Chinese Pharma Firms Aggressively Prune R&D Pipelines Amid Industry Restructuring

SPH

Pharmaceutical R&D and Manufacturing

Zai Lab

Innovative Global Biopharmaceutical Company

Bio-Thera

Innovative Drug Developer

For a pharmaceutical company, cutting pipeline assets is hardly big news. But what if a major pharma giant with annual revenues exceeding RMB 200 billion slashes seven pipeline programs within just a month and a half? That seems rather “intriguing.”

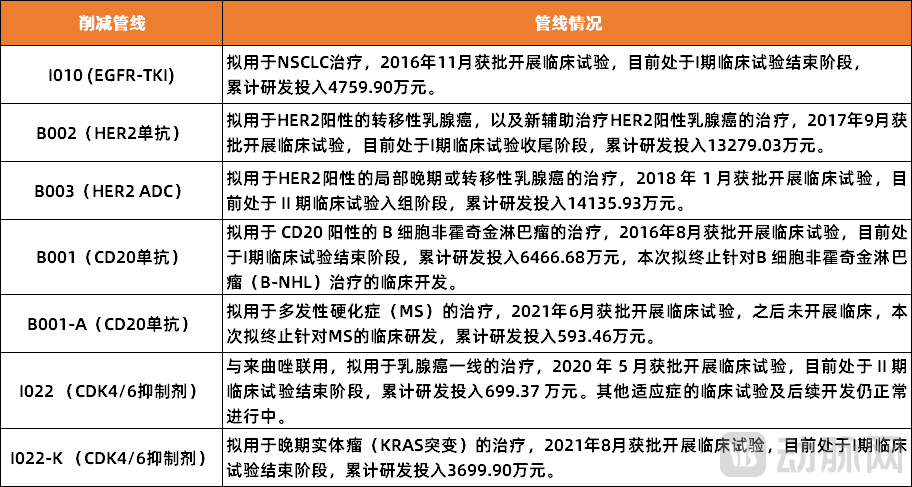

Reportedly, the pharmaceutical giant in question is Shanghai Pharmaceuticals Holding Co., Ltd. (SPH), which topped the A-share pharmaceutical sector in 2023 with RMB 260.3 billion in revenue. However, this achievement did not attract significant attention; instead, its recent successive cuts to its drug pipeline have resonated more strongly with industry insiders. On May 1, 2024, SPH decided to terminate three clinical trials and subsequent development programs; on June 8, it announced the termination of clinical trials and further development for four additional R&D projects.Within less than a month and a half, seven new drug R&D projects were consecutively terminated, involving R&D expenditures totaling RMB 437 million.。

Figure 1. Seven Pipelines Discontinued by SPH (Source: Public Information)

Figure 1. Seven Pipelines Discontinued by SPH (Source: Public Information)

This is not an isolated case; many domestic pharmaceutical companies have already scheduled pipeline cuts this year. For instance, Zai Lab has discontinued three pipelines since the fourth quarter of 2023, namely Margetuximab, Odronextamab, and BLU-945, with Margetuximab being just one step away from commercialization. Additionally, Staidson announced on March 25 the termination of four COVID-19 projects, involving R&D expenditures of RMB 383 million. Furthermore, more than 25 domestic pharmaceutical companies, including BeiGene, Huadong Medicine, TopAlliance Biosciences, Yahong Medicine, Apeloa Pharmaceutical, Tiantan Biological Products, and Walvax Biotechnology, have disclosed information regarding pipeline cuts this year. Of course, this is only the tip of the iceberg, with much more hidden beneath the surface.

Amid this wave of pipeline cuts, unlike in the past, the market offered little sarcasm and instead reached a consensus that this was a positive development, marking the maturity of China’s pharmaceutical industrySo, what is the actual situation? The answer lies in examining the specific pipelines that were cut.

China’s Quiet Wave of Pipeline Cuts Has Arrived

When it comes to discontinuing pipeline candidates, many domestic pharmaceutical companies choose to keep such decisions confidential. As a result, in most cases, one can only uncover subtle clues by comparing corporate annual reports or querying relevant databases.

However, this situation is changing, primarily because domestic pharmaceutical companies are increasingly scaling back their drug pipelines. In response, industry experts stated, “In the second half of this year, domestic large pharmaceutical companies will continue their “slimming down,” and many pipelines will be abandoned in the future.”

So, what is the underlying cause?

Let us first examine the pharmaceutical companies themselves. Over the past year or two, affected by the market downturn, the entire pharmaceutical industry has been “tightening its belt.” Layoffs and pipeline cuts have always been the two primary cost-saving measures for pharmaceutical companies; therefore, most of the discontinued pipelines lacked “economic viability.” Of course, this needs to be analyzed from multiple dimensions, includingPipeline progress falls short of expectations, lack of competitiveness in the pipeline, and uncertainty in the market size of the pipelineWait.

Specifically, take the case of pipeline progress falling short of expectations. At the end of 2023, Staidson Biopharma voluntarily terminated the Phase Ib/II clinical trial of STSG-0002 Injection, a gene therapy drug for hepatitis B. After thorough communication with the principal investigator regarding the existing clinical trial data, the company concluded that the observed preliminary efficacy data did not meet expectations. Although the study had lasted for four years and incurred costs exceeding RMB 120 million, Staidson Biopharma chose to cut its losses in a timely manner to reduce risks to subjects.

Next, let us discuss pipeline competitiveness. Taking the popular target HER2 as an example, according to incomplete statistics from PharmaCube, by the end of 2023, there were a total of 171 HER2-related pipelines either marketed or under development by Chinese pharmaceutical companies, accounting for approximately 42% of global HER2 pipelines. When further narrowed down to the ADC sector, China’s share of clinical-stage HER2 ADC pipelines has exceeded 70% of the global total. As related products continue to reach the market, many pharmaceutical companies have chosen to gracefully exit by “cutting their pipelines” in an increasingly saturated competitive environment. Typical examples include Bio-Thera, Eddingpharm, and BeiGene.

Figure 2. List of Selected Global ADC Pipelines Discontinued in 2023 (Data Source: Zhiyaoju)

Figure 2. List of Selected Global ADC Pipelines Discontinued in 2023 (Data Source: Zhiyaoju)

It is worth noting that both BAT8001 from Bio-Thera and TAA013 from TopAlliance Biosciences have reached Phase III clinical trials, yet even so, they could not escape the fate of having the emergency “brake” applied. In this regard, a pharmaceutical investor commented, “The more popular a drug pipeline is, the fiercer the competition tends to be. Therefore, if progress is slow or efficacy is suboptimal, and no new indications can be identified, proactively abandoning the project is undoubtedly a prudent decision.”。

Following this logic, GLP-1 represents another major pipeline category. In early 2023, as semaglutide propelled Novo Nordisk’s market capitalization to soaring heights and tirzepatide made substantial contributions to Eli Lilly’s valuation, enthusiasm among Chinese pharmaceutical companies for entering the GLP-1 sector was instantly ignited. To date, nearly 50 domestic firms—including Hengrui Medicine, CSPC Pharmaceutical, Innovent Biologics, Borui Medicine, Huadong Medicine, and Hansoh Pharma—have established a presence in this field. However, as the “gold rush” fervor gradually subsides, many of these companies have begun to abandon their respective GLP-1 pipelines.

For instance, Huadong Medicine announced in late 2023 that it would terminate further development of an oral small-molecule GLP-1 receptor agonist licensed from the U.S.-based vTv Therapeutics LLC. This outcome was hardly surprising. The weight-loss drug sector is fiercely contested, dominated by diabetes giants Novo Nordisk and Eli Lilly, while formidable newcomers such as Amgen are aggressively entering the market. In this highly competitive landscape, it is indeed difficult for a candidate lacking superior efficacy or safety profiles to carve out a viable path forward.

Finally, it is worth noting the market size of the drug pipeline. Since the beginning of this year, several domestic pharmaceutical companies have begun to withdraw from the R&D landscape for COVID-19 vaccine products. Typical examples include Staidson Biopharma, Walvax Biotechnology, and Kain Technology. Taking Staidson Biopharma as a prime example, in March 2024, it simultaneously terminated five clinical development programs for four COVID-19 drug candidates, with total R&D investments amounting to RMB 383 million. In fact, this has become a growing consensus. According to the “2024 Annual Review White Paper on Pharmaceutical R&D Trends” recently released by Citeline, the scale of novel coronavirus pipelines decreased by 11.2% in 2023. This is hardly surprising: as the global impact of the pandemic gradually wanes and sales of COVID-19 vaccines shrink significantly, many pharmaceutical companies have shifted from profitability to losses, forcing them to make painful cuts to limit further losses.

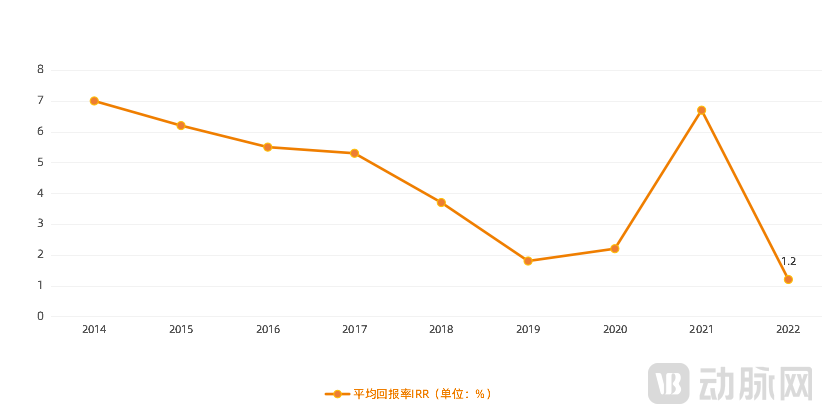

Beyond factors inherent to the pipelines themselves, industry shifts are also driving the wave of pipeline cuts among Chinese pharmaceutical companies. For instance, the return on investment for innovative drugs has declined significantly. According to Deloitte statistics, in 2022, as global new drug approvals returned to normal, the average internal rate of return (IRR) for biopharmaceutical R&D dropped to 1.2%, hitting a ten-year low. Moreover, the average cost of developing a new drug has risen to $2.284 billion. Amid increasingly tight cash flows, pharmaceutical companies are forced to confront the substantial challenge of these soaring costs.

Figure 3. Changes in the Average Return on Investment for Biopharmaceutical R&D (Source: Deloitte)

Consequently, Chinese pharmaceutical companies have shifted their R&D approach from “comprehensiveness” to “precision,” increasingly terminating low-efficiency pipelines with suboptimal prospects and concentrating more resources and efforts on their core and advantageous therapeutic areas.In response, a representative from a pharmaceutical company stated, “Leveraging advantages in capital and commercialization, large pharmaceutical companies often adopt a broad-based pipeline strategy, operating on the logic that a single blockbuster drug can offset all other costs. However, this approach has led to declining R&D efficiency among some major players, a trend that has become increasingly pronounced amid market downturns. Consequently, to ensure survival, it is becoming common practice for these companies to concentrate their internal resources on key pipelines, thereby achieving a higher return on investment.”

Global Buzz: 8 MNCs Slash 30+ Pipeline Assets in Q1

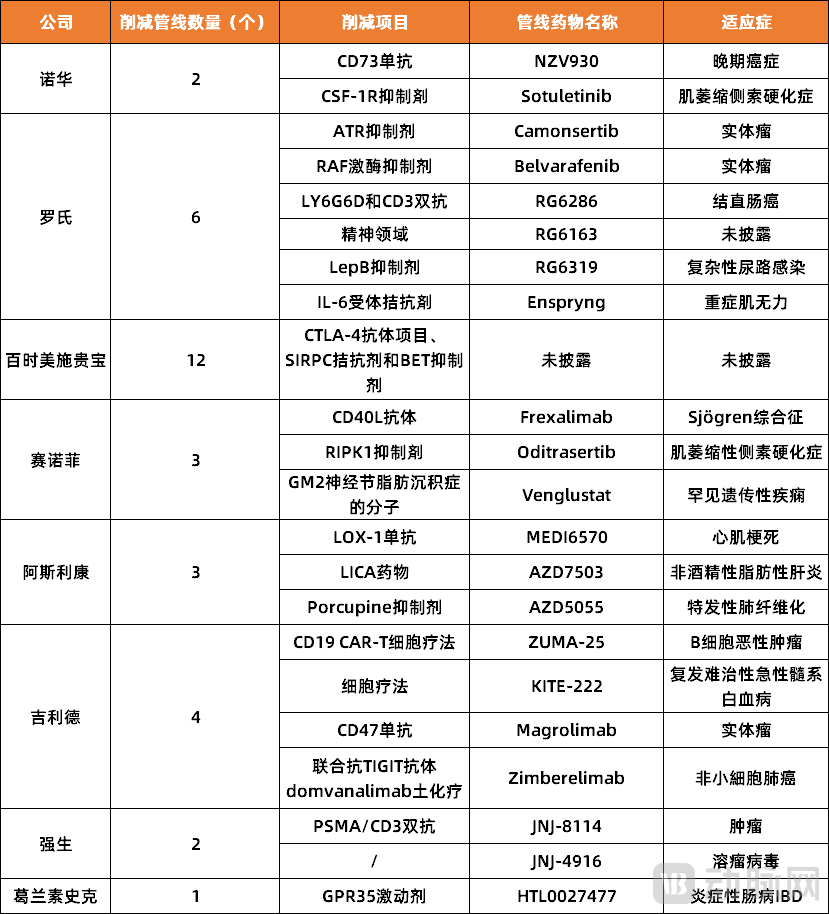

In fact, it is not only domestic pharmaceutical companies that are intensively pruning their pipelines; multinational corporations (MNCs) are also accelerating the “subtraction” of their portfolios. According to the *2024 Annual Review White Paper on Pharmaceutical R&D Trends*,A total of 3,895 candidate drugs were withdrawn from the R&D pipeline in 2023., and in the first quarter of this year, eight multinational pharmaceutical giants collectively cut more than 30 pipelines, with BMS making the most significant move by slashing approximately 12 investigational projects from its portfolio at once.

Figure 4. MNC Pipeline Reductions in Q1 2024 (Source: Public Information)

As with domestic pharmaceutical companies, the motivations for multinational corporations (MNCs) to “trim their pipelines” are twofold. First, driven by internal crises such as patent cliffs, intensifying competition in core therapeutic areas, and declining core business performance, MNCs must focus on and reinforce their competitive advantages in key therapeutic fields to safeguard future growth trajectories and stock performance. Second, against the backdrop of declining R&D returns, MNCs are eager to pursue greater certainty and higher success rates in research and development.

Certainly, as industry bellwethers, the cost-cutting measures adopted by multinational corporations (MNCs) are bound to trigger a tightening across the entire pharmaceutical supply chain. In fact, the current wave of pipeline cuts among domestic pharmaceutical companies is partly linked to this trend, as seen with BeiGene’s PD-1 and I-Mab’s CD47, among others.This is because the R&D pipelines of Chinese pharmaceutical companies are largely benchmarked against multinational corporations (MNCs); therefore, when MNCs begin to aggressively cut their pipelines, domestic companies’ pipelines inevitably suffer collateral damage.。

So, which pipelines have MNCs actually cut this year? VCBeat has selected a few typical representatives.

Let’s start with Gilead.In the first quarter of 2024, Gilead Sciences abruptly terminated ten R&D projects. Among these, the most notable was magrolimab, a CD47 antibody acquired through its $4.9 billion purchase of Forty Seven, Inc.; all six of its clinical trials were removed from the development pipeline, marking a complete abandonment of the CD47 target. In fact, CD47 antibodies had long been hailed by the industry as the next “star” target in oncology immunotherapy following PD-1/PD-L1 antibodies. However, the clinical development of magrolimab experienced significant setbacks, with both safety and efficacy failing to meet expectations.

It is reported that in terms of the complete remission rate (CRR), patients receiving the Magrolimab combination chemotherapy regimen had a numerically lower CRR of 21.3%, compared to 23.6% in the placebo plus azacitidine (AZA) group. Additionally, regarding safety, 76.4% of the 263 patients in the Magrolimab group experienced grade 3 or higher adverse events related to the study drug, whereas 56.4% of the 264 patients in the control group experienced such events. Therefore, its discontinuation was an inevitable outcome.

Looking at the domestic landscape, there have been continuous reports in the past year or two of CD47-related programs being halted. For instance, in September 2022, I-Mab announced that it had terminated its agreement with AbbVie for the joint development and commercialization of the CD47 antibody candidate lemzoparlimab, which was established in 2020. Additionally, Zai Lab also canceled the Phase II clinical trial of its CD47 monoclonal antibody, ZL-1201. Furthermore, companies such as BeiGene and Hengrui Medicine have begun to downscale or abandon their development efforts targeting CD47 antibodies.

This trend is not a fleeting whim. The primary reasons include the high difficulty of CD47 drug development, severe side effects, slow clinical progress, strategic adjustments, and failed collaborations. In this regard, experts have noted, “The expression distribution and signaling pathways of CD47 are highly complex, making it extremely challenging to balance safety and efficacy in clinical treatment. Furthermore, CD47 is also expressed on normal cells, particularly red blood cells, which adds to the complexity of its druggability.” Nevertheless, it would be unfair to dismiss all efforts in this field. Akeso’s AK117 and ImmuneOnco’s CD47-targeted therapies have both recently achieved significant milestones.

Next, let’s discuss Roche.In its Q1 2024 financial report, Roche publicly announced the discontinuation of six pipeline assets, primarily in oncology, including the ATR inhibitor camonsertib, the RAF kinase inhibitor belvarafenib, and the bispecific antibody RG6286 for colorectal cancer. This is not the first time Roche has made substantial cuts to its oncology pipeline; as early as Q3 2023, the company terminated 20% of its pipeline at once, most of which were early-stage oncology assets, including the T-cell bispecific antibody cibisatamab and the BCL-2 inhibitor Venclexta.

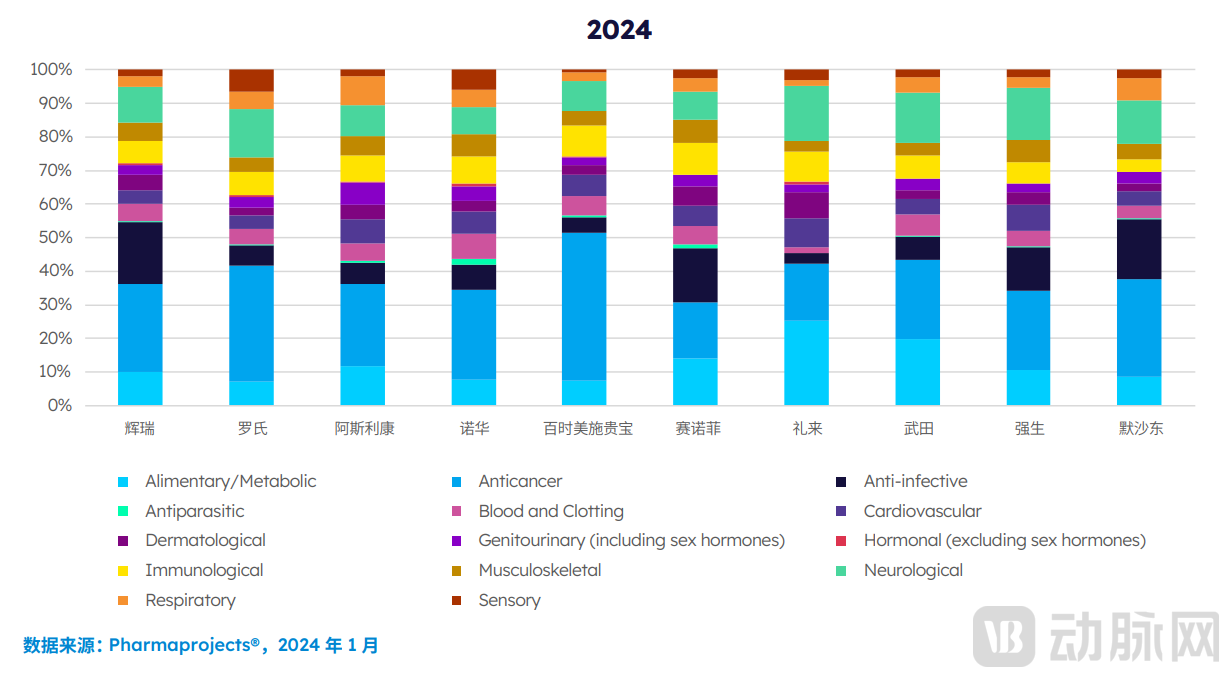

Figure 5. Therapeutic Areas of Focus for the Top 10 Global Pharmaceutical Companies (Image source: “2024 Annual Review White Paper on Pharmaceutical R&D Trends”)

Figure 5. Therapeutic Areas of Focus for the Top 10 Global Pharmaceutical Companies (Image source: “2024 Annual Review White Paper on Pharmaceutical R&D Trends”)

As is well known, oncology has long been a fiercely contested battleground for pharmaceutical giants. In Roche’s case, its oncology pipeline accounted for half of its total portfolio in 2023, and from a performance perspective, oncology remains the highest-revenue segment within Roche’s pharmaceutical business. However, in recent years, driven by patent expirations and the successive market entry of biosimilars, the “three pillars”—bevacizumab, trastuzumab, and rituximab—have been on a downward trajectory, with sales of these three products dropping by CHF 4.5 billion in 2021 alone. Consequently, as the oncology business gradually reached a bottleneck, Roche decisively opted for “streamlining,” a plan that has continued into the second half of this year.

The same trend is evident in China, where oncology pipelines are currently being streamlined. For instance, among the seven pipelines recently discontinued by Shanghai Pharmaceuticals Holding Co., Ltd. (SPH), six were oncology-related, primarily targeting indications such as breast cancer and lymphoma. In addition, several other pharmaceutical companies, including Zai Lab, Ascletis Pharma, and Yihua Pharma, have also been accelerating their withdrawal from oncology pipelines in recent years. This shift is driven mainly by two factors: first, inherent issues within the pipelines themselves; and second, considerations based on changes in the industry landscape, such as intensifying market competition, patent cliffs, and pressure on financial performance.

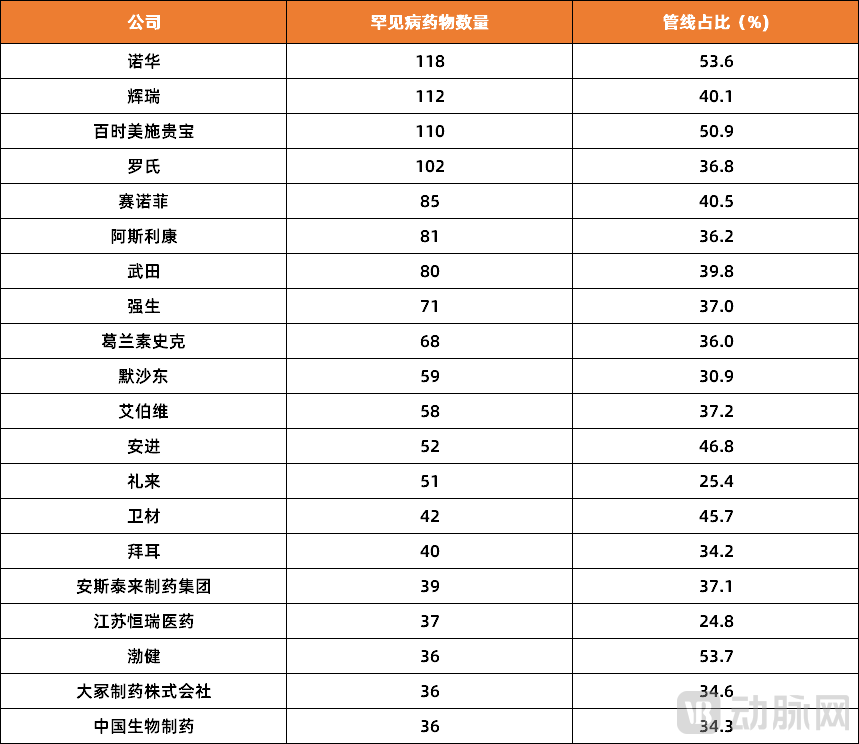

Finally, rare diseases should be mentioned.According to VCBeat, among the pipelines discontinued by eight multinational corporations (MNCs) in the first quarter, many were related to rare diseases. Examples include Sanofi’s venglustat, a molecule for treating the rare genetic disorder GM2 gangliosidosis, and oditrasertib, a RIPK1 inhibitor for treating amyotrophic lateral sclerosis (ALS), as well as Novartis’ orphan drug sotuletinib. Additionally, among the 12 pipelines abruptly terminated by Bristol Myers Squibb (BMS), some were also related to rare diseases.

Figure 6. Top 20 Pharmaceutical Companies Focused on Rare Diseases (Data Source: “2024 Annual Review White Paper on Pharmaceutical R&D Trends”)

Figure 6. Top 20 Pharmaceutical Companies Focused on Rare Diseases (Data Source: “2024 Annual Review White Paper on Pharmaceutical R&D Trends”)

Driven by the substantial profits generated from successfully developing indications for rare diseases, rare diseases have become a key focus in the pipelines of multinational corporations (MNCs) in recent years. In early 2024, the number of drugs under development for rare diseases worldwide reached 7,191, a 7.6% increase from 6,682 the previous year. Among these, Novartis, Pfizer, Bristol Myers Squibb (BMS), and Roche ranked in the top four, each with more than 100 rare disease drugs in their portfolios. However, entering this year, many MNCs have begun to streamline their rare disease pipelines, primarily because some rare diseases are too “rare,” posing significant challenges in both development and commercialization.

Domestic pharmaceutical companies are facing similar challenges. Although China has a relatively large patient population, the number of patients truly willing to pay for treatment remains low. Consequently, domestic pharmaceutical companies are currently streamlining their rare disease pipelines. For instance, in April this year, Canaan Healthcare disclosed that it had terminated its glioblastoma pipeline candidate, CAN008. Additionally, Jointown Pharmaceutical announced at the end of 2023 that it was halting the development of two rare disease pipeline candidates.

Therefore, looking back,MNCs streamline their pipelines primarily under the overarching premise of "cost reduction and efficiency enhancement," before evaluating the market certainty of specific assets, considering factors such as R&D complexity, pipeline competitiveness, and future returns.. Their every move will, to a certain extent, influence the progress of drug pipelines at domestic pharmaceutical companies.

Cutting Pipeline Programs Is Not Necessarily a Bad Thing

Regarding pipeline cuts, most Chinese pharmaceutical companies choose to remain silent, primarily because the market tends to view this as a “failure,” leading to a corresponding decline in their stock prices.

However, this is not absolute. As market conditions evolve, discontinuing pipelines with unfavorable prospects to cut losses in a timely manner, and redirecting more resources toward core pipelines or those with greater market potential, may well be a sound strategy. In this regard, industry insiders have pointed out thatBehind the Intensive Pipeline Cuts May Lie the Dawn of a New Era for Domestic Drug Innovation and R&D。

On one hand, it demonstrates that domestic pharmaceutical companies are gradually entering the deep-water zone of innovation.Currently, domestic pharmaceutical companies are making significant adjustments to their R&D pipelines. This is primarily because the probability of late-stage clinical failure for drugs targeting novel mechanisms or new indications is far higher than that for me-too products. Research on the mechanisms of action for novel targets remains relatively scarce, and there is a lack of referenceable clinical development pathways.On the other hand, it indicates that the entry barriers for certain pipelines are rising., for instance, the successful launch of DS-8201 has disrupted the entire landscape of HER2-positive tumor therapy, further intensifying market competition.

Of course, pipeline cuts do not mean that domestic pharmaceutical companies are left idle. In fact,While Domestic Pharmaceutical Companies Are Cutting Their Pipelines, They Are Also Actively Embracing MNCs, in exchange for a higher success rate in research and development, which is pushing the competition in innovative drugs to a new height.

1. “$20 Billion Pharma Giant Slashes Pipeline” – Archimedes Biotech;

2. “The Wave of Domestic Pipeline Cuts Has Arrived” – Dengling Society;

3. “As Pipeline Cuts Become Routine for Big Pharma, Competition in Innovative Drugs Reaches New Heights” — Amino Observation.