, such as Zimmer Biomet and Stryker, chose to withdraw their bids or were disqualified due to factors including their global pricing strategies and limited profit margins for distributors. Therefore,The normalization of centralized procurement benefits leading domestic manufacturers, as distribution channels increasingly favor Chinese producers with cost advantages, thereby accelerating the process of import substitution.

While centralized procurement brings channel advantages, it will inevitably lead to shrinking product profit margins. According to the National Healthcare Security Administration, the prices of winning bid products have remained stable with a moderate decline; post-procurement product pricesAverage reduction of 84%.

Overall, domestic manufacturers have gradually taken a dominant position in the market following centralized procurement. Although market concentration remains relatively dispersed, the trend of domestic substitution is becoming increasingly evident, bringing new challenges along with it.

For companies that won bids in the centralized procurement, under the pressure of shrinking profit margins, how enterprises can ensure product quality and performance while reducing costs, improving efficiency, and enhancing market competitiveness has become a new challenge. Furthermore, how to increase market share when neither distribution channels nor pricing hold a competitive advantage isQuestions for Companies That Failed to Win the Bid. Consequently, companies that failed to win the bid must adjust their investments in research and development, brand promotion, and other areas.Only by formulating corresponding strategies and measures can one stand firm in fierce market competition.