Solving the Challenges of Non-Standard Health Insurance through Strategy Design, Business Coaching, and Centralized Operations

“Approximately 88% of insured individuals with non-standard health profiles plan to purchase additional insurance within the next year. The number of such policyholders may double in the coming year.” Recently, the *Research Report on Insurance Innovation for Individuals with Pre-existing Conditions*, jointly released by *China Banking and Insurance News* and the Center for Insurance and Economic Development Research at the Chinese Academy of Social Sciences, revealed the strong willingness of non-standard risk populations to purchase insurance.

However, compared with the traditional “one-size-fits-all” health insurance products, non-standard risk health insurance faces obvious challenges across various aspects, including pricing, risk control, marketing, and medical health services. Encouragingly, the industry is collaboratively addressing the operational difficulties of non-standard risk health insurance through model innovation.

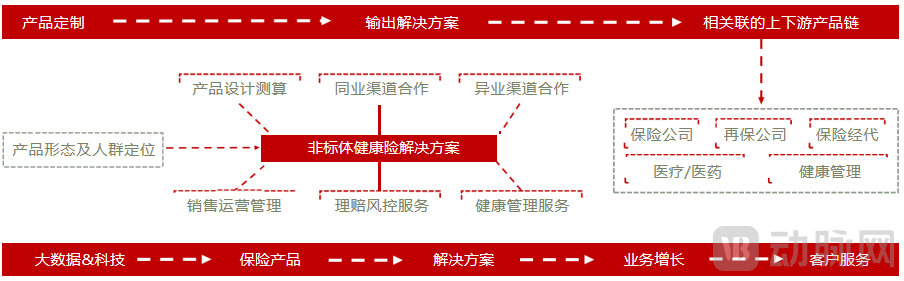

Taking Shanghai Weijia Insurance Brokerage Co., Ltd. (hereinafter referred to as “Weijia Brokerage”), a subsidiary of Winning Health Technology Group, as an example, it launched a health insurance solution for non-standard risks in 2023. Leveraging its proprietary insurance brokerage sub-brand “Xiaoweibao” platform, along with the parent company’s industry accumulation and expertise in medical insurance and commercial health insurance, Weijia Brokerage has established a unique model featuring “strategic design + business accompaniment + intensive operations.” This model is employed to serve numerous B-side partners within the health insurance industrial ecosystem, creating a “showcase model” for non-standard risk insurance and further accelerating the development of the non-standard risk insurance market.

“Xiaoweibao” Core Services for Non-Standard Risk Health Insurance Solutions

In recent years, the homogenization of health insurance products has intensified, competition has become increasingly fierce, penetration rates among healthy populations have reached relatively high levels, and premium growth has slowed. Against this backdrop, expanding into non-standard risk health insurance has become a consensus for the next stage of development in the health insurance sector and represents an inevitable trend in the industry’s evolution.

In the blue-ocean market, insurers are vying to establish their presence. Given the operational complexities of non-standard health insurance, forward-looking strategic planning should be undertaken in product design and marketing, taking into account macro policies, market landscape, and policyholder needs.

Since 2015, million-yuan medical insurance products offered by various insurers have emerged in large numbers. With coverage limits reaching millions of yuan for premiums of only a few hundred yuan, coupled with the convenient purchasing channels provided by the internet, these products have experienced robust growth. However, challenges have arisen: significant product homogenization has intensified competition. To date, raising the maximum underwriting age, lowering deductibles, or even offering zero-deductible plans have become common tactics in the fierce “involution” of the million-yuan medical insurance market. Even so, as the pool of applicants meeting health requirements shrinks, the growth rate of million-yuan medical insurance, along with the overall health insurance market, has slowed. Therefore, providers of non-standard risk health insurance products should learn from these precedents and engage in proactive product strategy planning.

Leveraging its parent company’s years of experience serving diverse stakeholders within China’s multi-tiered healthcare security system, Weijia Insurance Brokers has accumulated profound market insights. These include the positioning of commercial health insurance, the gap between existing product offerings and market demand, and the urgency and key requirements for non-standard risk insurance among populations with different medical conditions.

Thus, Weijia Brokerage uses its sub-brand “Xiaoweibao” as the entry point for collaboration, assisting partner insurance companies in strategic design. By integrating the insurers’ existing resources, market demand, and supply gaps, it formulates differentiated product strategies for non-standard risk health insurance, enabling rapid market capture while minimizing the long-term risk of “involution.”

For example, in response to demographic and fertility policy trends, “Xiaoweibao” has partnered with Sunshine Property & Casualty Insurance to co-develop a customized “IVF” insurance product that addresses the high costs and low success rates associated with assisted reproductive technologies, thereby providing tangible coverage for customers.

Furthermore, “Xiaoweibao” integrates the physiological, psychological, and disease-specific characteristics of women, targeting females aged 20 to 45 who possess health protection awareness and needs as its core audience, and designating this segment as a key direction for future expansion.

In the current health insurance market, non-standard risk insurance has expanded to cover a wide range of diseases and populations, including specific disease insurance products for diabetes, breast cancer, and pediatric leukemia. Beyond disease categories, individuals with non-standard health risks can be further segmented by severity of health risk, age, gender, and other factors, with additional granularity achieved through cross-dimensional analysis. For insurers, this segment offers a broad target audience and significant room for product differentiation. The key lies in leveraging third-party expertise early on to formulate effective market and product strategies.

Operating non-standard health insurance is challenging not only because of the complex health conditions of policyholders but also because it requires integrating resources for product development and sales targeting specific diseases and populations.

Overall, the key industry players involved in non-standard risk health insurance primarily include direct insurers, reinsurers, medical and health management service providers, and pharmaceutical and medical device companies. The broader the population covered by non-standard risk health insurance, the greater the number of industry players required, as well as the more diverse the dimensions and methods of resource integration. Deep integration and efficient collaboration among these players and resources are therefore critical.

However, given the large number of stakeholders and their differing immediate interests, while it may not be difficult to align business objectives between two parties, achieving alignment between actual operations and ultimate goals among multiple parties is exceedingly challenging. Therefore, introducing a third party, rather than relying on direct end-to-end communication, has become the optimal solution to this problem. “Xiaoweibao” serves precisely as such a third party, leveraging a holistic perspective on the supply-demand matching of insurance products to identify common ground among the interests of all parties and facilitate cooperation among the relevant stakeholders.

Specifically, with “Xiaoweibao” as the hub, we partner with primary insurers and reinsurers to jointly launch competitive insurance products; collaborate with service providers to integrate high-quality medical and health services into insurance offerings, thereby serving policyholders collectively; and connect with distribution channels to enable precise product outreach to a broader user base and expand incremental markets. Ultimately, this fosters a collaborative network that delivers mutual benefits and win-win outcomes for all stakeholders.

Of course, establishing connections is not a simple 1+1=2 combination; rather, it requires deep integration of resources from all parties, continuous product delivery, and the satisfaction of diverse stakeholder interests to create a mutually beneficial business ecosystem.

“Xiaoweibao” can fully integrate industry resources to provide “business accompaniment” for partners throughout the entire lifecycle of insurance products, offering integrated consulting and implementation solutions that cover product development and design, underwriting and claims risk control, sales system establishment, and health management.

“Xiaoweibao” leverages its parent company’s long-standing professional expertise to cultivate in-house business development and operational capabilities. It has assembled a team of business solution experts and established a multidisciplinary professional group comprising product specialists, actuaries, physicians and pharmacists, health insurance analysts, and algorithm engineers. Deeply engaged in AI- and big data-driven analytics, clinical analysis, and other intelligent health assurance services within the basic medical insurance and commercial insurance sectors, Xiaoweibao provides specialized human resource support for “business companionship” services.

Meanwhile, “Xiaoweibao” also engages in extensive collaborations with medical institutions, health management organizations, and insurance brokerage firms, empowering these professional entities to deliver high-quality medical and health services to policyholders, thereby reducing the risk of diseases or complications.

Taking the non-standard risk “Zhenxiang e-Sheng” million-yuan medical insurance product, launched in collaboration with PICC Property and Casualty Company, as an example, this product is not only empowered by Weijia Brokerage’s comprehensive insurance technology services, but also integrates Puxiang Health’s health management services. It was jointly released with industry partners across the “insurance + healthcare + broader health” ecosystem, including Qingsong Bao Yanxuan, Weimai, Xinyikang, Yixin Technology, Zhongchi Insurance, and Yizhentong.

Furthermore, after nearly a year of development, IVF insurance has provided “business accompaniment” solutions for professional brokerage firms such as Mingya and Little Umbrella, while continuously delivering end-to-end services encompassing both product and operations.

Overall, “Xiao Wei Bao” can be regarded as a “model template” for business accompaniment built by various partners. Within this “model template,” “Xiao Wei Bao” serves its partners throughout the entire process by modularizing industrial resources and its own practical experiences.

Short-term health insurance is characterized by low coverage amounts and a high volume of policies, which can lead to elevated operational costs for insurers in areas such as policyholder inquiries and claims processing. Individuals with non-standard health profiles present diverse health conditions and tend to raise more questions about specific products. Furthermore, as the market is still in its early stages, consumers have limited knowledge of these products, necessitating extensive market education and thereby driving up operational costs even further.

To address these challenges, third-party platforms can leverage human and material resources as well as diverse channels and methods in a centralized manner. On one hand, they can continuously educate the public about non-standard risk health insurance over the long term, thereby reducing product promotion costs. On the other hand, they can operate specific products on a project basis to control operational costs throughout the entire process and enhance the overall effectiveness of promotion and operations.

Taking “Xiaoweibao” as an example, the platform has established a service matrix on social media channels such as WeChat, Xiaohongshu (Little Red Book), and Douyin (TikTok), encompassing insurance education, health services, curated product selection, and consultation. First, “Xiaoweibao” educates users on diseases and insurance knowledge, building its content brand and professional influence to bridge the information gap between target audiences for non-standard risk insurance and specialized expertise. Second, leveraging its professional influence, “Xiaoweibao” provides consultation services and develops tailored insurance solutions for individuals with non-standard risks, thereby reducing the information asymmetry between this precisely targeted audience and specific insurance products.

In other words, the insurance plans formulated by “Xiaoweibao” for users are built on a foundation of long-term operations. This intensive operational approach can deepen users’ overall understanding of non-standard risk insurance, thereby facilitating their purchase decisions. Such decisions are grounded in rational evaluation and genuine needs, thus avoiding irrational purchases or those driven by cognitive biases, which could otherwise lead to complications in subsequent claims processing.

Furthermore, “Xiaoweibao” can also assist insurance companies in decision-making by leveraging the data accumulated from the aforementioned service matrix.

Therefore, intensive operations help numerous B-side partners efficiently and accurately establish and refine user perception, thereby enhancing the overall comprehensive benefits of non-standard risk insurance operations.

Despite the rapid growth of insurance for non-standard risks, the industry has long recognized that commercial insurers still face numerous challenges in underwriting and claims settlement due to insufficient data, which has, to some extent, become an obstacle to industry development.

At the same time, it is important to recognize that, in order to improve the multi-tiered medical security system, the healthcare security authorities have been vigorously promoting the breaking down of data barriers.

In 2023, the Shanghai Municipal Healthcare Security Administration and six other departments issued the "Several Measures of Shanghai Municipality on Further Improving the Multi-tiered Payment Mechanism to Support the Development of Innovative Drugs and Medical Devices," which outlined 28 key tasks, 16 of which pertained to promoting the standardized development of commercial health insurance. For instance, eligible commercial insurance companies may, in compliance with regulatory and safety requirements, legally leverage big data from medical services and medical insurance to conduct actuarial analyses, develop market-appropriate products, achieve scientific and precise pricing, effectively reduce risk control costs, and lower product prices.

Previously, the National Healthcare Security Administration also conducted pilot programs for the authorized inquiry and use of personal medical insurance information in more than 10 cities across China.

“Xiaoweibao” continues to accumulate risk control expertise and data analytics capabilities. As policies are gradually relaxed and become more favorable, the data barriers that once hindered non-standard health insurance are poised to be broken down within a legal and compliant framework. Non-standard health insurance holds significant promise for the future, with companies possessing strong foundational strengths expected to gain momentum more rapidly.