Major Funds Secure Massive Capital Raises, Bolstering Confidence in China's Healthcare Primary Market

Since the beginning of this year, pessimism has continued to spread in the primary market.

Whether it is the intense industry debate over whether “the primary market is dead” or the palpable struggles faced by numerous investment institutions in fundraising and startups in securing financing, all signs point to one fact: China’s venture capital and private equity industry has undergone a dramatic transformation from the previous decade, which was characterized by exuberant growth and frenzied activity.

Accompanying these changes is a steady stream of negative news from the medical innovation industry, including layoffs, plant closures, sell-offs, and divestments. The chill pervading the sector, as revealed by each incident, has been stereotyped, deliberately interpreted, and continuously amplified.

The more one is swayed by emotions, the harder it often becomes to notice the subtle clues that the current industry may be undergoing a shift.

Just recently, two major fundraising events were overlooked by many:

· First, Jiangyuan Investment’s inaugural US dollar fund has officially closed, raising nearly USD 400 million. The limited partners (LPs) of this fund include international institutional investors such as insurance capital from Asia and Europe, professional asset management firms, and well-known funds of funds.

The amount raised and the LP structure indicate that foreign investors remain consistently and firmly bullish on the Chinese market.

· Second, Sequoia China completed the fundraising of a new RMB fund worth 18 billion yuan, marking the largest fundraising activity by a Chinese venture capital firm in the past year. The limited partners (LPs) behind this effort include Hangzhou Capital and several insurance companies.

This reflects the state’s consistent encouragement and support for insurance funds and other investors to participate in primary-market investments in sci-tech innovation.

Furthermore, from a broader macroeconomic perspective, the state has repeatedly emphasized this year the need to strengthen “patient capital” and actively create conditions to attract more medium- and long-term funds into the capital market. Alongside these developments, new detailed changes are emerging.

· For instance, in terms of policy support, on June 19, the State Council released the "Several Policy Measures to Promote High-Quality Development of Venture Capital" (hereinafter referred to as the "17 VC Measures").

The “17 Measures on Venture Capital” propose to orderly expand the opening-up of venture capital investment and facilitate foreign investors in conducting venture capital activities within China. In particular, it emphasizes “Support international professional investment institutions and teams in establishing RMB-denominated funds within China, leveraging its investment experience and comprehensive service advantages.”

· Similarly, in terms of capital implementation, many local state-owned assets have already begun exploring and piloting liability exemption mechanisms for early-stage and small-scale investments. For instance, Shandong Province released relevant administrative measures on July 4, proposing subsidies for loss-making projects in early-stage structures and encouraging the establishment of due diligence-based liability exemption mechanisms; Wuhan City stated in its February document that it aims to foster a sci-tech innovation environment that is tolerant of errors.

It can be seen that,Common Issues Surrounding State-Owned Capital as LPs, Previously Widely Discussed in the Industry, Are Improving. At a time when state-owned limited partners (LPs) have become the primary investors in venture capital (according to ZERONE data, state-owned and state-controlled LPs accounted for 73% of total capital commitments in 2023), the implementation of these measures is undoubtedly of positive significance.

Meanwhile, three industrial pilot fund-of-funds with a total scale of RMB 89 billion have also been established in Shanghai. Among them,Biopharmaceutical Fund of Funds with a Scale of RMB 21.5 Billion, primarily targeting areas such as innovative drugs and advanced formulations, high-end medical devices, biotechnology, and advanced pharmaceutical manufacturing equipment.

It is evident from the aforementioned details that capital conditions are improving. Investment institutions will have more abundant “dry powder” at their disposal, thereby bolstering confidence in the primary healthcare market.

However, capital alone is far from sufficient; what matters more is whether China’s medical innovation ecosystem continues to trend upward—The continuous emergence of promising medical innovation projects and high-quality assets is the key to enabling capital to invest with confidence, and serves as the decisive factor for the prosperity of the medical venture capital industry.

Therefore, this article will provide a detailed discussion of the underlying logic behind the substantial opportunities that remain in China’s healthcare venture capital industry, potential investment opportunities, the inevitable challenges, and corresponding recommendations from industry professionals.

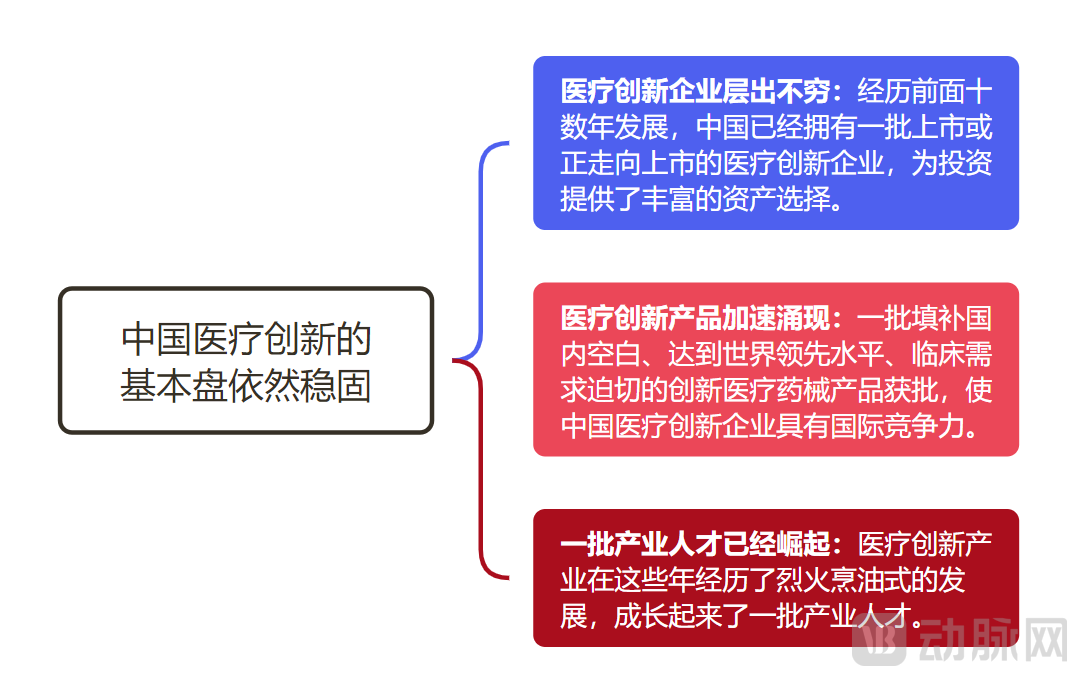

Looking back over the past decade or more, China’s healthcare innovation industry has undergone a period of explosive growth.

“It is no exaggeration to say that the past decade or so has been a process for China’s healthcare industry to go from zero to one and gradually integrate into the global system, with naturally abundant incremental opportunities,” an investment director at a RMB-denominated fund told VCBeat. “The influx of hot money kept the industry in a state of flourishing prosperity, reaching its peak in 2021.”

According to the VCBeat database, China’s healthcare primary market attracted over $150 billion in investment between 2015 and 2023, peaking at $52.4 billion in 2021. This substantial influx of capital has drawn a wealth of talent into the industry, particularly professionals from cross-sector backgrounds, while also cultivating a large cohort of specialized healthcare investors.

Supported by hot money, talent, and favorable policies, waves of medical innovation enterprises have emerged, grown, and ultimately gone public through initial public offerings (IPOs).: From 2015 to 2023, there were 612 successful domestic IPOs of medical innovation enterprises.

Taking Suzhou BioBAY as an example, tenant companies such as BeiGene (IPO on February 3, 2016), Innovent Biologics (October 31, 2018), CStone Pharmaceuticals (February 26, 2019), Alphamab Oncology (December 12, 2019), and Ascentage Pharma (October 28, 2019) have successfully completed their initial public offerings.

The proliferation of companies, emerging like mushrooms after rain, has sparked an explosion of innovative medical products.Between 2015 and 2023, China approved 243 innovative medical devices and more than 250 Class 1 innovative drugs for market launch. These products span diverse fields, including monoclonal antibodies, cell and gene therapy, synthetic biology, neurointervention, brain-computer interfaces, regenerative materials, and ophthalmic equipment, driving comprehensive growth across China’s medical innovation industry.

It is worth noting that,Product innovation has not slowed down, but rather accelerated, even during the “capital winter” of the past year or two.

For instance, in the field of innovative medical devices, VCBeat’s statistics reveal that a total of 110 innovative medical device products were approved between 2022 and 2023, surpassing the combined total from the eight-year period of 2014 to 2021. Among these approvals were numerous innovative medical devices that fill domestic gaps, reach world-leading standards, and address urgent clinical needs.

For example, in the field of innovative drugs, 34 domestically produced Class 1 new drugs were approved in 2023, representing a year-on-year increase of 156% compared to 2022 and setting a new historical record for approvals. Meanwhile, the approved domestically produced Class 1 new drugs are no longer concentrated among a few companies as before; instead, many new players have emerged, signaling that an increasing number of innovative pharmaceutical companies are reaching the commercialization stage.

As can be seen, China’s healthcare industry has amassed a rich portfolio of medical innovation products that are on par with global standards, and in some areas even leading the way. This progress is underpinned by healthcare innovation enterprises that have continuously forged ahead, as well as by industry talent who have grown alongside the sector over the years.These elements form the foundation of China's medical innovation, and this foundation remains solid.

(Chart by VCBeat)

Where the soil for innovation and entrepreneurship remains, investor confidence naturally follows.

“Jiangyuan’s global limited partners (LPs) maintain a long-term bullish outlook on technological innovation opportunities both globally and within China, including China’s vast market size and the opportunities arising from industrial transformation and upgrading, as well as global technological development trends. We also believe that in a large-base market like China, there are still opportunities to generate alpha returns,” Li Jiaan, Partner at Jiangyuan Investment and Head of Healthcare and Big Health Investments, told VCBeat.

“The ceiling for China’s healthcare industry is far from being reached.” Liu Hao, Founder and CEO of Haoyue Capital, also stated in an interview with Caijing Magazine that the combined market capitalization of the 800 listed companies in China’s healthcare sector falls short of the total market value of Novo Nordisk and Eli Lilly; only about 100 of these companies have a market capitalization exceeding RMB 20 billion.

Meanwhile, from a demographic perspective, against the backdrop of China’s aging population, the healthcare sector offers a long runway with substantial opportunities, underpinned by stable long-term growth expectations.

In other words, there are definite opportunities, both in terms of corporate growth potential and overall market expansion.

Certainly, as the industry undergoes a transition, new changes are emerging, and the themes of healthcare investment are rotating.

As mentioned above,With a solid foundation for medical innovation in China, the industry chain is gradually improving, attracting high-end scientific research talents to return continuously. All these factors have enabled China to establish a favorable ecosystem for "source innovation.", a large number of “source innovation” companies have subsequently emerged, becoming an investment theme for the foreseeable future.

For instance, in the field of drug development, Li Yuhui, Founding Managing Partner at Panlin Capital, previously pointed out to VCBeat that in the past, many startups introduced targets or drug modalities already validated abroad into the Chinese market. Today, however, many domestic founding teams are leveraging their solid scientific research accumulation in specific fields over many years to translate their findings into new technological platforms or novel drug modalities, thereby addressing significant clinical pain points and meeting unmet clinical needs.

“These new drug modalities and technologies are in very early stages, closely mirroring the development phases of their international counterparts. In fact, many of their technical features and mechanisms of action stem from original research by scientists, with virtually no comparable equivalents abroad.”

For example:

· At the biotechnology level, the booming development of cell and gene therapy (CGT) has sparked a wave of innovation in drug R&D. Continuous breakthroughs and positive progress in technologies such as CAR-T, AAV-based gene therapy, and iPSCs have propelled China from running neck-and-neck with global peers to taking a leading position.

· At the level of R&D and translation of target mechanisms, the innovation translation ecosystem in Chinese universities is gradually being established and maturing. Medical research in China on the translation of innovative disease biological mechanisms continues to make progress, holding promise for addressing a growing number of clinical needs through source innovation in target mechanisms;

· At the intersection of biotechnology and other disciplines, information technology has significantly empowered the application of biotechnology in disease diagnosis and treatment, driving source innovation across multiple domains such as AI-driven macromolecular design and AI-enabled gene editing.

Meanwhile, VCBeat holds a strong conviction that as China’s foundational scientific research capabilities strengthen, a shift in academic centers is underway—truly globally influential academic journals are emerging from within China.

Currently, several new academic journals have emerged in China, rapidly building their influence within their respective specialized fields. For instance, five new publications focused on biomedicine, edited by Academician Wei Yuquan, have seen their impact factors rise quickly. These include MedComm (with an impact factor of 9.9, which has three subsidiary journals: Future Medicine, Oncology, and Biomaterials and Applications), Molecular Biomedicine (with an impact factor of 4.0), and Signal Transduction and Targeted Therapy (with an impact factor of 39.3). Additionally, Peking University has launched the English-language journal Medical Review.

As academic centers relocate, the soil for source innovation in China will become increasingly fertile.

According to data cited by Song Ruilin, Executive President of the China Pharmaceutical Innovation Promotion Association, at the inaugural Pujiang Biopharmaceutical Source Innovation Forum, the number of Chinese institutions among the top 100 life sciences research organizations in 2023 increased by 32 compared with 2015, while the number of U.S. institutions decreased by 21, indicating significant progress in China’s basic research capabilities.

In addition, as an innovation ecosystem centered around academic hubs that follows the “introduction–agglomeration–layout–reconfiguration” pattern, China’s university science parks have developed rapidly: over the past three decades, 139 national-level university science parks have been established in China; by 2020, the country’s research output had ranked second worldwide, representing a 63.5% increase over five years.

As the healthcare industry enters a new phase of source innovation, investment logic is also evolving.Some investors have previously stated that project return rates will no longer be the sole criterion for investment decisions; instead, addressing unmet clinical needs will become a core focus for institutional investors. Meanwhile, projects should demonstrate greater focus, and investment strategies must become more refined. Furthermore, institutions are expected to engage deeply in the development of the entire healthcare industry value chain, creating additional value through the integration of industry and finance.

“Our investment strategy is also a sniper-style approach focused on specific industries. For instance, we conduct meticulous project sourcing, employing a top-down analysis to break down the healthcare and technology sectors into hundreds of sub-segments. We then select only 15% of these niches for investment, aligning our tactics with a refined, precision-driven methodology,” Li Jiaan, Partner at Jiangyuan Capital and Head of Healthcare and Greater Health Investments, told VCBeat. “We seek out companies that are either ‘the only one’ or ‘the number one’ in their field, entering at a sufficiently early stage and making consecutive follow-on investments once we have identified promising targets. To this end, the fund reserves 30% of its capital for subsequent follow-on rounds.”

Undoubtedly, the prevailing trend toward source innovation imposes higher demands on both industry entrepreneurs and institutional investors.

The trajectory of the healthcare industry’s evolution toward source innovation aligns perfectly with the national emphasis this year on vigorously developing new quality productive forces. It can be said that, in terms of timing and trends, the healthcare innovation industry has entered a new era.

However, new quality productive forces in science and technology, represented by source innovation in healthcare, often undergo a rather arduous process, characterized by substantial capital requirements and prolonged return cycles. In response, the state has repeatedly voiced its support,We must both strengthen the layout of national strategic scientific and technological forces and actively develop venture capital to expand patient capital.

Consequently, a series of related policies have been successively implemented. For instance, in mid-to-late June, the General Office of the State Council officially issued the “17 Measures for Venture Capital,” injecting greater confidence into the venture capital market.

For exampleOn the fundraising front, the “17 Measures for Venture Capital” point out that sources of capital should be expanded by engaging long-term investors, asset management institutions, and financial asset investment companies, while diversifying the product types of venture capital funds to better match the needs of long-term capital.

In this regard, the document states that we should fully leverage the roles of the National Emerging Industry Venture Capital Guidance Fund, the National Small and Medium-sized Enterprise Development Fund, and the National Science and Technology Achievement Transformation Guidance Fund, further optimize and strengthen them, improve the efficiency of market-oriented operations, and support strategic emerging industries and future industries through the “fund-of-funds + equity participation + direct investment” model.

Furthermore,The difficulty of institutional exit is also easing.It is reported that the China Securities Regulatory Commission (CSRC) has launched a pilot program for the in-kind distribution of shares by private equity and venture capital funds, allowing them to distribute held shares of listed companies to investors through non-transactional transfers. This approach not only diversifies exit channels but also helps mitigate market impact.

Meanwhile,Many signs also indicate that numerous foreign investors remain firmly bullish on China’s industrial innovation opportunities, which will bring more possibilities to the venture capital and private equity industry.

For instance, in a recent media interview, Brett Wall, Global Executive Vice President of Medtronic and President of its Neuroscience Portfolio, stated, “In reviewing Medtronic’s operations in China, we have identified opportunities for growth and sustained expansion here. Moreover, to be candid, leveraging the unique resources, technologies, and capabilities available in the Chinese market has also enabled Medtronic to become a better company.”

Notably, China is the only market worldwide where Medtronic has established a dedicated regional venture capital fund.

We believe that, with the support and companionship of patient capital, China’s healthcare venture capital industry will regain confidence and continue to move toward a more innovative and prosperous future.