A New Breakthrough Opportunity in Ophthalmology: The $100 Billion Myopia Management Blue Ocean Market Is Unfolding — Release of the '2023 China Vision Care Industry White Paper'

The ophthalmology industry is ushering in another historic opportunity—the explosion of the blue-ocean market for optometry and vision care.

On one hand, optometry is a rare segment within consumer healthcare that is easily standardized, scalable, and capitalizable, offering substantial market growth potential. Previously, senior industry investors told VCBeat that the optometry sector in the United States is relatively mature, with eight chain optometry institutions operating more than 500 clinics each. In contrast, China currently has fewer than 3,000 optometry service providers in total.

This means that new unicorn companies can also emerge in the field of optometry services, or ophthalmic giants can recreate another “Aier Eye Hospital” or “Huaxia Eye Hospital” by strategically investing in this sector.

On the other hand, investment institutions have also shown great enthusiasm for investing in optometry and vision care. In recent years, a number of firms—including Sinovation Ventures, Temasek, Jingwo Investment, BlueRun Ventures, Qingchi Capital, Ruimengxi Capital, Taikang Life Insurance, and Yaojin Capital—have made substantial investments. Companies such as Beitong Pediatric Ophthalmology, Ruishi Technology, Aikangte, and NovaSight have successfully secured financing.

Meanwhile, on the policy front, the “14th Five-Year Plan for National Eye Health (2021–2025)” was officially released in 2022, providing further policy support to the optometry and vision care industry. Coupled with rising user awareness in recent years and new breakthroughs in technology and business models by industry participants, the optometry and vision care sector is undergoing subtle yet significant changes, creating greater market opportunities and potential.

To gain insights into industry trends, VCBeat, in collaboration with Meituan Medical, released the “2023 White Paper on the Optometry and Vision Care Industry.” Through comprehensive and systematic research, this report examines the current state of the optometry and vision care sector, analyzes the development characteristics of consumers and industry participants—such as ophthalmic hospitals and optometry centers—within emerging internet-based channels, and explores the underlying transformations occurring across the industry chain. It further provides forecasts and recommendations for the industry’s future development, aiming to facilitate the continued growth of the optometry and vision care sector.

Access the full report:

Method 1: Follow the official WeChat account “Meituan Hemei Merchant Home” and reply with the keyword “Optometry White Paper” to obtain it.

Method 2: Scan the QR code to add the assistant and send a private message to obtain it.

Core Trend Insights:

Trend 1: Internet Platforms Become the Primary Channel for Business Operations and Services in Optometry Institutions

Trend 2: The genetics field is becoming a hotspot for R&D in ophthalmology, bringing more solutions to optometric services

Trend 3: AI and Other Emerging Technologies Drive New Growth in the Eye Health Screening and Monitoring Market

Trend 4: “Specialization of Talent + Universal Access to Services,” Promoting the Balanced Distribution of Optometry and Ophthalmology Medical Resources

Trend 5: From Monitoring and Prevention to Intervention, Digitalization Accelerates the Construction of a Closed-Loop Service Ecosystem in the New Optometry Industry

Trend 6: Close Collaboration Among Stakeholders to Build a New Barrier for Eye Health Prevention and Control

Industry Overview: Massive Demand Drives New Optometry Business Models, with a Blue Ocean Market Just Within Sight

Amid the worsening of eye health issues, the optometry industry is booming and evolving into new business formats through upgrading and iteration, bringing huge market opportunities.

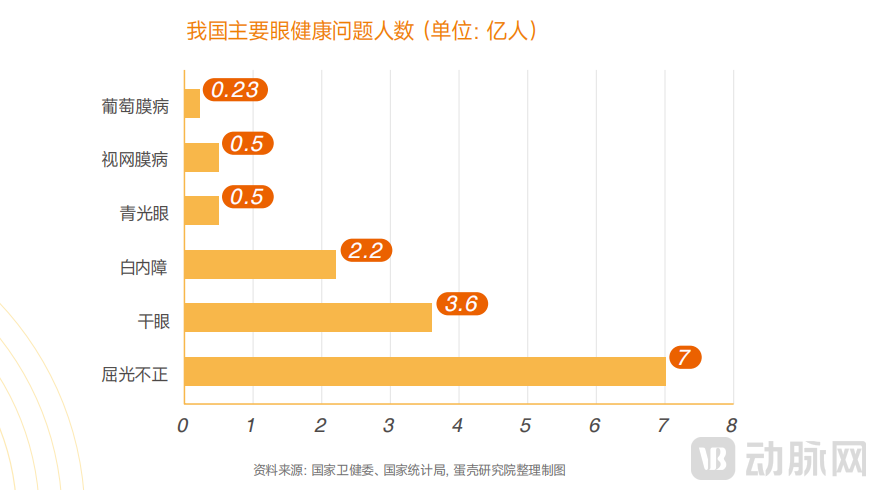

From the demand side, in recent years, China has witnessed an accelerated pace of population aging and the widespread adoption of electronic devices, leading to a high prevalence of eye health issues. Among these, 700 million people suffer from refractive errors, and approximately 360 million are affected by dry eye disease. Myopia also shows a trend toward affecting younger age groups, with the overall myopia rate among adolescents reaching 52.7% in 2020. Consequently, public demand for optometric products has grown accordingly.

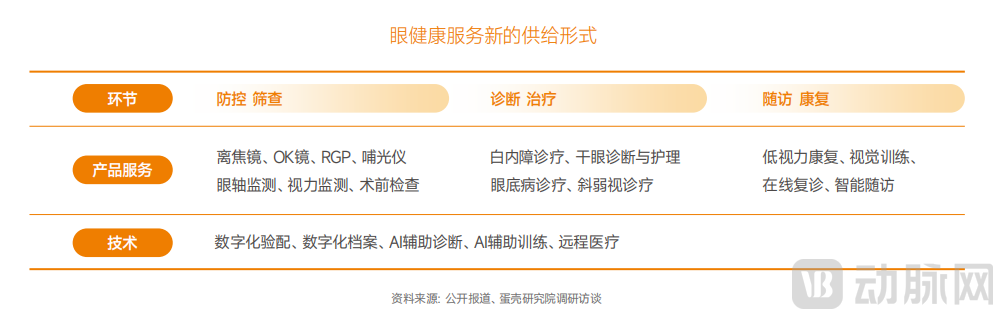

On the supply side, traditional optometric services have primarily focused on addressing refractive errors, strabismus, amblyopia, and low vision, offering services such as prescription eyeglasses and contact lens fitting. However, with growing public awareness of eye care, there is an increasing demand for professional eye health services. Driven by emerging trends—including new concepts in eye health, evolving consumer demands, and innovative service delivery models—the modern optometry industry is rising and presenting a vast blue ocean of opportunities.

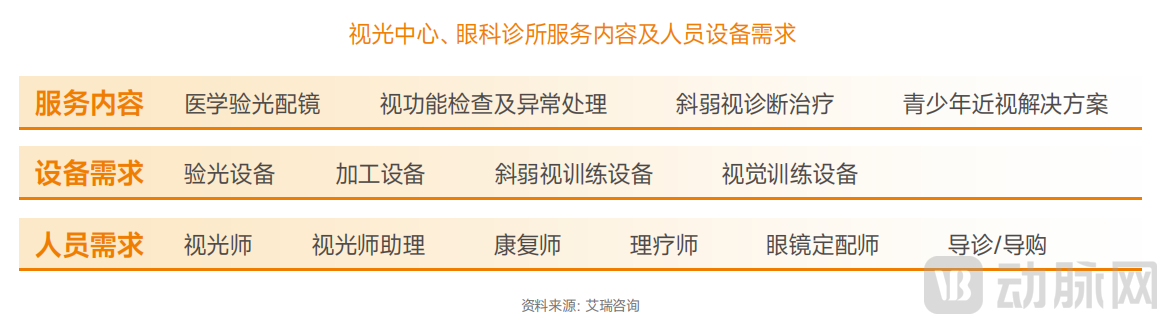

Emerging optometric services span the three major disciplines of ophthalmology, optometry, and vision science. Centered on the prevention, diagnosis, and correction of refractive errors, these services also incorporate screening and treatment for common eye diseases, while expanding into visual training and digital therapeutics. This comprehensive approach aims to improve public eye health. To better support these new services, new practice models such as ophthalmology clinics and optometry centers have emerged, characterized by broader distribution and closer proximity to patients and consumers, thereby establishing a distinct industry positioning.

Emerging Business Models: Bridging Medical and Consumer Services to Become the “Vanguard” of the Eye Health Ecosystem

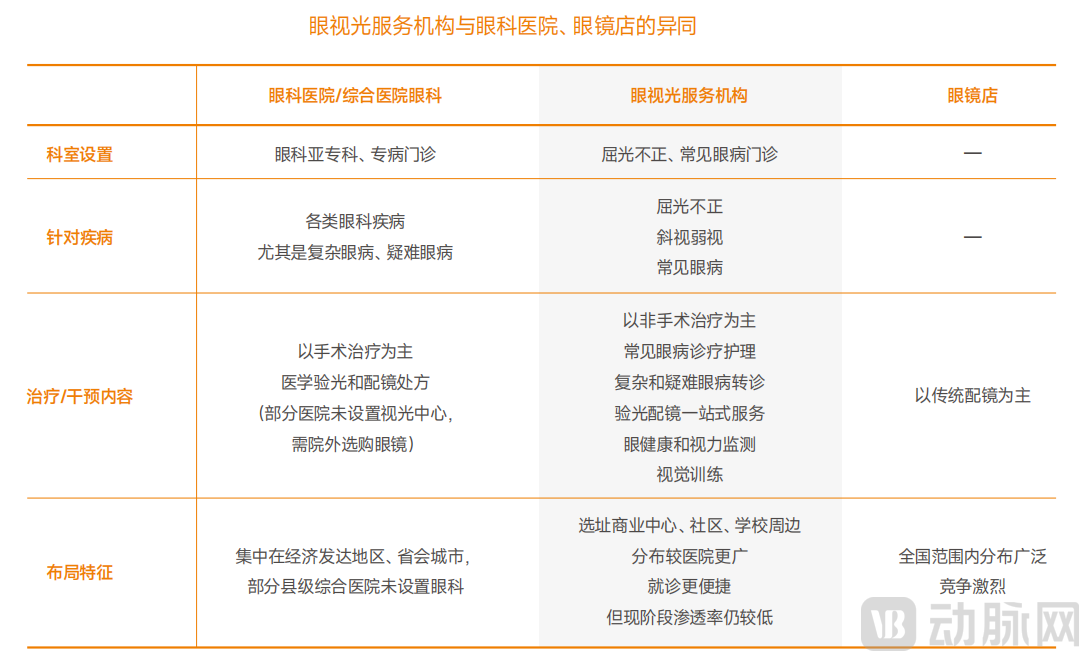

Within the ecosystem of eye health services, ophthalmic hospitals are positioned to provide comprehensive diagnosis and treatment for ocular diseases, with a particular focus on complex and challenging cases, and have established multiple subspecialty clinics or disease-specific outpatient departments. However, high-quality resources in ophthalmic hospitals are predominantly concentrated in economically developed regions and provincial capitals. Some county-level general hospitals do not have ophthalmology departments, and certain ophthalmology departments in general hospitals lack optometry centers, requiring patients to obtain eyeglass prescriptions and purchase glasses externally.

While traditional optical stores are widely distributed and offer high product accessibility, they suffer from low service professionalism, a singular profit model, and increasingly intense competition.

Therefore, optometry centers have emerged as a new business model bridging hospital-based medical services and consumer-oriented optical retail. Currently, there are more than 2,000 such optometry centers in China. As the primary units of the eye health system, these centers serve as frontline outposts responsible for eye health monitoring, basic diagnosis, referral coordination, preventive correction, and rehabilitation. They complement ophthalmic hospitals, which primarily handle complex cases and surgical interventions, and represent a key direction for the professional transformation of traditional optical shops.

However, as an emerging business model, the number of optometry and vision care institutions remains limited, and their penetration rate within the eye health ecosystem is still low, indicating substantial growth potential in the future.

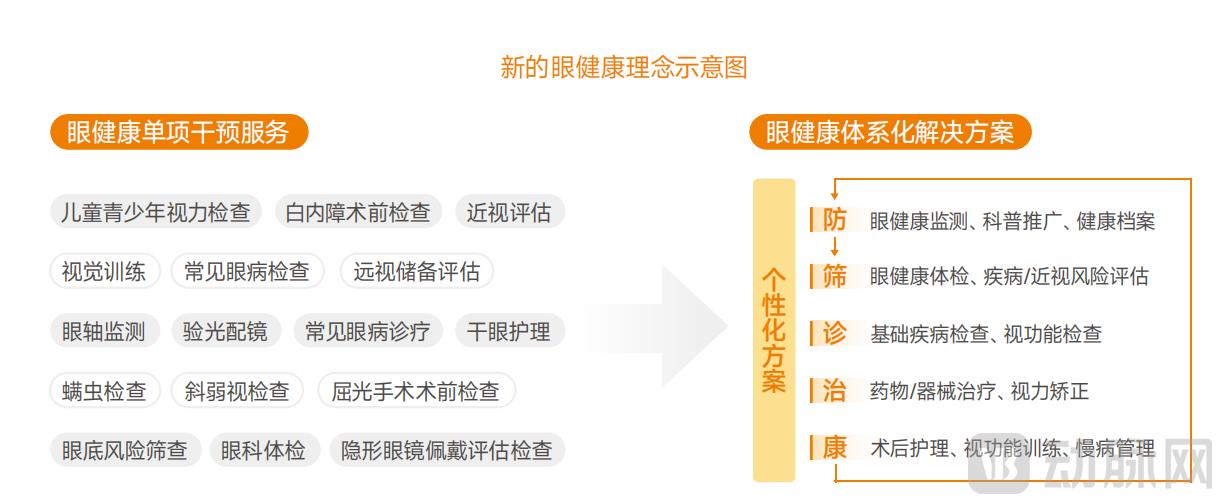

New Eye Health Concepts in Emerging Business Models: Evolution from Single Interventions to Systematic Eye Health Management Solutions

Ocular health issues rarely exist in isolation. Research indicates that patients with myopia have a higher prevalence of dry eye disease, while those with high myopia face an elevated risk of fundus diseases. Furthermore, although contact lenses can correct vision, improper use may lead to various complications, including toxic conjunctivitis, corneal epithelial damage, and infectious keratitis.

In the past, there was a relative disconnect between ophthalmic hospitals and optical retail stores, with limited collaboration among ophthalmologists, optometrists, and refractionists. Interventions for patients’ ocular health issues were mostly one-off and single-service oriented. The “Healthy China” strategy calls for a shift from a disease-centered approach to a health-centered one. In recent years, the concept of eye health has evolved accordingly, placing greater emphasis on delivering personalized and systematic solutions for patients or consumers that span prevention, screening, diagnosis, treatment, and rehabilitation, thereby forming a closed-loop system for eye health management.

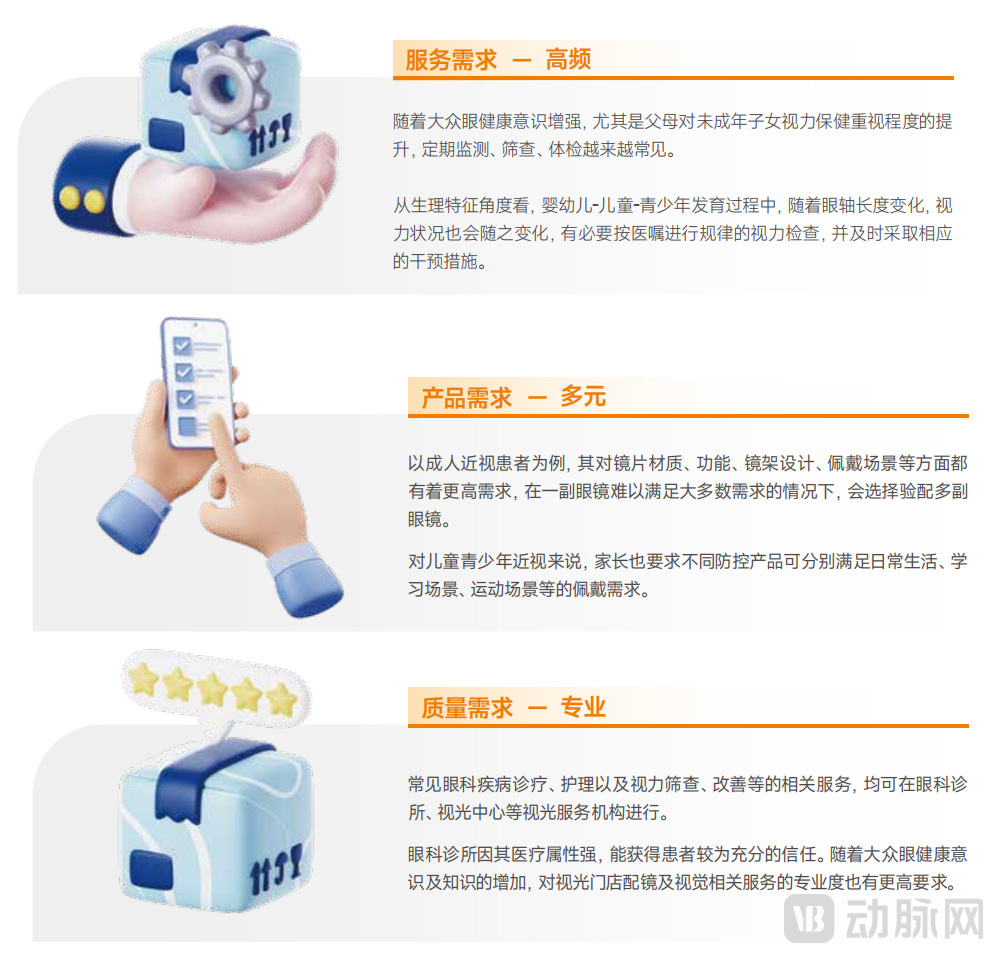

New Consumption Demands in Emerging Business Models: More Frequent Service Needs, More Diverse Product Needs, and More Professional Quality Requirements

Demand for eye health services is both inelastic and high-frequency. Data indicate that among first-time patients in optometry, 50.7% undergo regular routine examinations; 26.3% present with visual difficulties or problems; 15.3% require new glasses to improve vision; 5.1% need replacement glasses due to loss or damage; and 4.3% suffer from eye diseases, infections, or injuries. Of these, only 4.3% of patients require referral to an ophthalmology hospital, while the remainder can be adequately served by optometry centers.

In the realm of optometric products, product demand is becoming increasingly diversified alongside the growth of the vision correction market. Merely achieving visual acuity—being able to “see”—is now only the most basic expectation for patients. Today, patients and consumers have higher expectations regarding comfort, aesthetics, and functionality, requiring products that are suitable for various scenarios, complement different outfits, and even express a distinct personal style. In summary, trends in optometric consumption are characterized by “multiple pairs per person,” “eyewear as fashion accessories,” and “colored contact lenses as cosmetic makeup.”

Given that many common eye diseases are difficult to cure and myopia can only have its progression slowed, patients have an increasingly urgent need for early screening, early intervention, and long-term management. These measures are critical for controlling disease progression and achieving optimal visual outcomes, while also more effectively preventing complications and blindness. This has led patients to demand higher levels of professional service from optometric and vision care institutions.

New Supply Models in Emerging Business Formats: Frequent Launches of Myopia Control Products and Long-Term Services, Covering the Entire Spectrum of Eye Health Interventions

As the frequency of demand for eye health services increases, patients have a corresponding need for greater accessibility. Typically, visiting an ophthalmic hospital involves processes such as appointment registration, on-site queuing for examinations, and waiting for consultations. These procedures are complex and time-consuming, making flexible and convenient care models increasingly necessary. Driven by market demand, new types of optometry institutions composed of ophthalmologists, optometrists, and optometric technical support staff are rapidly emerging.

Currently, a large number of chain and franchise ophthalmic clinics or optometry institutions have emerged in China, most of which originated from the downward expansion of resources from ophthalmic hospitals, entrepreneurship by ophthalmologists, transformation of the traditional eyewear industry, and extension of businesses within the ophthalmic device supply chain.

In recent years, the eye health services sector has witnessed continuous innovation and the emergence of specialized product and service offerings. Myopia control products, such as orthokeratology (OK) lenses, defocus spectacle lenses, and red-light therapy devices, have been successively launched to market. Meanwhile, long-term care services—including axial length monitoring, dry eye management, and vision therapy—have gained increasing popularity. These novel products and services span the entire spectrum of eye health interventions and are empowered by digital technologies, enabling their efficient deployment in lightly operated service facilities. This trend has, in turn, accelerated the rapid development of new-type optometry and ophthalmology institutions.

New Business Models Unlock Major Opportunities: A Multi-Billion Yuan Optometry and Vision Care Market Is Poised to Emerge, with Private Institutions Providing Strong Momentum for the Industry

New Business Models Bring New Opportunities. Behind the fact that more than half of China’s population suffers from eye health issues lies a massive demand driving the rapid expansion of the optometry and vision care services market.

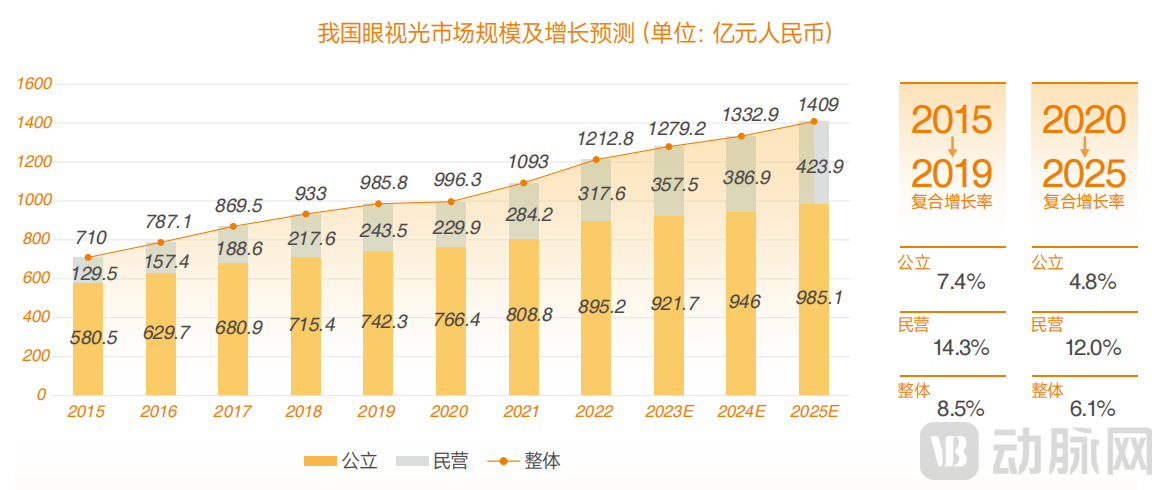

According to data from Frost & Sullivan and CIC Consulting, VCBeat estimates that the market size of China’s optometry and vision care industry grew from RMB 71 billion in 2015 to RMB 121.28 billion in 2022, with a compound annual growth rate (CAGR) of approximately 8.5%. Driven by the increasing number of patients with refractive errors and rising per-visit costs for vision correction, the market is projected to reach RMB 140.9 billion by 2025.

From the perspective of the segmented medical optometry market, private institutions will once again provide strong momentum for market growth. From 2015 to 2019, the compound annual growth rate (CAGR) of the market size for private institutions was 14.3%, and it is projected to maintain a CAGR of 12.0% from 2020 to 2025, both of which are higher than the overall growth rate.

Policy Support Boosts the Optometry Industry: Promoting Full-Lifecycle Eye Health Services, Unlocking Greater Market Potential

In recent years, a series of policies on eye health have been introduced, encouraging the further development of a high-quality and efficient eye health service system. These policies aim to provide lifelong eye health services, with particular attention to the elderly and children, who are at higher risk for ophthalmic diseases. This presents significant market opportunities in the optometry and vision care sector.

In 2018, the Ministry of Education, the National Health Commission, and six other departments jointly issued the "Implementation Plan for Comprehensive Prevention and Control of Myopia in Children and Adolescents," which set myopia prevention and control targets to be achieved by 2023: the prevalence of myopia among 6-year-old children should be controlled at around 3%, the rate among primary school students should be reduced to below 38%, that among junior high school students to below 60%, and that among senior high school students to below 70%. Subsequently, the National Health Commission released documents on service standards and technical guidelines for myopia prevention and control.

In 2022, the National Health Commission formulated the “14th Five-Year Plan” for National Eye Health (2021–2025), which proposed focusing on two key populations—children and adolescents, and the elderly—and targeting major eye conditions such as refractive errors (including myopia), cataracts, fundus diseases, glaucoma, and corneal blindness. The plan also aimed to expand the capacity of high-quality ophthalmic medical resources and extend their reach to grassroots levels. This strong policy emphasis on eye health has further strengthened eye health awareness among schools, students, and families, creating greater opportunities for optometry and vision care services.

The Industry Chain Is Becoming Increasingly Mature: Diverse and Complementary Participants in the Optometry and Vision Care Sector Jointly Deliver High-Quality Services

From the supply side, ophthalmic medical institutions provide patients with services such as disease diagnosis and treatment, surgery, and medical optometry for glasses prescription. Optical stores also offer optometry, glasses prescription, and myopia prevention and control services, while additionally providing other vision care consumer products. The two sectors have distinct service focuses and form a complementary relationship, jointly serving patients and consumers.

Within the optometry market, medical institutions primarily include ophthalmic hospitals, ophthalmology departments in general hospitals, ophthalmology clinics, and optometry centers licensed for medical practice. There is an overlap between medical institutions and optical retail stores in providing optometry and eyewear dispensing services; however, they differ in that medical institutions can perform medical optometry and fit rigid gas permeable (RGP) lenses and orthokeratology (OK) lenses, whereas optical stores are widely distributed, offer streamlined fitting processes, and provide a diverse range of eyewear products. Consequently, the optometric services provided by these two entities are complementary, better addressing patients’ needs from both medical and consumer perspectives.

Insights into Needs: Explanation of Survey Data

Survey: The data in this chapter were primarily collected through questionnaire surveys and database queries.

Objective: 1. To gain insights into the basic characteristics of optometry consumers; 2. Based on these basic characteristics, to deconstruct the current consumption preferences of optometry consumers.

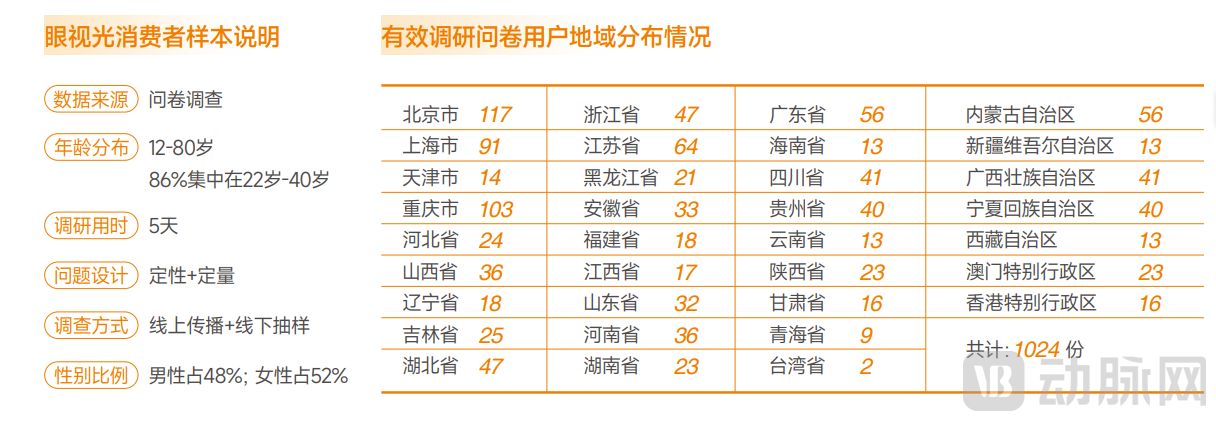

Method 1: Questionnaire Survey. To ensure the validity of the survey, VCBeat Research Institute adopted a combined approach of online dissemination and offline sampling. The survey covered 34 provincial-level administrative regions across China, targeting consumers aged 12 to 80. A total of 1,349 questionnaires were distributed, with 1,183 responses collected. After review, 1,024 valid questionnaire samples were retained.

Method 2: Sampling Survey of Meituan Platform Data. To obtain more extensive consumer spending data, VCBeat, as an independent third-party research institution, adhering to the principles of fairness and impartiality, collaborated with Meituan to draw a sample of consumers with prior online purchases of optometry and vision care products from Meituan’s database. To ensure data accuracy, we conducted our analysis after de-identifying the data.

After cleaning and analyzing two datasets, we mapped out the latest consumer profile for optometry and vision care by identifying correlations within the data.

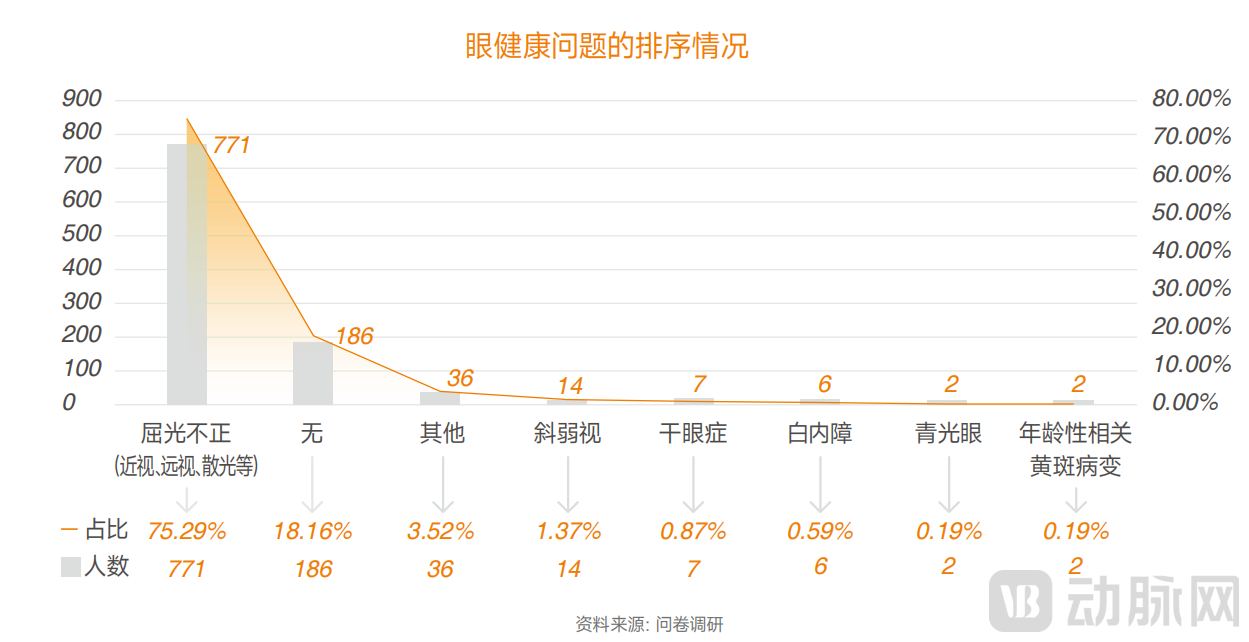

Optometry Consumer Profile 1: Refractive Errors Have Become the Biggest Eye Health Issue for Chinese People, with Over 700 Million Patients

According to this survey, among 1,024 respondents, only 186 were free from eye health issues, accounting for 18.16%. In other words, more than 80% of individuals reported eye health-related problems. Among these, refractive errors had the highest prevalence, having become the most significant eye health concern in China.

VCBeat Institute calculated, based on data from the National Health Commission and the National Bureau of Statistics, that in 2022, the number of patients with refractive errors in China exceeded 700 million, representing nearly 50% of the country’s total population.

As a type of ocular health issue, refractive error is a condition in which, when the eye is not accommodating, parallel light rays fail to form a clear image on the retina after passing through the eye’s refractive system, instead focusing either in front of or behind the retina. It includes hyperopia, myopia, and astigmatism.

From a clinical perspective, refractive errors have multiple etiologies. Genetic factors play a significant role, while improper eye use is another critical contributing factor that cannot be overlooked. Children are in a period of growth and development; poor ocular hygiene—such as incorrect posture during reading or writing, inadequate lighting, excessively short viewing distance between the eyes and reading materials, prolonged reading sessions, or reading while walking or riding in vehicles—can lead to excessive eye strain, thereby predisposing them to refractive errors.

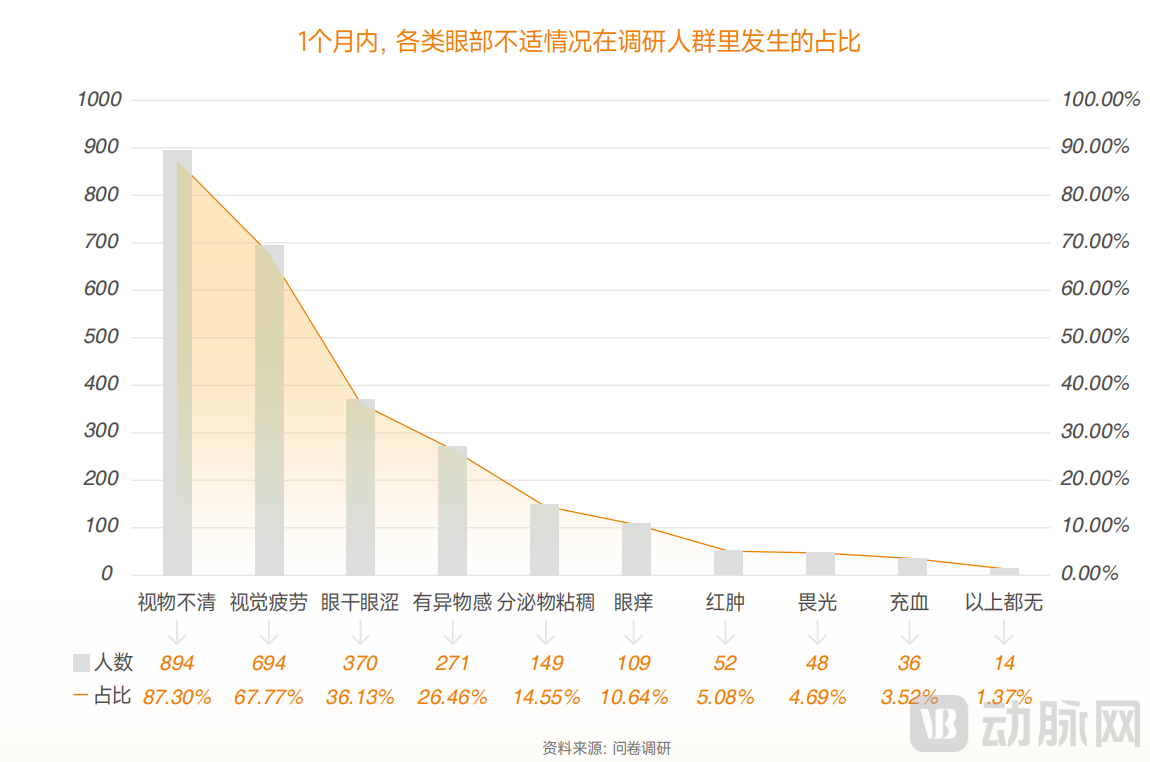

Consumer Profile of Optometry Patients 2: Frequent Eye Discomfort, with Blurred Vision and Visual Fatigue Ranking as the Top Two Issues

Among the 1,024 respondents surveyed by VCBeat Research Institute, eye discomfort was highly prevalent. In the past month, a significant proportion of participants reported symptoms such as blurred vision, visual fatigue, dry and gritty eyes, foreign body sensation, viscous discharge, ocular itching, redness and swelling, photophobia, and conjunctival injection. Blurred vision and visual fatigue ranked as the two most common symptoms, with prevalence rates of 87.3% and 67.77%, respectively, while only 1.37% of respondents reported no such symptoms.

Causes of eye discomfort include both physiological factors, such as foreign bodies like dust and sand entering the eye, and eye strain from prolonged use of computers, mobile phones, or books; as well as pathological factors, such as bacterial or viral infections, and the accumulation of necrotic cells or metabolic waste beneath the conjunctiva.

Once eye discomfort or disease occurs, 46.48% of survey respondents believe that the greatest negative impact is psychological burden, which affects both mental and physical health. Additionally, 21.39% of respondents indicated that eye diseases, particularly myopia, lead to changes in the eyeball, with the most significant negative impact being on personal appearance. Only 6.15% of respondents considered financial pressure to be the greatest negative impact.

Consumer Profile of Optometry and Vision Care #3: Nearly Half of the Population Uses Electronic Devices for More Than 6 Hours Daily

With the widespread adoption of electronic devices and mobile internet, the population using electronic devices over extended periods is growing rapidly. According to the 2022 Statistical Communiqué on National Economic and Social Development released by the National Bureau of Statistics, China’s internet users have reached 1.067 billion, among whom 1.065 billion access the internet via mobile phones. The internet penetration rate stands at 75.6%, with the rural internet penetration rate reaching a high level of 61.9%.

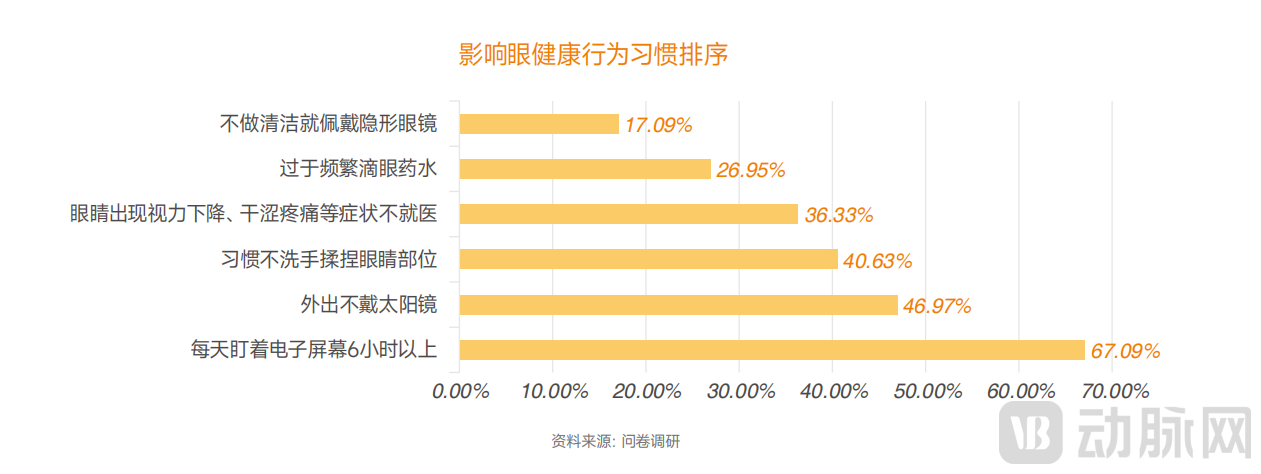

In addition to the expansion of the affected population, the duration of electronic device usage is also increasing. According to the survey data from VCBeat Research Institute, 49.51% of respondents—nearly half—reported using electronic devices (such as smartphones and tablets) for more than six hours per day.

Prolonged and high-frequency use of electronic devices places significant strain on eye health. For instance, it can impair the eye’s accommodative function and binocular vision, leading to eye fatigue. It may also result in insufficient tear secretion, causing dryness of the ocular surface and associated discomforts such as itching and pain.

Consumer Profile 4 in Optometry: Over 30% of users undergo eye health examinations and treatments due to daily life scenarios such as studying or working.

In addition to prevention, the examination and treatment of eye health are also of paramount importance.

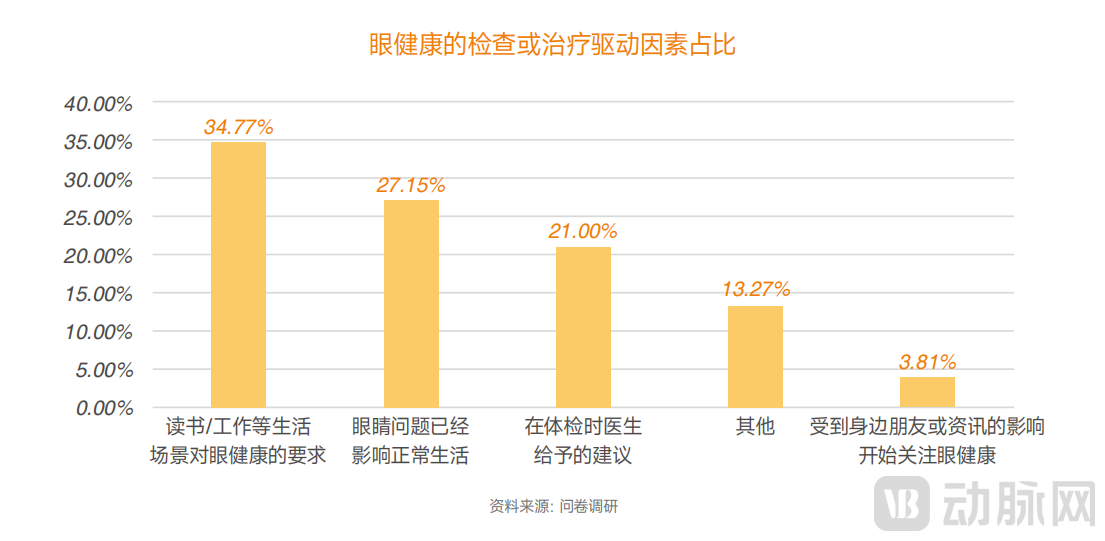

Survey data indicates that 34.77% of respondents choose to undergo eye health examinations or treatments due to the demands placed on ocular health by daily life scenarios such as reading or work. This figure exceeds the 27.15% who seek examination or treatment because eye problems have already impaired their normal daily lives, with these two groups combined accounting for over 60%. In other words, for most people, the decision to undergo eye health examinations or treatments is primarily driven by passive factors—such as findings during routine physical exams or influence from friends and media—while the proportion of individuals proactively seeking examination and treatment remains relatively low.

To protect daily eye health, survey respondents’ annual non-therapeutic expenditures (such as purchasing eye massagers, eye drops, and routine examinations) are primarily concentrated in the range of RMB 1,000–3,000, accounting for 47.75% (nearly half). The second most common spending bracket is RMB 3,000–10,000, representing 31.06%. This indicates that users are willing to invest in safeguarding their daily eye health.

Consumer Profile of Optometry Consumers 5: Approximately 30% of Users Prefer Online Channels to Learn About Eye Health Protection Methods

With the rapid advancement of information technology, the methods and channels for understanding eye health have become increasingly diverse. Currently, in addition to seeking consultations and examinations at offline institutions such as hospitals or optometry centers, individuals can also consult and obtain information through online video platforms, text-and-image resources, and internet-based medical services.

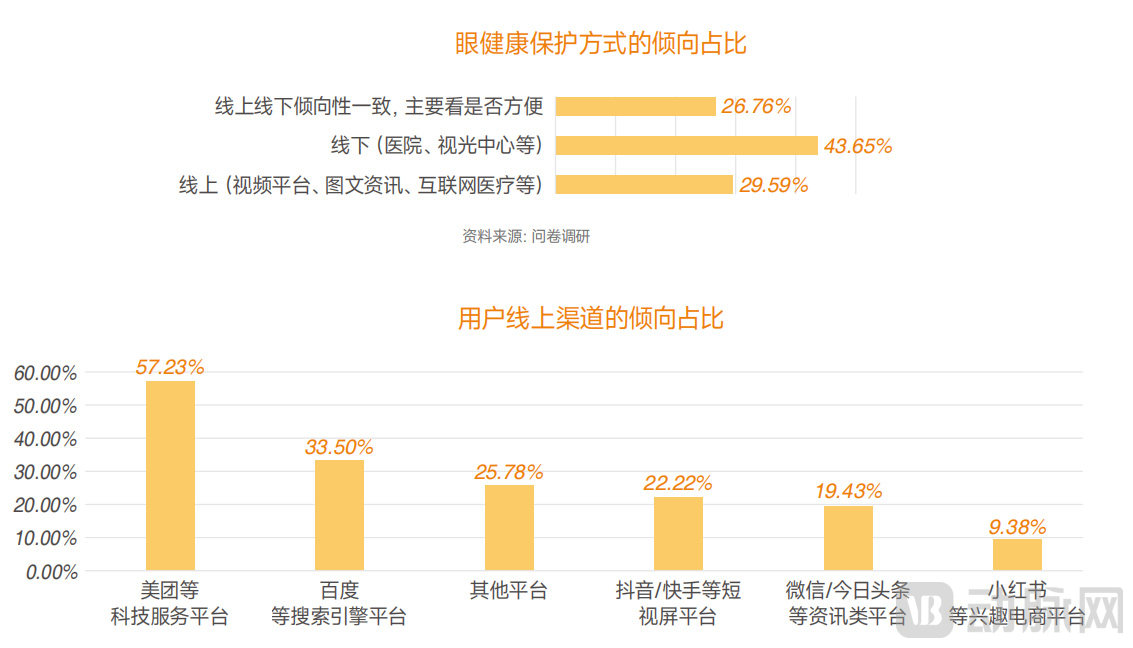

Survey data indicates that 29.59% of users prefer online channels (such as video platforms, text-and-image news, and internet healthcare services) to learn about eye health protection methods, accounting for nearly 30% of respondents. Meanwhile, 26.76% of users are open to both online and offline approaches. Combined with the proportion of online-only users, this means that nearly 60% of users are amenable to obtaining information via online channels.

Regarding the specific selection of online channels, users have a wide range of options, including tech service platforms such as Meituan, search engines like Baidu, short-video platforms such as Douyin and Kuaishou, news and information platforms like WeChat and Toutiao, and interest-based e-commerce platforms such as Xiaohongshu, among others. Notably, tech service platforms (e.g., Meituan) and search engines (e.g., Baidu) ranked as the top two choices, selected by 57.23% and 33.5% of users, respectively.

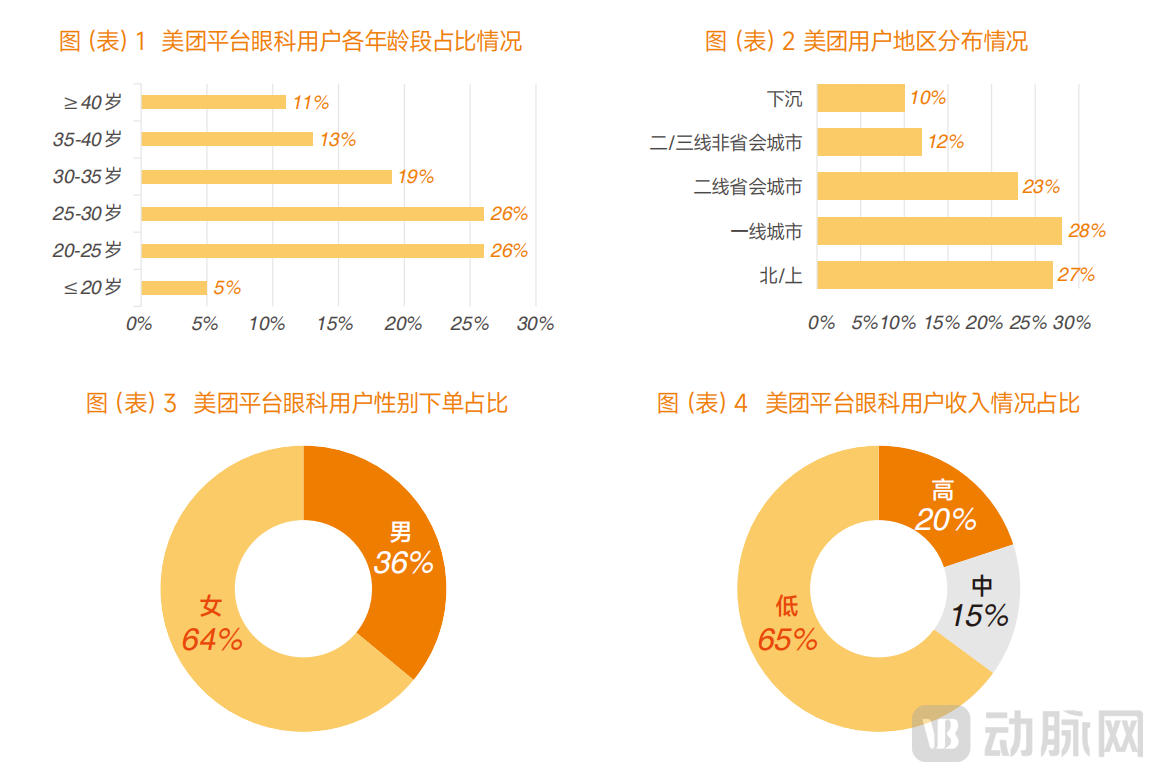

Consumer Profile of Optometry Customers 6: Ophthalmology Users on the Meituan Platform Are Primarily Young Women Aged 20–35

Online User Demographics: According to data from the Meituan platform, ophthalmology users are primarily young women residing in first- and second-tier cities who are characterized by high income, high consumption, and a pursuit of quality. The age group is concentrated between 20 and 35 years old, accounting for 71% of the user base, with a trend toward expanding into younger age groups. In terms of geographic distribution, Beijing and Shanghai account for 27% of users, with gradual expansion into second-tier cities.

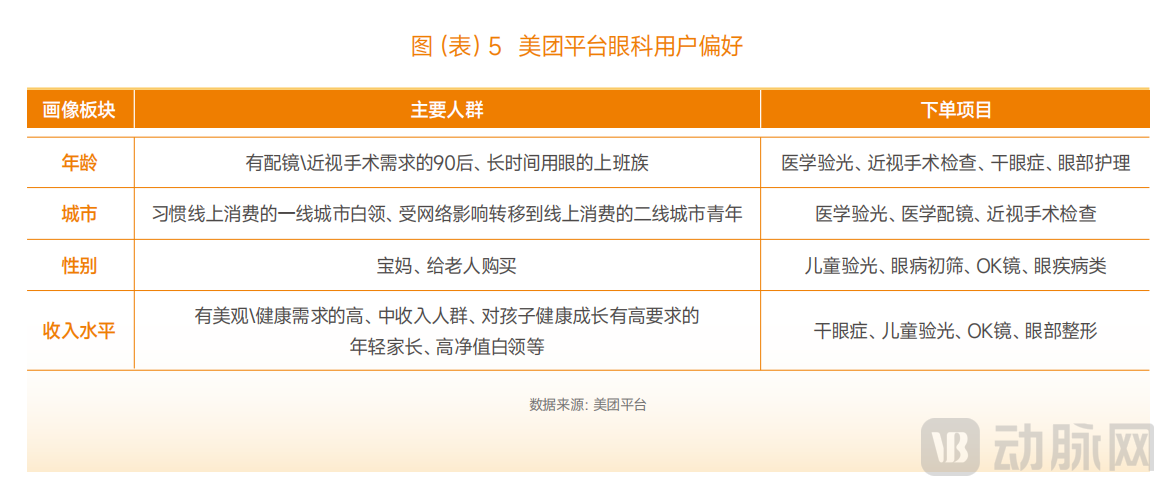

Consumer Profile of Optometry and Vision Care 7: Refraction, Eyeglass Fitting, and Myopia Surgery Are the Primary Online Demands, While Dry Eye Disease Is Seeing Rapid Growth

User Consumption Behavior Patterns: According to data from the Meituan platform, optometry, eyeglass dispensing, and myopia correction surgery are the primary online demands, with dry eye disease showing rapid growth.

Consumer Profile in Optometry 8: Brand Awareness and the Professionalism of Optometrists/Doctors Are the Two Most Valued Factors by Users

As users increasingly turn to online channels to learn about and consult on eye health knowledge and experiences, a growing number have visited optometry centers or ophthalmology hospitals prompted by introductions or advertisements on these platforms. According to the latest survey results from VCBeat, 40.82% of respondents reported having visited an optometry center or ophthalmology hospital due to such online promotions.

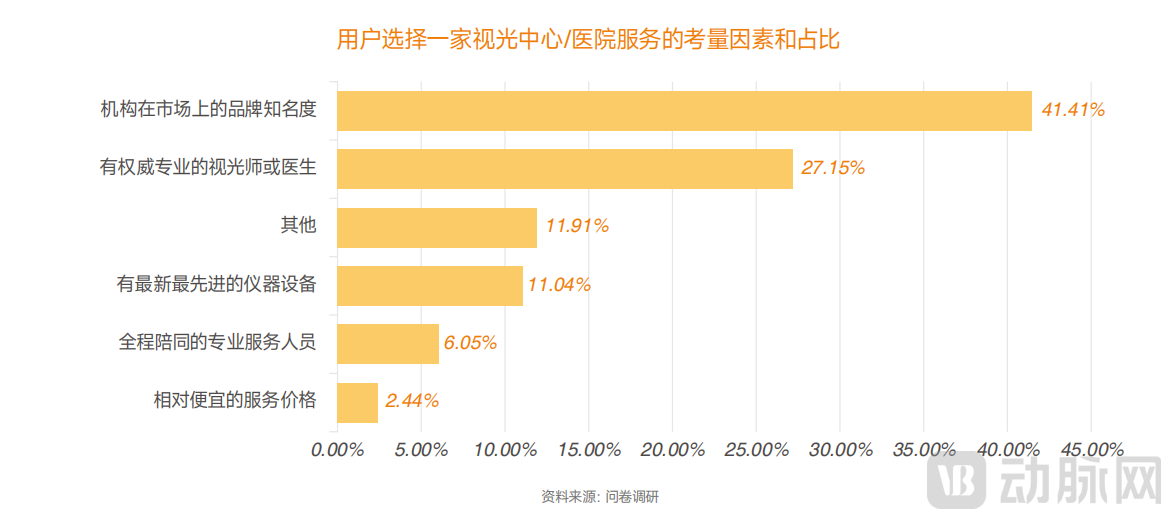

Furthermore, when selecting an optometry center or hospital, users consider a diverse range of factors. These include the institution’s brand recognition in the market, the availability of authoritative and professional optometrists or physicians, and the presence of cutting-edge equipment, as well as practical considerations such as the provision of dedicated accompanying staff throughout the service process and relatively affordable pricing.

Survey data indicate that among various considerations, brand recognition in the market and the availability of authoritative, professional optometrists or ophthalmologists are the two factors most valued by users. Therefore, eye care institutions and vision care centers should place particular emphasis on brand building, as well as the recruitment, training, and standardization of their optometrist and physician teams.

Supply-Side Status 1: Optometry Services Attract Industry Giants and Capital Influx

In the optometry sector, ophthalmic industry giants are actively expanding their presence. In mid-2023, Chen Bang, Chairman of Aier Eye Hospital Group, emphasized at the shareholders’ meeting: “We have been continuously exploring an optometry clinic model aligned with the company’s development. Currently, our model has proven highly successful and is readily scalable. We have set an initial target of 1,000 clinics, with further expansion to be determined based on future conditions.” Not only Aier Eye Hospital, but also other industry leaders such as He’s Eye Hospital and Huaxia Eye Hospital are rapidly advancing their optometry businesses. For instance, Su Qingcan, Chairman of Huaxia Eye Hospital, stated in early April 2023 that the number of chain optometry centers managed by Huaxia would reach 200 within the next five years, with a strategic focus on cities characterized by large populations, developed economies, and strong consumer spending power. Similarly, during its May 2023 earnings press conference, He’s Eye Hospital announced plans to establish approximately 30 new optometry centers.

The upstream segment of the ophthalmology industry is also intensifying its efforts in optometry services. For instance, Autek China has already established a network of more than 200 optometry outlets and plans to set up 1,300 optometry centers. iCare Medical has also extended its reach into this sector; its equity-invested affiliate, Jiongjiong Ophthalmology, has commenced operations, with key services including myopia prevention and control among adolescents, as well as medical optometry and prescription eyewear dispensing.

On the capital front, investment institutions have also demonstrated strong enthusiasm. In recent times, a host of firms—including Sinovation Ventures, Temasek, Jingwo Investment, BlueRun Ventures, Primavera Capital, Remegen Capital, Taikang Life Insurance, and Yaojin Capital—have made substantial cash investments. Consequently, companies such as Beitong Pediatric Ophthalmology, Ruishi Technology, Aikangte, and Nova-Sight have successfully secured financing.

Current Status of the Supply Side 2: Strong Demand, Optometry Services Become a Key Growth Driver for Major Listed Ophthalmic Enterprises

Eye health and eye care, as essential needs, have become the explosive growth point for the ophthalmology industry.

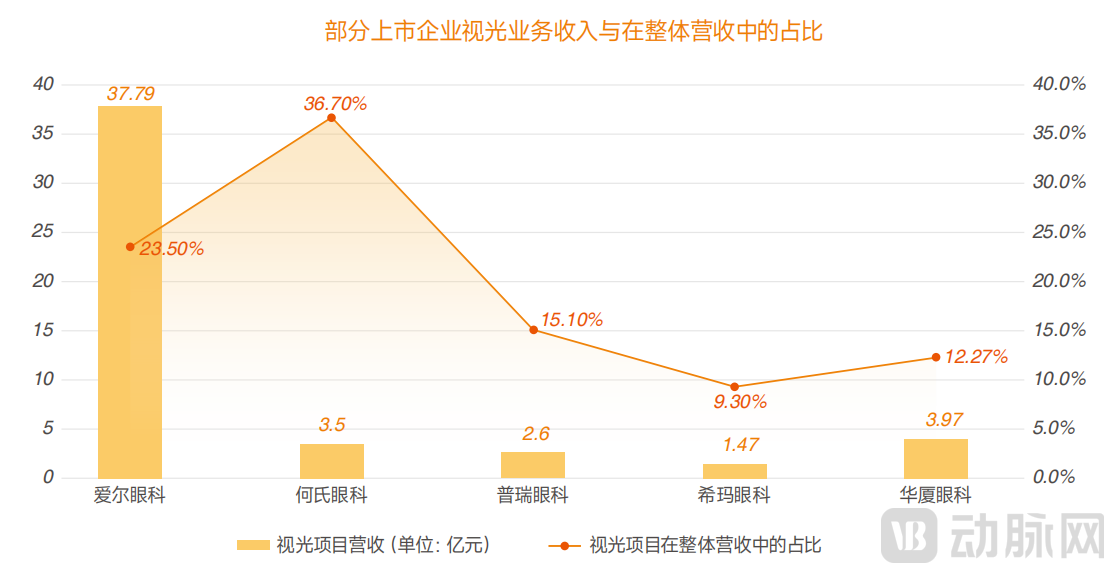

According to the annual reports of major listed companies, in 2022, optometry services accounted for 23.50%, 36.70%, 15.10%, 9.30%, and 12.27% of the revenues of Aier Eye Hospital, He Eye Specialist Hospital, Purui Eye Hospital, C-MER Eye Care, and Huaxia Eye Hospital, respectively, becoming a significant growth driver and key support for their revenue.

Ophthalmic institutions interviewed by VCBeat Institute unanimously agreed that the state’s vigorous promotion of strategies such as “myopia prevention and control” and “blindness prevention and treatment” has yielded certain results in medical science popularization. Residents’ awareness of eye health and medical consumption has improved, driving the rapid development of the optometry and ophthalmology industry.

Supply-Side Status 3: Private Eye Care Institutions Are Experiencing Rapid Growth, Becoming the Primary Recipients of Incremental Market Demand in Optometry Services

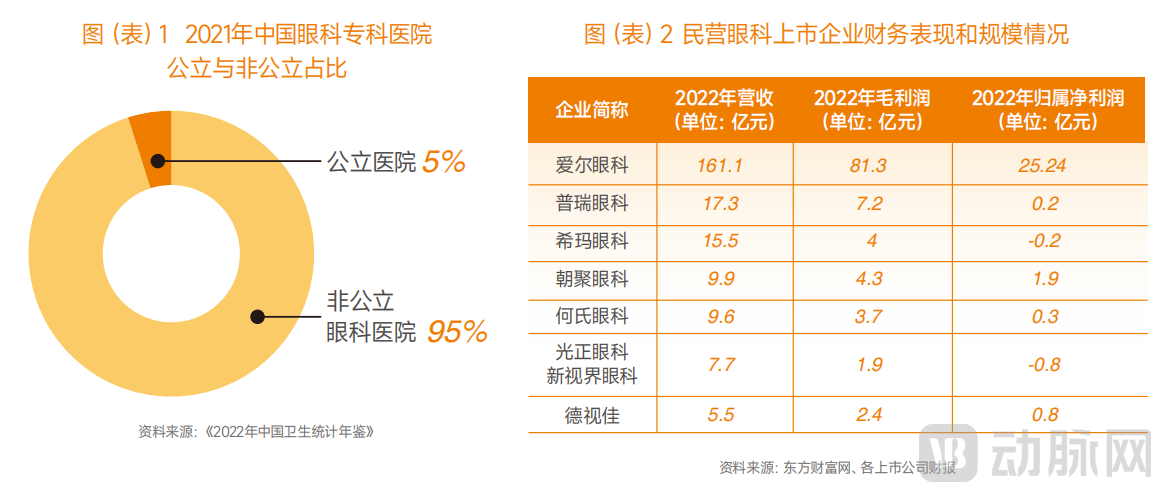

Ophthalmic care in public general hospitals is often subsumed under the Department of Otorhinolaryngology–Head and Neck Surgery (ENT), resulting in relatively low overall return on investment and institutional prioritization. Within the public system, institutions with strong comprehensive capabilities include Beijing Tongren Hospital, Zhongshan Ophthalmic Center at Sun Yat-sen University in Guangzhou, Fudan University Eye & ENT Hospital in Shanghai, and the Eye Hospital of Wenzhou Medical University. According to the China Health Statistics Yearbook 2022, there were 1,203 specialized ophthalmic hospitals in China in 2021, among which only 59 were publicly owned. The number of non-public ophthalmic hospitals was nearly 20 times higher, totaling 1,144.

Private healthcare providers have become the mainstay of optometry and ophthalmology services. In recent years, private ophthalmic brands such as Aier Eye Hospital, Taixue Eye Hospital, C-MER Eye Hospital, EuroEyes, Chaoju Eye Care, He’s Eye Hospital, Purui Eye Hospital, and Huaxia Eye Hospital have begun to achieve economies of scale, leading the supply and grassroots expansion of resources in private ophthalmic medical and eye care services.

Current Status of the Supply Side 4: Community-Based Optometry Clinics and Eye Care Centers Enter a Phase of Rapid Growth

To shorten the time patients spend seeking care for eye diseases, expand access to eye health services, and meet the substantial needs of the large myopic population for prevention, correction, and rehabilitation, community-based optometry clinics and vision care centers have emerged.

In the field of optometry, traditional optical shops and eye care institutions have rapidly expanded due to low entry barriers, asset-light models, and a strong focus on chain operations. According to incomplete statistics, there are as many as 80,000 non-medical-grade optometry institutions in the market. In recent years, in addition to pediatric clinics actively expanding their services in pediatric ophthalmology and medical optometry, new types of optometry clinics—composed of ophthalmologists, optometrists, and optometric technical support staff—are emerging rapidly.

In China, a large number of chain and franchise optometry clinics have emerged, founded by ophthalmologists, traditional eyewear retailers, and ophthalmic equipment supply chains. For instance, Doctor Glasses has partnered with hospitals and community health centers to establish multiple optometry centers; Ophkon, an ophthalmic equipment supplier, has successively invested in over one hundred optometry clinics and ophthalmology clinics across various regions; Bolin Eye Care operates more than 20 ophthalmology clinics in North China; and Xinmei Eye Care, founded by a PhD in optometry from Sun Yat-sen University, runs over ten facilities of considerable scale.

Supply-Side Status 5: The Chain Expansion of Optometry Services Is Steadily Advancing, Expanding from Regional to National Coverage

Since 2014, Aier Eye Hospital has accelerated the expansion of its hospital network, both within and outside the listed company structure, through industrial investment funds, achieving a business footprint both domestically and internationally. Later entrants in the ophthalmology sector have continuously expanded outward from their core regions, broadening their regional and national presence. Currently, Aier, Huaxia, and Purui have established nationwide layouts; He Eye Care and Chaoju Eye Care demonstrate significant regional advantages, with expansion strategies still focused on growth beyond their home provinces. Specifically, He Eye Care has deeply cultivated the Liaoning market and is gradually expanding into key urban clusters, while Chaoju Eye Care has focused on Inner Mongolia and is progressively extending its reach into North and South China.

Current Status of the Supply Side 6: The Online Transition of Optometry and Vision Care Service Institutions Is Accelerating, with Tier-2 and Tier-3 Cities Accounting for 40%

The optometry market is vast, yet competition is exceptionally fierce. The number of private ophthalmic hospitals has surpassed one thousand, while nearly 3,000 optometry institutions are vying for community-level patient traffic and intercepting offline referrals, making customer acquisition increasingly difficult for both ophthalmic and optometry providers. This situation has given rise to two major challenges: rising customer acquisition costs and low customer stickiness. In response, ophthalmic institutions have accelerated their digital transformation in recent years.

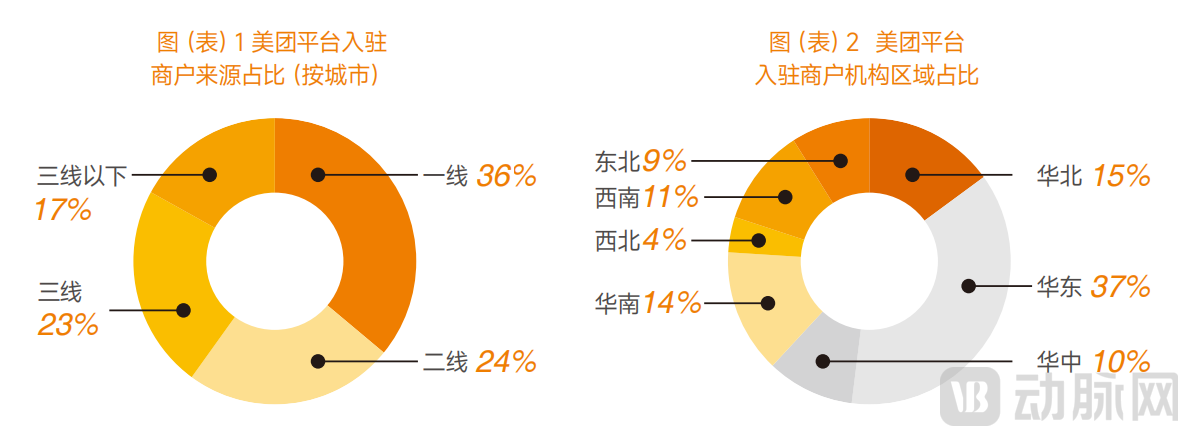

According to data from the Meituan platform, merchants in first-tier, second-tier, third-tier, and lower-tier cities account for 36%, 24%, 23%, and 17% of all merchants on Meituan, respectively. It can be seen that the proportion of merchants in third-tier and lower-tier cities has reached 40%.

In terms of regional distribution, East China has the largest number of registered merchants, accounting for 37%, while Northwest China has the fewest, at 4%. This shows a certain positive correlation with the level of economic development in each region.

Platform Service Provider Role: Serving as a Bridge to Enhance Supply-Demand Matching Efficiency

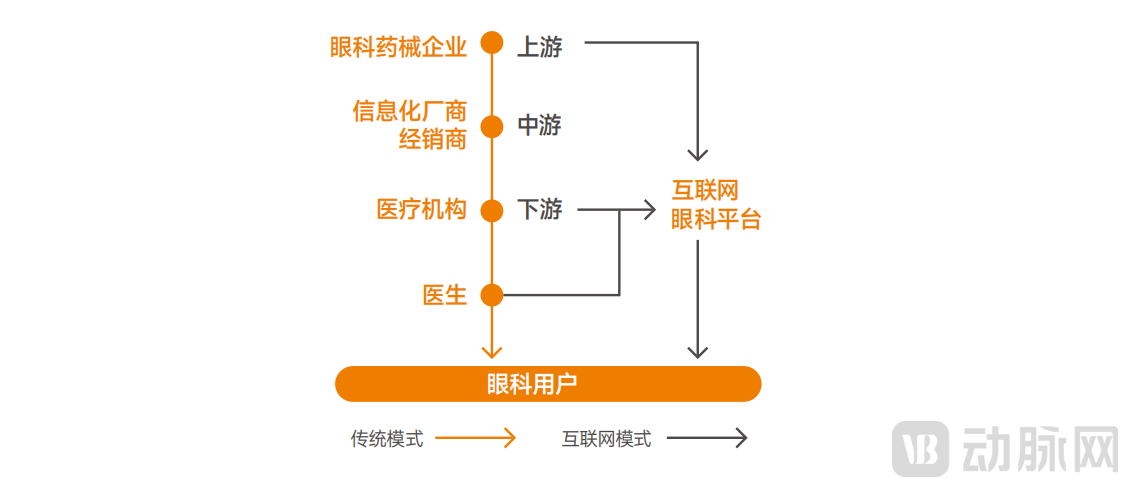

Traditional Ophthalmic Consumption Model: Healthcare institutions directly serve ophthalmic consumers by providing them with medical services.

Ophthalmology Consumer Internet Model: O2O, an abbreviation for Online To Offline, refers to the integration of offline business opportunities with the internet, enabling the internet to serve as a platform for offline transactions.

The core of the internet ophthalmology model is to use an internet ophthalmology platform as a bridge to connect medical institutions and ophthalmic patients.

B-side: Expand customer acquisition channels for offline medical institutions by disseminating their information online through price discounts, information provision, appointment services, and other means.

C-end: Provide patients with more choices and richer product information.

Role of Platform Service Providers: Facilitating the Digital Transformation of Optometry and Vision Care Consumption

Internet Ophthalmology Platform: An internet-based ecosystem that reshapes and transforms the value chains of the industry and its various stakeholders by leveraging internet technologies and ecosystems. The platform fully utilizes the internet’s role in optimizing and integrating the allocation of production factors, achieving deep integration between the internet and the optometry and ophthalmic services industry.

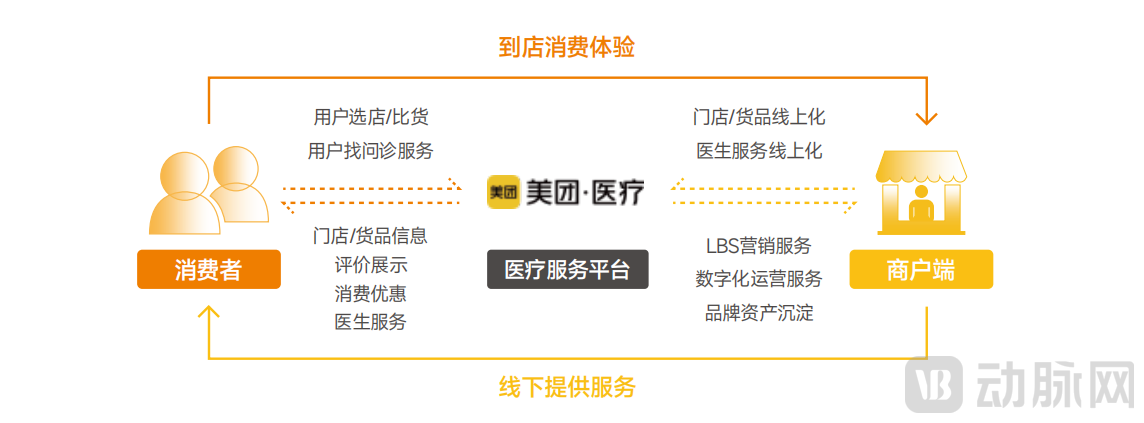

Meituan Healthcare: Building an Information and Transaction Platform for Both Supply and Demand Sides to Deliver Bilateral Value

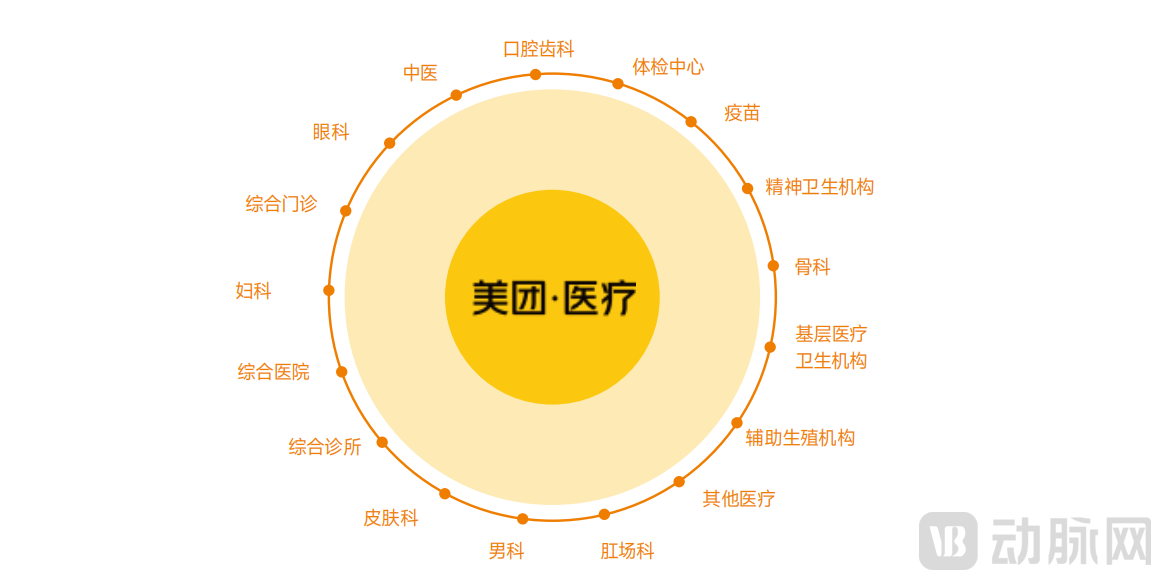

Meituan’s consumer healthcare segment was launched in 2019, providing users with information-driven decision support and service selection ranging from health screening and preventive care to the treatment of minor ailments. It covers 35 industries, including ophthalmology, physical examinations, vaccinations, and traditional Chinese medicine, as well as 106 subcategories of services such as dental fillings, orthodontics, HPV vaccination, acupuncture, and myopia correction surgery.

Meituan’s consumer healthcare business builds an information and transaction platform for consumers and local merchants, delivering dual-sided value.

Consumers: We offer a wide selection of stores and products, online physician consultation services, and diverse purchasing scenarios—including group buying, pre-orders, appointments, and team purchases—providing convenient, professional, and secure options for consumer decision-making and medical consultations.

Merchant Platform: Centered on localized consumption, Meituan provides digital services—including LBS-based precision marketing, IT solutions, and operational support—to help merchants boost sales and accumulate online brand equity, establishing itself as an essential platform for online customer acquisition and brand influence building.

Meituan Healthcare: Building a “One-Stop Aggregated Business Portal” for Merchants Based on Four Core Infrastructure Components

Healthcare Customer Operations Center: Meituan Healthcare has developed a "one-stop aggregated operations portal" that integrates store management, advertising placement, customer lead management, and business advisory services. This platform is built upon the core needs of healthcare industry clients and leverages Meituan’s four key infrastructural capabilities: operational, data, algorithmic, and marketing competencies.

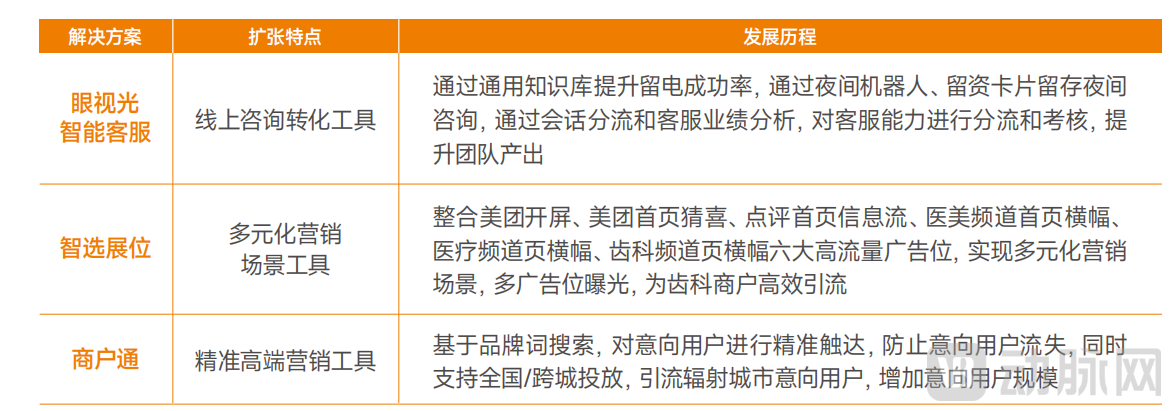

Meituan Healthcare: Six Digital Marketing Solutions to Boost Operational Efficiency for Medical Institutions

Meituan Healthcare offers a suite of digital marketing solutions—including Merchant Connect, Promotion Connect, Data Radar, Intelligent Customer Service for Optometry and Ophthalmology, Smart Select Ad Placements, and Brand Showcase—tailored to the operational needs of healthcare institutions. These solutions cover the entire lifecycle of institutional operations, empowering sustainable long-term growth.

Meituan Healthcare: Integrating Resources, Fostering Innovation, and Providing Diversified Services for Consumers, Physicians, and Merchants

Meituan Healthcare integrates high-quality industry resources and leverages its platform advantages to provide distinctive services for consumers, physicians, and merchants, building upon its robust marketing capabilities. It creates a convenient and premium service environment for users, helps physicians establish highly engaging personal brands, and empowers merchants to build influential commercial IPs.

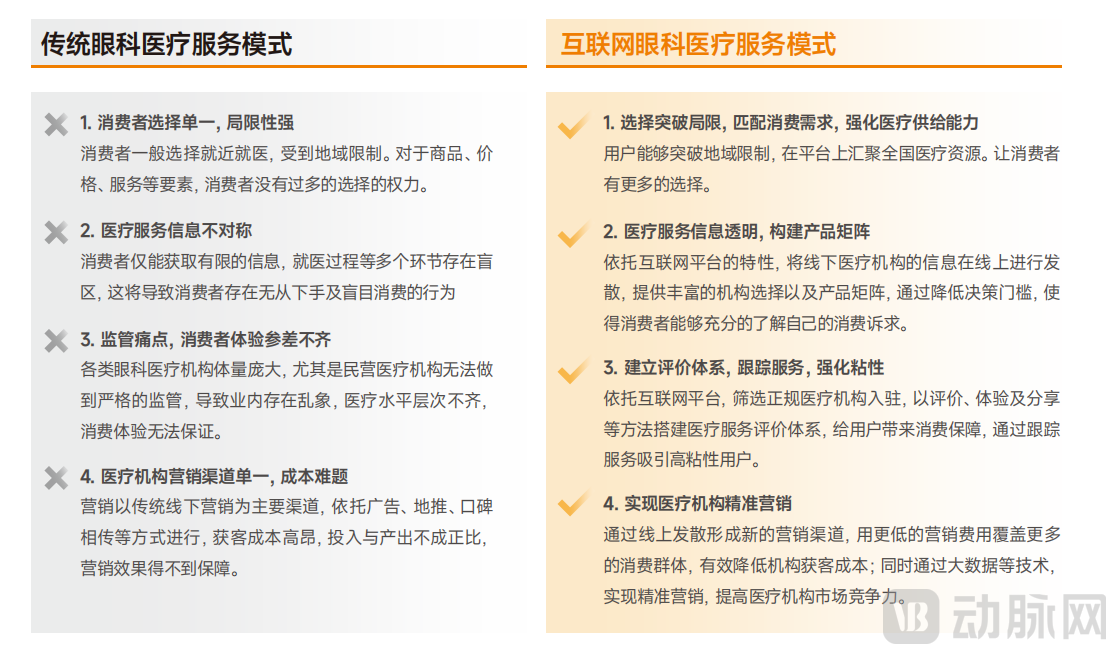

Trend 1: Internet Platforms Have Become the Primary Channel for Operation and Service Delivery in Optometry Institutions

Internet platforms have become the primary channel for marketing and promotion by ophthalmic medical institutions, with customer acquisition through online channels emerging as a key trend. This shift is driven by the fact that digitalization represents the future direction of the ophthalmology sector; the pandemic has accelerated demand for online consultations and other digital services, prompting numerous ophthalmic institutions to actively pursue digital transformation to enhance continuity of care and post-visit patient services.

Furthermore, by building big data and artificial intelligence platforms to organize and analyze the operational performance of ophthalmic medical institutions as well as patient health information, high-quality analytical insights into clinical care and operational management can be generated. This helps improve medical quality and operational efficiency, enhance the institution’s profitability and competitive advantage, and serve as a model for the future upgrading of ophthalmic medical institutions.

Trend 2: Genetics is becoming a hot spot for R&D in ophthalmology, offering more solutions for optometric services

Diseases such as high myopia, age-related macular degeneration, and diabetic retinopathy have also been found to be associated with high-risk genetic loci. Although these high-risk genetic loci do not directly cause the diseases, they increase susceptibility to them.

Research from Shantou University indicates that, under identical visual conditions, carriers of a specific gene face a 23.63-fold higher risk of developing high myopia compared to others. Consequently, genetic prediction technology is emerging as a key focus in ophthalmology. By understanding genetic factors, we can better assess disease susceptibility. The greatest promise of gene therapy lies in providing solutions for certain ocular diseases that were previously untreatable.

Now, gene therapy has opened up new therapeutic avenues, bringing new hope to these patients. According to the “Research Report on the Current Development Status and Industry Prospect Forecast of China’s Ophthalmic Gene Therapy Market” released by Market Research Network, only one ophthalmic gene therapy drug has been marketed globally to date: LUXTURNA from Spark Therapeutics, which was launched in the United States in 2017 for the indication of inherited retinal diseases (IRD). In terms of research and development progress, Lumevoq from GenSight Biologics is poised to become the second approved ophthalmic gene therapy drug worldwide.

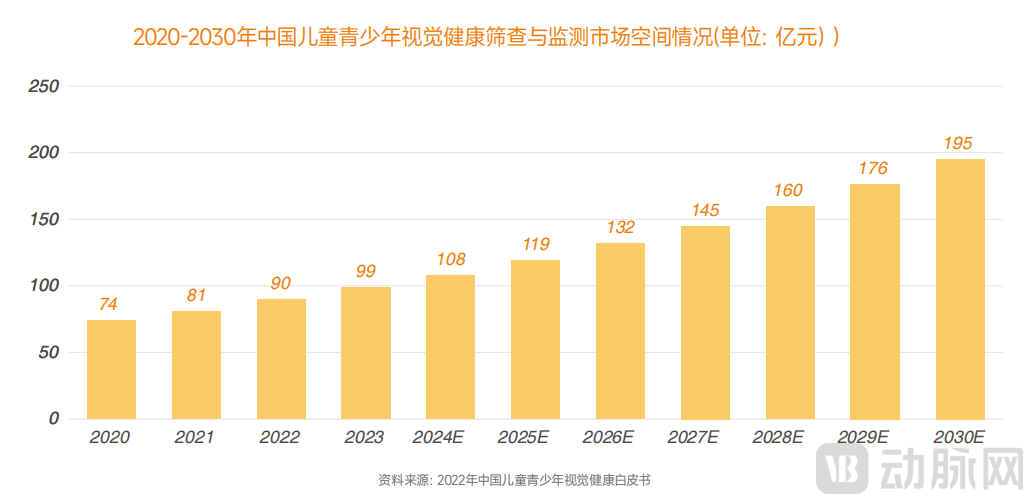

Trend 3: New Technologies Such as AI Drive New Growth in the Eye Health Screening and Monitoring Market

In recent years, against the backdrop of heightened societal attention to visual health among children and adolescents—particularly concerning persistently high myopia rates—the government has successively introduced multiple policies aimed at improving the management chain for pediatric and adolescent visual health. Currently, vision screening and monitoring, which form the foundation of myopia prevention and control in this population, are driven solely by education commissions, health commissions, schools, and public hospitals. This sector faces significant challenges, including heavy workloads, high costs, and limited resources.

The integration of emerging technologies such as artificial intelligence (AI) and big data can effectively enhance screening efficiency, reduce costs, and strengthen the analytical and predictive capabilities of visual health platforms. This facilitates the gradual normalization and personalization of vision screening and monitoring for children and adolescents, thereby improving public healthcare service capacity and supporting precise prevention and control. As the application of AI-based intelligent screening deepens and the construction of visual health big data platforms advances, the advantages of this “new infrastructure” in visual health are becoming increasingly evident, driving further market development. Driven by continuous national policy support and the ongoing refinement of novel intelligent screening and monitoring products, the market size for vision screening and monitoring among children and adolescents in China is projected to exceed RMB 10 billion by 2024.

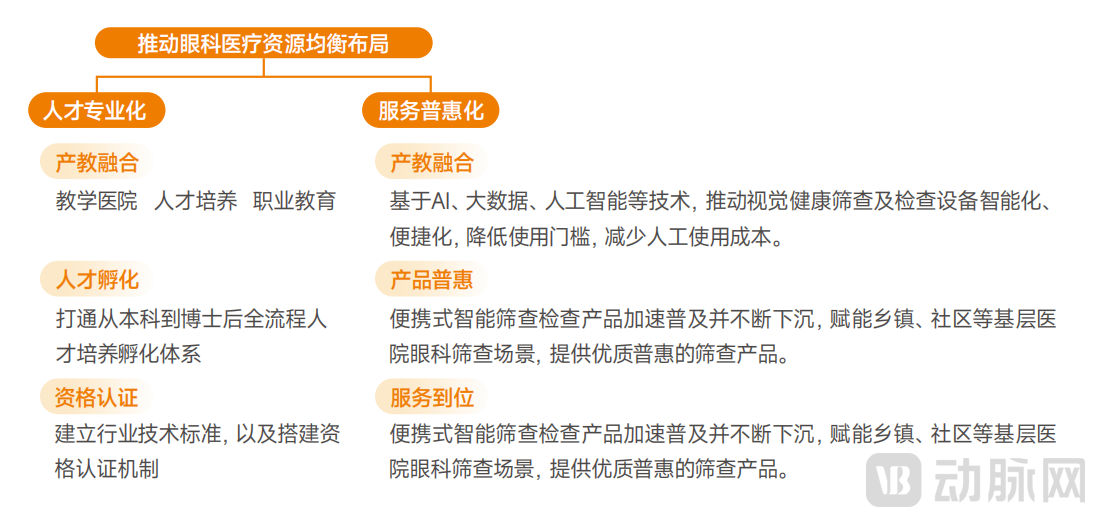

Trend 4: “Specialization of Talent + Universal Access to Services,” Promoting the Balanced Distribution of Optometry and Ophthalmology Medical Resources

Currently, China has approximately 44,800 ophthalmologists, yet there is a severe shortage of optometry professionals, with significant disparities in their professional competency. Therefore, in the future, efforts will be accelerated on one hand to train specialized optometry personnel, aligning vocational education with industry development, establishing technical standards and qualification certification mechanisms for the sector, and developing an academic education system for cultivating specialized technical talent.

On the other hand, smart products will continue to penetrate deeper into the market and become more widely adopted. By deploying affordable devices in grassroots and remote areas and leveraging technologies such as big data and artificial intelligence, operations can be simplified and screening processes intelligentized. This approach reduces employment requirements and labor costs, enabling grassroots regions to access diagnostic capabilities comparable to those of physicians at Tier 3 Grade A hospitals and providing higher-quality ophthalmic services, thereby enhancing the accessibility of ophthalmic medical resources. Meanwhile, professional equipment and data information involved in visual health screening will gradually become standardized through policy support and market development, thus driving the overall growth of the children and adolescent visual health screening market.

Trend 5: From Monitoring and Prevention to Intervention, Digitalization Accelerates the Construction of a Closed-Loop Service Model for the New Optometry Industry

Currently, the processes involved in managing visual health among children and adolescents—from monitoring to prevention and intervention—are relatively fragmented. In the future, screening and monitoring products will become more diverse, covering a wider range of scenarios. Visual health data analysis will become safer and more efficient, with integrated data interfaces enabling data sharing and real-time monitoring.

Devices for medical and non-medical institutions in the field of vision prevention and control will continue to undergo technological iterations to meet more refined examination needs. Based on examination results, personalized management plans will be developed for children and adolescents, with data tracking implemented, regular follow-ups conducted, and dynamic interventions applied to address visual health issues. Building upon optimizations across all stages, and leveraging emerging digital technologies such as AI and big data, the entire process of visual health management is expected to form a new optometric service closed loop, spanning from monitoring to intervention.

Trend 6: Close Collaboration Among Stakeholders to Build a New Barrier for Eye Health Prevention and Control

All sectors of society will further deepen their collaboration through big data platforms to achieve multi-party coordination and establish an alliance for the prevention and control of visual health in children and adolescents. Within this alliance, the government will strengthen top-level design and implement relevant measures to improve visual health screening for children and adolescents; parents, with growing awareness, will purchase various products and services for their children to comprehensively prevent and control myopia; schools, as the primary entities responsible for students’ on-campus life, will enhance outdoor physical activities and enforce high-standard controls on electronic devices during信息化 teaching; medical institutions will adopt more diverse approaches to actively participate in visual health education and promotion while enhancing their examination and service capabilities. Meanwhile, external stakeholders, such as institutions for training vision-related professionals and manufacturers of visual health products, will support the alliance’s operations through talent provision and product and service offerings.