China's Peptide CDMO Sector Gains Momentum as TedMed Files for Hong Kong IPO

WuXi AppTec

New Drug R&D and Production Service Provider

ASYMCHEM

Pharmaceutical R&D and Production Outsourcing Service Provider

GLP-1 Remains Red-Hot, Propelling Drug Developers to the Forefront and Now Opening Capital Market Doors for Upstream Suppliers

On May 31, peptide CDMO Medtide formally filed its prospectus with the Hong Kong Stock Exchange, seeking a listing on the Main Board.Since its inception, Medtide has received investments from institutions including Puhua Capital, Haibang Investment, Qiantang Industrial Group, and Jingsheng Capital.

Medtide is the parent company of China Peptides. In 2015, China Peptides was acquired by Xinbang Pharmaceutical. In 2020, Zhejiang Medtide repurchased China Peptides from Xinbang Pharmaceutical. Established in 2001, China Peptides is a well-known peptide CDMO with R&D and production bases in both China and the United States, serving numerous multinational corporations (MNCs) and biotech companies.

Therefore, Medtide’s IPO application can be seen as a long-established peptide CDMO finally embarking on the path to public listing, also illustrating that the GLP-1 boom is benefiting upstream suppliers. It is an industry consensus that peptide production capacity is in short supply. Not long ago, Eli Lilly announced an additional $5.3 billion investment to expand GLP-1 production capacity at its Indiana manufacturing site—the largest manufacturing investment in the century-old pharmaceutical company’s history and the largest single investment in synthetic drug API manufacturing in U.S. history.

Furthermore, CDMOs such as WuXi AppTec and ASYMCHEM are aggressively expanding production capacity and securing successive orders. In a biopharmaceutical market that remains subdued, are domestic peptide CDMOs becoming increasingly competitive?

How Is the Business of Established Peptide CDMOs?

In Medtide’s prospectus, its 2023 revenue was RMB 337 million, accounting for 1.5% of the global market share. Based on sales data, Frost & Sullivan defined the company as the world’s third-largest CRDMO focused on peptides.

Source: Medtide Prospectus

According to Frost & Sullivan, this ranking defines peptide-focused CRDMO companies as those deriving more than 50% of their revenue from peptide CRDMO services. Companies A and B in the table refer to two Swiss peptide CDMO giants, Bachem and PolyPeptide, respectively, followed by Medtide.

As of January 1, 2023, Medtide’s peptide project pipeline comprised 249 CDMO projects and six CMO projects. In 2023, the company also secured 72 new CDMO projects and seven new CMO projects. Furthermore, throughout 2023, Medtide completed 8,728 CRO projects. Medtide’s projects span more than 50 countries, covering major markets such as China, the United States, Japan, Europe, South Korea, and Australia. As of May 27, 2024, the company had nine GLP-1 drug development projects with seven clients developing GLP-1 products. In addition to peptides, Medtide has developed a diversified project pipeline focused on other categories of TIDES drugs, such as POC, PDC, and RDC.

However, in terms of revenue, Medtide reported revenues of RMB 282 million, RMB 351 million, and RMB 337 million from 2021 to 2023, respectively; its adjusted net profits were RMB 108 million, RMB 128 million, and RMB 101 million, respectively. In 2023, when the peptide drug market was booming, the company’s revenue and profit instead declined.

In its prospectus, Medtide pointed out that the decline in its 2023 revenue was primarily due to a decrease in average revenue per customer, which was mainly attributed to a significant reduction in demand for its services from three major customers, resulting from changes in their own peptide drug development resources, plans, and cycles.

Medtide’s strength may lie in its subsidiary, China Peptides, which has cultivated deep expertise in the peptide field for many years. With a profound understanding of peptide drug research and development, as well as strong communication channels with pharmaceutical companies in both China and the United States, Medtide is well-positioned to secure a place in the long-term competition for peptide production.

What is the current level of peptide production in China?

If anyone has truly reaped the production benefits of GLP-1, it is undoubtedly the major CDMO giants.

WuXi AppTecThe capacity expansion projects at the Changzhou and Taixing bases were completed in 2023, with the new production capacity becoming operational in January 2024, increasing the volume of solid-phase peptide synthesis reactors to 32,000 L. Eli Lilly collaborates with WuXi AppTec to produce a key ingredient of tirzepatide, and Eli Lilly has stated that finding alternative suppliers “may not be feasible or could take a considerable amount of time.”

Leveraging its capacity advantages, WuXi AppTec’s TIDES business (oligonucleotides and peptides) generated RMB 3.41 billion in revenue in 2023, a year-on-year increase of 64.4%. By the end of 2023, the backlog of orders for the TIDES business had grown significantly by 226% year on year.

ASYMCHEMis the CDMO for mazdutide, a dual-target weight-loss drug co-developed by Innovent Biologics and Eli Lilly. This GLP-1R/GCGR dual agonist has demonstrated superior weight-loss efficacy compared to semaglutide and tirzepatide, and is expected to be officially launched this year or next. Additionally, ASYMCHEM has secured orders for Eli Lilly’s oral small-molecule drugs and is advancing peptide orders for Eli Lilly’s tirzepatide, with some projects having entered the validation production phase.

To meet the demands of commercial projects, ASYMCHEM is accelerating the expansion of its commercial-scale peptide production capacity, which is expected to reach 14,250 L by the end of June 2024.

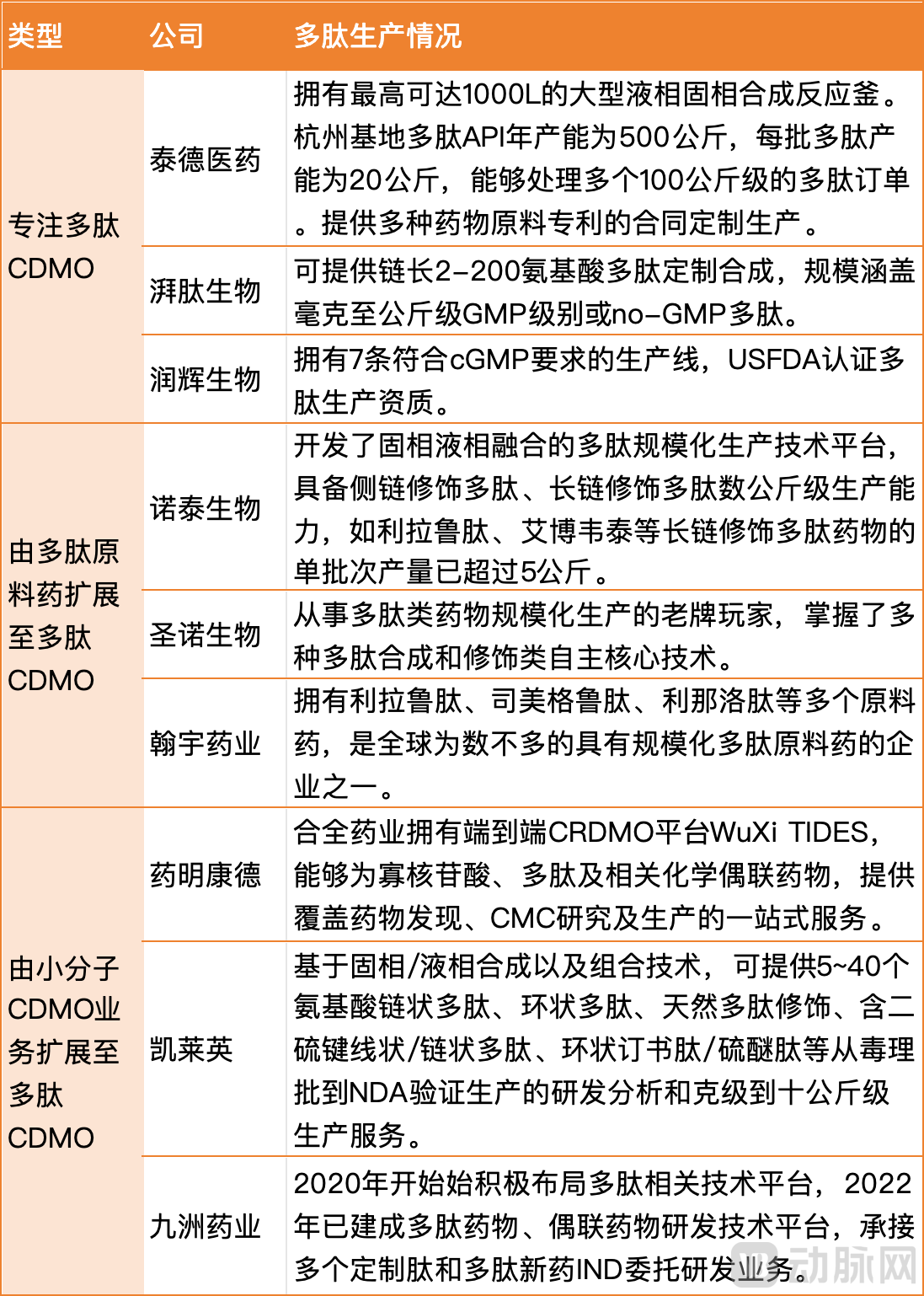

There are also some companies that have disclosed their production capacity, such asHybio PharmaceuticalProduction capacity of 1,000 kg has been established;Nuotai BioFollowing the technological upgrades to its existing production facilities, the annual capacity reached 400–500 kg. The submission of documents for this purposeMedtideHangzhou has an annual peptide API production capacity of 500 kg, with a batch capacity of 20 kg, enabling it to handle multiple orders at the 100-kg scale.

Nuotai Bio has signed a seven-year supply contract with a major European pharmaceutical company for cGMP-grade advanced pharmaceutical intermediates, with a cumulative contract value of approximately $102 million; deliveries commenced in 2024. Hybio Pharmaceutical has entered into a contract worth RMB 219 million with an overseas client for the supply of GLP-1 peptide active pharmaceutical ingredients (APIs).

Next, the domestic patent for semaglutide in China is set to expire in 2026. A large number of domestic generic drug manufacturers have already made strategic arrangements, which will further stimulate demand for production orders, and the imbalance between supply and demand is expected to persist. According to Frost & Sullivan data, the global market size for peptide drugs, measured by sales revenue, is projected to grow to USD 261.2 billion by 2032, while the market size for peptide drugs in China will reach RMB 251.2 billion.RMB。

The market is vast, but rapidly entering the peptide production arena is no easy feat. In other words, the peptide CDMO sector is characterized by high barriers to entry. Combinatorial peptide synthesis involves complex methodologies and numerous considerations, while the generation of diverse and complex impurities during synthesis poses significant challenges for purification.

Currently, peptide production in China primarily relies on chemical synthesis, dominated by liquid-phase and solid-phase synthesis methods. With the surge in GLP-1 drugs, the industry is beginning to optimize manufacturing processes, showing a trend toward the integrated development of chemical synthesis, biological fermentation, and enzymatic hydrolysis. However, most companies still lack sufficient accumulation of biological technologies.

Apart from a small number of companies specializing in peptide CDMO, the domestic players capable of building peptide manufacturing capacity and addressing a wide range of end products are primarily enterprises that have expanded from peptide active pharmaceutical ingredients (APIs) to peptide CDMO, as well as established small-molecule CDMO companies with strong capabilities.

Representative Domestic Peptide CDMOs, Compiled by VCBeat

Can It Compete Globally?

According to Frost & Sullivan, the global market size of peptide CDMOs, measured by sales revenue, increased from $1.6 billion in 2018 to $3.1 billion in 2023, representing a compound annual growth rate (CAGR) of 14.8%, and is projected to further grow to $18.8 billion by 2032, at a CAGR of 22.0%.

Bachem, currently the global leader in the peptide CDMO market by share, reported revenue of $644 million in 2023, with its peptide business contributing $431 million. Bachem is actively expanding its production capacity, with new facilities scheduled to commence operations in the second half of 2024, aiming for annual revenue of approximately $900 million by 2026.

PolyPeptide, ranked second, reported revenue of $347 million in 2023, with its peptide business contributing $313 million.

In other words, in this rapidly expanding market, there is currently no absolute leader.Although peptides are not WuXi AppTec’s core business, its TIDES segment generated approximately $474 million in 2023, a figure not significantly behind the top two global players. Moreover, WuXi AppTec’s order backlog continues to grow, with TIDES revenue reaching RMB 780 million in the first quarter of this year, representing a year-on-year increase of 43.1%.

While domestic peptide CDMOs naturally possess cost and supply chain advantages, Novo Nordisk and Eli Lilly have not made significant investments in China for their capacity expansion. Instead, they have primarily focused on building their own factories or forming partnerships in Europe and the United States, citing concerns over unknown systemic risks and supply chain security.For example, Novo Nordisk plans to invest approximately $8.7 billion in its Danish production facilities from 2022 to 2029, primarily to increase the production of active pharmaceutical ingredients (APIs). To address supply gaps in raw materials and formulated products, Eli Lilly announced last November a $2.5 billion investment in the construction of its Alzey plant in Germany; reached agreements with National Resilience and the Italian pharmaceutical company BSP Pharmaceuticals this March; and acquired a manufacturing facility from Nexus Pharmaceuticals in April, among other initiatives.

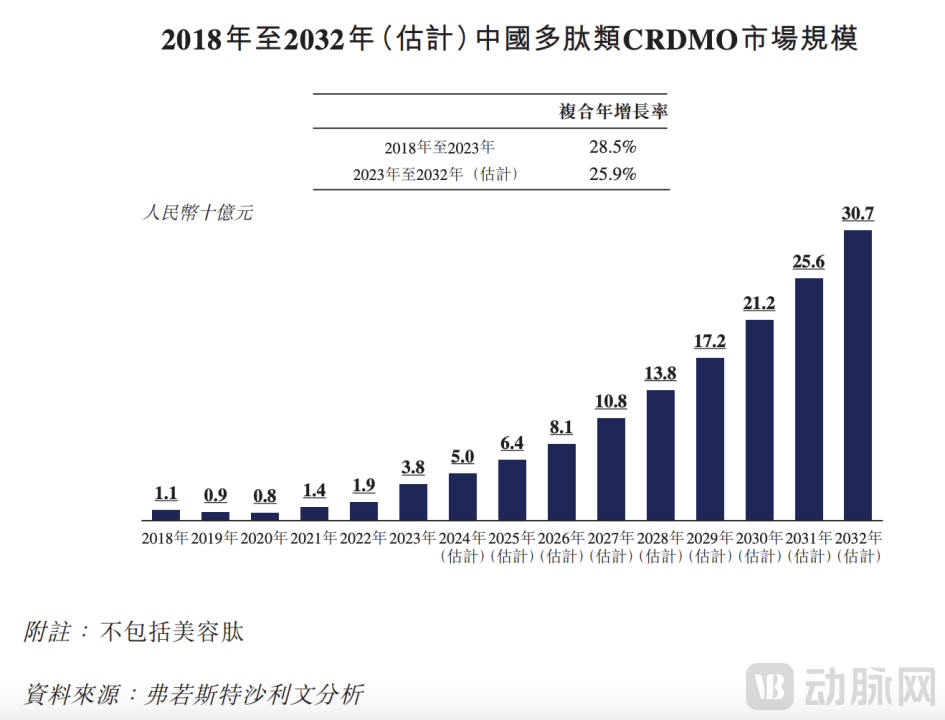

This has limited the full participation of China’s peptide CDMOs in global competition. However, as patents for originator drugs expire, the expansion of the domestic market will absorb part of the production capacity, and the cost advantages of Chinese peptide active pharmaceutical ingredients (APIs) will become evident.According to Frost & Sullivan, the market size of China’s peptide CDMO industry reached RMB 3.8 billion in 2023 and is projected to further increase to RMB 30.7 billion by 2032, representing a compound annual growth rate (CAGR) of 25.9%.

Source: Medtide's IPO Prospectus

At that time, China’s global market share in peptide CDMO is expected to reach approximately 22%, compared to only around 5% in 2020.

Peptide CDMO Is a “Hard Demand”

For pharmaceutical companies, peptide drug CDMOs represent a “hard necessity”; given the high upfront investment and long lead times required for peptide production, few pharmaceutical companies can develop these drugs without relying on CDMOs.

“Unlike small-molecule drugs, which require relatively modest investment in manufacturing—with facilities of 1,000 L or 2,000 L being sufficient—it is nearly impossible for peptide pharmaceutical companies to handle production in-house. Moreover, peptide CDMOs benefit from economies of scale, enabling them to reduce costs through appropriate synthesis methods,” said an industry insider.

Compared with small-molecule drugs, peptide drugs have more complex structures. Impurity control represents a significant challenge throughout the entire manufacturing process. Unlike small-molecule drugs, which can achieve purity levels exceeding 98.5% or even 99%, attaining a purity of 93–94% for peptides is already considered favorable. Given the wide variety of impurities, establishing quality standards is highly complex. Typically, in innovative small-molecule pharmaceutical companies, the ratio of personnel engaged in process development to those in analytical development is 1:1; however, due to the substantial challenges associated with peptide analysis, this ratio needs to be expanded to 1:2 or even 1:3.

Scale-up of peptide manufacturing processes is also challenging. There are significant barriers between the R&D processes and large-scale production of peptide drugs. Furthermore, a wide variety of protecting agents are required during peptide synthesis. The selection and use of these protecting agents have become a key focus for environmental organizations. Continued reliance on traditional solvents poses substantial challenges, necessitating the exploration of novel protecting agents as alternatives.

Overall, China’s peptide CDMO sector remains immature, particularly due to a shortage of high-level talent with specialized peptide expertise and the ability to comprehensively oversee peptide drug manufacturing.

Taking the currently hottest GLP-1 as an example, capacity planning for GLP-1 is intricate and requires comprehensive consideration of multiple factors, including sales forecasts, cash flow, and competitors’ responses. Early entrants may benefit from appropriately overbuilding capacity to seize market share, whereas latecomers need to exercise greater caution.

“A CDMO executive stated, ‘There are very few candidates in the market who can meet our requirements. Likewise, I believe it is extremely difficult for an innovative pharmaceutical company to recruit professionals with a peptide background.’”

However, the high barriers to entry in peptide manufacturing yield substantial returns. CDMOs are required to provide sample synthesis during the preclinical research phase of peptide drugs, and the subsequent commercial launch of new drugs relies even more heavily on CDMOs’ industrialization expertise in process development and quality control. Consequently, peptide CDMO clients often exhibit a stronger dependence on these services. Furthermore, the complex production processes and significant quality control challenges associated with peptides typically necessitate that the entire manufacturing workflow—from starting materials to active pharmaceutical ingredients (APIs)—be completed within a single enterprise. This makes intermediate handovers difficult and drives a high demand for integrated solutions.

With increasing market attention and investment in peptide drugs, new blockbuster candidates beyond GLP-1 may emerge, and peptide-drug conjugates (PDCs) are also highly anticipated. Chinese CDMO companies specializing in peptides are poised to secure influential positions in the global wave of peptide drug development—provided they obtain entry into peptide manufacturing and possess strong evolutionary capabilities.

References:

Guolian Securities: Peptide Drugs Have Broad Prospects, with Rising Demand for CDMO/API Services

Drug Hunter Club, https://mp.weixin.qq.com/s/7dNJSqIbbJpSwwV4Wr1B_A