Domestic New Drug Approval Intensifies EGFR Market Competition as Johnson & Johnson Poised to Disrupt with Amivantamab

Recently, the National Medical Products Administration (NMPA) website announced the approval of Rezivertinib Mesylate Capsules (development code: BPI-7711; brand name: Ruibida), a Class 1 innovative drug and third-generation EGFR inhibitor submitted by Betapharma (Shanghai) Co., Ltd. The approved indication is for the treatment of adult patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) who have experienced disease progression during or after prior therapy with an epidermal growth factor receptor (EGFR) tyrosine kinase inhibitor (TKI) and whose tumors test positive for the EGFR T790M mutation.

Rezivertinib is the fifth third-generation EGFR inhibitor approved for marketing in China. With the entry of Betapharma, the competition among Hansoh, Allist, Beta Pharma, and AstraZeneca will undoubtedly intensify. The already fierce battle for the third-generation EGFR-TKI market is set to become even more contentious and unpredictable.

In addition to the third-generation EGFR-TKIs already on the market, fourth-generation EGFR-TKIs are also under development. The driving force behind their continuous upgrading and iteration is “drug resistance.”

EGFR mutations are the most common driver genes in patients with lung adenocarcinoma. The prevalence of EGFR gene mutations is significantly higher in Asian populations than in Caucasian populations, generally exceeding 40%; for instance, the EGFR mutation rate among Chinese patients with non-small cell lung cancer is approximately 40%. As the primary therapeutic agents for patients with EGFR mutations, these drugs have made the Asian market a key battleground for pharmaceutical companies.

First-generation EGFR-TKIs, represented by gefitinib and erlotinib, are sensitive to EGFR 19del/L858R mutations. However, drug resistance has gradually emerged in clinical practice; for instance, resistance mediated by the T790M mutation accounts for more than 60% of cases. This has spurred the development of second-generation inhibitors such as afatinib and dacomitinib. Nevertheless, due to their lack of selectivity, these agents have failed to achieve ideal clinical efficacy and are associated with greater toxicity and adverse effects, thus falling short of representing a successful product iteration.

The mechanisms of resistance following third-generation EGFR TKI therapy are complex. After first-line treatment with osimertinib, the first third-generation agent approved in China, the incidence of EGFR-dependent resistance mutations is approximately 6%–12%, predominantly consisting of EGFR C797X mutations. Following second-line osimertinib treatment, the incidence of EGFR-dependent resistance mutations is approximately 10%–20%, also primarily driven by C797X mutations. EGFR-dependent resistance mechanisms mainly include MET amplification, cell cycle-related gene alterations, PIK3CA mutations or amplification, and HER2 mutations or amplification.

Following AstraZeneca’s osimertinib, Hansoh’s almonertinib, Allist’s furmonertinib, and Betta Pharmaceuticals’ befotertinib have successively received approval. With the recent approval of rezivertinib, the market is poised for intense competition among these key players.

In addition to the recently approved rezivertinib, the other four third-generation EGFR-TKI drugs have all been included in the National Reimbursement Drug List (NRDL). Among them, AstraZeneca’s osimertinib, Hansoh Pharmaceutical’s aumolertinib, and Allist’s furmonertinib have obtained indications for both first- and second-line treatments and are covered by the NRDL. In contrast, Beta Pharma’s befotertinib is currently reimbursed only for second-line therapy, as its indication for first-line treatment was not approved until late 2023.

The five third-generation EGFR-TKIs marketed in China share a consistent basic structure, all featuring side-chain modifications on a backbone similar to that of osimertinib. This implies that differences in overall efficacy data are likely to be minimal, with each manufacturer’s unique advantages being demonstrated through their respective clinical strategies.

As the first third-generation drug to be marketed, osimertinib achieved a median progression-free survival (mPFS) of 10 months in second-line treatment, after which its indications were expanded to include first-line treatment and postoperative adjuvant therapy.

Data from a real-world study of 1,556 patients showed that the objective response rates (ORR) for osimertinib and first-generation drugs were 63.4% and 48.0%, respectively (P<0.001). Significant improvements were observed in both progression-free survival (PFS) (19.4 vs. 10.9 months; hazard ratio [HR] for progression, 0.47; 95% CI, 0.38 to 0.59; P<0.001) and overall survival (OS) (40.5 vs. 34.3 months; HR, 0.76; 95% CI, 0.58–1.00; P=0.045). Meanwhile, osimertinib demonstrated a more manageable safety profile.

The advent of osimertinib has enabled third-generation drugs to aggressively capture the market for first-line treatment of EGFR-mutated NSCLC.

As a first-in-class (FIC) drug, osimertinib has captured the market by leveraging its first-mover advantage and has demonstrated efficacy and safety through extensive clinical validation. However, osimertinib is not without limitations. In patients with classic EGFR mutations (exon 19 deletion [19del] or L858R), osimertinib nearly doubled progression-free survival (PFS) compared to first-generation tyrosine kinase inhibitors (TKIs) in those with exon 19 deletions. In contrast, it did not show a significant advantage over first-generation TKIs in patients with the L858R mutation; clinical trials conducted in China failed to demonstrate statistical significance (PFS HR=0.69, 95% CI: 0.39–1.21).

This provides domestic followers with a clear direction for strategic focus.

Hansoh Pharmaceutical’s almonertinib is the first domestically developed third-generation EGFR-TKI to receive approval. Its structural design features the substitution of a methyl group with a cyclopropyl group on the indole ring, and it was the subject of the first registration study for first-line treatment of NSCLC with a third-generation EGFR-TKI conducted in the Chinese population.

In the AENEAS clinical trial, a total of 429 patients with EGFR mutation-positive advanced non-small cell lung cancer (NSCLC) were enrolled. The results showed that almonertinib, compared with gefitinib, significantly prolonged median progression-free survival (mPFS) (19.3 months vs. 9.9 months; HR=0.46, P<0.0001) and median duration of response (mDoR) (18.1 months vs. 8.3 months; HR=0.38, P<0.0001).

Among them, in the 19del mutation subgroup, the mPFS was 20.8 months in the almonertinib group and 12.3 months in the gefitinib group (HR, 0.39; P < 0.0001); in the L858R mutation subgroup, the mPFS was 13.4 months in the almonertinib group and 8.3 months in the gefitinib group (HR, 0.60; P = .0102).

Overall, as the first domestically developed third-generation drug, almonertinib has followed a "me-too" approach and has not demonstrated significant advantages over osimertinib in terms of data.

Furmonertinib, launched subsequently by Allist, features further structural optimization by replacing the methoxyphenyl group in osimertinib with a trifluoroethoxypyridine moiety, thereby enhancing its potency and improving blood-brain barrier penetration (facilitating more effective entry into the brain and yielding superior efficacy against brain metastases).

In the randomized, double-blind, active-controlled, multicenter Phase 3 FURLONG study, furmonertinib demonstrated a median progression-free survival (PFS) of 20.8 months, which was significantly superior to the 11.1 months observed with gefitinib (HR=0.44 [95% CI 0.34–0.58], P<0.0001), with consistent benefits across all subgroups.

At triple the dose, furmonertinib achieved a confirmed objective response rate (cORR) of 78.6% and a median duration of response (mDoR) of 15.2 months in treatment-naïve patients with non-small cell lung cancer (NSCLC) harboring EGFR exon 20 insertion mutations. Furthermore, this indication received Breakthrough Therapy Designation from the U.S. Food and Drug Administration (FDA) last October, and the global pivotal Phase III clinical trial is currently enrolling patients.

At the recently concluded 2024 American Society of Clinical Oncology (ASCO) Annual Meeting, a real-world study on high-dose furmonertinib for the treatment of patients with EGFR-mutated non-small cell lung cancer (NSCLC) and leptomeningeal metastases (LM) attracted significant attention within the industry.

Leptomeningeal Metastasis (LM) is a severe complication of advanced lung adenocarcinoma (LUAD), typically associated with a poor prognosis. EGFR exon 20 insertion mutations represent the third most common type of EGFR mutation, and the optimal treatment strategy for patients harboring these mutations remains unclear.

In this study, furmonertinib combined with intraventricular chemotherapy via an Ommaya reservoir was evaluated. With a median follow-up of 9.3 months, the intracranial objective response rate (iORR) reached 60%, and the intracranial disease control rate (iDCR) reached 90%. The median intracranial progression-free survival (iPFS) was 7.3 months (95% CI, 3.3 months–NR), and the median overall survival (OS) was 8.8 months (95% CI, 4.9 months–NR). Compared with other third-generation EGFR-TKIs, it demonstrated robust control over brain metastases.

Clinical Data of Third-Generation EGFR-TKIs Approved in China: Non-Head-to-Head Comparisons

Befotertinib, which was subsequently approved for marketing, also demonstrates strong competitiveness.

In a pivotal Phase III clinical trial, befotertinib demonstrated significant efficacy as a first-line treatment for patients with advanced non-small cell lung cancer (NSCLC) harboring EGFR mutations. The study results showed that the median progression-free survival (PFS) was 22.1 months in the befotertinib group, compared with 13.8 months in the control group. Furthermore, befotertinib significantly reduced the risk of disease progression or death by 51% (HR 0.49, P < 0.0001). Notably, among patients with baseline brain metastases, the median PFS was 19.4 months in the befotertinib group versus 13.7 months in the control group, also demonstrating a significant benefit (HR 0.48, P = 0.0086).

Befotertinib also demonstrated excellent efficacy as a second-line treatment. In a clinical study involving 290 patients with non-small cell lung cancer (NSCLC) who had progressed after first- or second-generation EGFR-TKI therapy and tested positive for the EGFR T790M mutation, befotertinib treatment yielded an objective response rate (ORR) of 67.6% and a disease control rate (DCR) of 94.8%. Notably, patients receiving the “100 mg QD” dosage achieved a higher ORR than those receiving the “75 mg QD” dosage (71.2% vs. 57.7%). The median progression-free survival (PFS) was 17.9 months in the high-dose group and 16.6 months in the low-dose group.

After weathering numerous controversies, rezivertinib, the fifth third-generation EGFR-TKI in China, has finally received approval for market launch.

Data from previous clinical trials showed an ORR of 64.6% and a DCR of 89.8%. The median duration of response was 12.5 months, and the median PFS was 12.2 months. The median OS was 23.9 months. Among the 91 patients (40.3%) with central nervous system (CNS) metastases, the median CNS PFS was 16.6 months.

With the approval of rezivertinib, the already fiercely competitive third-generation EGFR-TKI market is once again undergoing a shift.

According to data from Guosen Securities, domestic sales of EGFR-TKIs exceeded RMB 10 billion as early as 2022, with third-generation agents accounting for approximately 70% of the total.

Whether a drug can achieve significant sales volume and profitability typically depends on the patient population base, penetration rate, and pricing. According to data from the report released by the National Cancer Center, there were approximately 4.825 million new cancer cases in China in 2022, with lung cancer ranking first at around 1.06 million cases. Non-small cell lung cancer (NSCLC) accounts for over 80% of these cases, and the EGFR mutation rate among lung cancer patients in China is approximately 50%. This means that there are more than 400,000 newly diagnosed NSCLC patients with EGFR mutations each year.

On the other hand, four previously launched drugs have been successfully included in the National Reimbursement Drug List (NRDL). Meanwhile, the per-box price of three domestically produced drugs has dropped to around RMB 2,000, driving rapid sales growth for these medications over the past two years.

Based on 2023 sales figures, osimertinib, having secured a first-mover advantage, firmly holds the top position in both global and domestic sales, with domestic revenue reaching approximately RMB 7 billion. Although almonertinib has not disclosed its sales figures, its 2022 sales amounted to RMB 2.4 billion. Furmonertinib recorded RMB 2 billion in sales, while befotertinib achieved RMB 60 million.

Taking furmonertinib as an example, its rapid growth enabled Allist to achieve a roughly threefold increase in its stock price from the bottom within just two years.

In March 2021, furmonertinib, after nearly a decade of research and development, was approved for marketing as a second-line treatment for non-small cell lung cancer (NSCLC) and was included in the National Reimbursement Drug List (NRDL) in the same year. Subsequently, in June 2022, it received approval for first-line treatment of NSCLC, with this indication also added to the NRDL later that year. In 2023, furmonertinib was once again included in the National Reimbursement Drug List through the simplified renewal process.

At that time, Mou Yanping, former Managing Director of MSD China’s Oncology Business Unit who was responsible for the domestic sales of Keytruda, joined Allist to oversee the commercialization of furmonertinib. Under the leadership of this “Queen of Oncology,” Allist built a marketing team covering 30 provinces and municipalities, established a comprehensive nationwide sales network, and reached more than 1,000 hospitals in core market regions. The company also partnered with Fosun Pharma to leverage its market channels, accelerating the “omni-channel” commercial layout and market coverage of furmonertinib.

Driven by a series of strategic initiatives, furmonertinib generated RMB 236 million in sales revenue upon its market launch in 2021, enabling Allist Pharmaceuticals to turn losses into profits. In 2022, sales revenue reached RMB 790 million, with Allist posting a net profit of RMB 130 million, a year-on-year increase of 614.44%. In 2023, sales revenue amounted to RMB 1.98 billion, and Allist’s net profit reached RMB 640 million, representing a year-on-year growth of 393.54%.

In Q1 2024, furmonertinib maintained its strong growth momentum. Allist generated revenue of RMB 743 million, a year-on-year increase of 168.65%; net profit attributable to shareholders of the listed company reached RMB 306 million, a year-on-year surge of 777.51%.

This sales landscape also aligns with the positioning of each product. Due to the structural similarities among these drugs, there will not be significant differences in their baseline data; the key lies in how each company designs its clinical trials to demonstrate differentiated advantages.

For instance, osimertinib, which holds a first-mover advantage, has not only conducted multicenter clinical trials involving over 1,000 patients worldwide but also expanded its indications through combination therapies with other drugs. For example, the CNS response rates for osimertinib combined with anlotinib or bevacizumab are both higher than those for osimertinib monotherapy.

As the first domestically produced third-generation EGFR-TKI, almonertinib has carved out a market niche despite lacking distinct clinical advantages, largely driven by its inclusion in the National Reimbursement Drug List (NRDL) and competitive pricing. Furmonertinib, leveraging its longer progression-free survival (PFS) and superior efficacy in controlling brain metastases, has become a preferred later-line therapy for intracranial progression following treatment with other third-generation agents. Furthermore, furmonertinib is poised for new growth opportunities if it subsequently gains approval for the indication of exon 20 insertion mutations.

Although befotertinib demonstrates prolonged progression-free survival (PFS) in both first- and second-line settings, along with favorable clinical data for L858R mutations, its market uptake has not yet fully accelerated, as only its second-line indication was included in the National Reimbursement Drug List (NRDL) in 2024. In contrast, the first- and second-line indications for osimertinib, aumolertinib, and furmonertinib in the treatment of non-small cell lung cancer (NSCLC) have all been incorporated into the NRDL. Notably, osimertinib is the first third-generation EGFR-TKI targeted therapy covered by the NRDL for postoperative adjuvant treatment.

For rezivertinib, the first-line treatment indication has not yet been approved, and it remains uncertain whether it will be included in the National Reimbursement Drug List (NRDL) negotiations. Given that it typically takes 3–4 years for drugs listed through national negotiations to achieve full hospital access, rezivertinib still has a long road ahead.

AstraZeneca has spared no effort in promoting osimertinib in recent years. Recently, the company announced that its supplemental New Drug Application (sNDA) for osimertinib has been accepted by the U.S. FDA and granted Priority Review designation for the treatment of adult patients with unresectable Stage III epidermal growth factor receptor-mutated (EGFRm) non-small cell lung cancer (NSCLC) following chemoradiotherapy (CRT). If approved, osimertinib will be indicated for EGFR-positive patients with exon 19 deletion (19del) or L858R mutations. The FDA is expected to complete its review in Q4 2024.

However, the spotlight in this niche segment was ultimately captured by Johnson & Johnson. In its inaugural foray into lung cancer treatment, J&J directly targeted AstraZeneca, the reigning leader in the EGFR-mutated NSCLC space.

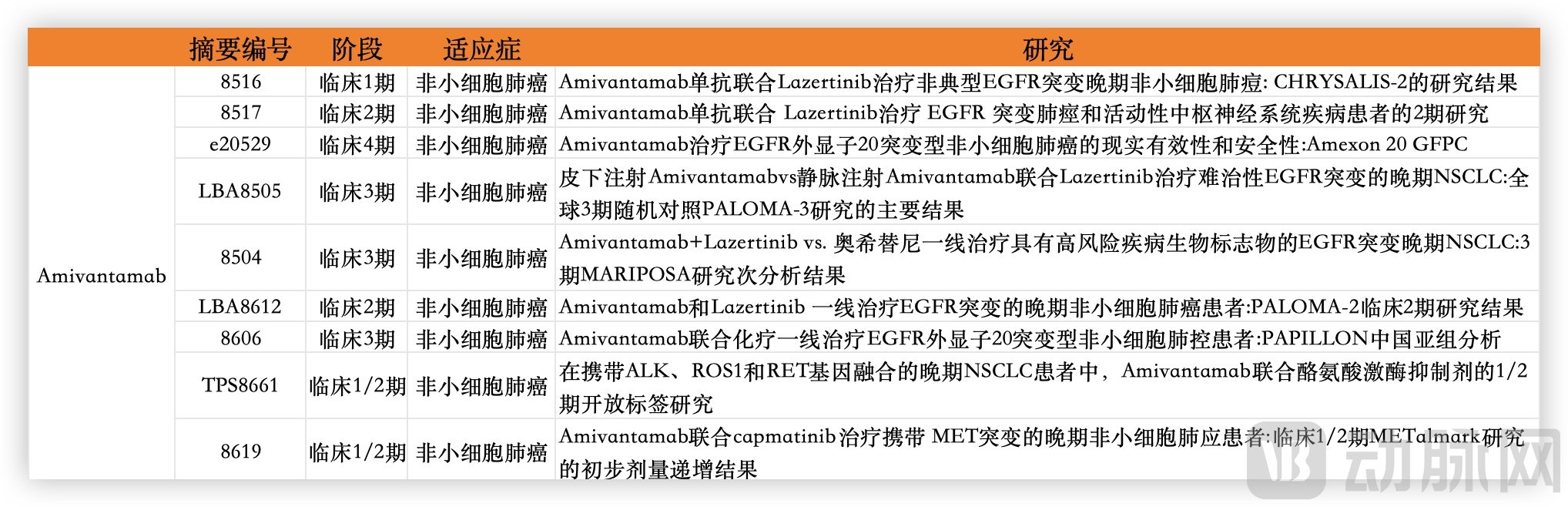

At ASCO 2024, Johnson & Johnson showcased its blockbuster drug Amivantamab, making a high-profile entry into the EGFR-mutated NSCLC arena. The significant attention it garnered stems from its strong performance in both first-line treatment and overcoming resistance.

Amivantamab Reports at the ASCO Annual Meeting: Data Compiled from ASCO

In the MARIPOSA clinical trial, a head-to-head study was conducted comparing two arms: amivantamab plus lazertinib versus osimertinib monotherapy. Among patients with TP53 mutations, the median progression-free survival (PFS) was 18.2 months in the combination therapy group, compared to only 12.9 months in the osimertinib group. In patients with detectable ctDNA, the median PFS was 20.3 months and 14.8 months, respectively. While the head-to-head comparison with osimertinib demonstrates its potential as a first-line treatment, amivantamab has also shown promising efficacy in the MARIPOSA-2 trial, which investigates resistance mechanisms.

At this year’s ASCO Annual Meeting, nine studies related to amivantamab were selected for presentation, underscoring its significant potential. To date, amivantamab has received FDA approval for the treatment of EGFR exon 20 insertion mutations. Moving forward, it will compete with AstraZeneca in the first- and second-line settings for EGFR sensitizing mutations. On one side, amivantamab is being combined with a third-generation EGFR-TKI that demonstrates outstanding efficacy against brain metastases; on the other, AstraZeneca is striving to maintain its market position through combinations involving chemotherapy and antibody-drug conjugates (ADCs). In the near future, we may witness a major transformation in the market for EGFR-mutant lung cancer.

It is worth noting that Johnson & Johnson has projected a peak sales figure of $5 billion for Amivantamab, while the National Medical Products Administration (NMPA) accepted its marketing authorization application in China in January 2024. For domestically produced EGFR-TKI drugs, more intense competition is imminent.