Is Valuation Reduction Enough for Mid-to-Late-Stage Medical Companies to Secure Funding?

It is currently very difficult to go public, but what if the goal is merely to raise funds?

The answer is that it is not easy either. According to incomplete statistics from the VCBeat Orange Database,In Q1 2024, China's healthcare sector completed a total of 243 financing deals, representing a year-on-year decline of 44.5%.. And if we focus only on the mid-to-late stages, the data is even less impressive. It is reported that as of May 31, 2024,Among the 203 healthcare companies that completed their Series B financing in 2022, 167 remain at the Series B stage, while only 36 have progressed beyond it, accounting for less than 20% of the total.This means that a large number of healthcare companies are stuck at Series B, and a “mid-to-late-stage investment drought” is rapidly spreading across the healthcare industry.

To secure funding and survive the winter, healthcare companies have increasingly accepted lower valuations in their financing rounds, making this a new industry norm. Thus, in the past year or two, similar to“Slashing Valuation by 40% to Secure Funding” “A Series B Company’s Valuation Cut to 60%” “A Unicorn’s Valuation Slashed by RMB 20 Billion”...news reports are commonplace. For instance, a medical device company specializing in brain-computer interfaces recently announced that it had secured nearly RMB 100 million in Series B financing. A review of its response announcement reveals that the pre-money valuation for this round has dropped by nearly half compared to the previous round.

However, this approach has not always been effective. A harsh reality is that although many healthcare companies are currently lowering their valuations to seek financing, they still struggle to find buyers. In response, a senior partner told VCBeat, “If the timing is off or the company is still far from reaching key milestones, even if it proactively lowers its valuation to raise funds, there will still be very few late-stage institutions willing to step in.。”

So, what are the exact criteria for healthcare companies seeking late-stage funding today?

“Valuation” is the primary barrier to investment in the mid-to-late stages.

In fact, there are many reasons for the current “drought in mid-to-late-stage investments,” such as companies failing to reach certain milestones, or investment institutions making strategic adjustments amid the economic downturn and shifting their focus to earlier stages. Among these factors, the most critical one is the irrational valuation system in the current healthcare industry, with a severe inversion between primary and secondary market valuations.

In response, a partner at a certain institution told VCBeat, “Over the past two to three years, the valuation frameworks of many so-called hot projects have proven unsustainable. This is because institutions’ frenzied pursuit has caused some healthcare companies to distort their business practices, disregarding natural development patterns and forcing premature growth. As a result, many founders are unclear about the true value of their own companies. AndAs market enthusiasm wanes, corporate valuations become stuck in an awkward limbo—unable to rise further yet resistant to falling—making it difficult to balance the interests of earlier and later-stage investors. Consequently, it becomes increasingly hard to find a “bag holder” to take over.’。”

This is becoming an intractable vicious cycle in the healthcare sector today. In an interview, a senior investor explicitly stated to VCBeat, “For portfolio companies, the worst-case scenario we can accept is zero return, meaning that preserving the principal plus interest is sufficient.”. Although investors have already made concessions, it is not easy to truly realize them in the market.

A review of the industry reveals that, in recent years, an overly rapid pace of fundraising has, to some extent, compressed the commercialization timelines of many healthcare companies. This has resulted in a significant shortfall in market realization during later stages, with numerous firms not only failing to achieve profitability but also lacking mature product launches even by their Series B financing round. In the current climate, which places greater emphasis on cash flow, scalable revenue, and scalable product coverage, such performance is clearly not favored by capital markets.

In this regard, a partner at a well-known Shanghai-based firm remarked, “Following the tightening of IPO regulations, if healthcare companies lack robust cash flow generation or have vague timelines for commercialization and profitability, achieving an exit in the later stages becomes quite difficult. Consequently, even though some companies have lowered their valuations significantly, external institutions remain reluctant to take over. This is because if mergers and acquisitions result in substantial discounts on the final consideration, subsequent investors may struggle to recoup their principal—even through a sale of the company. After all, investment amounts range from hundreds of millions to billions of yuan, creating a significant disparity in financial interests.”

Regarding this situation, a senior partner shared her deep concerns, stating, “Given the uncertain exit channels and inflated overall valuations, if we fail to identify valuable healthcare investment targets from the pool,”"The more lavishly you invest now, the uglier the reckoning will be later."“As a result, few investors are currently pouring capital into mid-to-late-stage ventures; even limited partners (LPs) are exerting indirect pressure and exhibiting a backlash sentiment toward such projects, thereby leading to the current ‘mid-to-late-stage investment drought’ in the healthcare sector.”

Who is actually pocketing the money in the mid-to-late stages, and who are the investors?

Although times are tough for everyone at the moment, some people are quietly finding happiness. The same holds true for mid-to-late-stage investing. A seasoned investor revealed to VCBeat, “It is indeed true that investment frequency has slowed and decision-making has become more cautious; however, in reality, all institutions are still actively investing, and profitable late-stage projects remain highly sought after.。”

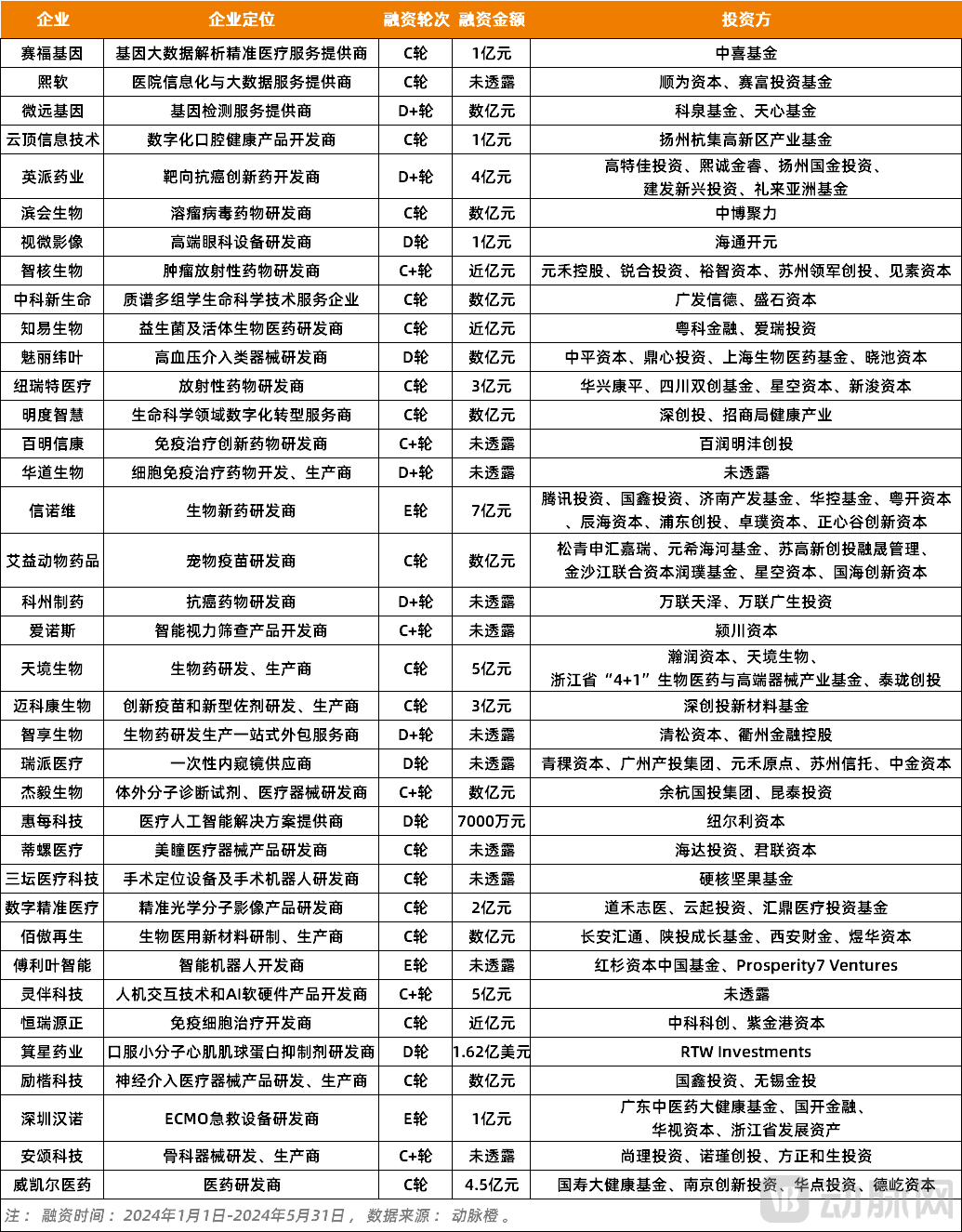

Figure 1. The 37 healthcare companies that have completed mid-to-late-stage financing this year

Figure 1. The 37 healthcare companies that have completed mid-to-late-stage financing this year

So, what kinds of medical projects can secure mid-to-late stage investments in the current climate? Let us seek answers from the 37 healthcare companies that have completed mid-to-late stage financing this year.

The first point, of course, is that “performance” must meet the target, i.e., achieve certain milestones.. As is well known, corporate financing rounds are closely tied to milestone events. A mature financing framework should be as follows: the angel round focuses on the team, Series A on the product, Series B on data, Series C on revenue, and Series D on profitability. In other words,As a company progresses into its mid-to-late stages, the capital market gradually looks beyond the founder’s halo, focusing instead on the enterprise’s concrete actions and the pace of industrial realization.。

withZhihe BiotechTake, for example, the company that recently completed a nearly RMB 100 million Series C+ financing round in mid-April, a achievement largely attributable to its significant progress in its pipeline over the past two years. In 2022, its self-developed radiopharmaceutical imaging agent, 68Ga-labeled PD-L1 (SNA002), received approval from both the U.S. Food and Drug Administration (FDA) and the Center for Drug Evaluation (CDE) of China’s National Medical Products Administration, becoming the first radionuclide imaging drug to obtain Investigational New Drug (IND) approvals in both China and the United States. This year, Zhihe Biopharma’s recombinant human thyroid-stimulating hormone injection (rhTSH, brand name Zhishujia®) was approved for marketing by the National Medical Products Administration, filling a therapeutic gap in the treatment of differentiated thyroid cancer in China. Additionally, novel targeted therapeutic radiopharmaceuticals such as SNA014 and SNA025 are currently under development.

Certainly, milestones encompass not only the product pipeline but also commercialization. As an information technology and big data service provider in the field of hospital economic operation management,Xiruan TechnologyWithin the past month and a half, the company has successfully completed two consecutive rounds of financing—Series B+ and Series C—attracting prominent investors including Sequoia Capital, Gaorong Capital, Shunwei Capital, Sherpa Capital, and Taikang. This strong investor interest is primarily driven by Xiruan’s robust market performance in recent years. According to public announcements, several of Xiruan’s products have won bids at multiple Grade-A tertiary hospitals across Guangdong, Sichuan, Guizhou, Shandong, and other provinces over the past six months, with the total bid amount exceeding RMB 15 million. The company has explicitly stated that the funds raised in these latest two rounds will be primarily allocated to product research and development as well as market promotion.

Second, companies demonstrate flexibility by proactively lowering their valuations to secure refinancing.. As previously mentioned, a typical characteristic of the current difficulties in mid-to-late stage financing is inflated corporate valuations. Compounding this issue, many healthcare companies remain unwilling to adjust their valuation expectations, choosing instead to hold firm, which makes it difficult to secure investors. In contrast, some healthcare companies are assessing the situation pragmatically; during the fundraising process, they are willing to adopt a more flexible stance by proactively lowering their valuations to facilitate financing.

In fact, this flexible and adaptable “mindset” is particularly crucial at present. Regarding this, a partner at a leading firm told VCBeat, “Over the past year or two, when arranging mid-to-late stage financing for certain projects, I would first prepare the founders,”Tell them that price reductions are necessary; do not get too hung up on valuation. Securing funding is the top priority. If you don’t raise capital now, as the winter deepens, even if you later become willing to lower your valuation to secure financing, there will be fewer and fewer investors willing to pay.。”

Therefore, investors play a crucial role in this process. In this regard, a seasoned investor stated, “Many founders are highly concerned with saving face. Often, they are actually willing to concede, but they need the investors to raise the issue first. Only after the investors do so will they go along with the flow, making their concessions in a half-hearted and veiled manner.”

The third point is that healthcare companies engage in mid-to-late-stage financing for specific purposes, such as initial public offerings (IPOs) or market promotion.This is extremely common nowadays. For instance, in preparation for an IPO, companies often introduce state-owned capital or industrial investors during the mid-to-late stages to lend credibility and support. Institutional investors are also generally willing to participate at this stage, but they carefully select projects with a high likelihood of successful listing. Beyond going public, some healthcare companies also pursue targeted mid-to-late-stage financing to support pipeline R&D or market collaborations.

So, who exactly is investing?

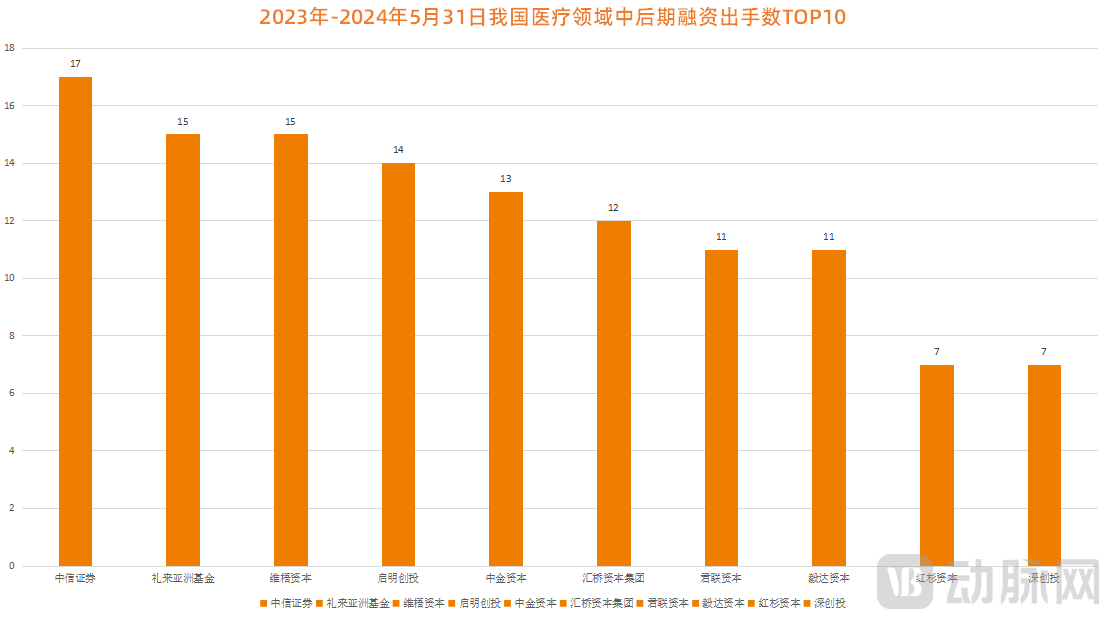

Figure 2. Top 10 Mid-to-Late Stage Financing Deals in China’s Healthcare Sector (2023–May 31, 2024)

Figure 2. Top 10 Mid-to-Late Stage Financing Deals in China’s Healthcare Sector (2023–May 31, 2024)

The largest payer is, of course, local state-owned capital. Although its proportion of investments in mid-to-late stages has declined in recent years, if we look at the current absolute values,State-owned capital remains the largest buyer in mid-to-late stage healthcare financing.. In this regard, a senior investor revealed to VCBeat, “State-owned institutions have virtually dominated the late-stage investment landscape.”. This is also borne out by the data: according to incomplete statistics from the Artery Orange database, local state-owned capital participated in 76% of the 87 late-stage financing deals completed in the healthcare sector this year.

In fact, there is an underlying industry logic at play. From the perspective of state-owned capital, under significant pressure to attract investment and businesses, investing in the mid-to-late stages serves a dual purpose: on one hand, it aims to support existing healthcare enterprises in their upward growth; on the other, it seeks to acquire more high-quality targets. For healthcare companies, bringing in state-owned capital during the mid-to-late stages not only provides endorsement and credibility but also addresses the need for capacity expansion. At this stage, the involvement of state-owned capital can precisely offer essential resources such as land and preferential tax policies.

Of course, in addition to local state-owned capital, some leading market-oriented institutions are also positioning themselves for mid-to-late-stage investments, such as Sequoia Capital, Legend Capital, Qiming Venture Partners, GTJA Healthcare, and Eli Lilly. Furthermore, certain institutions are adopting a consortium approach for mid-to-late-stage investments to mitigate risks. For instance, AiYi Animal Health, a developer of pet vaccines, completed its Series C financing with as many as six investors. This strategy not only helps alleviate funding pressures but also reduces risk to a certain extent.

The Rarer It Is, the More Rationally You Should Approach Mid-to-Late-Stage Investments

In a sense, the current “investment drought” in the mid-to-late stages of the healthcare sector is not necessarily a bad thing.

Take enterprises as an example. In the past, some healthcare companies completed two or even three rounds of financing in a single year to rapidly capture market share. While this was certainly encouraging, it also placed a significant strain on corporate resources. After all, each round of financing typically requires three to six months of dedicated effort. Completing two to three rounds in one year would mean that the company might spend the entire year focused solely on fundraising, which is inevitably detrimental to its long-term development.

The same holds true for investment firms. After aggressively increasing their investments in the early stages, they found themselves unable to exit their portfolio companies as the industry bubble burst, leaving them with nothing but a mess. In fact, many firms are currently deeply entrenched in this predicament. As a result, they are now focusing on post-investment management and have become more rational and cautious in their project selection.

Therefore,The current “investment drought in the mid-to-late stages” is, in effect, an ecological baptism for the healthcare industry., some healthcare companies that have not yet met the standards can take this opportunity to focus on refining their products or accelerating commercialization, while high-quality assets with genuine market value will be better positioned to stand out. On this point, a partner at a leading firm remarked in an internal speech, “Capital is no longer as abundant as it once was. Companies lacking vitality will gradually struggle to secure subsequent funding rounds. Meanwhile, those with strong resilience will be highly sought after and face no difficulties in raising capital.”With less irrational capital disrupting the market, high-quality companies are better positioned to achieve sustainable long-term growth.。”

Therefore, for investment institutions, after clearing out a portion of projects with uncertain commercialization prospects,As the market gradually returns to rationality, now is actually a better time to enter.. To this end, a partner at a well-known venture capital firm told VCBeat, “We will have more time to identify truly strong teams and promising directions, and to enter investments at reasonable valuations.”

Of course, for some healthcare companies,Late-stage investment is not necessarily a mandatory option at present.Just as tightening listing policies have made an IPO no longer the sole objective for healthcare companies, the same holds true for late-stage investment. Although many healthcare firms are currently engaging in extensive Series A+, B+, and C+ financing rounds to “wait out” late-stage investors, this is not a sustainable long-term strategy. Rather than bearing immense pressure and engaging in cutthroat competition within a constrained space, it is better to remain agile and adopt a “maximize exit” approach when favorable business development (BD) partnerships or acquisition opportunities arise.

In fact, this consensus is quietly being reached in the medical field.

1. “To Secure Funding, I Slashed My Valuation by 40%” — Investment Circle;

2. “How Did a ‘Series C Drought’ Emerge?” — ChinaVenture;

3. “A Series B Company’s Valuation Slashed by 40%” – Investment Circle.