2024 Big Health Industry Marketing White Paper: Insights from 30 Enterprise Interviews and Over 3,000 Consumer Surveys Reveal New Opportunities for Brand Conversion

Since the release of *Healthy China 2030* in 2016, the focus on health has gradually shifted from “disease treatment” to “disease prevention,” giving rise to a comprehensive “big health” sector that covers the entire lifecycle of prevention, diagnosis, treatment, and rehabilitation.

On one hand, the expanding market offers significant potential for growth; on the other hand, as centralized volume-based procurement continues to advance, an increasing number of non-winning products are losing their share in the hospital market and facing unprecedented challenges. Meanwhile, with the online circulation of prescriptions and further policy support for online reimbursement through basic medical insurance, the out-of-hospital retail market—particularly the online segment—is becoming increasingly important.

Based on research involving nearly 30 health and wellness companies, analysis of leading social media platforms, interviews with more than 10 expert physicians, and review of over 3,000 consumer surveys, we have produced the “2024 Health and Wellness Industry Marketing White Paper,”Analyze the Current State of Marketing in the Big Health Industry, Focus on the Development Opportunities of Social Media Platforms as Emerging Marketing Channels, and Seize Future Trends.

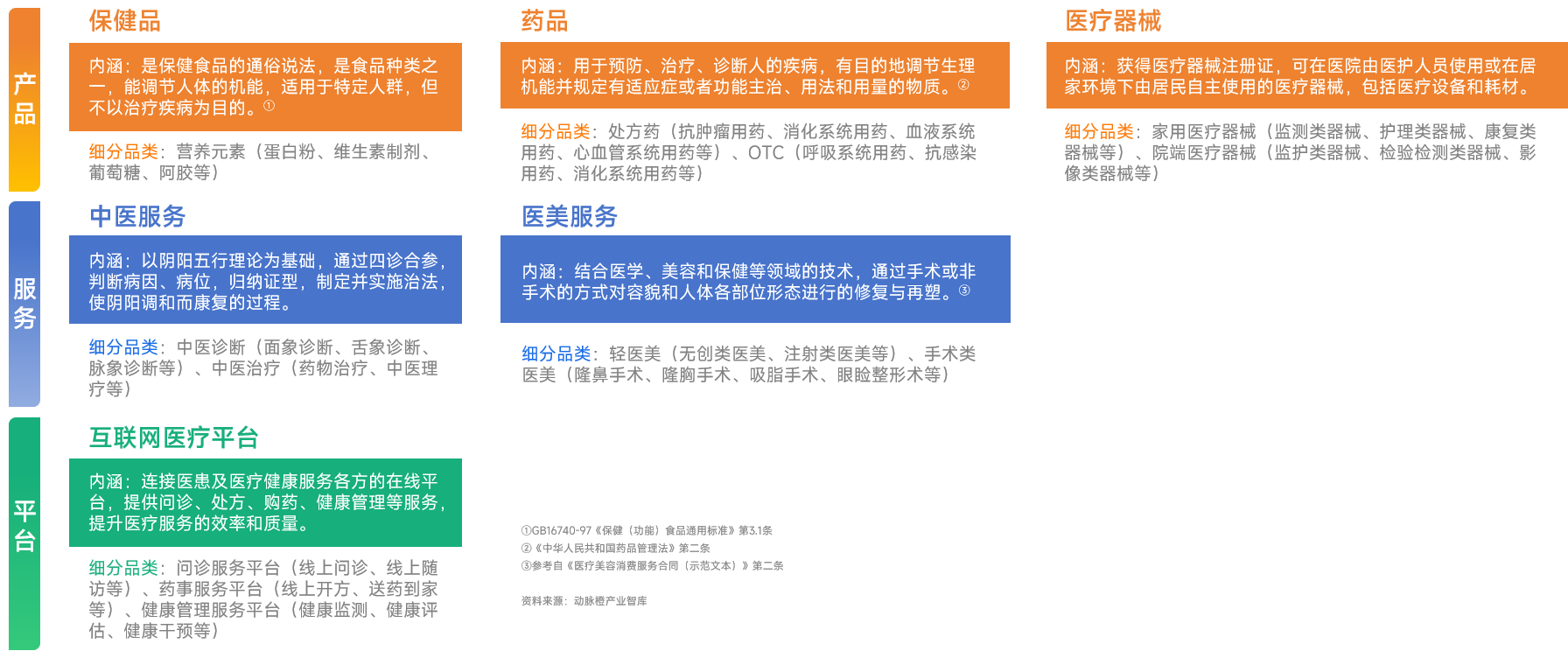

This study focuses on six sub-sectors across three major segments: health products (health supplements, pharmaceuticals, and medical devices), health services (traditional Chinese medicine services and medical aesthetics services), and internet healthcare platforms.

Sectors and Sub-segments of the Big Health Industry, Source: VBInsight

Frequent Policy Releases Strengthen the “Prevention and Healthcare First” Mindset, Driving the Growth of the Trillion-Yuan Big Health Market.

Since the release of the “Healthy China 2030” Planning Outline in 2016, the state has continuously emphasized the importance of “prevention,” shifting the focus from disease treatment to preventive healthcare, and has made numerous related decisions and deployments. From 2015 to 2020, average life expectancy increased from 76.34 years to 77.93 years, with major health indicators ranking among the forefront of upper-middle-income countries.

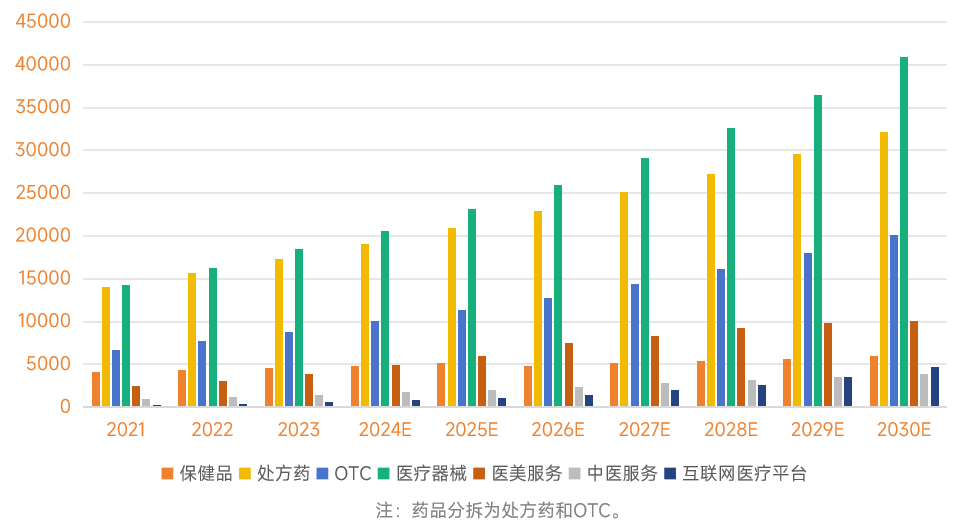

According to data released by the National Bureau of Statistics, China’s per capita expenditure on healthcare consumption reached 2,460 yuan in 2023, a year-on-year increase of 16%. In terms of market size across six subsectors, medical devices, prescription drugs, and over-the-counter (OTC) medicines ranked as the top three.

Market Size of Six Sub-sectors (2021-2030) (RMB 100 Million), Data Source: VBInsight

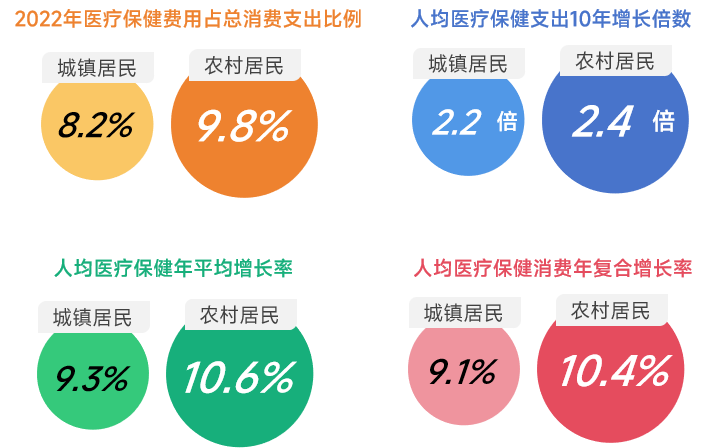

Growing health awareness and rising healthcare expenditures among the general public are expanding the market size of the broader health industry.

Data from the National Bureau of Statistics shows that living standards in China have been continuously improving, with per capita annual consumer expenditure rising year by year. Over the past decade, consumer spending among urban residents has increased to 1.6 times its previous level, while that of rural residents has grown to 2.2 times. The pandemic has significantly shifted public perceptions of disease and health, accelerating the formation and development of a nationwide awareness of holistic health.

As national health awareness has strengthened, per capita healthcare expenditure among urban residents has grown at an average annual rate of 9.3% over the past decade, reaching 2.2 times its initial level, while that of rural residents has increased at an average annual rate of 10.6%, reaching 2.4 times its initial level. The continuously rising healthcare spending by residents is gradually expanding the domestic market size of the broader health industry.

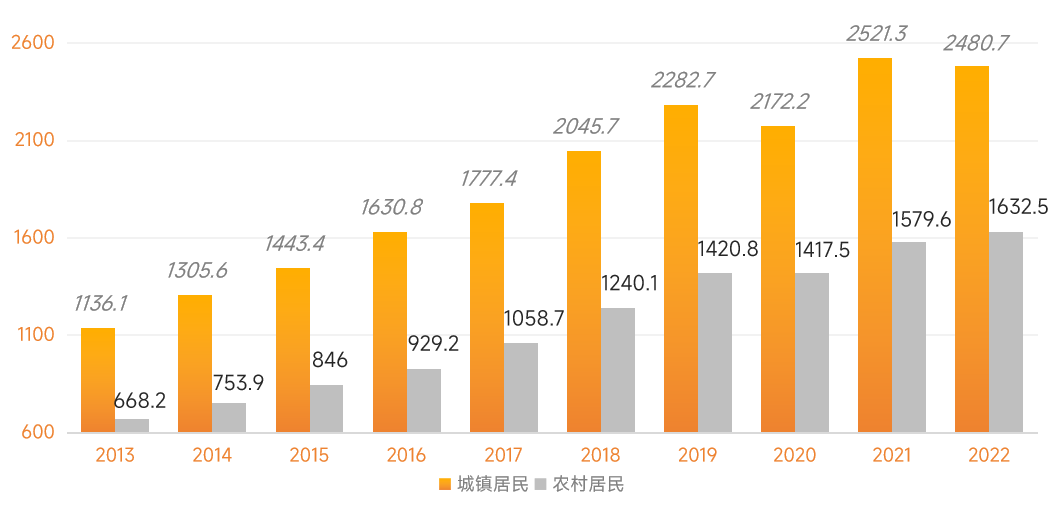

Growth in Per Capita Healthcare Consumption of Chinese Residents, 2013–2022. Data Source: National Bureau of Statistics, VBInsight

Per Capita Annual Healthcare Consumption Expenditure of Chinese Residents (2013–2022) (CNY), Data Source: National Bureau of Statistics, VBInsight

Per Capita Annual Healthcare Consumption Expenditure of Chinese Residents (2013–2022) (CNY), Data Source: National Bureau of Statistics, VBInsight

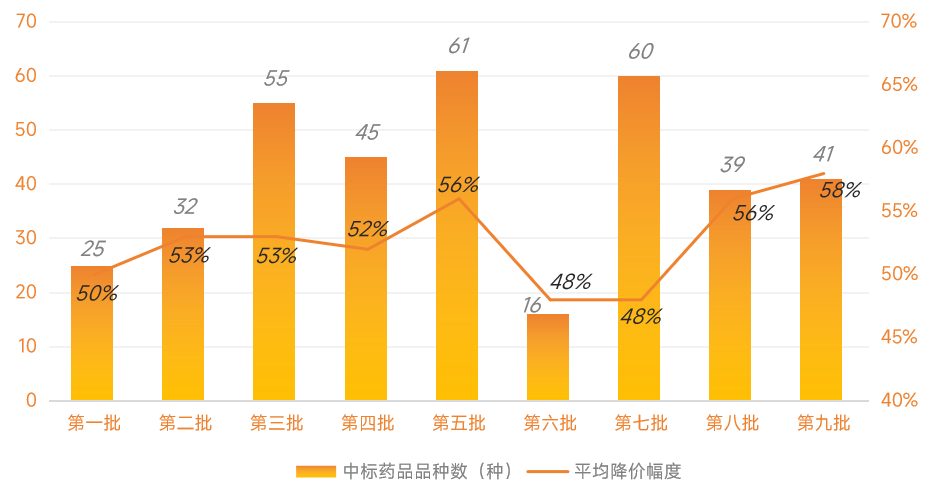

The Continuously Improving Centralized Procurement System Accelerates Competition and Promotes Industrial Optimization.

In recent years, the Chinese government has continuously intensified centralized volume-based procurement (VBP) of pharmaceuticals and high-value medical consumables, leading to substantial price reductions and providing clinical practice with a wide array of affordable, high-quality drugs and medical devices. Taking pharmaceuticals as an example, during the 2024 "Two Sessions," the *Report on the Work of the Government for 2024* highlighted that the national centralized drug procurement system emphasizes both "volume" and "quality." Currently, national-level drug procurement covers nearly 400 medications. Regarding "quality," in addition to ensuring the inherent quality of the drugs themselves, the National Healthcare Security Administration has organized multiple Grade A tertiary hospitals to conduct real-world studies on VBP-selected drugs. The published results indicate that the clinical efficacy and safety of generic drugs selected through VBP are comparable to those of originator drugs.

Centralized procurement has ended the era when companies could “reap easy profits for 20 years” with a single product, spurring continuous innovation, the delivery of more competitive products and services, and driving transformation in the broader health industry.

Overview of the Nine Batches of National Centralized Drug Procurement; Data Source: VBInsight

Current Distribution of the Industry Chain: Health products have entered the top tier, health services are actively breaking through the dilemma of homogenization, and service platforms are continuously expanding their scope of services.

In the upstream segment of the big health product industry, market competition has stabilized through natural selection, with market share increasingly concentrated among leading enterprises that hold significant competitive advantages. In the midstream segment, domestic manufacturers have leveraged innovation to overtake competitors and capture market share; by combining this with localized service advantages, some Chinese companies have ascended into the top tier. In the downstream segment, online channels demonstrate clear advantages, with their sales proportion steadily expanding. In 2021, the total sales volume of pharmaceutical e-commerce enterprises directly reporting data reached RMB 216.2 billion, accounting for 8.3% of the total national pharmaceutical sales market.

Against the backdrop of digital development in the upstream sector of the broader health industry, medical service and medical product companies are actively embracing digital transformation, exploring internet-based online business models. In the midstream of the broader health platform ecosystem, online consultation, pharmaceutical e-commerce, and health management represent the three mainstream types of health service platforms. Various platforms are expanding their service scopes, increasingly incorporating each other’s offerings, leading to greater homogenization.

Current Status and Structure of the Big Health Industry Chain, Image Source: Public Information

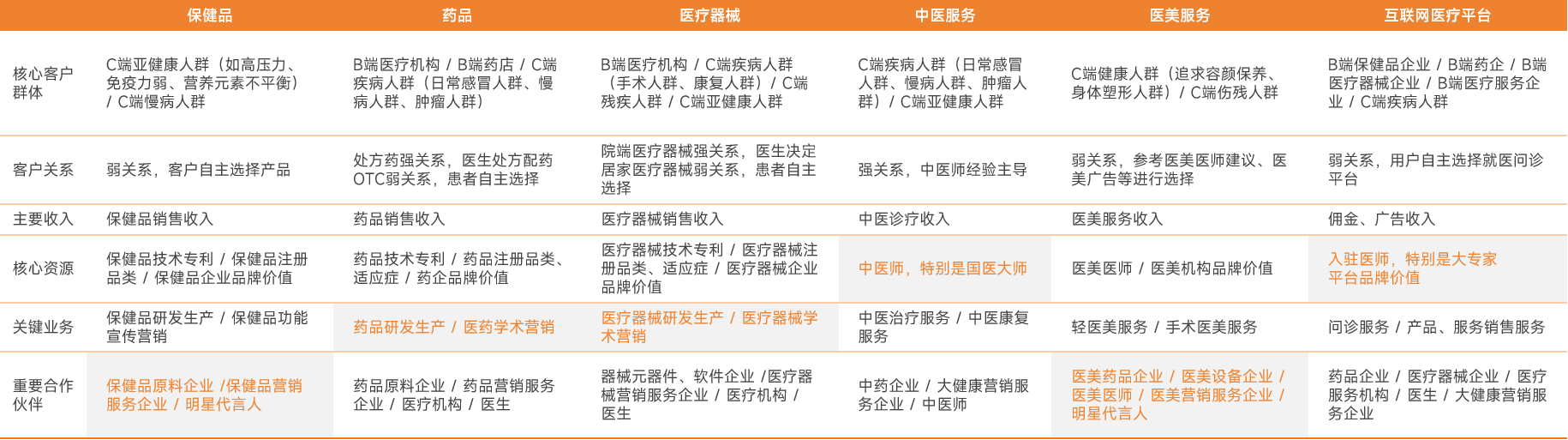

Business Model: Consumer-oriented products/services prioritize collaborative promotions with intellectual property (IP) figures such as celebrities, while medically-oriented products/services rely more on professional endorsements from leading medical experts.

Health supplements provide dietary nutrients to individuals in a sub-health state, helping to improve immunity. Medical aesthetics services are primarily consumer-oriented, focusing on anti-aging and body contouring. Both categories exhibit strong consumer attributes, offering customers considerable autonomy in their choices. Therefore, in the marketing of health supplements and medical aesthetics, celebrity endorsements significantly influence consumers’ brand preferences and can more effectively drive purchasing decisions.

Pharmaceuticals and medical devices are primarily used for the diagnosis, treatment, and rehabilitation of diseases. Given their strong medical attributes, the use of these products must be based on professional medical advice. Consequently, physicians’ choices significantly influence sales. Academic conferences serve as a key channel for pharmaceutical and medical device companies to promote their products. Currently, major manufacturers are actively organizing numerous academic conferences, inviting physicians from leading hospitals to attend, where they present the latest technologies and products to influence prescribing and usage decisions.

Analysis of Business Models in Six Subsectors, Data Source: VBInsight

As the supply side of the health and wellness industry undergoes changes, the demand side is also exhibiting new characteristics. The following conclusions are drawn from an analysis of over 3,000 consumer surveys.

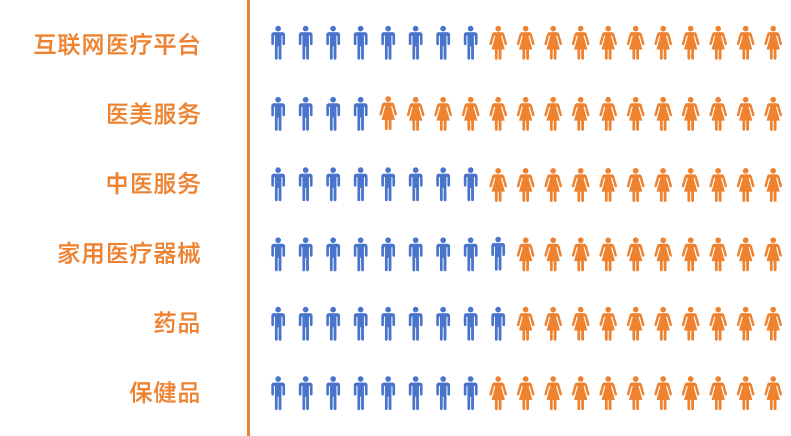

Gender Distribution of B2C Respondents Across Sub-sectors, Source: Questionnaire Survey

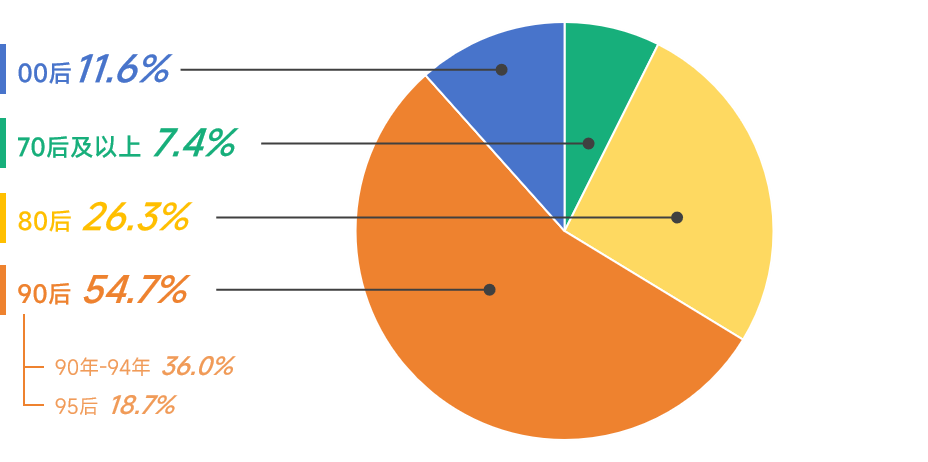

User Profile: Individuals born in the 1990s are the primary seekers of health information, with females outnumbering males.

The male-to-female ratio of users searching for health-related information on social media platforms is 4:6. Among respondents targeted through health keyword search histories, 54.7% were born in the 1990s, representing the largest proportion and constituting the primary group for health information searches; of these, 36.0% were born between 1990 and 1994.

Distribution of Age Groups Among Consumer Respondents, Data Source: Questionnaire Survey

User Profile: The Rise of the “He” Economy—High-Income Individuals Are More Willing to Pay for Products and Services.

Surveys covering health supplements, home medical devices, and medical aesthetics services reveal that men are more susceptible to product recommendations and thus more likely to make purchasing decisions. While health and wellness marketing has habitually focused on female consumers, the male demographic warrants greater marketing attention.

Scoring of Susceptibility to Product Recommendations Among Male and Female Respondents, Data Source: Questionnaire Survey

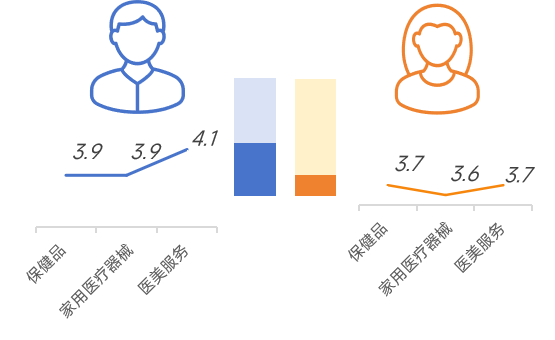

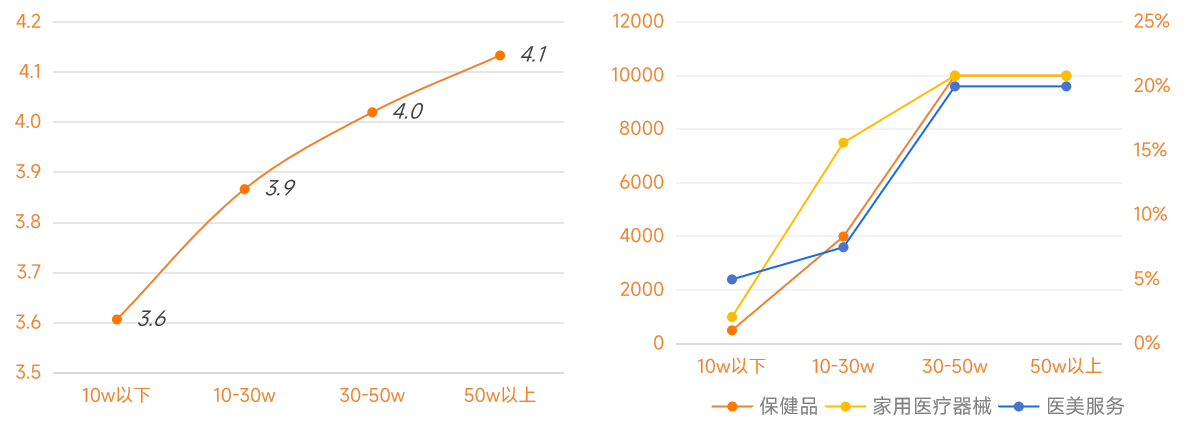

A survey covering health supplements, medical aesthetics services, and home-use medical devices reveals that as income rises, respondents are more likely to be influenced by product recommendations in their purchasing decisions, and the average annual expenditure in the broader health sector also increases.

Average Susceptibility to Product Recommendations by Annual Income Level and Median of the Most Common Annual Spending Range Among Respondents; Data Source: Survey

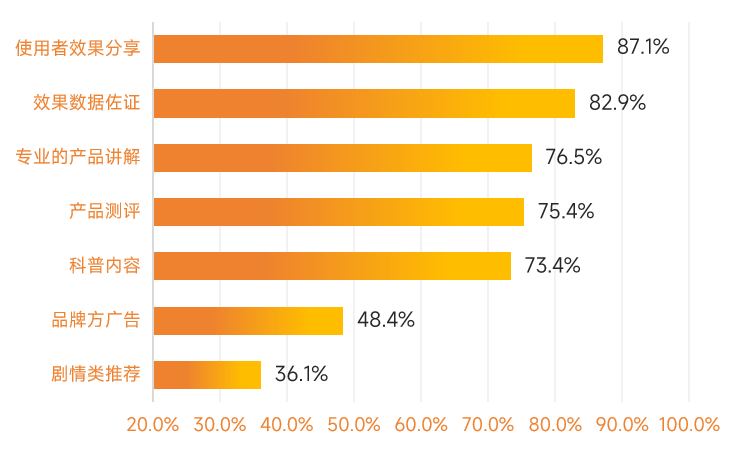

Content Preference: Explanations by leading influencers, KOLs, and medical experts, along with product reviews, are more likely to garner high user trust.

An increasing number of experts are incorporating real medical records and case studies into their science communication content, making specialized knowledge more accessible and providing multidimensional evidence to support professional viewpoints. Enterprises have also demonstrated significant attention to this type of content; for instance, medical aesthetic institutions are diversifying their marketing collaborations with influencers through initiatives such as inviting them for clinic visits and producing series that document post-procedure experiences and track treatment outcomes.

Percentage of Respondents Who Trust and Make Consumption Decisions Based on Various Types of Content, Data Source: Questionnaire Survey

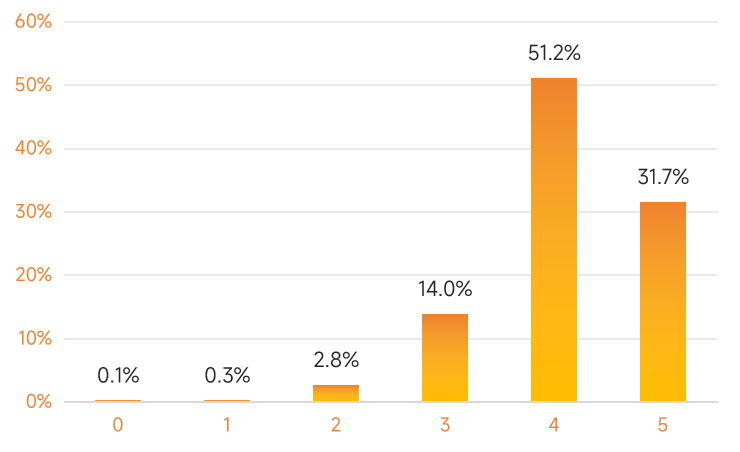

Decision Basis: Social media platforms serve as a critical source of information for consumer decision-making and are also a key channel for enterprises to launch and promote new products.

82.9% of respondents indicated that social media platforms serve as a critical source of information in their healthcare and wellness consumption decisions. Characterized by convenience and strong interactivity, social media platforms are reshaping consumer habits, leading to growing reliance on them. As technology advances, platform algorithms will become increasingly precise, complemented by continuously innovative marketing formats, thereby enabling more efficient and effective connections between enterprises and consumers.

Respondents’ Dependence on Social Media Platforms in Health and Wellness Consumption Decisions, Data Source: Questionnaire Survey

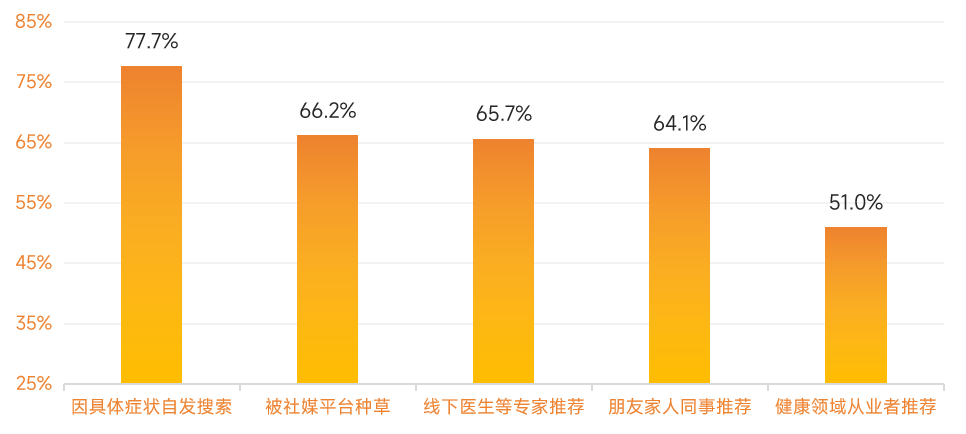

Nearly 80% of respondents indicated that social media platforms are a key channel for discovering new products. Among these, “spontaneous searches driven by specific symptoms” was selected by 77% of respondents, while “being influenced by recommendations on social media platforms” ranked second at 66.2%, surpassing recommendations from offline experts, friends, family, colleagues, and healthcare professionals.

Channel Selection Rate for Respondents’ Awareness of New Products/Services; Data Source: Questionnaire Survey

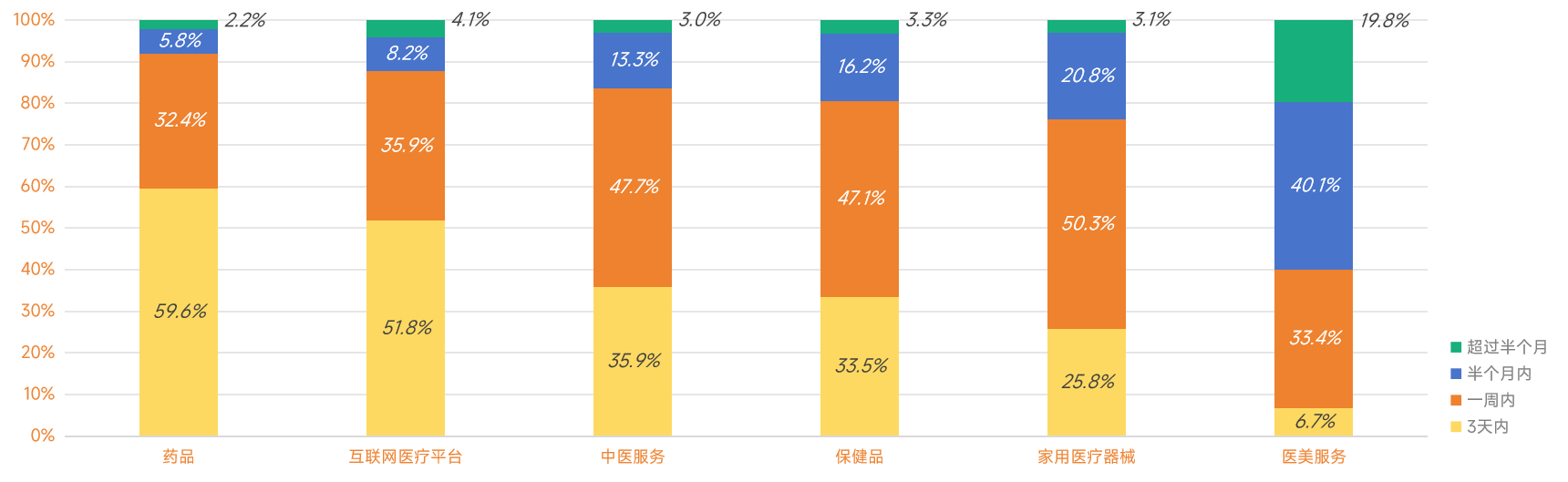

Decision Cycle:In high-consumption sectors such as health supplements, users have long decision-making cycles, requiring continuous engagement to influence their mindset.

Respondents from the pharmaceutical sector demonstrated the shortest decision-making cycle, with 92.0% making decisions within one week. This was followed by internet medical service platforms, traditional Chinese medicine (TCM) services, health supplements, and home medical devices. Respondents in the medical aesthetics services sector had the longest decision-making cycle.

The stronger the consumer-oriented nature of a niche sector, the longer the consumer decision-making cycle. Serious healthcare, represented by pharmaceuticals, involves high urgency, requiring prompt decisions. In contrast, consumer healthcare, exemplified by medical aesthetics services, exhibits significantly lower urgency, allowing consumers more time for consideration. Furthermore, in serious healthcare, physicians and specialists play a decisive role, with patients largely adopting professional recommendations directly, thereby shortening the decision-making cycle. This indicates that niche sectors with strong consumer attributes, such as health supplements and medical aesthetics services, require long-term marketing strategies.

Percentage of Respondents in Each Sub-sector by Consumer Decision-Making Cycle, Data Source: Questionnaire Survey

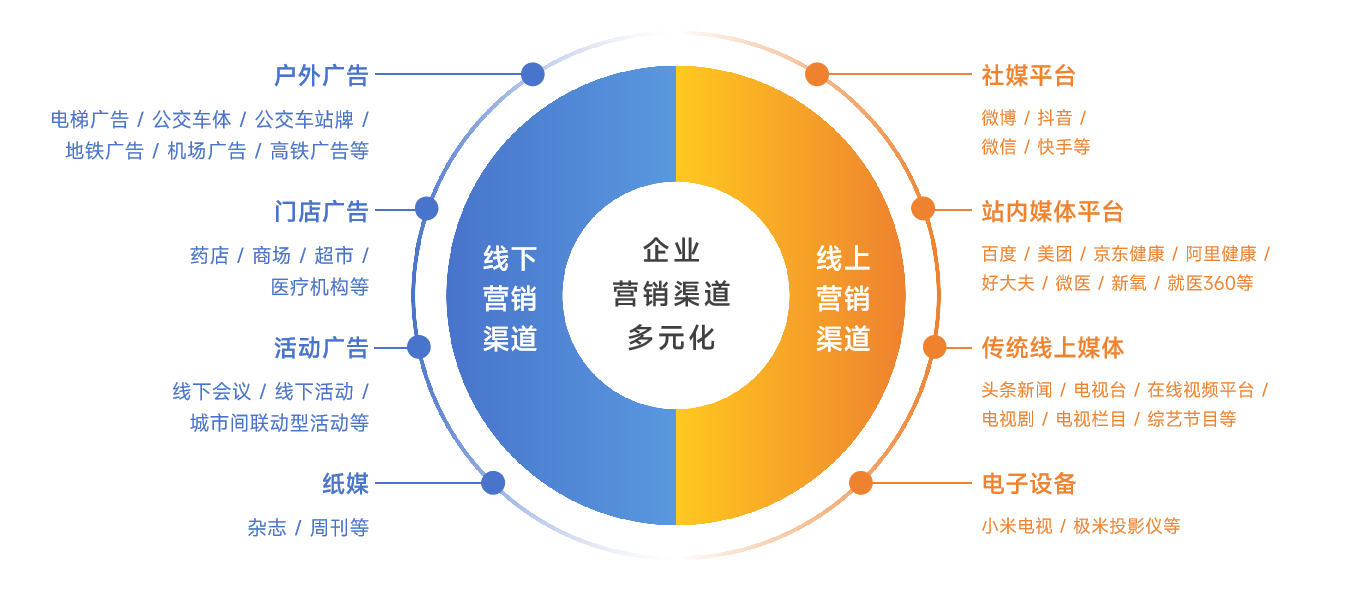

As a bridge connecting both the supply and demand sides of the general health industry, social media platforms have become a crucial online marketing channel for companies in this sector, representing an essential opportunity that must be seized.

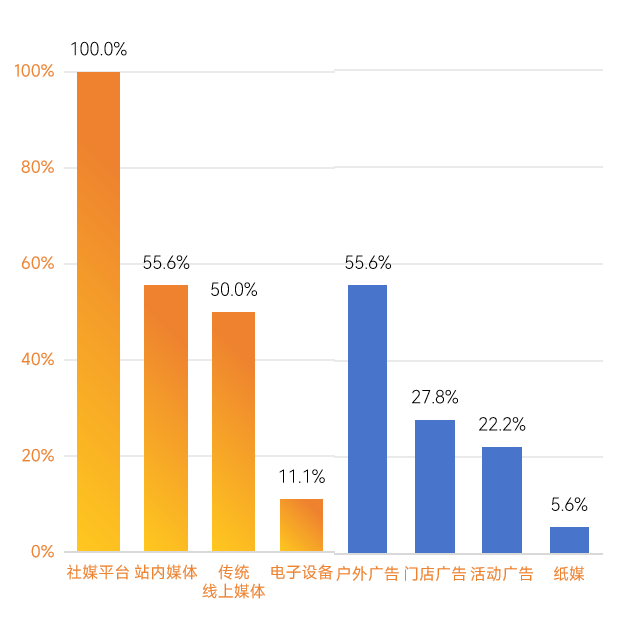

A survey of 18 big health enterprises across six sub-sectors revealed that social media platforms are the only marketing channels adopted by all companies, with a penetration rate surpassing that of other online and traditional offline channels. Deepening social media marketing efforts, accelerating omnichannel social media deployment, and striving to identify new engines for business growth have become the top priorities for these enterprises.

Percentage of surveyed companies selecting each marketing channel. Data source: survey interviews

Diversification of Marketing Channels in Healthcare and Wellness Enterprises, Data Source: Survey Interviews

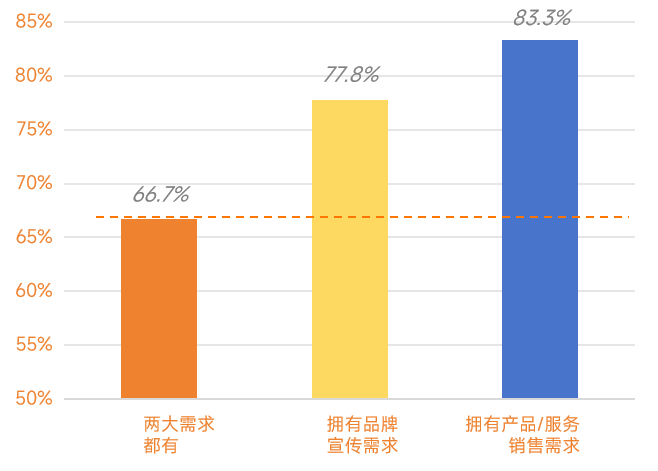

Brand promotion and sales conversion are the focal points of online marketing in the health and wellness sector, with brand promotion serving as the cornerstone for building user trust.

Interviews reveal that a growing number of health-focused enterprises are increasingly prioritizing brand building and promotion. Leveraging online social media platforms to collaborate with physicians on science popularization and patient education, thereby establishing user trust, has become the core objective of brand promotion in online marketing. Market penetration into lower-tier cities and the improvement of logistics infrastructure are key channels driving online sales conversion.

Corporate Marketing Objectives on Social Media Platforms; Data Source: Survey Interviews

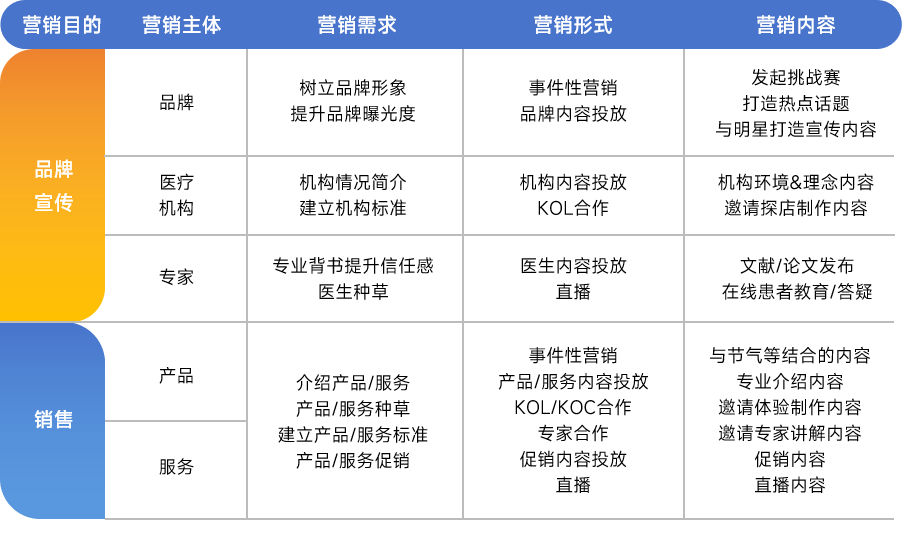

Marketing on social media platforms primarily aims to enhance brand awareness and drive sales conversions. Depending on their specific objectives, companies focus their marketing efforts on brands, institutions, products, services, and experts, while strategically aligning marketing formats and content with the attributes of specific products.

Deconstructing the Current State of Marketing Collaborations Between Big Health Enterprises and Social Media Platforms: Data Source: Survey Interviews

Differentiated platform attributes meet the diverse marketing needs of enterprises, and solutions are built based on these platform attributes.

Consumers go through three stages when making purchasing decisions: “cognitive education,” “search penetration,” and “solution evaluation.” To successfully engage consumers across these three stages, companies need to leverage multiple platforms in a coordinated strategy.

During the cognitive awareness stage, user volume is the primary consideration. A large total user base serves as the foundation for reaching a broader pool of potential consumers, an area where Weibo and Douyin hold significant advantages. Notably, during peak marketing periods—such as cold medication campaigns during flu season or health product promotions aligned with traditional solar terms—Weibo’s event-driven marketing capabilities demonstrate exceptionally high alignment with market demand. In the search penetration stage, users seek quick and intuitive information regarding product or service functions, efficacy, and usage instructions; at this point, the platform’s ability to generate consumer interest (“zhongcao”) becomes the key focus. During the solution evaluation stage, users compare multiple shortlisted products to make final purchasing decisions, making the platform’s capacity for robust content output particularly critical.

This report, in collaboration with Weibo, provides insights for healthcare companies to seize opportunities on social media platforms, based on an analysis of six key ecosystem dimensions: users, content, media, physicians, scenarios, and IP.

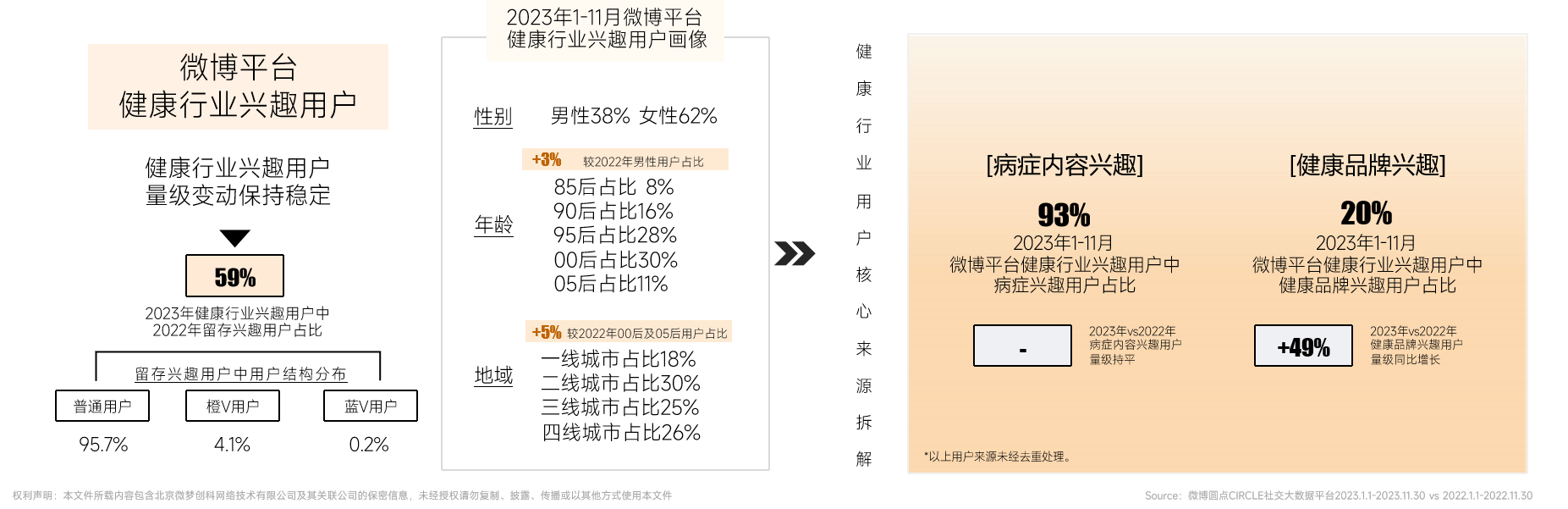

User Ecosystem: Consumers of health-related content span all age groups. Users interested in disease-specific content constitute the core of the industry’s user base, while those with an interest in health brands are showing a growing trend.

In 2023, the scale of users interested in the health industry remained stable, with retained interested users from 2022 accounting for 59%, predominantly consisting of general users who continuously engaged with health-related content. An analysis of the user profile within the health industry reveals that individuals across all age groups demonstrated interactive interest in health-associated content, among whom the proportion of male users and those born after 2000 and 2005 showed an increasing trend. In terms of consumption of segmented content within the health industry, users interested in disease-related content constituted the core base, contributing a substantial 93%. Users interested in health brands also represented a significant source of industry engagement, with their numbers experiencing a year-on-year growth of 49%.

Weibo Platform Users Interested in the Health Industry

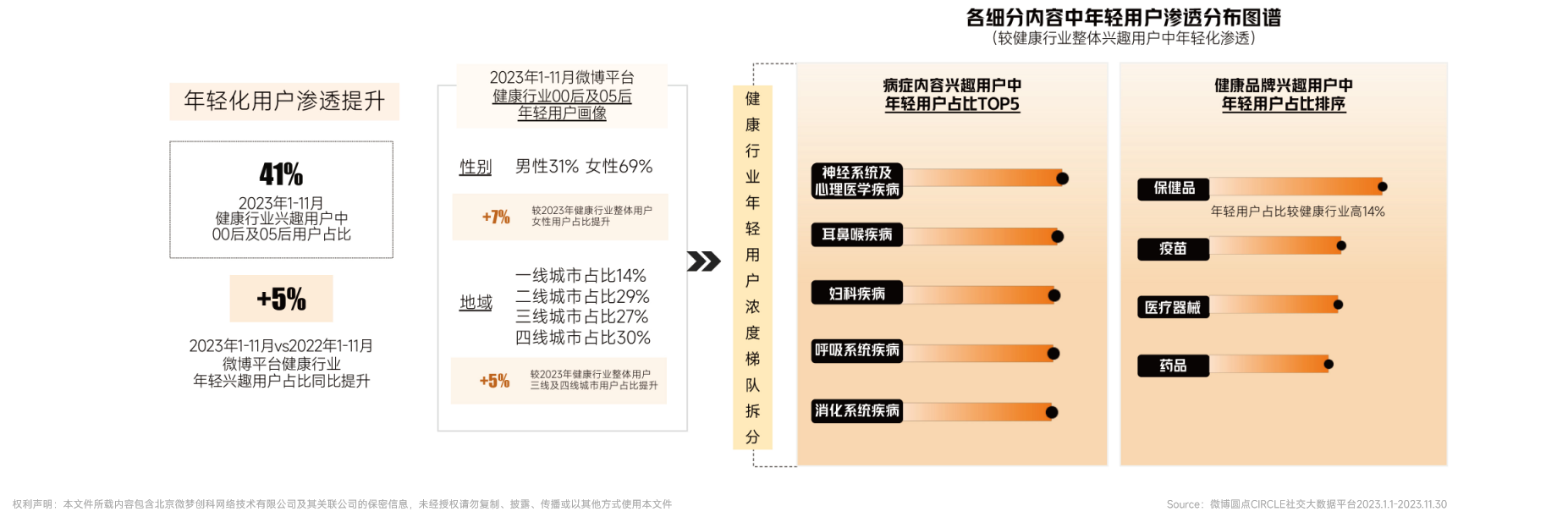

User Ecosystem: There is a growing trend among young users consuming health-related content, predominantly female users from third- and fourth-tier cities. Notably, the penetration of younger demographics interested in neurological/psychiatric conditions and health supplements is significantly higher than the industry average.

In 2023, users born in the 2000s and 2005s accounted for 41% of those interested in the health industry. The volume of young users showed a year-on-year growth trend compared to 2022, with a growth rate of 5%. In terms of the demographic profile of young users in the health industry, female users from third- and fourth-tier cities constitute the core group of young audiences for health-related content on Weibo. Regarding the penetration rate of young users across specific health content categories, there is a high level of penetration among young users interested in neurological/psychiatric disorders and health supplements.

Penetration Rate of Younger Users in the General Health Industry and Distribution Map of Young User Penetration Across Various Content Segments

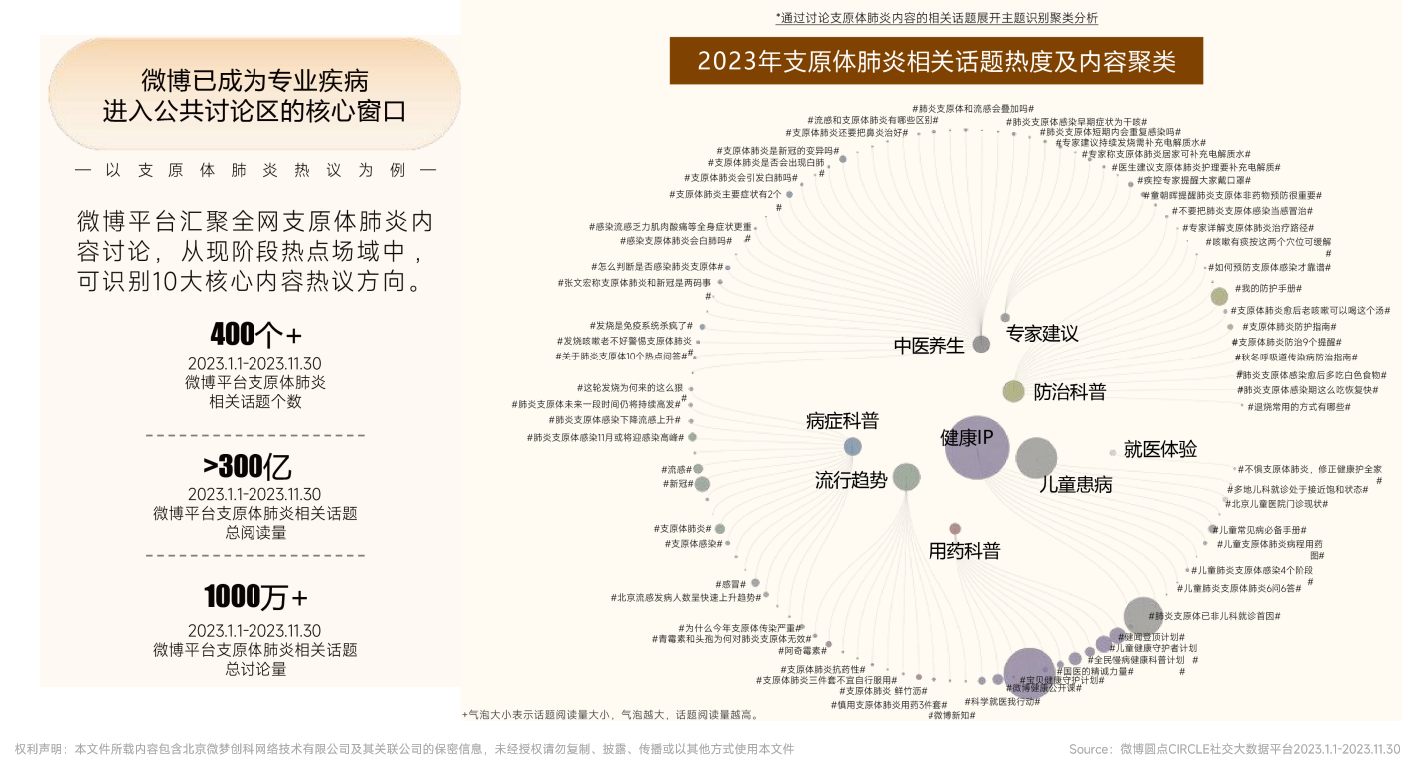

Content Ecosystem: Health-related hot topics continue to be discussed, gain momentum, and permeate society, enhancing public health awareness.

The “square effect” of social media platforms has fostered sustained attention to health-related content and triggered periodic spikes in public discussion, profoundly shaping health awareness across China. On Weibo, popular science content on various diseases covers a comprehensive range of topics, including common illnesses, chronic diseases, pediatrics, nutrition, and dermatology. During the 2023 outbreak of Mycoplasma pneumoniae pneumonia, discussions expanded from anxiety induced by the disease to broader aspects such as disease understanding, prevention, and treatment.

Weibo has become a core window for specialized diseases to enter public discourse.

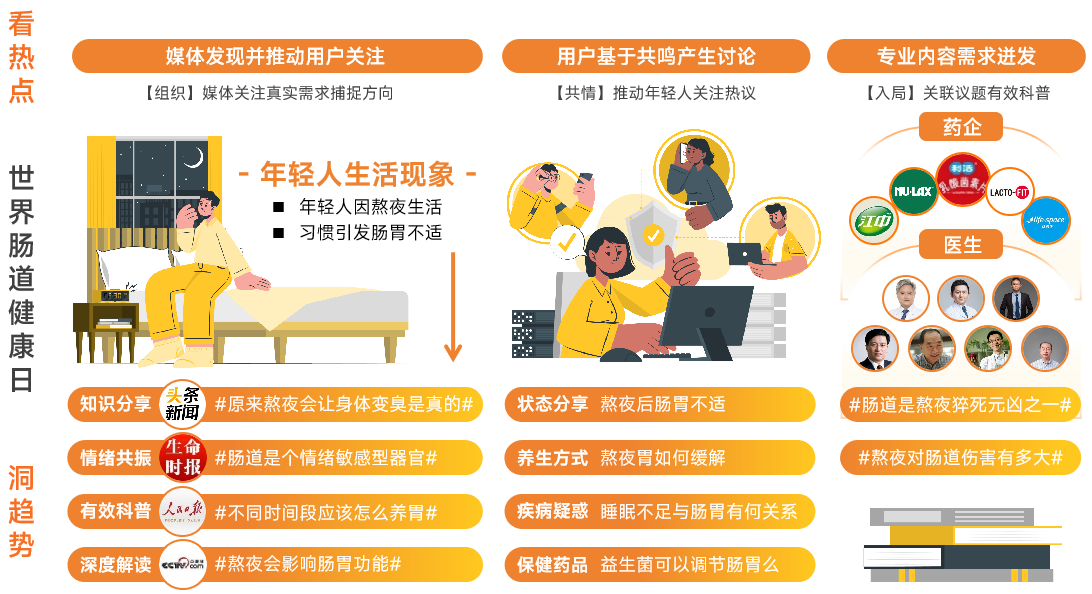

Media Ecosystem: Media Matrix, Driving Diversified Discussions on Health Issues and Strengthening Trust Endorsements.

On World Gut Health Day, government agencies such as the National Health Commission and the National Medical Products Administration interpreted pharmaceutical industry policies, while authoritative media outlets, including central and national media, developed various health-related topics to educate the public on health knowledge. Media plays multiple roles in this process, including identifying health issues, promoting health discussions, and guiding health awareness. Amidst trends of heightened media attention, vigorous public discussion, proactive user searches, and growing platform content, social media platforms have provided more scenarios for the dissemination of health topics. This enables big health enterprises to better connect with users through these scenarios, thereby achieving effective health brand promotion and marketing implementation.

Continuous Improvement in the Construction of the Media Organization Matrix

How Media Achieve Content Dissemination Based on Health Topics, Data Source: Weibo Social User Data Bank

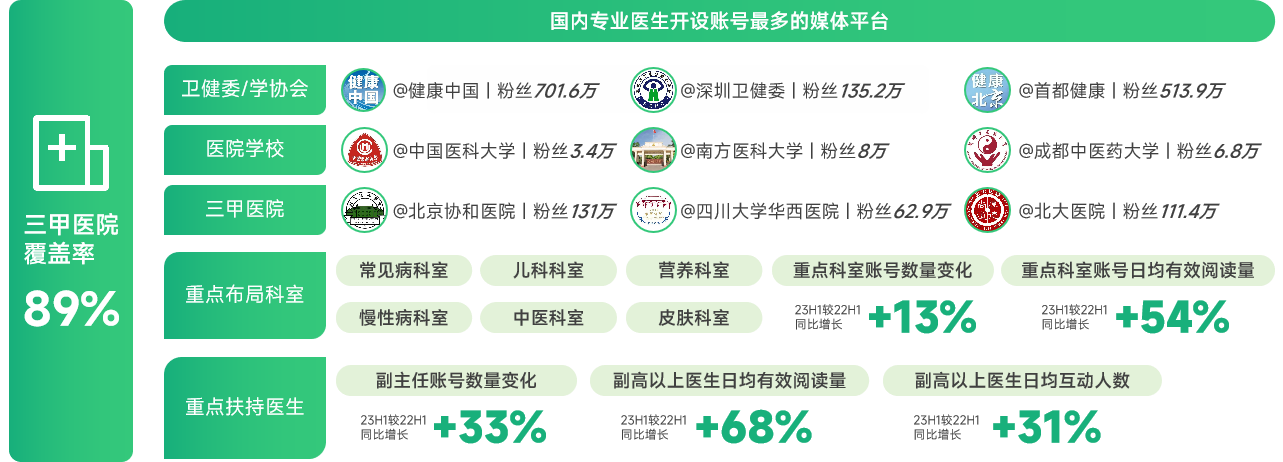

Doctor Ecosystem: Medical institutions and physicians across all specialties, serving as a professional force for science popularization.

It has become a phenomenon for the general public to acquire health literacy through trending health topics on Weibo. Weibo is the media platform with the largest number of accounts operated by professional physicians in China, covering nearly 90% of Grade A tertiary hospitals. For instance, in discussions surrounding the topic “Are Probiotics Genuine Health Boosters or a Scam?”, pediatric experts focused on science communication, stating that “probiotics can be used for children with gut microbiota imbalance.” Specialists in medical aesthetics, plastic and burn surgery, and medical aesthetics and cosmetology emphasized the selection of probiotics, citing relevant research from the World Health Organization (WHO), while obstetricians and gynecologists concentrated on dietary recommendations. The diverse interpretations provided by physicians from different specialties have fostered multifaceted patient education on the Weibo platform and enhanced the credibility of health-related content.

Weibo has become the media platform with the largest number of accounts opened by professional doctors in China. Data source: Weibo Social User Data Bank

The above is an excerpt from the main content of the “2024 White Paper on Marketing in the Big Health Industry.” To access more exciting content, please scan the QR code to add our assistant and obtain the full report.