Sinopharm Boya Bio Announces $253 Million Acquisition of Green Cross HK to Expand Blood Products Portfolio

On July 17, Boya Bio-pharmaceutical Group Co., Ltd. (300294.SZ) announced that it would acquire 100% equity interest in GREEN CROSS HK HOLDINGS LIMITED (Chinese name: Green Cross Hong Kong Holdings Limited; abbreviated as Green Cross (Hong Kong) or GC HK), held collectively by GC, Synaptic, and individual sellers, for RMB 1.82 billion, thereby indirectly acquiring the domestic blood products entity Green Cross (China) Biological Products Co., Ltd. (abbreviated as Green Cross (China)).

The actual premium for this acquisition target exceeds 180%, and the target has been incurring losses in recent years. According to the announcement, the transaction amount is RMB 1.82 billion, accounting for 24.86% of Boya Bio-pharmaceutical Group Co., Ltd.’s latest audited net assets. This acquisition is expected to result in substantial goodwill for Boya Bio-pharmaceutical.

In addition, the announcement stated that Boya Bio-pharmaceutical Group Co., Ltd. will join hands with its controlling shareholder, China Resources Pharmaceutical, to jointly sign a Strategic Cooperation Framework Agreement with GC. The parties will cooperate on business integration of Green Cross (China), import and export sales of pharmaceuticals, as well as businesses related to blood products, vaccines, cell and gene therapy, and diagnostics, for a cooperation period of 10 years.

Upon completion of this transaction, Boya Bio-pharmaceutical Group Co., Ltd. will become the sole owner of a blood products manufacturing enterprise, adding one production license, four operational plasmapheresis stations, and expanding its plasma station footprint into two additional provinces.

The M&A target is in a loss-making position.

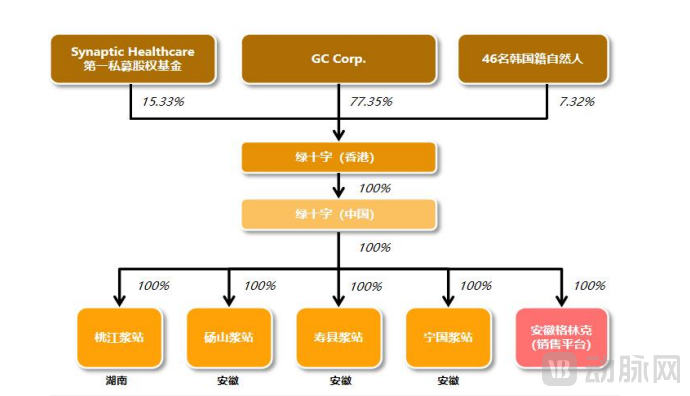

According to the announcement, GC HK, as a holding platform, wholly owns all of its business entities within mainland China. Among them, Green Cross (China) is the blood products company established by GC in mainland China through GC HK.

Green Cross (China) Equity Structure Source: Boya Bio-pharmaceutical Group Co.,Ltd. Announcement

Green Cross (China) Equity Structure Source: Boya Bio-pharmaceutical Group Co.,Ltd. Announcement

According to available data, Green Cross (China) specializes in the research and development, manufacturing, and sales of blood products. It currently offers 16 specifications across six product categories: albumin, intravenous immunoglobulin (IVIG), Factor VIII, fibrinogen, hepatitis B immune globulin, and tetanus immune globulin. The company operates four plasma collection stations, with a plasma collection volume of 104 tons in 2023 and a compound annual growth rate (CAGR) of 13% from 2017 to 2023. Additionally, through its sales platform subsidiary, Anhui Greencross, it distributes imported albumin, recombinant Factor VIII, and medical aesthetic products in China. In the field of coagulation products, particularly human-derived Factor VIII, Green Cross (China) holds advantages in production capacity, market share, and brand recognition. The company has also introduced recombinant Factor VIII, making it one of the few blood product enterprises in China with sales rights for both human-derived and recombinant Factor VIII.

Prior to the completion of the transaction, GC held a 77.35% equity stake in Green Cross (Hong Kong), the private equity fund Synaptic held a 15.33% stake, and an additional 46 Korean natural persons collectively held a 7.32% stake. GC is South Korea’s third-largest biopharmaceutical company, the first in the country to manufacture blood products and HIV diagnostic reagents, the third company globally to develop a hepatitis B vaccine, and the fourth globally to develop recombinant human coagulation factor VIII.

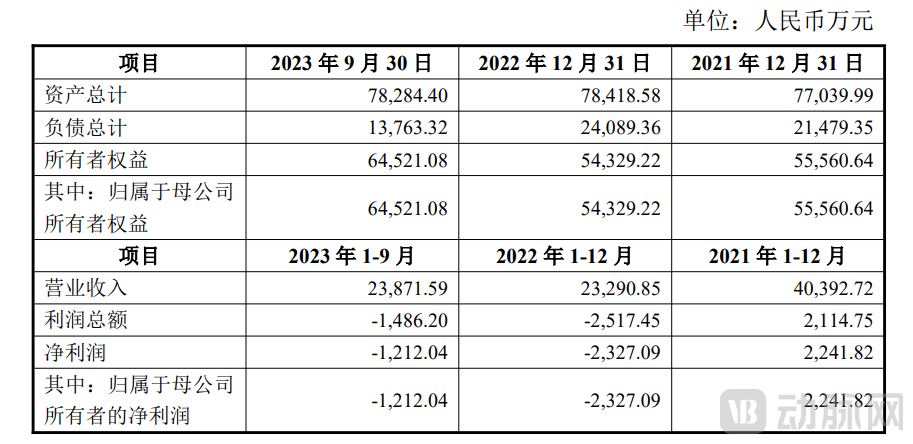

As of the valuation reference date of September 30, 2023, the net assets attributable to shareholders of the parent company for GC HK amounted to RMB 645 million. Boya Bio-pharmaceutical Group Co., Ltd. stated that the final valuation conclusion was based on the income approach, under which the total equity value of GC HK was determined to be RMB 1.677 billion, representing a value-added rate of 159.97%. Based on the transaction price of RMB 1.82 billion, the actual premium for GC HK stood at 182.17%.

Key Financial Data of GC HK for the Past Two Years (Audited) and the Current Period (Audited) Source: Boya Bio-pharmaceutical Group Announcement

Key Financial Data of GC HK for the Past Two Years (Audited) and the Current Period (Audited) Source: Boya Bio-pharmaceutical Group Announcement

According to the financial statements, GC HK reported revenues of RMB 404 million, RMB 233 million, and RMB 239 million in 2021, 2022, and the first three quarters of 2023, respectively. The corresponding net profits attributable to shareholders of the parent company were RMB 22.4182 million, -RMB 23.2709 million, and -RMB 12.1204 million. Although the company continued to report net losses attributable to shareholders of the parent company, its revenue in 2023 saw a slight increase compared to the previous year, and the losses began to narrow. However, the announcement did not disclose the reasons for GC HK’s losses.

Blood Products Market: Supply Falls Short of Demand Amid Strict Regulation

In China, source plasma used for the production of blood products is collected exclusively through legally established plasmapheresis centers. These centers are approved by provincial health and family planning commissions, managed by blood product manufacturers, and serve as exclusive resources for these enterprises. Plasmapheresis centers must use automated apheresis machines to collect plasma; after separation, red blood cells, platelets, and white blood cells are returned to the donor’s body. The collected plasma can be put into production only after undergoing three rounds of viral testing. Plasma proteins undergo initial fractionation (using the cold ethanol method combined with centrifugation or pressure filtration) and further purification (using chromatography techniques) to produce various blood products. In China, blood products are subject to a lot release system. Each batch must pass the manufacturer’s internal quality control tests before an application for lot release is submitted. Only after approval by the National Medical Products Administration (NMPA) can the products be marketed and sold.

Given the unique characteristics and stringent safety requirements of blood products, national regulations mandate traceable process records for all stages—including raw material collection, testing, storage, transportation, production, and sales—thereby implementing strict end-to-end supervision. China’s regulatory authorities have adopted rigorous oversight measures and introduced a series of regulatory policies to ensure the healthy and orderly development of the industry.

According to Huajing Industry Research Institute, the volume of plasma collected by domestic blood product manufacturers in China reached approximately 10,181 tons in 2022, representing an 8.3% year-on-year increase. Despite the rebound in plasma collection following the pandemic, a significant gap remains between the supply and demand for source plasma in China. Constrained by insufficient upstream plasma resources, per capita consumption of blood products in China remains far below the levels observed in developed countries.

Based on the data, the market size of China's blood products industry was RMB 26.8 billion in 2016 and reached RMB 38.3 billion in 2021. With improvements in healthcare standards and the perfection of the medical security system, the clinical usage of blood products is expected to continue increasing, thereby expanding market capacity. The blood products industry is poised to maintain steady growth in the future. According to publicly available data, China had 287 plasma collection stations in 2021, with a total plasma collection volume of 9,390 tons, averaging 6.6 liters per 1,000 people.

However, according to an announcement by Boya Bio-pharmaceutical Group Co., Ltd., the state has not approved any new manufacturers since May 2001 and has implemented aggregate production controls on existing ones. Currently, there are fewer than 30 blood product manufacturers operating normally in China, with a small number of enterprises holding multiple production licenses. This results in high industry barriers and extremely scarce licensing resources for manufacturers. Consequently, despite GC HK’s continuous losses, it remains a scarce investment target.

Boya Bio-pharmaceutical's profits are also declining.

According to Boya Bio-pharmaceutical Group Co., Ltd.'s financial report, its full-year revenue in 2023 was RMB 2.652 billion, a year-on-year decrease of 3.87%; the net profit attributable to shareholders of the parent company was RMB 237 million, a year-on-year decrease of 45.06%. According to Boya Bio-pharmaceutical, the significant change in performance was affected by two factors: first, the transfer of equity interests in Guangdong Fuda Pharmaceutical Co., Ltd. (hereinafter referred to as "Fuda Pharmaceutical") and Guizhou Tianan Pharmaceutical Co., Ltd. (hereinafter referred to as "Tianan Pharmaceutical"); second, the impact of goodwill impairment provisions and other asset impairment provisions arising from the acquisition of Xinbai Pharmaceutical.

Xinbai Pharmaceutical is a pharmaceutical company specializing in the research and development of biochemical drugs. Its main products include Compound Bone Peptide Injection, Oxytocin Injection, and Heparin Sodium Injection. In 2015, Boya Bio-pharmaceutical Group Co., Ltd. acquired an 83.87% equity stake in Xinbai Pharmaceutical for RMB 520 million, making it a wholly-owned subsidiary. However, influenced by comprehensive market factors such as centralized procurement policies and adjustments to the National Reimbursement Drug List, Xinbai Pharmaceutical’s performance has continued to decline in recent years.

In 2022, Xinbai Pharmaceutical’s operating revenue and net profit were RMB 438 million and RMB 30 million, respectively. In the first half of 2023, its operating revenue continued to decline to RMB 185 million, while net profit was halved to RMB 15 million, representing year-on-year decreases of 11.43% and 23.25%, respectively.

In 2023, to address horizontal competition among controlling shareholders, Boya Bio-pharmaceutical transferred Fuda Pharmaceutical and Tian’an Pharmaceutical, both of which had been acquired previously. Tian’an Pharmaceutical, which focuses on the research and development of diabetes medications, came under the control of Boya Bio-pharmaceutical at the end of 2013. In 2015, Boya Bio-pharmaceutical further acquired a 27.77% equity stake in Tian’an Pharmaceutical for RMB 140 million. Fuda Pharmaceutical is a blood products distribution company. In September 2017, Boya Bio-pharmaceutical acquired an 82% equity stake in Fuda Pharmaceutical for RMB 218 million. In January 2018, the company increased its capital investment in Fuda Pharmaceutical.

In 2021, China Resources Pharmaceutical Holdings Limited, a subsidiary of China Resources Pharmaceutical (3320.HK), obtained control of Boya Bio-pharmaceutical Group Co., Ltd. by acquiring shares held by Shenzhen GTJA Investment Group Co., Ltd., accepting voting rights proxies, and fully subscribing to the shares issued by Boya Bio to specific investors, thereby integrating Boya Bio into the China Resources Group’s healthcare sector.

Under the strategic guidance of China Resources Group, Boya Bio-pharmaceutical (a subsidiary of China Resources) has been clearly positioned as the Group’s primary platform for blood products. A strategic plan was formulated to rank among the leading domestic blood product enterprises by the end of the “14th Five-Year Plan” period and to become a “world-class blood products enterprise” in the medium to long term. Subsequently, Boya Bio-pharmaceutical began to continuously divest its non-blood product businesses.

Currently, the blood products sector in China exhibits a pronounced leader effect, with a competitive landscape dominated by industry giants such as Tiantan Biological Products, Shanghai RAAS Blood Products, Hualan Biological Engineering, and Taibang Biological Group. According to data from Huajing Industry Research Institute, in 2022, the combined plasma collection volume of these four leading companies accounted for more than half of the national total, while Boya Bio-pharmaceutical Group ranked fifth in terms of operating revenue.