Major Shift in China's Aesthetic Medicine Sector: 'Big Three' Slow Down as Diversified Pharma Companies Surge

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

Amid frequent rejections of biopharmaceutical IPOs and commercialization hurdles in the medical device sector, the medical aesthetics industry—characterized by rapid monetization and high profit margins—has undoubtedly become a “safe haven” for many pharmaceutical companies and investors, with related investments and industrial deployments occurring from time to time.

But in reality, the medical aesthetics industry has also been having a tough time in recent years, justTaking the “Three Musketeers”—Bloomage Biotech, Imeik, and Haohai Biological Technology—as examples, their recent financial performances have all declined to varying degrees.For instance, Bloomage Biotech’s total revenue decreased by 4.45% year-on-year in 2023, while its net profit attributable to shareholders of the parent company dropped by 38.97% year-on-year. Imeik experienced a slowdown in growth, with its revenue growth rate declining by 20% and its net profit growth rate falling by nearly 30% year-on-year in the first quarter of 2024. Haohai Biological Technology began lagging behind as early as 2022, when its net profit plummeted by 48.76% year-on-year. Although its performance improved significantly in 2023, its revenue and net profit scales remained the lowest among the “Three Musketeers.”

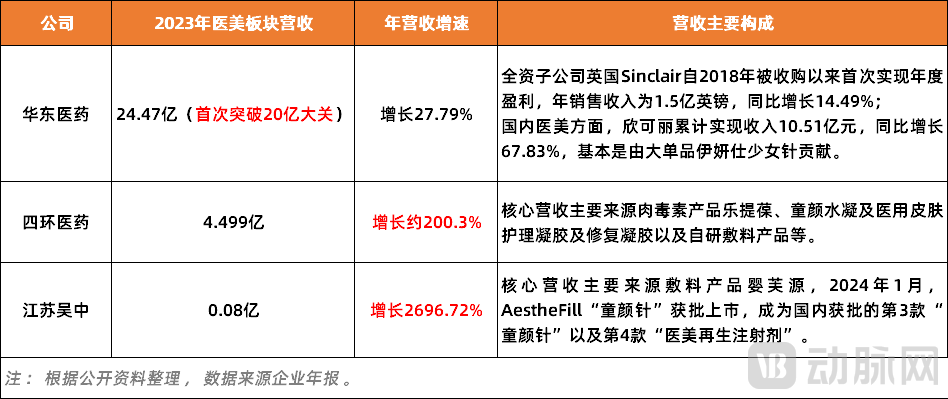

Figure 1. Aesthetic Medicine Revenue of Selected Cross-Industry Pharmaceutical Companies in 2023 (Source: Corporate Annual Reports)

Figure 1. Aesthetic Medicine Revenue of Selected Cross-Industry Pharmaceutical Companies in 2023 (Source: Corporate Annual Reports)

However, this does not represent the full picture of the medical aesthetics industry. On another front, pharmaceutical companies that have diversified into this sector are finally reaping substantial rewards after years of accumulation. A typical representative is Huadong Medicine; according to its annual report, the medical aesthetics segment achieved a total operating revenue of RMB 2.447 billion in 2023, a year-on-year increase of 27.79%, gradually approaching the level of the “Big Three.” Sihuan Pharmaceutical’s revenue from medical aesthetics products in 2023 amounted to RMB 449.9 million,Year-on-year increase of approximately 200.3%; Although Jiangsu Wuzhong's revenue from medical aesthetics and life sciences amounted to only RMB 8 million in 2023,Increase of up to 2696.72%, with a clear upward trend.

As the “Three Musketeers” collectively slow down, cross-industry pharmaceutical companies are rising strongly. Amid this ebb and flow, undercurrents are surging throughout the medical aesthetics industry, with a major transformation reshaping the industrial landscape quietly underway.

Are Cross-Industry Pharmaceutical Companies Officially Joining the Aesthetic Medicine Arena?

Over the past year, the "Three Musketeers" have all experienced significant declines in market capitalization, with Imeik shrinking by 53 billion yuan, Bloomage Biotech decreasing by 18.5 billion yuan, and Haohai Biological Technology dropping by 2.7 billion yuan. The reasons for this are as follows:To a large extent, the “Three Musketeers” have all encountered varying degrees of growth bottlenecks in their performance in recent years., investors lack confidence in this.

As is well known, the core business of the “Three Musketeers” revolves around hyaluronic acid. However, since 2022, intensified market competition and continuous capacity expansion have led to a sustained decline in the price of hyaluronic acid raw materials, with the drop exceeding 60% at one point. This has consequently made it increasingly difficult for the “Three Musketeers” to generate revenue. Taking Bloomage Biotech, which has the largest revenue scale, as an example, the revenue growth rates of its four major skincare brands all declined significantly in 2023, with an average decrease of more than 15%.

However, this is not the most thorny issue, ““The Three Musketeers” May Find It Harder to Make Money, but Are Becoming Increasingly “Generous” in Spending. For instance, with regard to selling expenses, the annual report indicates thatIn 2023, the “Three Musketeers” spent a total of RMB 3.912 billion on marketing promotion, which is nearly 700 million more than in 2021, the year with the fastest performance growth.

Furthermore, at the R&D level. In recent years, the “Big Three” have been continuously increasing their investment in new pipelines. Currently, Bloomage Biotech has 7–8 collagen products under development; Imeik has 9 projects in the pipeline, mainly focused on botulinum toxin; and Haohai Biological Technology has a total of 17 projects under development, including 6 in the medical aesthetics sector. Behind this lies substantial expenditure, as indicated by the annual reports,“The Three Musketeers” Invested Nearly RMB 1 Billion in R&D in 2023Coupled with high sales expenses and sluggish revenue growth caused by the fading hyaluronic acid dividend, it is not difficult to understand why the “Three Musketeers” have experienced slowed growth rates and declining net profits.

However, this does not mean that the medical aesthetics market is shrinking. In fact, the industry is still expanding, particularly in the field of non-surgical medical aesthetics.The compound annual growth rate remains above 15%.So, who exactly has taken a “share of the pie”? The answer lies with the increasingly prominent cross-industry pharmaceutical companies.

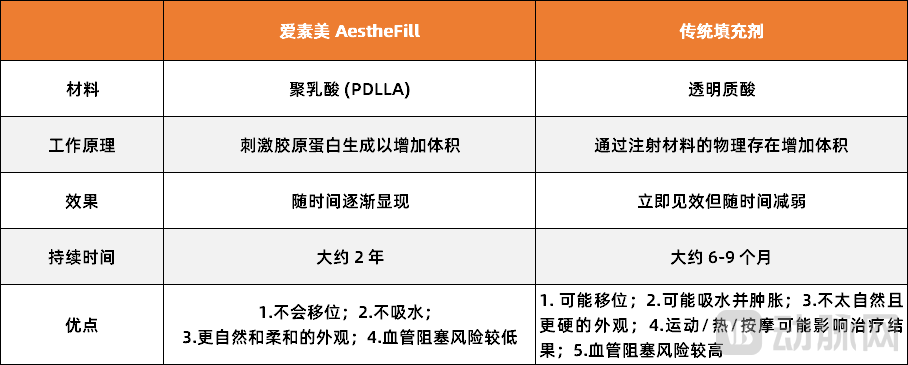

All of this is, of course, traceable.First, a large number of medical aesthetic products from cross-industry pharmaceutical companies have begun to receive approval and enter the market.For instance, Huadong Medicine currently offers 38 medical aesthetic products featuring “minimally invasive and non-invasive” technologies, 24 of which have been launched in domestic and international markets. Sihuan Pharmaceutical also has more than 10 Class III and over 20 Class II self-developed medical aesthetic products, including Ellansé (“Girl Needle”) and Sculptra (“Baby Face Needle”). Additionally, Jiangsu Wuzhong is ramping up its efforts; in January 2024, its regenerative injectable AestheFill received approval from the National Medical Products Administration (NMPA) for market launch and is poised to begin generating revenue.

Figure 2. Comparison of the regenerative injectable AestheFill with traditional fillers

Figure 2. Comparison of the regenerative injectable AestheFill with traditional fillers

However, having products alone is not enough; market competitiveness must also keep pace. Take Jiangsu Wuzhong’s AestheFill as an example: it contains poly-L-lactic acid (PLLA), a synthetic biodegradable material that stimulates collagen regeneration. Additionally, Sihuan Pharmaceutical holds the exclusive agency rights for SYLFIRM X, a radiofrequency (RF) microneedling device. As the world’s first RF microneedling instrument to utilize dual-wave technology (combining continuous and pulsed waves), it addresses skin concerns across all layers, from superficial to deep, offering multiple benefits including facial and body tightening, lifting, and hair regeneration.

Lastly, sales capability deserves mention. In an interview, an investment firm deeply entrenched in the medical aesthetics sector stated, “A key advantage for pharmaceutical companies entering the medical aesthetics sector lies in their established sales channels, which can effectively support the distribution and promotion of their own aesthetic products.”。

In fact, as pharmaceutical companies’ medical aesthetics products gradually enter the market, this advantage is being amplified. Take Huadong Medicine as an example: long hailed as having a “sales iron army,” it possesses distinct advantages in marketing and distribution channels and excels at creating blockbuster products, which aligns perfectly with the promotion logic for medical aesthetics offerings. Sihuan Pharmaceutical follows a similar path; according to its announcements, its sales channels now cover more than 4,700 medical aesthetics institutions, achieving 100% coverage of leading players in the sector. Therefore, it is hardly surprising that cross-industry pharmaceutical companies are able to capture a certain share of the market from the “Three Musketeers.”

M&A Advisory Heats Up as Competition Intensifies Among Upstream Players in the Medical Aesthetics Industry

As the era of “hyaluronic acid for everything” gradually fades into the past, the entire medical aesthetics industry is searching for the next blockbuster product. Judging from strategic deployments in recent years,Most have set their sights on emerging fields such as collagen and botulinum toxin.. In fact, the achievement of this industry consensus is premised on certain conditions.

For major medical aesthetics companies, as the growth of hyaluronic acid slows down, they have gradually realized that relying on a single product is no longer a viable strategy. Consequently, they are shifting their focus to collagen and botulinum toxin, which offer greater market potential. As for pharmaceutical companies entering the field from other sectors, most of them entered the market around 2018–2020. If they were to invest heavily in hyaluronic acid at this stage, they would clearly lack competitive advantage. Instead, targeting collagen and botulinum toxin—sectors that are currently gaining momentum and feature a more open market landscape—would be a more cost-effective strategy.

Another critical factor is the shift in market demand,"Gradually"Centered on concepts such as regeneration and anti-agingFollowing this logic, categories such as botulinum toxin and collagen evidently hold greater market persuasiveness.

Figure 3. Comparison of Performance Between Hyaluronic Acid and Botulinum Toxin Products

Figure 3. Comparison of Performance Between Hyaluronic Acid and Botulinum Toxin Products

It is reported that hyaluronic acid is a high-molecular-weight glycosaminoglycan. After injection into the skin, it primarily promotes hydration, thereby improving texture or reducing roughness; thus, it is commonly used for moisturizing and restoring skin texture. Botulinum toxin, on the other hand, is a paralytic neurotoxin that induces localized muscle paralysis by blocking the release of acetylcholine at the neuromuscular junction, thereby reducing facial wrinkles. Consequently, it is mainly used for wrinkle reduction and cosmetic purposes.

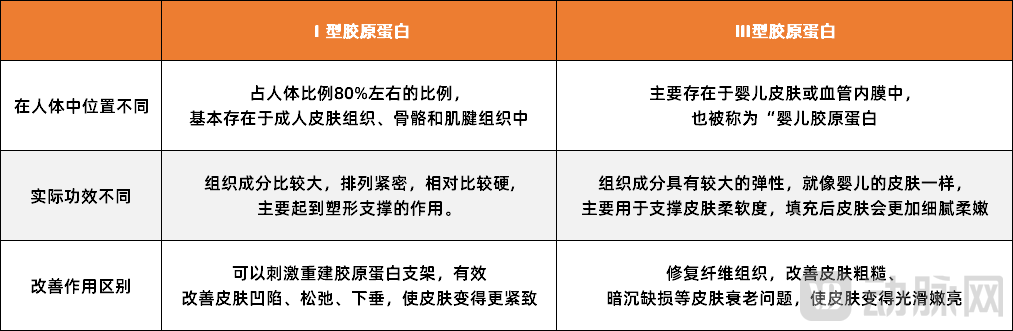

Figure 4. Comparison of Type I Collagen and Type III Collagen

Figure 4. Comparison of Type I Collagen and Type III Collagen

Collagen is a complex collagen that replenishes, induces, stimulates, and rebuilds collagen fibers, reshapes the skin's fibrous structure, synthesizes new collagen, and regenerates new tissue, thereby providing robust structural support and strength to prevent facial wrinkles and depressions.

In response, the head of a medical aesthetics company told VCBeat, “There is no inherent superiority or inferiority among these three; they simply have different specific functions due to their distinct ingredients. Therefore, when selecting products, you should base your choice on your own skin type."Of course, from the current perspective, wrinkle reduction and anti-aging are clearly the mainstream consumer trends. Coupled with the oversupply of hyaluronic acid, it is not surprising that collagen and botulinum toxin have become fiercely contested areas as the medical aesthetics industry urgently seeks a second growth curve."

So, how should one strategize? Through observation,The most direct and common approaches are mergers and acquisitions (M&A) and agency agreements, essentially a “buy, buy, buy” strategy.。

Taking Imeik as an example, to enter the botulinum toxin sector, it first signed an exclusive agency cooperation agreement with South Korea’s Huons Global in 2018 for Type A botulinum toxin products in China. Subsequently, in 2021, it invested nearly RMB 890 million to acquire a stake in South Korea’s Huons Bio, thereby securing the exclusive distribution rights in the Chinese market for Huons Bio’s botulinum toxin product, Hutox (commonly known as “Orange Toxin”). Recently, Hutox announced the completion of its Phase III clinical trials and has initiated the registration application process.

Compared with traditional medical aesthetics companies, cross-industry pharmaceutical enterprises are even more aggressive in their M&A activities. Taking Huadong Medicine as an example, in its bid to rapidly transition into the medical aesthetics sector,Nearly 20 major BD deals were closed over the past three years.Among these, the most significant transaction was the $220 million acquisition of Sinclair in 2018, a long-established British medical aesthetics company. Huadong Medicine’s current best-selling medical aesthetics product, “Ellansé” (commonly known as “Girl Needle”), originates from this acquisition. According to the 2023 annual report, Sinclair has achieved annual profitability.

In this regard, a senior investor in the medical aesthetics sector remarked, “Compared with in-house R&D, mergers and acquisitions are clearly a more effective, or rather, more cost-efficient approach, primarily when considering the speed of realization,”After all, from the market logic of medical aesthetic products, if a company enters the market later, it will lose its first-mover advantage. To turn the tide subsequently, it would require significantly higher marketing costs or more substantial product upgrades and iterations, which entail enormous expenditures and industry risks.。”

Therefore, mergers and acquisitions are undoubtedly a shortcut for medical aesthetics companies and cross-industry pharmaceutical enterprises to move “upstream,” but such shortcuts come with uncertainties. In September 2023, Bloomage Biotech officially announced the termination of its partnership with Medytox. The immediate trigger was Medytox’s regulatory violations: three botulinum toxin products were investigated by South Korea’s Ministry of Food and Drug Safety (MFDS) and subjected to indefinite production suspensions due to the use of unapproved bulk solutions and falsified experimental materials. This incident not only incurred substantial costs for Bloomage Biotech but also severely disrupted its strategic layout in the botulinum toxin sector.

This is not an isolated case. On June 19, 2023, the National Medical Products Administration (NMPA) terminated the registration review of the “cellulose hydrogel capsules” application submitted by CMS Pharmaceutical Group. In response, CMS Pharmaceutical Group stated that its marketing authorization application was based on clinical data approved in the United States; however, the NMPA required additional domestic clinical trials. After careful consideration, the company ultimately decided to voluntarily withdraw its application. This decision was driven by the fact that even if the clinical trials were eventually successful, the resulting losses in time and capital would be irrecoverable.

And through these two typical cases, it is not difficult to find that,Acquisitions and distributorships of medical aesthetics products are not merely transactional; beyond the quality of the target assets, a company’s ability to empower these products is equally critical, serving as the key determinant of their ultimate market success.。

2024 Will See a Surge in Approvals for New Aesthetic Medicine Products: Innovate or Be Eliminated

When discussing the current state and future trends of the industry, a seasoned investor stated, “In the past few years, the medical aesthetics industry has undoubtedly been the hottest market trend, with vast amounts of hot money flooding into this sector. For a time,Medical aesthetics is like an all-encompassing basket that can accommodate any type of enterprise.. However, as more players enter the market and the industry’s siphon effect gradually weakens, all are beginning to face growth anxiety, with market capitalizations also undergoing a halving ordeal, which is sufficient to indicate that,China’s Medical Aesthetics Industry Is Entering the ‘Black Iron Era’ of Capability Competition’。”

How can this be seen?

First, there are changes at the level of market demand. In this regard, a head of a medical aesthetics company stated, “The medical aesthetics market, which previously attracted heavy capital investment, was primarily driven by the ability to capitalize on era-specific dividends and create scenarios that catered to consumer demand.. However, from the current perspective, this extensive development model is increasingly difficult to sustain, as consumers have become more cautious and place greater emphasis on personalized services,Therefore, market logic is no longer just about changing sales scenarios through new product replacements, but rather about creating more effective value for customers by excelling in professionalism and product quality.。”

And this is precisely the second point: the medical aesthetics market has placed higher demands on the products themselves.2024: A Banner Year for the Centralized Approval of New Medical Aesthetic Products, both the “Three Musketeers” and cross-industry pharmaceutical companies have reaped substantial rewards this year. Taking Sihuan Pharmaceutical as an example, more than ten Class III medical device products independently developed by the company, such as first-generation “baby face injections,” second-generation “girl injections,” human-derived collagen, and skin boosters for minimally invasive aesthetic procedures, are expected to receive approval and launch in the next two years. In addition, several medical aesthetic products from companies including Imeik, Huadong Medicine, Giant Biogene, and Chuangjian Medical are also poised for imminent regulatory approval and market launch this year.

Figure 5. Product Distribution of the Top 5 Medical Aesthetics Companies in China (Source: Public Information)

Figure 5. Product Distribution of the Top 5 Medical Aesthetics Companies in China (Source: Public Information)

Among this batch of new products, a clear trend is emerging: an increasing number of innovative technologies are being integrated. An investment firm deeply rooted in the medical aesthetics sector has taken note of this shift, stating, “First, recombinant collagen technology continues to gain momentum and is receiving increasing market recognition. Second, the currently high-profile “collagen+” new materials have also made progress to varying degrees. Finally, polymeric filler materials are increasingly emerging, such as PLLA, PHA, and hydroxyapatite.。”

Of course, there are also the hot topics in recent yearsSynthetic BiologyAccording to industry experts, the upstream production of raw materials in the medical aesthetics sector relies heavily on animal and plant sources or chemical compounds. This dependence not only makes large-scale production difficult and costly but also poses safety risks. In contrast, biosynthesis offers advantages such as high purity, safety, and homology, holding significant practical value for addressing the current challenges in scaling up raw material production for medical aesthetics. Once breakthroughs are achieved in technology and industrialization, it will undoubtedly unlock greater potential for the upstream segment of the medical aesthetics industry. It is precisely for this reason that numerous medical aesthetics companies, including Giant Biogene, Bloomage Biotech, and Taichuang Biotech, are continuously increasing their investments in this area.

From the perspective of the capital market,Recombinant collagen and other synthetic biomaterials are also a key focus of strategic deployment.. According to incomplete statistics from the VCBeat database, there were more than 20 investment and financing events in the medical aesthetics industry in 2023, among which those closely related to concepts such as synthetic biology and recombinant collagen accounted for one-quarter, includingTrautec Medical, ZhiTai Bio, Zhentai Bio, Liying Bioetc. This trend continued into 2024,Shengzhi Runhe, Fleming, Yiru Biotech, Junhemengand other related concept companies have also successfully secured financing.

This is not difficult to understand, after all, for the current medical aesthetics industry, it has become a consensus that growth has stalled.The industry is gradually entering an era of “too many monks, too little gruel,” making it even more critical to strengthen internal capabilities.. Of course, this largely refers to the development of specific products, namelyHow to Leverage Emerging Technologies or Materials to Enhance the Efficacy of Medical Aesthetic Products While Maintaining a Price Advantage。

This invisible “war” is quietly unfolding between traditional medical aesthetics companies and cross-industry pharmaceutical firms.

1. "The Medical Aesthetics Industry Enters the 'Black Iron Era'—Botulinum Toxin Insights";

2. “The ‘Hyaluronic Acid Queen’ Endures Growing Pains” — Cninfo WAVE;

3. “Laying Bare the Cards of Imeik, Bloomage Biotech, and Their Peers: Where Is the Next Big Trend in Medical Aesthetics?” – Jinduan.