IPO Gate Reopens: Medical Sector Sees First Light with New Filings

IPO Acceptance Resumes! Medical IPO Applications Finally Accepted!

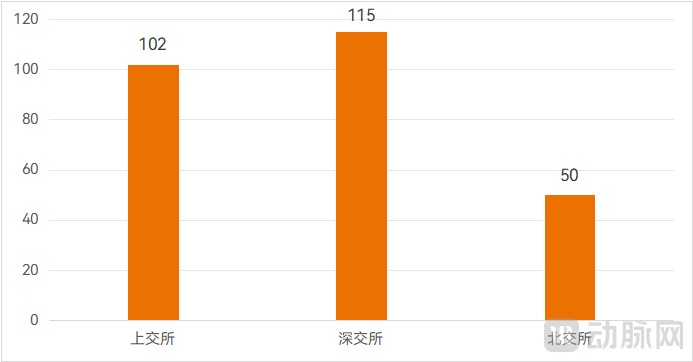

On June 20, the Shanghai and Shenzhen Stock Exchanges each accepted one new listing application; on June 21, the Beijing Stock Exchange accepted three IPO applications. This marked a six-month gap since the last acceptance of applications by the Shanghai and Shenzhen Stock Exchanges.

As of June 26, the three major stock exchanges accepted IPO applications from 17 companies within a week, with the Beijing Stock Exchange alone accepting 15, signaling clear positive momentum in the secondary market.

# IPO Application Acceptance Resumes: A One-Week Review of Companies Accepted by the Three Major Exchanges, Source: Official Websites of the Respective Exchanges

Encouragingly, healthcare companies have already emerged among the first batch of firms whose IPO applications were accepted following the resumption of IPO processing. Specifically, Ashelin’s IPO application on the Beijing Stock Exchange changed to “accepted” status on June 26. Ashelin is primarily engaged in the research and development, production, and sales of disposable medical consumables used in professional rehabilitation nursing and medical protection. The company generated RMB 575 million in revenue in 2023.

Over the past year, medical IPOs have been in a slump. Against this market backdrop, Aishelun has become the first healthcare company since 2024 to have its IPO application accepted. This milestone, achieved mid-year, could significantly boost industry confidence in IPOs.

Coincidentally, on June 26, the first dental IPO of 2024 emerged—Aidite’s listing on the ChiNext Board. It was one of the few companies to successfully go public on China’s A-share market in the first half of the year, further bolstering confidence within the industry.

Since the China Securities Regulatory Commission (CSRC) announced a phased tightening of the IPO pace in August 2023, IPO access has become increasingly stringent, with a marked slowdown in the acceptance of IPO applications and listings committee reviews. This trend continued in the first half of 2024.

Specifically in the healthcare sector, as of2024On June 26, more than 10 companies successfully went public in the first half of the year, among which only five, including Aidite and Haisheng Pharmaceutical, were listed on the A-share market.

At the same time, a large-scale wave of order cancellations emerged.

According to incomplete statistics from VCBeat,In the first half of 2024, more than 30 healthcare-related companies listed on China’s three major stock exchanges withdrew their IPO applications, resulting in the termination of regulatory reviews. These companies included star startups in the biopharmaceutical venture capital sector—backed by multiple renowned investors and extensively engaged in innovative product development—as well as established firms with years of operation and significant revenue scales.

Most companies that terminated their IPO applications had already reached the inquiry stage prior to withdrawal; based on acceptance dates, their queueing time was approximately one year. In individual cases, companies withdrew their applications even after waiting in the queue for nearly two years and being just one step away from listing.

Few New Listings, Surge in Terminations, and a Renewed Stall in Application Acceptances: Healthcare IPOs Appear to Have Hit Rock Bottom

During the period of slowed IPO pace, regulatory authorities refined rules governing issuance and listing. In April 2024, the State Council issued the “Several Opinions on Strengthening Supervision, Preventing Risks, and Promoting High-Quality Development of the Capital Market,” which called for strict control over entry thresholds for issuance and listing, further improvement of the issuance and listing system, elevation of listing standards for the Main Board and the ChiNext Board, and refinement of the evaluation criteria for the scientific and technological innovation attributes of companies listed on the STAR Market. It also emphasized enhancing the quality and effectiveness of pre-listing tutoring and expanding the coverage of on-site inspections for companies under review and their relevant intermediaries.

Subsequently, the China Securities Regulatory Commission (CSRC) and the Shanghai and Shenzhen Stock Exchanges successively issued supporting regulations, significantly raising the listing thresholds for the Main Board, the STAR Market, and the ChiNext.

Multiple healthcare investors stated that, under stricter listing requirements, the IPO paths for medical companies are primarily hindered by issues related to financial performance, growth potential, and regulatory compliance.

“Upon close examination of the key points in IPO review inquiries, regulatory authorities primarily focus on innovation and growth, addressing issues such as sector positioning, track positioning, market size, sustainability of operations, and core patented technologies,” said Yu Jianlin, Deputy General Manager of GTJA Investment. He noted another new development: regulators are placing greater emphasis on the reasonableness and compliance of promotional and selling expenses.

Of course, the IPO freeze is not limited to the healthcare sector. Data disclosed by the three major stock exchanges shows that more than 200 companies have had their reviews terminated since 2024; June saw the highest concentration, with as many as 90 companies updated to “review terminated” status as of June 25.

Number of Companies Whose Reviews Were Terminated by the Three Major Exchanges Since 2024 (as of June 25); Data Source: Official Websites of the Respective Exchanges

For healthcare companies, operations are characterized by high capital investment, long development cycles, and significant risks. During the post-launch commercialization phase, processes such as hospital listing and clinical application must be conducted in compliance with regulations, while also being closely tied to the improvement of payment systems. These industry-specific characteristics make the troughs in medical IPO activity particularly pronounced.

Meanwhile, some investors believe that the current situation is less of a “freezing point” and more a return to the calmer market conditions seen a few years ago.

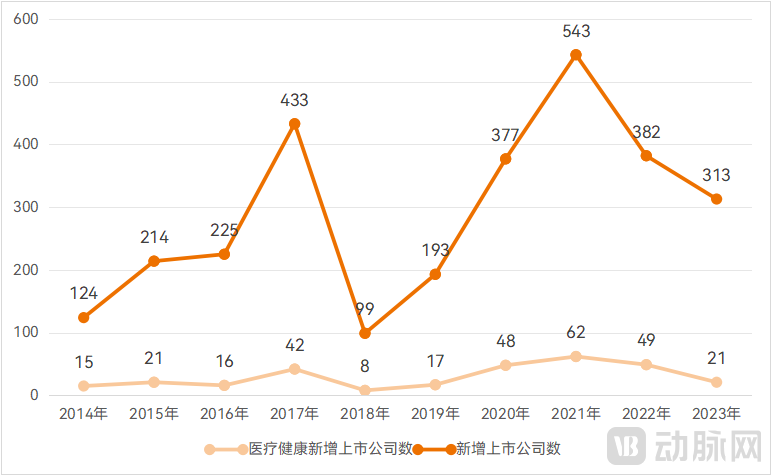

Looking at the longer timeline, it is evident that the number of newly listed companies on China’s A-share market peaked in 2021, with more than 500 listings, including over 50 in the healthcare sector. Since 2022, driven by broader platform-level shifts, both the total number of cases and those specifically in healthcare have declined rapidly.

Nevertheless, under the normalized conditions of the A-share market, initial public offerings (IPOs) in the healthcare sector have maintained a certain scale, reaching 21 companies in 2023—a figure that is not insignificant compared to the pre-2019 years characterized by normal market operations.

New Listed Companies on the A-Share Market in the Past Decade, Data Source: CSRC, Choice

A comparison between A-share data and the Hong Kong stock market reveals that the latter experienced similar fluctuations from 2019 to 2023, entering a relatively subdued phase starting in 2023.

Furthermore, with the raising of listing standards, timely withdrawal of application materials serves as a prompt loss-mitigation strategy for companies terminating their IPOs, enabling cost savings and preparation for future listing endeavors.

Overall, how should we interpret the phased downturn in IPOs of healthcare companies? There is no one-size-fits-all answer to this question; it requires a more rational perspective that takes into account industry-specific characteristics and cycles, as well as the overall conditions of the secondary market. What is certain, however, is that the recent acceptance of medical IPO applications has broken the “zero” streak seen since 2024, providing a boost of confidence to the industry.

A difficult IPO path implies blocked channels for raising capital through public listings, while the primary market also faces challenges including difficulties in corporate financing, fundraising by investment institutions, and exit strategies. In response to changes in listing standards and their cascading effects, the healthcare sector has adopted various measures to cope.

Yu Jianlin has learned that many companies are currently focusing on strengthening their internal capabilities and adjusting their business strategies. For instance, whereas companies previously strove to expand their pipelines as much as possible, there is now a growing recognition that a large and comprehensive pipeline is not necessarily meaningful. Instead, companies need to streamline and focus, retaining only those assets with genuine core clinical value. Non-core pipeline assets should be divested or deferred as appropriate, and licensed out whenever possible. “We also encourage companies to adapt their sales strategies and seize opportunities in external business development (BD), such as through patent assignments, pipeline asset licensing, collaborative development, and equity divestitures. By going global and increasing their visibility in international markets, companies can enhance their transaction opportunities.”

In terms of capital strategy, while actively diversifying financing channels, efforts should be made to extend cash flow runway. “During periods of capital bubbles, some companies, in their rush to go public, have aggressively expanded their drug pipelines and recruited executives from multinational corporations on a large scale, assembling lavish portfolios and management teams. However, when cash flow becomes tight, these high-priced executives are often the first to leave. Therefore, a pragmatic approach to hiring is essential.”

However,In any case, it is difficult for healthcare companies to avoid the interim “three-no” phenomenon—no products, no revenue, and no profits. Meanwhile, regulatory requirements across all stages, including product development, registration and market approval, and commercialization, must be strictly complied with. Under these overarching premises, medical IPOs continue to receive support from regulatory authorities.

Taking the STAR Market as an example, a number of healthcare companies have benefited from its advantages in recent years. Since the launch of the STAR Market in 2019, nearly 40 related companies have been listed on it. It is understood that companies under review for listing on the STAR Market are primarily focused on next-generation information technology and the bio-industry.

A major highlight of the STAR Market is that its fifth listing criterion allows pre-profit companies to go public. In 2024, the China Securities Regulatory Commission (CSRC) further clarified relevant matters concerning the listing of pre-profit companies on the STAR Market. The “Sixteen Measures on Capital Market Services for the High-Quality Development of Technology Enterprises,” issued in April 2024, pointed out that the financing environment for the listing of technology-based enterprises will be optimized, and high-quality pre-profit technology enterprises with key core technologies, significant market potential, and prominent scientific and technological innovation attributes will be supported in going public in accordance with laws and regulations.

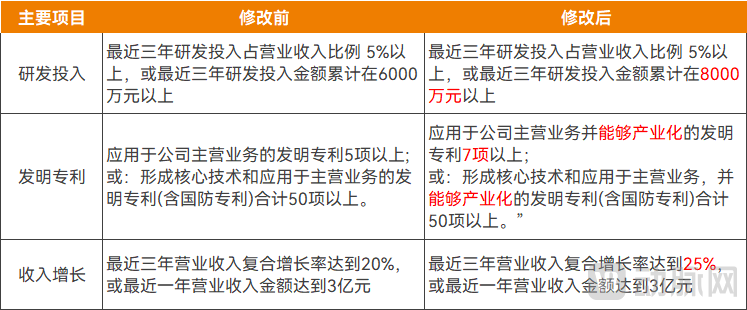

On the other hand, half a month after the aforementioned measures were issued, the “Decision on Amending the ‘Guidelines for Evaluating Sci-Tech Innovation Attributes (Trial)’” was released, raising the requirements for prospective listing companies in terms of R&D investment, the number of invention patents, and the compound annual growth rate of operating revenue.

“Guidelines for the Evaluation of Scientific and Technological Innovation Attributes (Trial)”: Key Revisions, Source: China Securities Regulatory Commission

The new guidelines adjust the cumulative R&D expenditure over the past three years from “more than RMB 60 million” to “more than RMB 80 million”; change the requirement for “five or more invention patents applied to the company’s core business” to “seven or more invention patents applied to the company’s core business and capable of industrialization”; raise the compound annual growth rate (CAGR) of operating revenue over the past three years from “20%” to “25%”; and revise the criterion for “a total of 50 or more invention patents (including national defense patents) that constitute core technologies and are applied to the core business” to “a total of 50 or more invention patents (including national defense patents) that constitute core technologies, are applied to the core business, and are capable of industrialization.”

The revised Guidelines for Evaluating Sci-Tech Innovation Attributes have strengthened key metrics measuring R&D investment, research outputs, and growth potential, thereby further guiding intermediaries to enhance the quality of applicant companies and recommend high-quality tech enterprises with truly critical core technologies for listing on the STAR Market. Meanwhile, the new evaluation guidelines emphasize “industrializability” in the application of invention patents and place particular focus on the ability of prospective listed companies to commercialize scientific and technological achievements.

Over the past decade, China’s biopharmaceutical industry has experienced rapid development. However, follow-on innovations characterized by relatively short R&D cycles, lower risks, and reduced investment have generally been more favored. To date, deficiencies persist in fundamental theories, core underlying technologies, and the accumulation of bioinformatics resources, with original innovation remaining a significant weakness. In the long term, pre-IPO companies should place greater emphasis on addressing unmet clinical needs, pursue differentiated pipeline strategies, and strive for source innovation within niche sectors.

Therefore,Higher listing standards and stricter regulation not only enhance the quality of listed companies from a performance perspective but also underscore that the fundamental support for industry innovation remains unchanged. For the IPO ecosystem, under the trend of survival of the fittest, high-quality innovative enterprises can secure more financing opportunities to achieve further development.

Looking at the overall IPO landscape, as of June 20, there were more than 400 companies undergoing IPO review across the Shanghai, Shenzhen, and Beijing stock exchanges, among which 29 had passed the listing committee’s approval and 21 had submitted for registration. The industry generally believes that the process of improving the listing system has come to a close, and IPOs may gradually return to normalcy in the future.

It can be seen that,Following the resumption of IPO application acceptance, the Beijing Stock Exchange (BSE) recorded the highest number of filings. From June 21 to June 26, new applications were accepted on each trading day, with the number reaching as high as six on June 26. The restart of IPO acceptance in the healthcare sector was also driven by the BSE.

On September 1, 2023, the “19 Measures for Deepening Reform” of the Beijing Stock Exchange (BSE) were officially released, explicitly allowing high-quality small and medium-sized enterprises (SMEs) that already meet listing requirements to conduct initial public offerings (IPOs) and list on the BSE, provided they align with the exchange’s market positioning. To date, there have been no substantive adjustments to the BSE’s listing thresholds.

Against the backdrop of generally heightened listing standards, the Beijing Stock Exchange (BSE) has emerged as a new listing option for a large number of innovative small and medium-sized enterprises (SMEs), characterized by its high inclusivity, compact and controllable timelines, and rapid review processes. VCBeat also learned in recent interviews thatThe Beijing Stock Exchange Has Become the Ideal Listing Destination for Healthcare Companies and Investors

According to statistics, a total of 30 companies have completed listing counseling this year, among which 26 plan to list on the Beijing Stock Exchange (BSE), accounting for more than 80%. VCBeat has learned that recently, the listing applications of several healthcare companies, including Aide Technology, Aishelun, and Jiachuang Biotech, have passed the counseling acceptance. Passing the counseling acceptance means that these companies can proceed with their BSE listing applications; notably, Aishelun’s IPO application has already been accepted.

In addition, Aide Technology is primarily engaged in the research and development, production, and sales of medical devices, with a focus on orthopedic consumables. Its core products include orthopedic medical consumables for spine, trauma, and sports medicine, as well as wound repair products for wound healing. According to data disclosed by Aide Technology, the company achieved operating revenue of RMB 64.55 million and net profit of RMB 16.32 million in the first quarter of 2024.

Jiachuang Bio provides cell testing and virus clearance process validation services to biopharmaceutical companies, medical institutions, and research institutes. According to the company’s disclosed information, Jiachuang Bio achieved an operating revenue of RMB 132 million and a net profit of RMB 46.62 million in 2023.

Which companies’ IPO applications will be accepted next? Will they still appear on the currently hottest Beijing Stock Exchange? These are all worth anticipating.

In any case, within the broader national context of encouraging new quality productive forces, innovative drugs, and biomanufacturing, positive changes are inevitable. While growing pains are unavoidable, practitioners can only focus on diligent efforts and patiently await the fruits of their labor.

References:

Shanghai Securities News: Over 80% of Companies That Have Passed Tutoring Inspection Plan to Launch IPOs on the Beijing Stock Exchange