Ma Ke of Haiwang Capital, Shanghai Science & Technology Innovation Group: 'Downturn Is a Critical Period for Strategic Investment in Future Healthcare'

The Evolution of Healthcare Investment Logic Aligns with the Broader Economic Cycle.

As economic cycles shift, the healthcare investment sector—particularly early-stage healthcare investment—continues to endure a winter, with investors and entrepreneurs advancing hand in hand. Meanwhile, we are also witnessing Chinese healthcare innovation leveraging the tailwinds of economic globalization to reach broader markets. Standing at the historical intersection of globalization and innovation, the potential of China’s healthcare industry is becoming increasingly prominent.

Amid the confluence of dual cycles, how can we uncover high-quality investment targets that have been overlooked? How can we navigate these cycles together? And how should we envision the future path of healthcare investment? On May 10, 2024, at the Top 100 Summit held during the VBEF Future Healthcare Ecosystem Expo organized by VCBeat, Marco Ma, Executive Partner of Haiwang Capital under Shanghai Science and Technology Innovation Group, delivered a keynote speech titled “Changes in Healthcare Investment Logic from the Perspective of Cross-Disciplinary Innovation,” sharing his insights and reflections on the future of healthcare investment during this challenging period.

Venture capital and early-stage investment strategies are significantly influenced by changes in the economic cycle.

China’s current development trajectory bears strong resemblance to Japan in the 1990s. On one hand, challenges such as real estate pressures, economic overheating, and rapid population aging have emerged; however, institutional differences may shorten the duration of these challenges. On the other hand, China’s healthcare industry has entered a prolonged period of rapid growth, significantly outpacing both Japan’s GDP and the Nikkei Index, with intense domestic competition driving a wave of overseas expansion. At this juncture, we must consider what new opportunities will arise during the evolution of health insurance payment capacity—for instance, import substitution? Exploring payment mechanisms for innovative drugs? Market shifts driven by declining birth rates and an aging population?

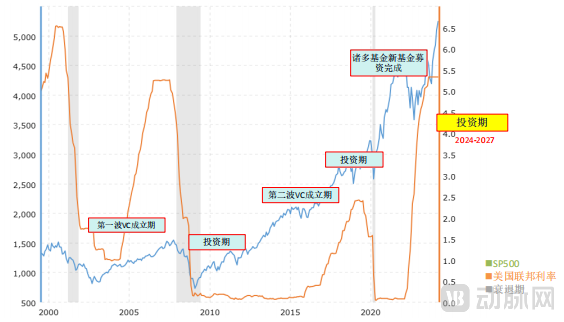

Overall, the economic cycles of China and the United States exhibit a high degree of correlation and resonance. Reviewing the evolution of venture capital (VC) over the past 20 to 30 years, the first cycle followed the dot-com bubble burst in 2000. During this period, the Federal Reserve engaged in rapid interest rate hikes followed by swift cuts, leading to capital outflows amid economic stimulus measures. Consequently, numerous US-dollar funds were established in China between 2003 and 2007, marking the dawn of China’s VC era. The second cycle began during the trough following the 2008 US financial crisis, spanning from 2009 to 2012. Evidence shows that investment firms active during this cycle achieved substantial returns in the subsequent phase and witnessed a second wave of VC fund formations. In 2018 and 2019, the Chinese stock market hit another low, presenting another favorable investment window, which culminated in significant gains in 2020 and 2021.

In summary, each cycle typically lasts approximately 5–8 years. From a broader cyclical perspective, I believe the period from 2024 to 2027 represents a favorable investment window. Although current sentiment is pessimistic, with market conditions perceived as dismal and cold, companies struggling to secure financing and facing dim prospects, it is precisely during such a downturn that high-quality enterprises often become available at reasonable valuations, warranting our careful and gradual consideration.

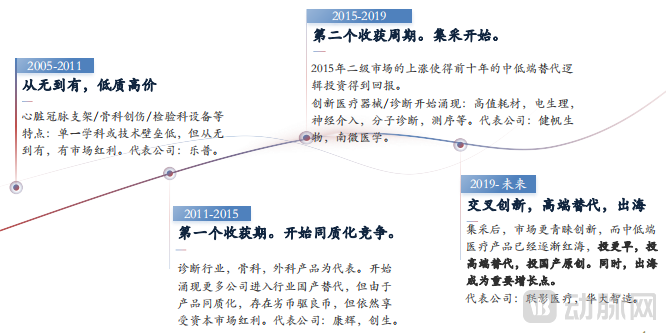

From inception through the first phase, China’s medical device innovation followed a model characterized by single-discipline, single-track development, progressing from low-quality, low-cost products to high-quality, low-cost domestic substitutes, with digital metrics alone sufficient to reflect corporate performance and growth. In the third phase, innovative medical devices and diagnostics began to emerge, gradually transitioning toward cutting-edge fields and expanding into overseas markets. Since 2019, the fourth phase has been marked by multidisciplinary cross-innovation as the mainstream, with high technological barriers and high-end import substitution becoming key growth drivers.

The investment transformation in medical devices and consumables reflects the penetration of cross-disciplinary innovation into healthcare, which is no longer confined to medical disciplines but has extended to the application of advanced manufacturing and processes in the medical field, as exemplified by South Korea’s Samsung and Japan’s Sony. Large-scale manufacturing enterprises with an innovative DNA can rapidly establish their presence in the healthcare sector and often surpass most startups in terms of foundational innovation.

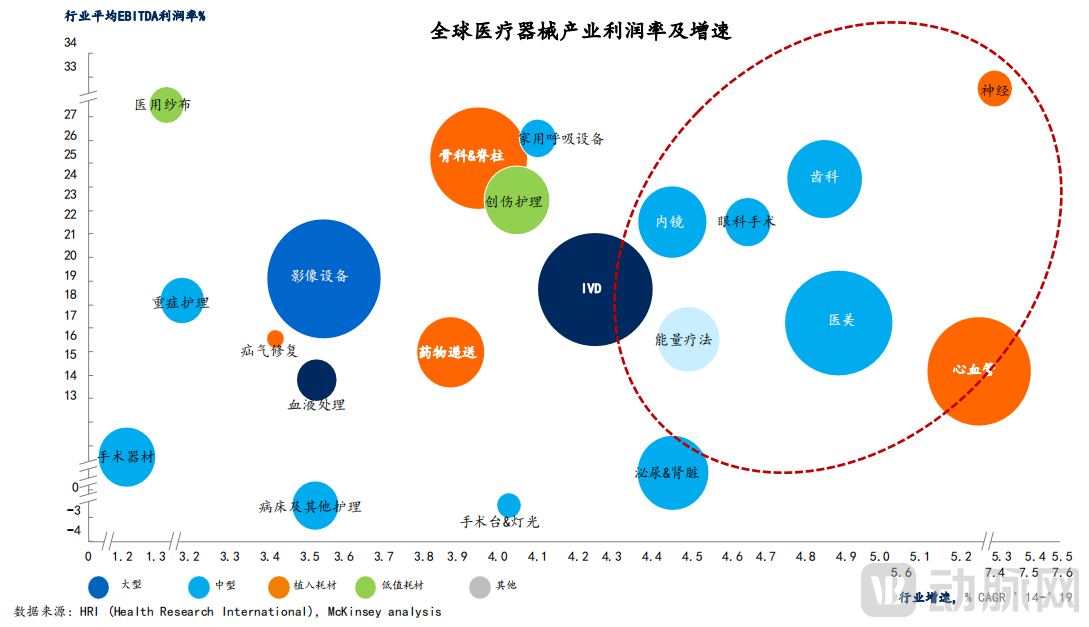

We conduct a bottom-up analysis of the future direction of the medical device industry, with the horizontal axis representing the growth rate of specific sub-sectors and the vertical axis indicating industry profit margins. We consider a sub-sector attractive if it simultaneously exhibits high profit margins and rapid corporate growth. The area within the red circle highlights currently popular investment tracks, which are also the key focus areas for Shanghai Science and Technology Innovation Investment. Upon further breakdown, Shanghai Science and Technology Innovation Investment will place greater emphasis on core, future-oriented, early-stage, and upstream bottleneck technologies, such as high-end imaging, ICU vital signs monitoring, cutting-edge in vitro diagnostics, and implantable and interventional products. It is evident that high-end, core domestic substitution will remain the primary investment thesis in the future.

Beyond the technical barriers mentioned above, investors place greater emphasis on comprehensive barriers, namely clinical, application, and market barriers. For a company with superior technology, has it adequately addressed the specific challenges within clinical scenarios? Is its product sufficiently user-friendly for physicians? How strong is its productization capability? Does the product possess iterative development capabilities? Can the company continuously expand its product portfolio in the future? Is the revenue ceiling high? Will it be able to meet the thresholds for an initial public offering (IPO) in the future? In summary, these comprehensive barriers fall into six major categories: platform-based technologies, robust productization capabilities, iterative development and product expansion capabilities, barriers built through clinical Principal Investigators (PIs) and Key Opinion Leader (KOL) resources, stickiness barriers within hospital markets, and strong sales capabilities.

According to data from the National Health Commission, China’s average life expectancy surpassed 78 years in 2021. As a startup, we must consider: Under current conditions of life expectancy and healthcare payment capabilities, what level of price support can be expected for highly innovative products? Where do the market potential and product positioning lie? How will continuous innovation drive iterative competition among treatment regimens?

New trends in entrepreneurship and investment are centered on meeting the demand for higher quality of life and improved living conditions. For instance, the rapid surge in the market for semaglutide-based weight-loss drugs is driven by the sharp rise in the number of people with diabetes, hypertension, and especially obesity. From 2004 to 2020, the obesity rate increased from 3.1% to 8.1%, underscoring the growing need to enhance the quality of life for individuals suffering from chronic diseases, age-related conditions, and metabolic disorders. Furthermore, clinical methodology iterations and the out-of-pocket payment market are continuously evolving alongside technological innovations. Entrepreneurs and investors must remain vigilant regarding the substitution threats faced by traditional manufacturers and their imperative for innovative transformation.

Data indicates that Asia accounts for approximately 20% of global medical device consumption. If we assume the Chinese market represents half of Asia’s share, this implies a 10:1 ratio between the global medical device market and the Chinese market, leaving a market opportunity nine times larger outside China. If an investment target is confined to intense domestic competition in China and lacks the capability to expand overseas, why should we forgo a market nine times its size? This is a critical consideration we must address.

According to statistics, the average proportion of overseas revenue for leading medical device companies such as Medtronic, Johnson & Johnson, and Danaher exceeds 50%. The overseas revenue of leading listed domestic medical device companies is also growing rapidly; for instance, Mindray’s share increased from 26% to 40%, and United Imaging’s rose from 2% to 14.7%. In comparison, the medical divisions of companies in export-oriented economies, such as Samsung and Olympus, generate over 70% of their revenue from overseas markets. Innovation at such companies is inherently globalized and capable of expanding beyond their countries of origin.

From an investor’s perspective, we do not necessarily determine whether a company has global expansion capabilities at the time of investment. However, from technological and product standpoints, it should possess potential for international markets, and its founders should demonstrate both vision and capability for global expansion. On the other hand, we must also critically assess ourselves to determine what resources and value we can provide to support the company’s overseas growth.

In addition, we must persist in investing at the right time.

Taking the acquisition of a biopharmaceutical company at the end of last year as an example, Series A investors achieved a multiple on invested capital (MOIC) of 6x and an internal rate of return (IRR) of 31% upon exit. However, starting from Series B, the IRR showed a linear decline, with IPO investors even incurring losses. During the private placement period after the IPO but before the acquisition, performance was outstanding, yielding an IRR of 235% and a return of 2.8x. This indicates that the timing of investment is crucial; optimal investment opportunities tend to follow a barbell strategy—either investing early or investing in certainty when there are relatively clear exit opportunities.

To summarize, I have two key points. First, “invest where others are not looking.” It is a significant challenge for investors to identify companies at an earlier stage and possess the ability to determine whether a project is worthy of investment. Second, can you engage with entrepreneurs, encourage them to start ventures, orchestrate these initiatives, and provide substantial support and confidence to facilitate their commitment? Objectively speaking, discovering high-quality early-stage targets is extremely difficult, particularly for projects that remain under the radar. Therefore, we should foster synergies with other funds to capture more early-stage opportunities.

The second principle: “Exit when the crowd is loudest.” When market liquidity is abundant and secondary markets are performing well, primary markets often become “overheated.” It is essential to think calmly and assess whether the current market is overheated or merely reflecting reasonable growth expectations. For companies with overextended valuations, investors should decisively and gradually exit, at least locking in a portion of DPI (Distributed to Paid-In Capital). Of course, a prerequisite for exiting is that investors have sufficient insight into the company’s internal operations and a thorough understanding of its market potential.

Overall, the core logic for future healthcare investment prioritizes unmet market needs, followed by high-end substitution and the localization rate of premium products in niche segments, and finally, overseas expansion opportunities. We have also observed that during economic downturns, M&A and license-out activities remain highly active (particularly in the biopharmaceutical sector), making exit opportunities through acquisitions impossible to ignore. Taking the pharmaceutical industry as an example, Haiwang Capital is currently focusing on new opportunities empowered by large language models (LLMs) in drug discovery.

China’s venture capital industry has evolved over the past two decades. As one of the most market-oriented limited partners (LPs), Shanghai Science and Technology Innovation Group has invested in 160 general partners (GPs). Today’s LPs possess deeper industry insights, more refined strategic understanding, and greater experience, leading to a more objective assessment of returns. Consequently, the key challenge for emerging GPs lies in ensuring internal consistency among their investment strategy, differentiation, and actual performance. Only by achieving coherence across these three dimensions can they succeed and meet the rigorous standards set by LPs.

Valuations in the primary market are currently showing a polarized trend: high-quality companies can still raise capital quickly at robust valuations (as investors seek certainty); mid-tier companies, just below the top tier, face significant fundraising challenges and must lower their valuations; while weaker companies will experience a wave of bankruptcies during the downturn.

Furthermore, I believe the economic downturn may persist until the end of the rate-cutting cycle in developed countries in 2026, or even into 2027—a prolonged period. Each rate-cutting cycle tends to be the most damaging phase; therefore, I anticipate that this year and next could mark the market’s weakest period. If you are an investor, you should collaborate with your portfolio companies to strategize on how to weather the winter. If you are an entrepreneur, you must focus on how to survive the winter.

Furthermore, as an investor, I believe we should be willing to invest time in conducting more thorough assessments and considerations of entrepreneurs and potential targets, thereby deepening our judgment of people. Ultimately, we must have the courage to invest in disruptive innovation. I recognize that many investors currently prioritize cash flow and service-oriented businesses due to fears of company failure. However, the risks and returns of early-stage investing are proportional; waiting for economic improvement may result in diminished explosive growth potential. Therefore, it is essential to maintain a certain allocation toward disruptive innovation.