Struggling Medical IT Firms Seek Revival Amid Sub-$10B Market Caps and New IPO Filings

The annual reports released some time ago showed that the medical IT industry performed better than expected.

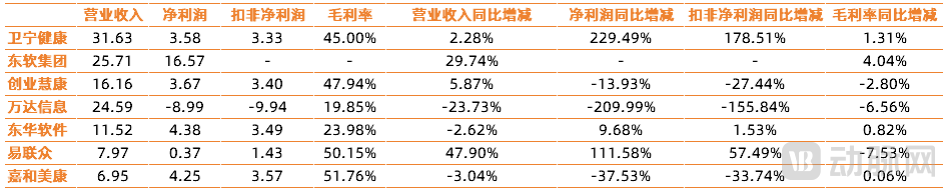

Amid cost-cutting and efficiency-enhancing measures, the revenues of three leading IT enterprises—Winning Health Technology Group Co.,Ltd., Neusoft (medical business segment), and B-Soft Co., Ltd.—continued to rise. Although DHC Software Co.,Ltd. and Goodwill E-health Info Co.,Ltd. did not achieve growth, their revenue declines remained within 3%. YLZ Information Technology Co.,Ltd., which had suffered losses for several consecutive years, achieved simultaneous growth in both revenue and profit in 2023, marking its first return to profitability since being designated as “ST” (Special Treatment).

In terms of gross profit margin, the fluctuations for all enterprises remained within single-digit percentages. The downward economic trend and the industry-wide anti-corruption campaign in the healthcare sector that swept through last year appear to have had no impact on business operations.

2023 Annual Report Data (Note: Neusoft only collected data from its healthcare segment)

However, the secondary market seems unwilling to pay for such data.

The surge in digitalization demand triggered by the COVID-19 pandemic once drove a rally in the medical IT sector. However, since the first quarter of 2023, stock prices across the entire medical IT industry have remained in a downward trend.

As of press time, the market capitalizations of most companies have fallen back below RMB 10 billion, with only Winning Health Technology Group Co.,Ltd. retaining a valuation above this threshold, though it remains less than half of its peak in 2020.

The chill continues to spread.

Many attribute the current state of medical IT to a limited market size.

The market perceives that although smart healthcare initiatives under the 14th Five-Year Plan and the development of close-knit county-level medical communities, as outlined in the "Guiding Opinions on Comprehensively Promoting the Construction of Close-Knit County-Level Medical Communities," have provided incremental growth for the industry, these projects are evenly distributed across individual years, with their corresponding value already reflected in stock prices. As the macroeconomic environment deteriorates, hospitals and public health institutions are reducing their budgets for informatization construction, leading to a decline in the market share that healthcare IT companies can secure.

However, what they overlook is that investments in logistics, hospital administration, data centers, and clinical quality control, while appearing as costs, actually generate indirect benefits for hospital operations, management, business performance, and scientific research, thereby driving hospitals to pursue more in-depth informatization.

In the era of big data, the benefits brought by such information infrastructure are even more pronounced. Across the ocean, Cerner has seen its market capitalization exceed RMB 200 billion thanks to this wave of digital transformation, with a growth momentum that has remained unabated for a decade. China’s healthcare informatization industry provides similar services; facing a potential customer base several times larger, the domestic healthcare IT sector naturally possesses equivalent room for growth.

However, the current medical IT industry does face certain issues, not at the macro level, but at the micro level.

Liu Zhan (pseudonym) once served as Deputy General Manager at a medical IT startup,He believes that China's medical IT industry is overly reliant on policy.

“Corporate business operations always align with hospital needs: we deliver what hospitals require. Hospitals, in turn, follow policy directives, procuring whatever the policies mandate. Under such an incentive mechanism, companies need only focus on how to meet the prescribed standards more efficiently and cost-effectively.”

Therefore, even if companies incur higher costs to develop products with more comprehensive features and richer content, hospitals are rarely willing to pay for these extra efforts unless they address hard demands that deliver genuine value.

The interplay between the two has yielded two somewhat negative outcomes.

On the one hand, healthcare IT products are becoming increasingly homogeneous, making it difficult for hospitals to accurately select solutions based on value assessment. Consequently, a “relationship network” driven by factors such as geography, brand recognition, influence, and interpersonal connections has emerged to fill this void.

On the other hand, hospitals are not particularly concerned with product innovation in the medical IT sector. After all, many new solutions merely represent incremental innovations built upon existing ones, and the value of most such innovations is quite limited, insufficient to persuade hospital administrators to replace their current products.

Liu Zhan told VCBeat, “Many IT vendors like to use the term ‘new generation’ to showcase the advanced nature of their systems, such as next-generation HIS systems and next-generation data centers. In reality, while these systems are indeed undergoing upgrades and iterations, there is no clear definition of what constitutes ‘new’ in the context of HIS. The vast majority of so-called ‘next-generation’ solutions lack epoch-making innovative significance. In other words, this innovation has failed to create new markets.”

Secondly, the continued poor circulation of medical data has strengthened the market dominance of leading enterprises, thereby hindering the entry of emerging players.

In practice, when startups leverage intelligent tools such as deep learning and adaptive learning to develop application products, they are constrained by privacy and security concerns, which prevent them from accessing the vast amounts of high-quality data stored in hospitals. Consequently, they can only obtain data in small batches through collaborations, resulting in high data governance costs.

The establishment of the National Data Bureau in early 2023 raised hopes for the standardization and even circulation of medical data, but a year and a half later, no new guidelines have been issued to direct the healthcare sector.

Looking back at the explosion of the medical big data industry, many investors flocked to the market after heavily betting on the future value of medical data. However, the current exodus of numerous Series A and B companies indicates that there is still a considerable distance to go before turning the envisioned potential of medical big data into reality.

Finally, the entry of the three major telecom operators has intensified industry competition to some extent.At this year’s CHINC conference, an executive from a publicly listed company lamented the current landscape, noting that in 2023, telecom operators secured numerous contracts previously dominated by healthcare IT firms, only to subcontract portions of these awards back to the healthcare IT companies.

Under these circumstances, while the number of orders secured by medical IT companies did not decline significantly, their actual revenue has indeed decreased substantially.

Under the suppressive effect of multiple factors, enterprises are exhausted from coping with market issues, lacking in innovation and competitiveness, and thus have little capacity left to achieve breakthroughs.

The “Internet + Healthcare” policy and the electronic grading policy issued by the State Council in the second half of 2018 drove the stock prices of health IT companies to high levels. Since then, market expectations for this sector have remained overvalued; the rapid surge witnessed at that time has been matched by an equally severe decline in recent years.

However, there is still a turning point here.

As the core support for hospital operations, medical IT may not easily generate disruptive innovation, but it is not devoid of innovation. In fact, this industry is undergoing a dual transformation driven by new markets and new technologies.

First, Let's Discuss the New Market. As a critical component of Digital China’s “2+8 system,” healthcare informatization is vital to national strategic security and public health safety; however, it remains a sector with relatively low penetration of information technology application innovation (Xinchuang).

Document No. 79 issued by the State-owned Assets Supervision and Administration Commission (SASAC) indicates that all central and state-owned enterprises must achieve 100% replacement of their office automation (OA) systems with indigenous innovation-based solutions by 2027. The transaction volumes from bidding processes were RMB 180 million in 2020 and RMB 358 million in 2021, surging directly to RMB 3.191 billion in 2022.

By 2024, tenders for IT application innovation in the healthcare sector experienced explosive growth. On April 18, medical institutions in Fuzhou released a project for IT application innovation-related informatization and equipment construction, with an amount reaching RMB 190 million, setting a new historical record. In May, two additional major contracts worth over RMB 100 million each were announced, issued by Wuhan Yangluo Central Hospital and Shanghai Ninth People’s Hospital, respectively. According to incomplete statistics from VCBeat, the total value of publicly disclosed procurement demands for IT application innovation and informatization across various regional healthcare systems in China approached RMB 700 million in the first five months of 2024 alone.

However, it is not easy for medical IT companies to transition into the Xinchuang (information technology application innovation) sector.

To date, products based on the C/S architecture still account for over 90% of the installed base. These legacy systems pose the primary challenge to replacing workstations in production environments during the next phase of China’s IT application innovation (Xinchuang) initiative. Furthermore, as traditional architectures rely more heavily on databases to execute business logic, enterprises must also address database compatibility issues within foundational software on a case-by-case basis.

Furthermore, the complex network architecture of hospitals also poses challenges to the entry of information technology application innovation (Xinchuang) initiatives. Following previous efforts to build smart hospitals characterized by 4G/5G convergence, the Internet of Everything, and multi-network integration, the boundaries between most internal and external networks at Xiyuan Hospital have become increasingly blurred. Amidst new demands driven by group-based operations, medical consortia, and "Internet+" models, it is difficult for enterprises to clearly distinguish which medical applications should remain within the hospital premises and which should be extended to external environments.

Data migration risks also constitute a significant challenge during the adaptation and integration of Xinchuang (information technology application innovation) products. During data migration, issues such as incompatible data formats, data loss, and data errors may arise, potentially even leading to the paralysis of legacy systems. Therefore, ensuring the reliability and security of data migration remains a key difficulty in the process of adapting domestic Xinchuang solutions.

Overall, healthcare IT innovation is a systematic engineering endeavor that requires the joint participation and coordinated efforts of the government, domestic ICT infrastructure providers, leading medical software enterprises, and industry experts. Furthermore, considering the breadth and complexity of healthcare scenarios, it is essential to address challenges progressively—from easy to difficult—by tackling key technical hurdles such as databases, operating systems, browsers, peripheral device drivers, and medical equipment integration, thereby driving the deepening and evolution of healthcare IT innovation.

Therefore, healthcare IT companies must shift their mindset when transitioning to the Xinchuang (Information Technology Application Innovation) ecosystem, viewing replacement and adaptation as the beginning of a long-term endeavor. In the long run, ensuring stable operations post-deployment—thereby reducing the difficulty and cost of operations and maintenance—is the shared goal and fundamental concern of both healthcare institutions and application vendors.

Revisiting New Technologies. As a cutting-edge technology in high demand across the entire industry, large models are most likely to first take root in healthcare IT upon entering the medical field.

As a cutting-edge technology in high demand across the industry, large models are most likely to first take root in healthcare IT upon entering the medical field.

Medicine is a rigorous discipline, and any decision made by physicians during diagnosis and treatment must adhere to the principles of evidence-based practice. Consequently, the development of large model applications in healthcare cannot proceed with the same flexibility seen in industries such as design, finance, and manufacturing. Therefore, most large models currently deployed in the medical informatics sector remain distant from direct clinical diagnosis and treatment. Instead, they focus on facilitating the flow of medical data, aiming to enhance the quality and efficiency of hospital operations, or on uncovering latent correlations within data to unlock the value of big data.

At the academic exchange conference on “Integrating Intelligence, Strengthening Quality, and Facilitating Development: Smart Hospitals Supporting the High-Quality Development of Public Hospitals,” convened by the Hospital Management Institute of the National Health Commission in May, hospital administrators and industry professionals revisited the issue of high-level electronic medical records, incorporating the capabilities of large language models into their considerations.

“Although earlier NLP techniques based on rules or statistical methods enhanced AI’s analytical capabilities, they did not break away from the logic of ‘input information – associated database – search results.’ This reasoning approach considers only the ‘preceding context’ while ignoring the ‘subsequent context.’ In contrast, physicians’ diagnostic reasoning not only incorporates data from various reports but also infers possibilities beyond the data based on prior experience. Therefore, quality control implemented via NLP does not constitute true connotative quality control,” said Wu Di, CEO of Fuxin Kechuang, in an interview.

“A basic example is that if gynecological medications are prescribed to a male patient, such an obvious error can be easily detected by NLP during subsequent reviews. However, there are more subtle and difficult-to-detect issues. For instance, within specific ethnic groups or geographic regions, unusual or atypical disease patterns or physiological characteristics may emerge. If there is a lack of prior understanding of such scenarios, or if relevant rules fail to cover these cases—or even fail to raise the appropriate questions for investigation—the intrinsic quality monitoring mechanism will be unable to effectively identify these problems.”

Therefore, such capabilities are particularly valuable to healthcare IT companies. After all, this technology is expected to unlock a new multi-billion-dollar market for high-level electronic medical record (EMR) system grading, thereby reshaping the existing landscape of the healthcare IT industry.

Beyond information technology application innovation and large language models, numerous healthcare IT enterprises are exploring new scenarios and technologies along their own distinct paths. Some are extending their traditional business lines, while others have expanded beyond the healthcare sector, continually demonstrating their innovation and profitability to the broader market.

Within a limited timeframe, it is difficult to determine who will ultimately prevail amidst the ongoing transformation. However, it is foreseeable that as healthcare institutions deepen their understanding of informatization development and the pressure from intense industry competition is alleviated, the medical IT sector will undoubtedly witness a new wave of innovation, with its valuation returning to its intrinsic value.