Digital Therapeutics 'Big Three' All Exit as New Unicorn Secures Nearly $1B Funding

Virtual Therapeutics

Digital Health Service Provider

Akili

Digital Medicine Therapy Developer

Click Therapeutics

Digital Prescription Therapy Solution Provider

On May 30, virtual reality software company Virtual Therapeutics (hereinafter referred to as “Virtual”) announced that it would acquire all shares of Akili Interactive (hereinafter referred to as “Akili”) and delist to become a private company. This meansThe “Three Musketeers” of Digital Therapeutics That Went Public During the 2021–2022 Digital Health Boom Have All Exited the Stage—Prior to Akili, Pear Therapeutics (hereinafter referred to as “Pear”) and Better Therapeutics (hereinafter referred to as “Better”) had successively announced their delisting and liquidation.

If we look only at the surface, the successive exits of the “Three Musketeers” undoubtedly indicate that digital therapeutics has hit a trough. However,The end of an old era often signals the beginning of a new one. VCBeat’s analysis reveals that, almost imperceptibly, a new wave of digital therapeutics appears to be quietly taking shape.。

Prior to its acquisition, Akili was struggling.

According to the financial report, this company, which focuses primarily on ADHD (attention-deficit/hyperactivity disorder), generated only $383,000 in revenue in the first quarter of 2024, marking a further decline from the $749,000 recorded in the fourth quarter of the previous year. This level of revenue was negligible compared to its total operating expenses of $11.1 million for the same quarter, resulting in a GAAP net loss of $9.8 million for the first quarter.

Given such dismal performance, its stock price trajectory is hardly surprising. Since mid-September last year, Akili’s share price has remained stagnant after falling below $1. On the day before the acquisition news broke, its stock was trading at just $0.23. According to its financial reports, as of the end of March 2024, Akili held $63.2 million in cash and cash equivalents, sufficient to sustain operations for approximately six more months, painting a grim outlook.

Prior to this, Akili had completed two rounds of layoffs in 2023, reducing its workforce by 30% and 40% respectively, in an effort to cut costs. Meanwhile, the company also explored over-the-counter (OTC) models for digital therapeutics in 2023. In June 2023, Akili launched EndeavorOTC, a product targeting adult patients with ADHD, which can be downloaded free of charge from the Apple App Store by any adult aged 18 or older without a doctor’s prescription. Of course, a monthly subscription is still required, with prices starting at approximately $10.

Under the plan at that time, Akili aimed to submit the corresponding data to the FDA in 2024 to obtain over-the-counter (OTC) authorization for this digital therapeutic, which is primarily intended for adults. Additionally, it sought to transition its pediatric digital therapeutic from prescription-only to OTC status.

Akili has long been labeled as the first “prescription video game.” Its EndeavorRx received FDA approval in 2020 to help children aged 8–12 with ADHD. However, its actual operational performance, particularly in terms of revenue, has clearly been unsatisfactory. Akili believes that the prescription model has limited product accessibility, which is why it is launching an over-the-counter (OTC) product for adults and seeking to convert its existing pediatric product to OTC status.

The over-the-counter (OTC) model is considered capable of reducing operating expenses, improving profit margins, and making these digital therapeutics more accessible to patients in need. It is projected that this shift in business model will reduce total annual operating expenses by approximately 20%, from $55–60 million in 2023 to $42–47 million in 2024. As a result, its cash flow will be sufficient to sustain operations until the second half of 2025.

According to Akili, EndeavorOTC attracted over 4,100 active users within a quarter, with each user contributing an average of nearly $82 in revenue, generating approximately $340,000 in total income.

However, this revenue is negligible compared to Akili’s costs. To date, the FDA has not approved its over-the-counter (OTC) authorization. Current indications suggest that this initiative has not yielded particularly favorable results; in April of this year, Akili initiated a new round of layoffs, announcing a 46% reduction in its workforce. Furthermore, Akili stated that it is seeking strategic alternatives.

It was not long before the scene described at the beginning of this article unfolded—Virtual announced its acquisition of Akili. Under the agreement, the acquisition is scheduled to be completed in the third quarter of this year. Virtual will acquire all outstanding shares of Akili at a price of $0.434 per share, representing a premium of approximately 4% over Akili’s closing price of $0.418 on May 28. To this end, Virtual will pay $34 million in cash.

In stark contrast to Akili’s prominent reputation, Virtual, founded in 2015, has remained largely obscure, with no public financing announcements over the years. According to its official website, Virtual is a healthcare company that leverages virtual reality games to provide mental health solutions. The website states that Virtual’s Breakthrough solution, which includes both hardware and software components, can significantly improve the mental well-being of corporate employees.

Virtual was relatively unknown before acquiring Akili.

This solution encompasses a range of gamified digital therapeutics, with its flagship product being a gamified therapy named Bloom. According to the official website, this gamified therapy provides patients with meditation techniques to enhance focus, cultivate mindfulness, reduce stress, and improve employee performance. Over a six-week course, Bloom has been shown to increase empathy levels in participants by 48% and significantly reduce anxiety levels among patients with mild, moderate, and severe anxiety.

It is not difficult to find that,Virtual Therapeutics is a typical digital therapeutics company. Its business direction and brand tone are quite similar to those of Akili, so the acquisition of Akili would clearly serve as a significant complement to its pipeline. On the other hand, this acquisition has propelled the previously little-known Virtual Therapeutics into the media spotlight overnight.Overall, this appears to be a rather cost-effective deal for Virtual.

It is worth mentioning that,If the acquisition is ultimately completed smoothly, Virtual’s ability to produce over $30 million in cash in the current environment—despite having no prior financing disclosures—suggests that its underlying strength should not be underestimated, making it a company worthy of long-term attention.。

Prior to Akili, Better had already delisted from the Nasdaq this March. Founded in 2015, this digital therapeutics company was one of the biggest beneficiaries of the digital health boom during 2021–2022. It went public in April 2021, even earlier than Pear.

What is even more striking is that Better’s products had not yet received FDA approval at the time of their market launch. In contrast, Pear and Akili had at least secured FDA clearance for their products before launching. As a result, Better generated virtually no revenue for the majority of the period following its launch, relying entirely on cash burn to stay afloat—a predicament that speaks for itself. It was not until last July that Better’s AspyreRx, indicated for type 2 diabetes, received FDA approval via the De Novo pathway. By then, nearly two years had passed since its initial market launch.

Prior to its delisting, Better had already undergone multiple rounds of layoffs and restructuring. Even the management team personally invested in subscribing to shares in an attempt to extend the company’s lifespan, but it never lived to see “better” days. Just over six months after securing its first medical device registration certificate, Better was forced to cease operations and delist.

Nevertheless, Better’s product portfolio remains quite attractive. In addition to AspyreRx for type 2 diabetes, Better’s pipeline includes BT-002 for high cholesterol, BT-003 for hypertension, and BT-004 for metabolic dysfunction-associated steatohepatitis (MASH).

For this very reason, immediately after Better delisted and ceased operations, a well-established digital therapeutics company swiftly acquired the aforementioned Better product pipeline. This veteran enterprise is Click Therapeutics (hereinafter referred to as “Click”), which was founded in 2012.In the field of digital therapeutics, Click is a well-established veteran. In fact, the term “digital therapeutics” was first coined by Click in 2012.。

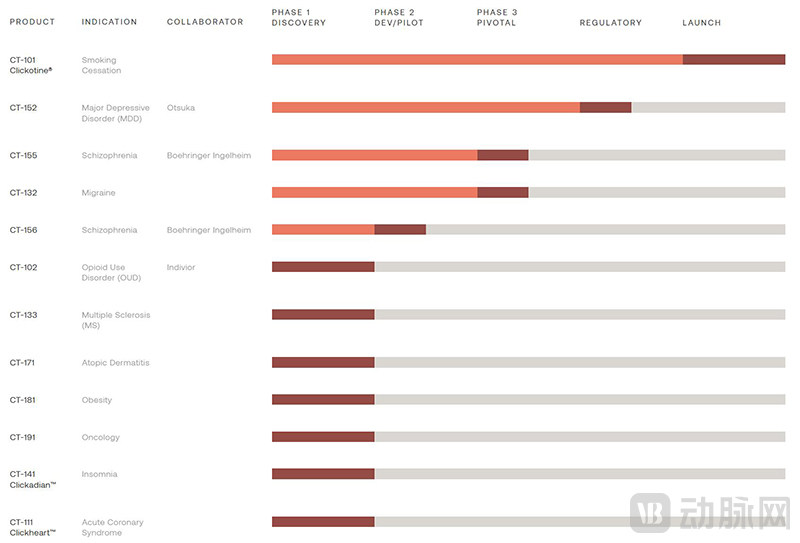

In terms of its product pipeline, Click initially focused on its digital therapeutic for smoking cessation, Clickotine, and has since expanded into a robust pipeline encompassing products for major depressive disorder, schizophrenia, migraine, opioid use disorder, multiple sclerosis, and other conditions.

As the wave of digital health IPOs swept in, Click’s spotlight was gradually eclipsed by these newly public companies. Nevertheless, Click has been quietly advancing its product R&D and commercialization. In particularClick has extensive experience in collaborating with pharmaceutical companies, maintaining partnership agreements with Otsuka Pharmaceutical, Boehringer Ingelheim, and Indivior.。

This March, Rejoyn, a digital therapeutic developed by Click Therapeutics and Otsuka Pharmaceutical over five years of collaboration, finally received FDA approval, becoming the first approved digital therapeutic for major depressive disorder in adults, to be used in conjunction with antidepressant medications.. As early as early 2019, Otsuka Pharmaceutical committed to fully funding the development of Rejoyn, with total commitments of up to $305 million, including $272 million in commercial milestone payments.

To facilitate the successful commercialization of its products, Otsuka Pharmaceutical has even established a new company called Otsuka Precision Health. This subsidiary will focus on data and technology to commercialize digital therapeutics and connected health products, ensuring that patients can easily access and afford them—a step that previous digital therapeutics companies have often failed to achieve. Rejoyn will be its first product to be launched.

Not only that,CT-155, a treatment for schizophrenia developed by Click Therapeutics in collaboration with Boehringer Ingelheim, has also initiated pivotal clinical trials and received FDA Breakthrough Device Designation in January this year.。

In recent years, Click has also expanded into the fields of obesity, diabetes, and cardiometabolic diseases, launching a prescription digital therapeutic candidate pipeline for obesity named CT-181. The acquisition of Better’s product portfolio will help Click advance its pipeline in obesity, diabetes, and cardiometabolic diseases, enabling it to capitalize on the upcoming wave of GLP-1 medications through dose calculation, side effect management, and behavioral therapy.

Click Therapeutics currently has a robust product pipeline.

According to Click’s official statement, it will not directly implement the existing AspyreRx; instead, it will first make adjustments to optimize its performance on Click’s artificial intelligence platform and enable integration with CT-181.

This is not the first time Click has made a move.As early as a year ago, when Pear filed for bankruptcy, Click stepped in to acquire the relevant patents of the Pear platform.. Meanwhile, in an environment rife with layoffs, Click continues to expand its team, a rarity indeed. Quietly, Click has built up a robust product pipeline, emerging as one of the most dynamic companies in the current digital therapeutics landscape.

In fact, it is not difficult to discover with a little attention,Although the operations of several publicly listed digital therapeutics companies have not been successful, their product pipelines clearly hold significant value, as evidenced by their acquisition by other enterprises within a short period. This also demonstrates that digital therapeutics are far from being without merit.。

As a software-based medical device, digital therapeutics offer stable output (more consistent than human-delivered interventions), lower costs (with zero marginal cost), and more convenient real-world data collection (as product usage inherently generates feedback data). These represent unique value propositions of digital therapeutics and constitute aspects that cannot be replaced by pharmaceuticals or traditional medical devices.

In addition to acquisitions, digital therapeutics, which have long been dormant in the primary market, are also seeing positive developments.In early June, Sword Health, a digital therapeutics company specializing in musculoskeletal rehabilitation, announced the completion of approximately $130 million in financing—a sum that would be considered “mega-round” territory even during the digital health boom of previous years.This has also brought Sword Health’s total funding to $340 million, with the company’s valuation reaching $3 billion. According to reports, its revenue has nearly tripled over the past year, and it is seriously considering an initial public offering (IPO).Unintentionally, a new unicorn is also emerging.。

As the new waves of the Yangtze River push forward the old, so do newcomers replace veterans in the ever-changing world. Over the past year or two, leading digital therapeutics companies—including Pear, Better, and Akili—have collapsed one after another, sending shockwaves through the industry. However, viewed over a longer timeframe, this is merely a brief interlude in the course of history. New enterprises are rapidly emerging, though whether they will grow into unicorns remains to be seen. VCBeat will continue to closely monitor industry developments and provide you with first-hand insights.