Yimai Sunshine Lists on HKEX, Becoming China's First Dedicated Medical Imaging Services Company to Go Public

Today, RIMAG, a third-party medical imaging service provider, listed on the Hong Kong Stock Exchange. As there had been no prior listings of companies primarily engaged in third-party medical imaging services, RIMAG has become the “first stock in medical imaging services.”

Imaging Center Services, Imaging Solution Services, and RIMAG Cloud Services constitute the three major business segments of RIMAG; among these, Imaging Center Services is the core business with the highest revenue share. As of the end of 2023, RIMAG’s medical imaging center network consisted of 97 imaging centers.

The prospectus shows that,In 2021, 2022, and 2023, RIMAG generated revenues of RMB 592 million, RMB 784 million, and RMB 929 million, respectively. With steady revenue growth and the initial emergence of economies of scale, RIMAG turned profitable in 2023, posting a profit of RMB 36.57 million.

Third-party medical imaging services have been a key area of strong national support in recent years. Third-party medical imaging service providers, including RIMAG, have played a significant role in improving access to healthcare, promoting the balanced distribution of medical resources, and enhancing the diagnostic capabilities of primary care institutions, thereby gaining market recognition.

In the past, patients preferred to seek medical care in major cities and large hospitals, particularly for more serious conditions. This tendency was not only due to deeply ingrained perceptions that are difficult to change in the short term, but also stemmed from a critical factor: the lack of advanced diagnostic imaging equipment in smaller cities and primary healthcare facilities. Constrained by local fiscal expenditure requirements, healthcare institutions struggled to rapidly deploy advanced medical imaging devices aligned with local clinical needs. With many essential diagnostic tests unavailable locally, patients had no choice but to travel to major cities and large hospitals for care.

In recent years, the state has increased investment in primary healthcare equipment. Favorable policies have promoted the introduction of advanced imaging equipment by primary healthcare institutions. However, due to the insufficient level, professional knowledge, and experience of radiologists and imaging technologists, as well as the limited ability of relevant clinicians to select precise imaging examination methods,Some primary healthcare institutions have exhibited a phenomenon where medical equipment, though not low in grade, suffers from low functional utilization. This is particularly evident with advanced imaging devices featuring high-end and complex functions, which have failed to deliver their intended value.

For example, even though some primary healthcare institutions in China are equipped with advanced CT scanners capable of cardiac imaging, the actual utilization rate of CT for cardiac scans remains low.

In 2013, the State Council’s “Several Opinions on Promoting the Development of the Health Service Industry” proposed vigorously developing third-party services and guiding the development of specialized medical laboratory centers and imaging centers. Over the subsequent decade, the state successively issued multiple documents,Encourage medical imaging diagnostic centers to develop chain and group operations, establishing standardized management and service models. Encourage regions with appropriate conditions to incorporate independently established medical imaging diagnostic centers and medical laboratories into mutual recognition systems, providing testing and examination services to healthcare institutions within the region and achieving resource sharing.

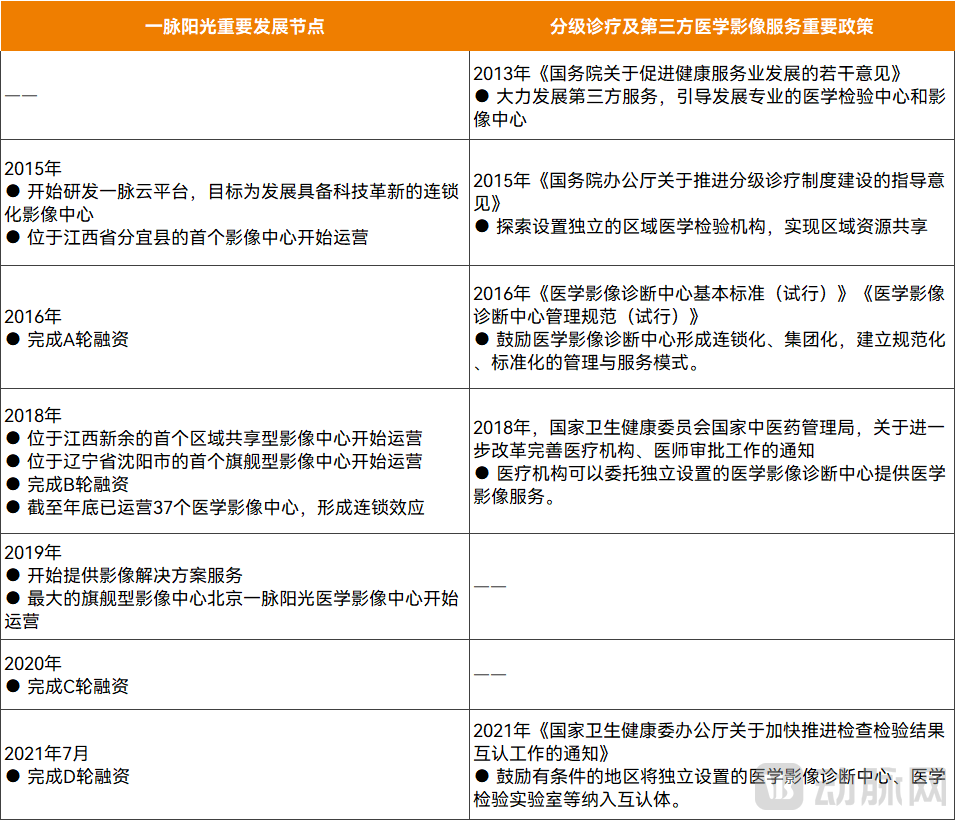

Cracking the challenges of medical imaging examinations is crucial to the advancement of tiered diagnosis and treatment. RIMAG has seized this opportunity, aligning precisely with key milestones in policy implementation.

Key Milestones for RIMAG Prior to Its IPO and Major Policy Milestones; Source: Prospectus, National Health Commission

In 2014, RIMAG was established, and in 2015, its first imaging center located in Fenyi County, Jiangxi Province, began operations.

In 2018, RIMAG began establishing a diversified network of imaging centers. Its first regional shared imaging center in Xinyu, Jiangxi Province, and its first flagship imaging center in Shenyang, Liaoning Province, commenced operations. By the end of 2018, RIMAG was operating 37 medical imaging centers, achieving a chain effect.

As of the end of 2023, RIMAG’s medical imaging center network comprised 97 imaging centers, covering 17 provinces, autonomous regions, and municipalities directly under the Central Government, extending from first- and second-tier cities to 59 county-level administrative divisions.

Among the 97 imaging centers, the Xinyu Regional Shared Imaging Center has emerged as a prominent benchmark. In 2022, “The Xinyu Model for Building County-Level Medical Imaging Sharing Centers” was featured in People’s Daily’s publication, “Vivid Practices of Chinese-Style Modernization: Typical Cases of National Governance Innovation Experiences (2021–2022).”

This model integrates the medical imaging departments of multiple municipal-level healthcare institutions to establish a Medical Imaging Sharing Center, which extends its services downward to county-level medical institutions and township health centers. While optimizing medical resources, alleviating fiscal burdens, reducing medical insurance expenditures, and lowering patient costs, it also enables patients to access higher-quality medical services closer to home.

After a decade of consolidation, RIMAG has bolstered its regional business operations by supplementing inspection equipment resources, particularly with advanced high-end devices.As of the end of 2023, RIMAG had equipped and managed a large number of advanced imaging devices, including PET scanners, superconducting MRI systems, and multi-slice spiral CT scanners, totaling more than 220 units, through its flagship imaging centers and regional shared imaging centers; it also provided imaging solution services to over 80 medical institutions.

At the same time, RIMAG has also supplemented physician resources in the regions where it operates.As of the end of 2023, more than 230 licensed radiologists had designated institutions under RIMAG as their primary practice sites.

Imaging center services are RIMAG’s core business, accounting for the largest share of revenue among its three major business segments.

Third-party medical imaging centers require significant capital investment and have long payback periods, as they must procure competitive diagnostic equipment that effectively meets clinical needs, while also complying with policy requirements for facility space (including equipment and office areas) and staffing with medical personnel of appropriate qualifications. However, among various types of non-public medical institutions, the asset-heavy nature of third-party medical imaging centers is particularly pronounced.

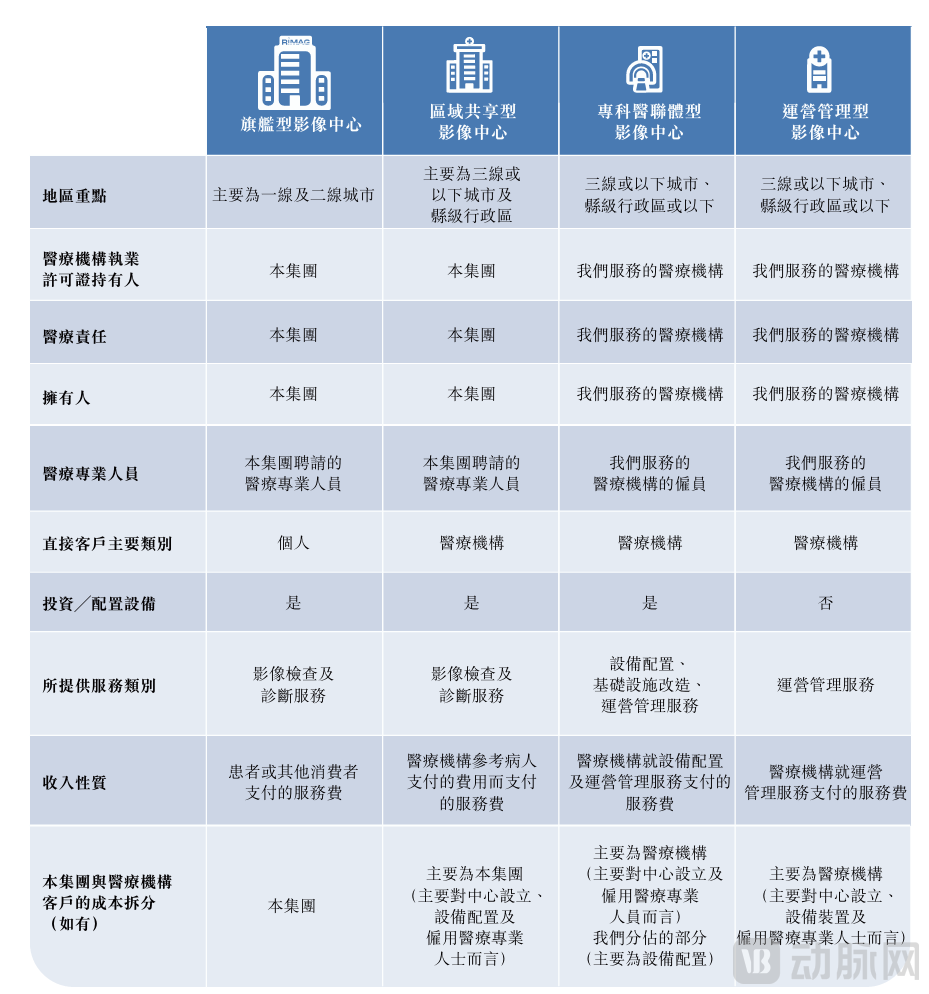

Why Has RIMAG Achieved Profitability Within 10 Years? Primarily because the company established a complementary “2C+2H” medical imaging center model, which significantly shortened its path to profitability.

Specifically, RIMAG has deployed four types of imaging centers across cities of varying scales, adopting differentiated strategies for their construction and operation.

Flagship imaging centers are typically located in densely populated medical areas of first- and second-tier cities, provincial capitals, or municipalities directly under the central government.It is an independent legal entity holding a Medical Institution Practice License. Such imaging centers are equipped with advanced devices, experienced professional teams, and a favorable medical environment, directly providing imaging examination and diagnostic services to end consumers, including MRI, CT, PET, X-ray, ultrasound, and mammography. Flagship imaging centers also serve as demonstration hubs for RIMAG to showcase its medical services, expert capabilities, academic research, and corporate brand.

Regional Shared Imaging Centers are primarily located in third-tier cities and below, established by relying on one or more local medical institutions.Such imaging centers integrate professional imaging resources within the relevant region by distributing imaging equipment and engaging physicians through multi-site practice or employment, thereby achieving shared access to data, equipment, and specialized personnel. Meanwhile, healthcare institutions within the region can also purchase medical imaging examination and diagnostic services from these shared imaging centers.

RIMAG has also established specialized imaging medical consortia, each composed of its imaging centers and one or more healthcare institutions.Within the medical consortium, RIMAG provides medical institutions with equipment configuration, infrastructure upgrades, and diversified medical imaging operation and management services—including professional skills enhancement, operational management consulting, and information technology construction—thereby establishing specialized medical consortium-based imaging centers.

Furthermore,RIMAG can provide diversified operational management services to medical institutions,including professional skills enhancement, operational management consulting, and information technology development, but excluding equipment configuration or infrastructure renovation,It is the operations-managed imaging centers that are expanding in this manner.

Characteristics of RIMAG’s Four Types of Imaging Centers, Source: Prospectus

From the perspectives of direct service recipients and service offerings, the four types of imaging centers are complementary. This complementarity is also evident in their performance outcomes.

According to the prospectus, by the end of 2023, RIMAG had achieved initial break-even for five flagship imaging centers, 24 regional shared imaging centers, 43 specialty medical consortium-based imaging centers, and 12 operationally managed imaging centers. Among these, the payback period for flagship imaging centers was significantly longer than that of other types, requiring 16.2 months, whereas the other three types required only 2–5 months.

During the same period, 11 regional shared imaging centers, 27 specialty medical consortium-based imaging centers, and 9 operationally managed imaging centers under RIMAG achieved positive cash-on-cash returns, while none of its flagship imaging centers did.

This once again visually demonstrates the characteristics of high investment and slow return associated with self-built third-party medical imaging centers.

However, by constructing and operating imaging centers through various models, RIMAG has resolved the challenge of prolonged profitability cycles.

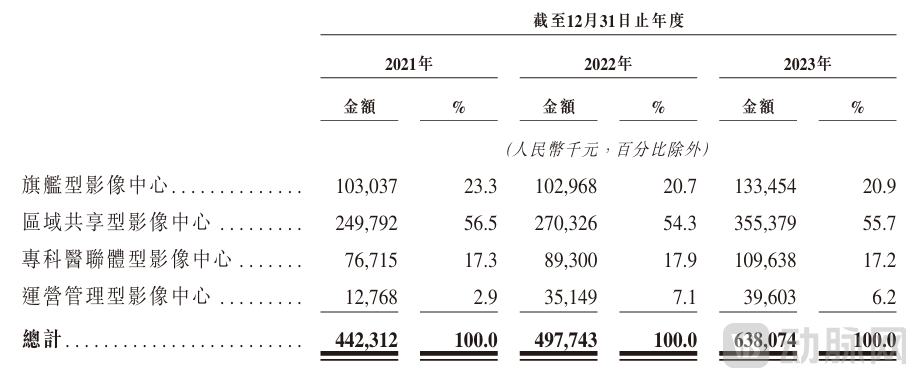

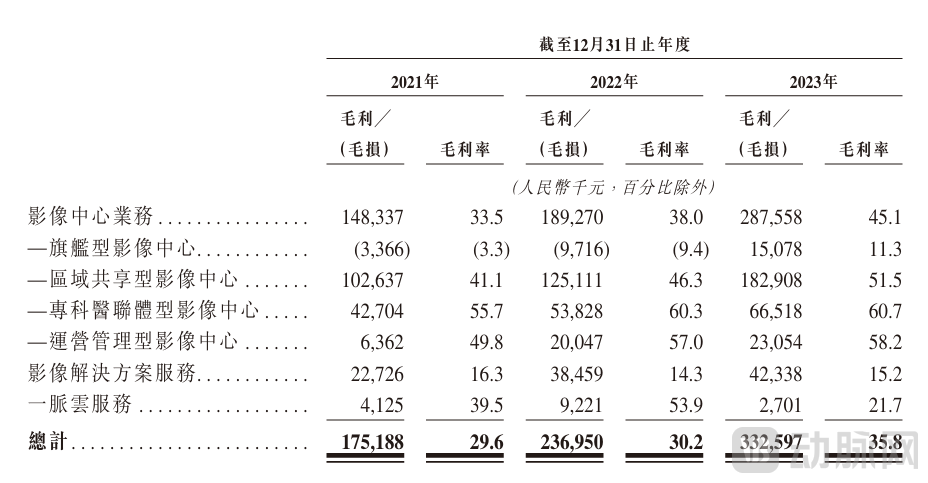

According to the prospectus data, regional shared imaging centers and flagship imaging centers accounted for the largest shares of revenue from imaging center services, representing over 50% and over 20%, respectively. In terms of gross margin, except for flagship imaging centers, which had a relatively low gross margin of only 11.3% in 2023, all other types achieved gross margins of 50%-60%.

RIMAG’s Revenue from Its Four Types of Medical Imaging Centers, Source: Prospectus

Gross Margin Profile of RIMAG’s Four Categories of Medical Imaging Centers, Source: Prospectus

In other words,Flagship imaging centers and regionally shared imaging centers are the primary drivers of revenue growth; although flagship imaging centers incur high costs and exhibit low gross margins due to their self-built model, the other three types of imaging centers offset these drawbacks, thereby ensuring more robust overall profitability.

Currently, most third-party medical imaging companies in the industry primarily focus on B2C services, directly providing medical imaging services to patients or health checkup users. RIMAG has established a B2C+B2H integrated model through four types of imaging centers, which not only forms a unique business model but also accelerates its performance growth.

In recent years, the digitalization of medical imaging has advanced rapidly. First, medical imaging infrastructure has been established within hospitals; currently, such infrastructure in tertiary hospitals is typically more comprehensive than that in primary healthcare institutions.

As the coverage of medical imaging infrastructure continues to expand, the digitalization of medical imaging will enter its second phase, characterized by data interconnectivity among healthcare institutions, enabling the sharing of medical imaging information and the dissemination of specialized expertise across hospitals.

In the process of digitalization, remote diagnosis can enhance the imaging diagnostic capabilities of medical institutions in remote areas and at the primary care level, thereby optimizing the allocation of medical resources. Digitalization also serves as the foundation for promoting mutual recognition of medical imaging examination results. Such mutual recognition can effectively improve the operational efficiency of medical institutions, promote the rational utilization of medical resources, alleviate the financial burden on patients seeking medical care, and reasonably control health insurance expenditures.

The digitization of medical imaging holds critical significance for patients, healthcare institutions, and health and medical insurance authorities alike.

To facilitate resource and capability sharing among its imaging centers, RIMAG has built the Yimai Cloud Platform, which supports the operation of chain imaging centers. While optimizing internal operations, RIMAG also commercialized the Yimai Cloud services in 2018.

RIMAG provides software products or technical services to medical institutions at all levels through RIMAG Cloud, including: the Medical Imaging Business Process Module, which covers the entire service workflow from appointment scheduling and selection of imaging examination items to the issuance of diagnostic reports. As the core product and service of RIMAG Cloud, it aims to enhance the efficiency of medical imaging workflows and address pain points for all stakeholders; and the Operations Management Module, which offers informational support and development momentum for data-driven medical imaging operations, including refined operations management and quality control modules.

Leveraging the momentum of the internet healthcare industry in previous years, RIMAG also established an internet hospital, obtaining its license in 2022. RIMAG collaborates with physical medical institutions through its internet hospital to provide remote diagnostic and multi-specialty consultation services, and plans to launch chronic disease management services for conditions such as hypertension and diabetes.

In recent years, RIMAG Cloud has contributed to RIMAG’s revenue. Although its share accounts for only about 1%–2%, RIMAG Cloud is poised to deliver significant strategic value in the future.

According to RIMAG’s prospectus, the Yimai Cloud Platform, as a key tool supporting the operational management of imaging centers and the provision of imaging solution services, is expected to become one of the company’s future revenue growth drivers.The company plans to continuously invest in R&D by strengthening its internal capabilities or collaborating with third parties.

For instance, RIMAG will continue to strengthen its data standardization capabilities, building core data competitiveness through continuous data accumulation. This will lay the foundation for subsequent workflow standardization, big data analytics and applications, and collaborations with medical imaging AI service providers. The company will also continue to invest in various application platforms, such as health management service platforms that enhance customer experience and broaden service offerings, as well as remote consultation platforms. By leveraging advanced technologies like AI and deep learning, RIMAG aims to diversify its revenue streams and business models.

Furthermore, RIMAG plans to collaborate with third parties to establish knowledge bases and knowledge graphs related to medical imaging and clinical diseases, continuously develop AI tools based on natural language processing and knowledge graphs, and expand the application of AI technologies across various stages, including patient consultations, image diagnosis, quality control, and business data analysis.

In the future, the digitization of medical imaging is also expected to evolve toward integration with AI and related technologies.

Compared with developed countries, China's third-party medical imaging service market started relatively late, has a shorter development history, and is currently still in its early stages.

According to Frost & Sullivan, the market size of China’s medical imaging services, measured by revenue, grew from RMB 147.4 billion in 2018 to RMB 270.9 billion in 2023, and is projected to reach RMB 661.5 billion by 2030. These revenues are primarily derived from medical imaging services provided by hospitals, third-party medical imaging centers, and private health examination centers.

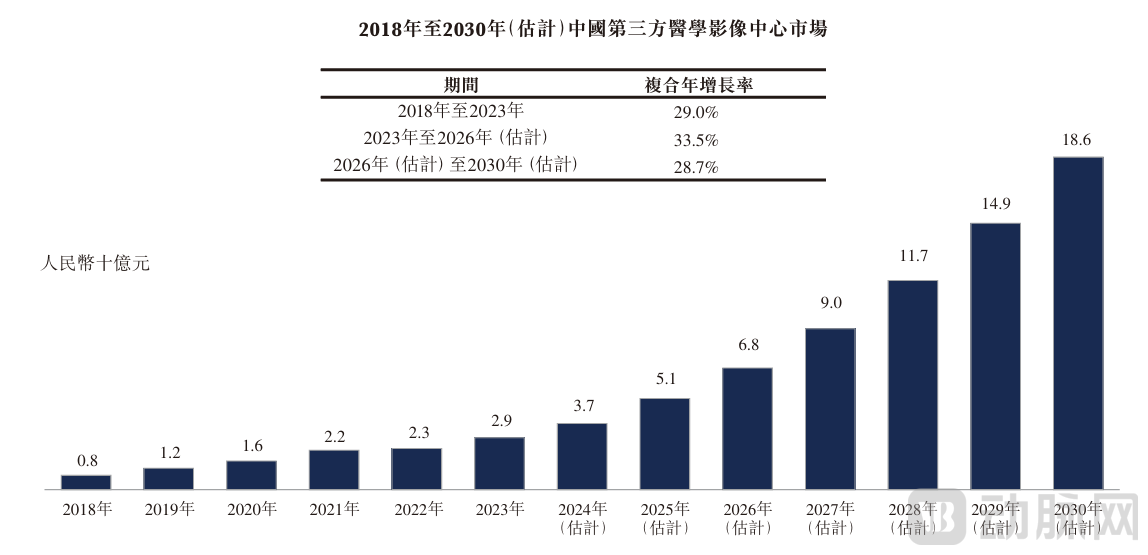

Over the past decade, third-party medical imaging services have experienced a period of rapid development. The market size of China’s third-party medical imaging centers grew from RMB 800 million in 2018 to RMB 2.9 billion in 2023, representing a compound annual growth rate (CAGR) of 29.0%. However, their share of the overall market remains relatively small, accounting for only approximately 1.1% of China’s medical imaging services market in 2023. Looking ahead, the sector demonstrates significant growth potential, with the market size projected to reach RMB 18.6 billion by 2030, reflecting a CAGR of 30.7% from 2023 to 2030.

Market Size Growth of Third-Party Medical Imaging Centers, Data Source: Frost & Sullivan

Meanwhile, as the overall market size for medical imaging services expands and resources in this sector continue to be augmented, the market size for corresponding hardware and software solutions is also poised for growth.According to Frost & Sullivan’s estimates, the market size of medical imaging equipment solutions in China is projected to reach RMB 190 billion by 2030, while the market size of cloud-based medical imaging services is expected to reach RMB 16.2 billion.

Overall, within the broader medical imaging services market, the rapid development of service providers such as public healthcare institutions and third-party medical imaging centers requires robust support from the supply of medical imaging equipment solutions and cloud-based medical imaging services. In turn, market expansion for the latter relies on the former. During the growth of the medical imaging services market, its various sub-segments also mutually reinforce one another.

However,Although each of the aforementioned market segments is experiencing rapid growth, individual markets may face inherent limitations. For third-party medical imaging service providers, adopting a diversified service model and entering different market segments can help broaden revenue streams and mitigate the risks associated with the industry’s high capital intensity through business synergies. This strategy also enables companies to consolidate their position in the rapidly expanding medical imaging services market.