Average Deal Size Up Nearly 30%, Hot Segments Rebound: H1 2024 Global Healthcare Investment and Financing Report

NovaBridge Biosciences

Biological Agent Developer

In the first half of 2024, the winter chill sweeping through the global healthcare investment and financing market entered a critical phase. Limited capital increasingly flowed toward projects with clear market expectations, while conceptual technological innovations no longer attracted favor from professional investors or even public shareholders.

In this report, VCBeat has compiled and analyzed over 1,000 global financing and investment transactions in the healthcare sector during the first half of 2024 (H1 2024). As per our established practice, we have integrated these findings with more than a decade of historical global investment data to provide a detailed characterization of the current landscape and subtle shifts in global medical innovation financing. Our analysis covers multiple dimensions, including sub-sectors, transaction sizes, deal frequency, funding rounds, investing institutions, and geographic regions.

We have found that, to this day, innovation remains the core theme in the global healthcare sector, with various related initiatives continuing to attract substantial capital investment on a large scale. However, there has been a consensus shift in the perception of innovation’s value, moving from the pursuit of technological extremity to a focus on efficiency.

Core Viewpoints

(I) In H1 2024, the phased downward trend in global healthcare investment and financing continued. However, considering seasonal variations and characteristics on a global scale, market performance in H2 may be promising. Domestically, less optimistic signals suggest that China’s total healthcare financing amount for the full year of 2024 could fall below $10 billion.

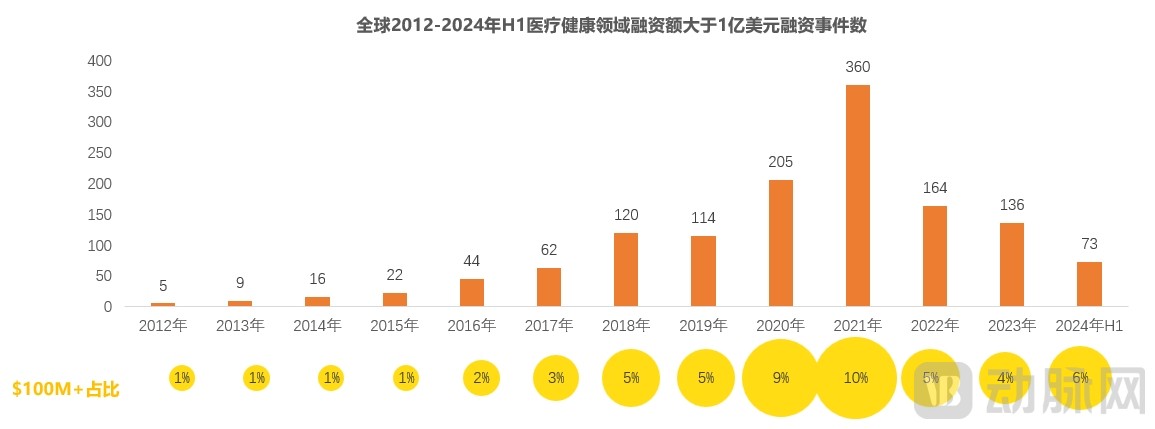

(II) The proportion of financing events exceeding $100 million reached 6%, the highest level in the past three years, even surpassing pre-pandemic levels.

(3) Total financing in the biopharmaceutical, medical device and consumables, and healthcare services sectors saw slight year-on-year increases of 9%, 7%, and 16%, respectively, indicating that high-quality projects in these corresponding sub-sectors continue to demonstrate strong capital attraction capabilities.

(4) Globally, 42 healthcare companies completed two or more rounds of financing, accounting for 3.6% of the total, a significant decrease from 8.6% in the same period of 2023, indicating that primary market healthcare funds are beginning to seek new investment opportunities.

(5) Amidst the wave of regulatory adjustments to listing rules in traditional popular IPO destinations for domestic healthcare companies, the Beijing Stock Exchange and the Hong Kong Stock Exchange are emerging as new hotspots for initial public offerings, with a clear trend of domestic biotech firms returning to list on the Hong Kong Stock Exchange.

I. Trends in Global Healthcare Industry Financing from 2012 to H1 2024

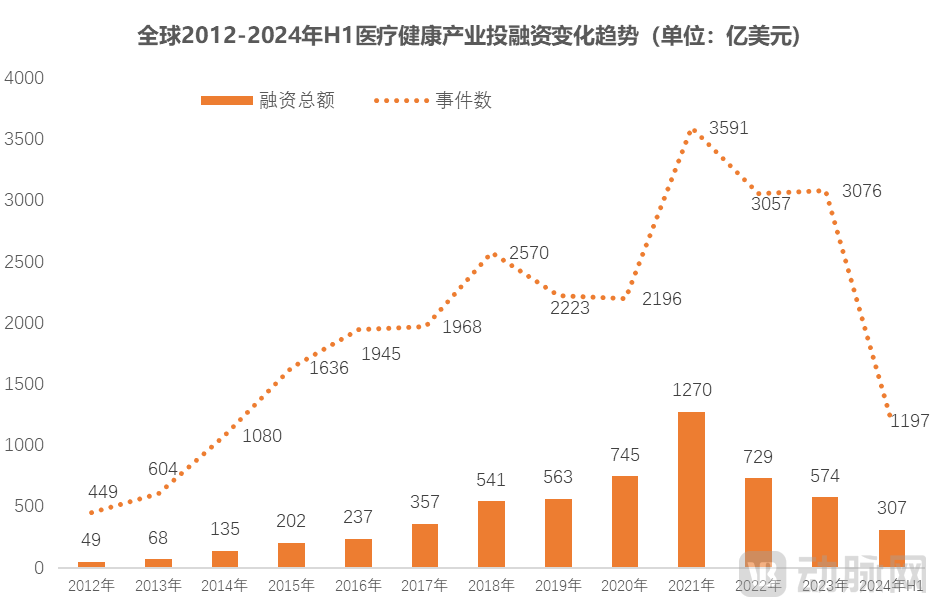

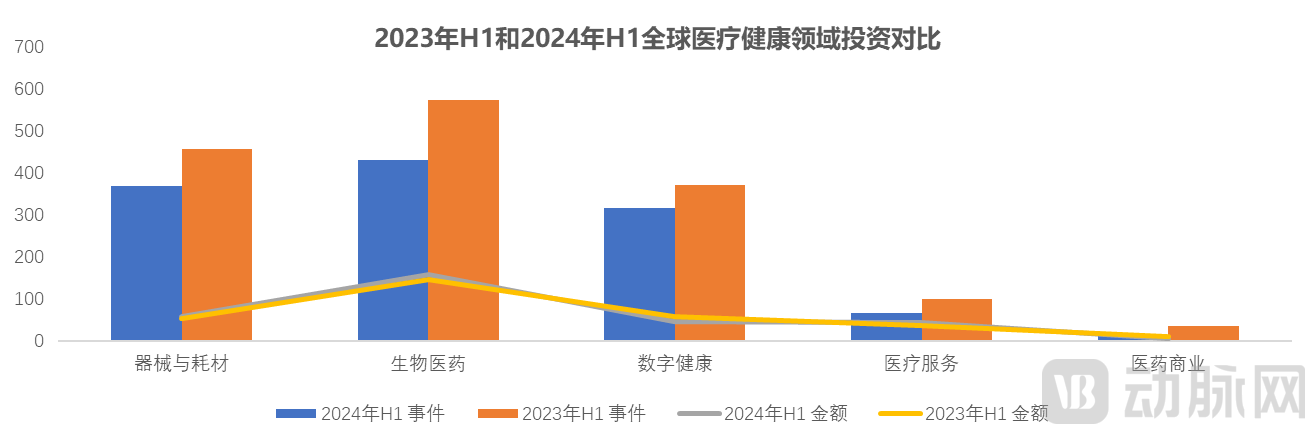

Overall, in the first half of 2024 (H1), the phased downward trend in global healthcare investment and financing continued. The number of transactions decreased by more than 20% year-on-year, while the average transaction amount increased by nearly 30%. Given seasonal variations, the second half (H2) may hold promise.

In H1 2024, a total of 1,197 primary market investments were completed in the global healthcare sector, with cumulative financing reaching $30.7 billion. Compared to the same period in 2023, the total financing amount over the past six months saw a slight increase of 1%. However, due to a sharp 21.9% decline in the number of financing transactions, the average financing amount experienced a significant counter-trend surge of 29.97%.

From a quarterly perspective, in Q1 2024, there were 159 financing deals completed globally in the healthcare sector, a slight increase from 151 deals in the same period of the previous year. Historically, Q1 has been a relatively active period for global pharmaceutical and healthcare financing. In previous years, the total financing amount and frequency in Q1 were often comparable to those in Q3 and Q4. Therefore, we can anticipate more robust performance in the global healthcare market in the second half of 2024.

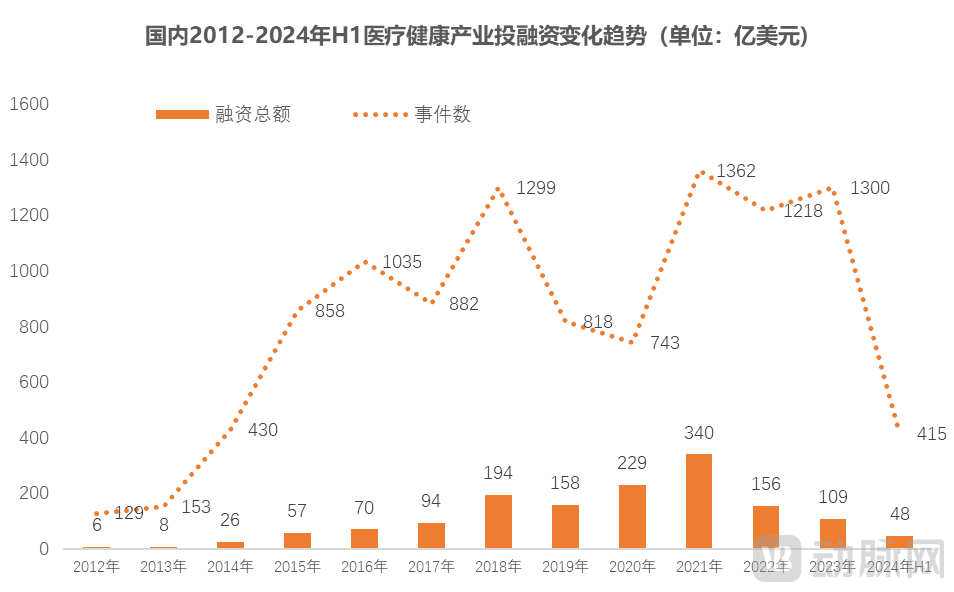

Amid Tightening Exit Channels, the Pace of Healthcare Financing in China Further Slows

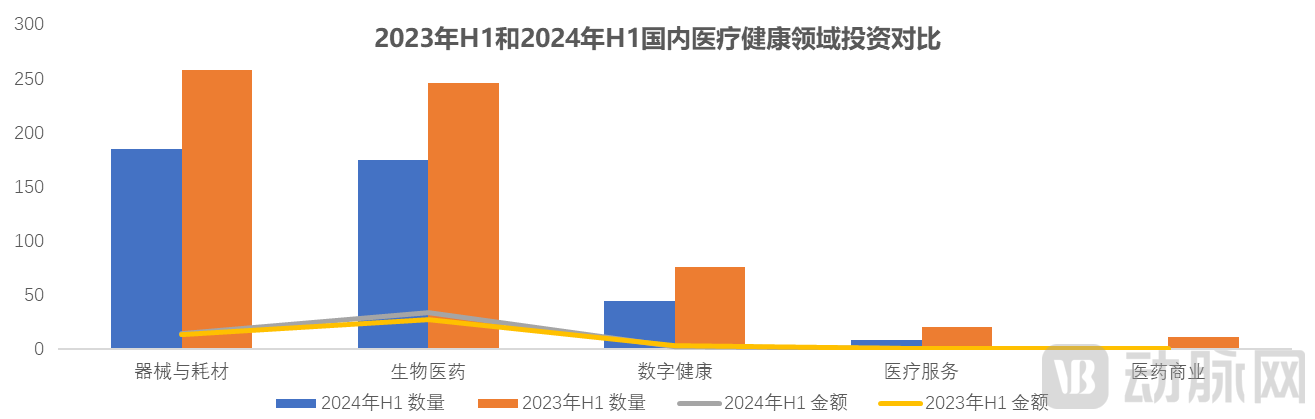

In China, the healthcare sector across various sub-sectors completed 415 primary market financing deals in H1 2024, with total funding amounting to approximately USD 4.8 billion. Compared to the same period in 2023, the number of healthcare financing transactions and the total amount in China decreased by 32.3% and 12.2%, respectively, in H1 2024. The contraction in both volume and value was more pronounced than that observed in the global healthcare market. However, at the level of average financing amount, the domestic market also saw a significant increase of 29.6% in H1 2024, keeping pace with the global market.

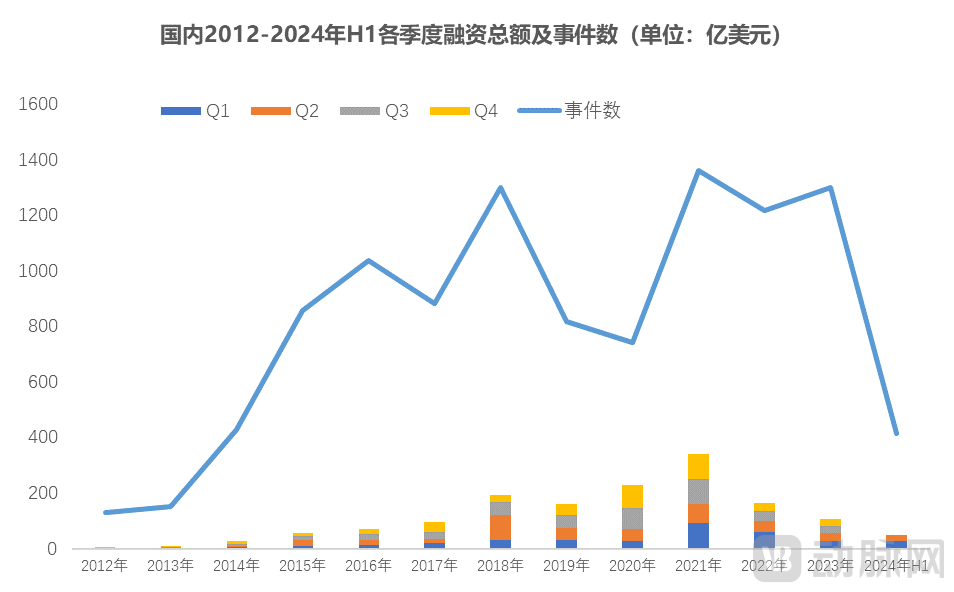

In terms of quarterly variations, in China, the second quarter (Q2), which immediately follows the Spring Festival each year, is often the most active period for healthcare investment and financing transactions. In contrast, Q1, Q3, and Q4 typically see lower transaction volumes with similar levels of activity. In Q2 2024, the domestic healthcare market secured nearly $2 billion in financing, equivalent to the average level observed from 2015 to 2017. Based on this less-than-optimistic signal, total annual healthcare financing in China for 2024 may fall below $10 billion.

Significant Increase in the Proportion of Mega-Deals: Multi-Million Dollar Biopharma Projects Are the Most Popular

H1 2024,A total of 73 primary market financing deals exceeding RMB 100 million were completed globally in the healthcare sector, a year-on-year decrease of 4 deals.. Relatively speaking, the proportion of financing events exceeding $100 million reached 6%, the highest level in the past three years, even surpassing pre-pandemic levels.

In H1 2024, the top three financing amounts were $2.344 billion, $1 billion, and $970 million, respectively, representing only a slight decrease from the $2 billion, $2 billion, and $1.1 billion recorded in the same period of the previous year. Amid declining enthusiasm for exit channels such as IPOs and M&A, the increased proportion of large-scale financings in the primary market clearly indicates a pronounced trend of capital accelerating its concentration toward leading projects.

In terms of subsectors, in the first half of 2024 (H1 2024), biopharmaceuticals remained the primary destination for global healthcare investment capital.

II. Hot Sectors in Global Healthcare Investment and Financing in H1 2024

Financing Deal Volume Shrinks Across Sectors; Pharmaceuticals and Medical Devices See Slight Increase in Capital Attraction, with China’s Pharmaceutical Sector Showing Signs of Recovery

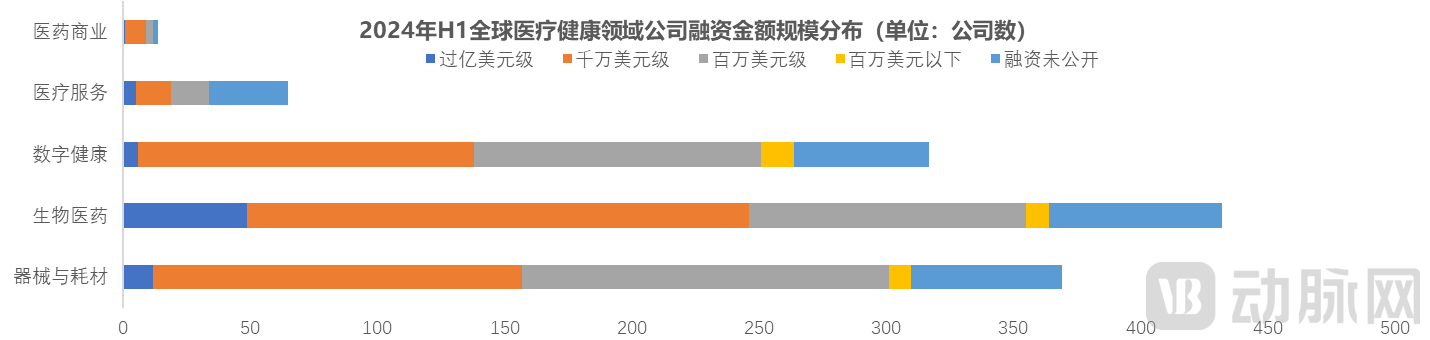

Globally, in H1 2024, healthcare industry financing by subsector included: 432 biopharmaceutical deals totaling $15.7 billion; 469 medical device and consumables deals totaling $5.7 billion; 317 digital health deals totaling $4.6 billion; 65 healthcare services deals totaling $4.3 billion; and 14 pharmaceutical commerce deals totaling $0.4 billion.

Among these sectors, total financing for biopharmaceuticals, medical devices and consumables, and healthcare services saw slight year-on-year increases of 9%, 7%, and 16%, respectively, indicating that high-quality projects in these respective sub-sectors continue to demonstrate strong capital attraction. In contrast, total financing for digital health and pharmaceutical commerce declined by 16.2% and 55.5%, respectively. Meanwhile, the total number of transactions decreased to varying degrees.

In China, the total financing amount in the biopharmaceutical sector reached USD 3.4 billion in H1 2024, ranking first among all sub-sectors; the medical devices and consumables sector recorded 185 financing transactions, the highest number of deals among all sub-sectors. In terms of trends, the total financing amount in the biopharmaceutical sector increased by 21.4% year-on-year, significantly outpacing global growth, while the total financing amount in the medical devices and consumables sector saw a modest increase of 7%. The transaction volumes in other sub-sectors and across all sectors declined year-on-year.

Series A and Seed/Angel Rounds Dominate; Early-Stage Medical Device and Consumable Projects See Divergent Valuations at Home and Abroad

Globally, in H1 2024, excluding deals with undisclosed funding rounds, biopharmaceutical projects recorded the highest number of Series A financing transactions, totaling 125, followed by medical device and consumable projects with 114 completed financing transactions. Healthcare service projects at Series D and above had the fewest financing activities, with zero transactions, while pharmaceutical commercialization projects at Series D and above completed only one transaction. Overall, Series A financing transactions were the most frequent, with 318 deals accounting for 26.5%, followed by Seed/Angel round transactions, with 207 deals accounting for 17.2%.

Distribution of Global Healthcare Industry Financing Rounds in H1 2024 Data Source: VCBeat Orange Database

Distribution of Global Healthcare Industry Financing Rounds in H1 2024 Data Source: VCBeat Orange Database

In China, during the first half of 2024 (H1 2024), excluding undisclosed funding rounds, Series A financing for biopharmaceutical projects and seed/angel round financing for digital health projects recorded the highest number of transactions, with 61 deals each. The lowest number of transactions was observed in medical service projects at Series D and above, with zero deals completed. Similarly, pharmaceutical commerce projects at Series D and above and Series A, as well as medical service projects at Series B, each completed only one transaction. Overall, Series A financing had the highest number of transactions at 155, accounting for 19.8% of the total, followed by seed/angel round projects with 146 transactions, representing 18.6%.

Distribution of Financing Rounds in China's Healthcare Industry in H1 2024 Data Source: VCBeat Orange Database

Biopharmaceuticals Lead by a Wide Margin, Medical Device Financing Is Fragmented, and Dental Solutions Providers Take the Top Spot Again

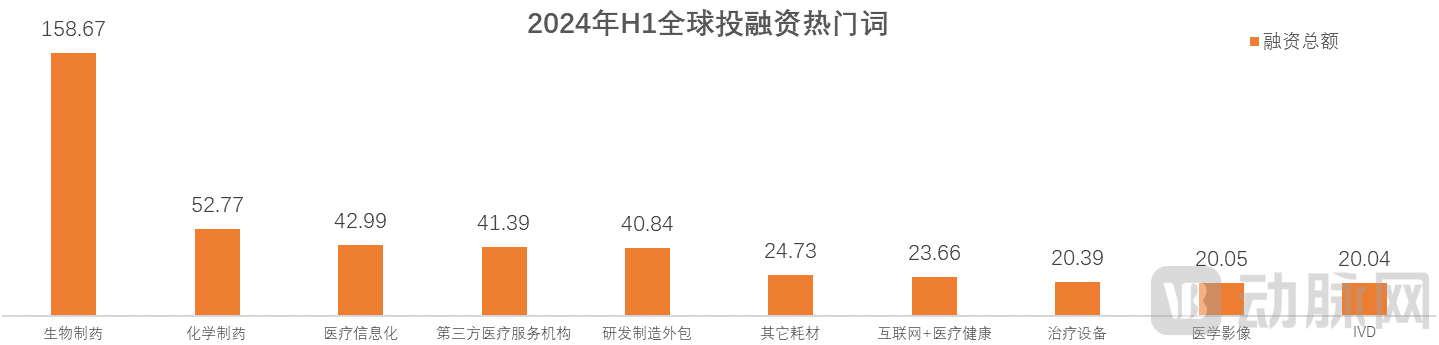

In H1 2024, biopharmaceuticals was the hottest financing category, accounting for a total of $15.867 billion in funding and representing 51.65% of the global primary market healthcare financing. In contrast, other popular sub-sectors such as chemical pharmaceuticals, healthcare informatics, third-party medical services, and R&D outsourcing collectively accounted for less than one-third of the financing volume seen in biopharmaceuticals. As the most capital-intensive area of medical innovation, biopharmaceuticals remains the most favored by investors.

In terms of individual financing transactions, in the first half of 2024, apart from the top two largest deals, eight of the top ten financing events by transaction amount were each valued at under $1 billion. Among the top ten financing events by transaction amount, the earliest-stage deal was the Series B financing completed by Hua Nuotai Bio.

MB2 Dental, a Texas-based dental services provider, emerged as the global healthcare innovation project with the strongest fundraising capability in H1 2024, securing a total annual financing amount of $2.344 billion. Interestingly, the healthcare market deal with the highest transaction value in 2023 was also closed by a Texas-based dental services company.

Top 10 Global Healthcare Financing Deals in H1 2024 Data Source: VCBeat Orange Database

Biopharmaceutical and medical device projects continue to dominate the rankings, while healthcare services and brain-computer interface projects rarely make the list.

In China, the largest single financing round in the first half of 2024 was a new round completed by Simcere Zaiming in February, which raised RMB 970 million. Most of the top 10 companies in domestic investment and financing are engaged in the development of innovative drugs and vaccines, or in the production and sales of medical devices. Notable exceptions include Taiyi Guanjia, which provides healthcare services, and Lingban Technology, which develops human-computer interaction technologies and AI hardware and software.

Top 10 Financing Deals in China's Healthcare Industry in H1 2024 Data Source: VCBeat Orange Database

Among them, Simcere Zaiming is a biopharmaceutical company under the Simcere Pharmaceutical Group, focusing on the research and development, production, and commercialization of innovative oncology drugs; it has been operating independently since 2023. Taiyi Guanjia is a family doctor service platform under China Pacific Insurance (CPIC). It provides online 24-hour medication guidance, sub-health management, and physical examination recommendations. Sequoia China is also one of the initiators of Taiyi Guanjia. Lingban Technology is a leading domestic human-computer interaction company. The financing round completed in January 2024 was the largest single investment in the AR sector in recent years.

AI Drug Developers Take the Lead, Mature Domestic Biotechs Secure Major Funding Rounds, and Nuclear Medicine CDMOs Make Their Debut on the List

In April 2024, Xaira Therapeutics, founded one year prior, completed a new round of financing amounting to $1 billion, becoming the most capital-attractive innovative enterprise in the first half of the year. Xaira Therapeutics is a typical West Coast U.S. technology innovation company, established by two distinguished venture capital experts in the biotechnology field. It aims to leverage AI for source innovation in drug discovery and secured substantial investments from professional institutions such as F-Prime Capital and Sequoia Capital upon its public debut.

Top 10 Global Biopharma Financings in H1 2024 | Source: VCBeat Orange Database

Among the top 10 global biopharmaceutical financing and investment deals in H1 2024, eight were from China. Notably, Midu Bio was the only third-party R&D and manufacturing service provider, specializing in CRO and CDMO services for radioisotope labeling and molecular imaging technologies.

Higher Bar for Late-Stage Financing Rounds; Multiple Biotechs Poised for IPOs as Investment and Financing in Radiopharmaceutical Companies Remain Red-Hot

In China, major biopharmaceutical financing deals in the first half of 2024 primarily originated from mature, earlier-generation biotech companies. Compared with biotech firms that completed their IPOs at an earlier stage, the R&D threshold for current biotech companies to reach later-stage financing rounds has risen significantly, as reflected mainly in the clinical progress of their core pipelines and the richness of their product portfolios. For instance, Simcere Biologics’ product portfolio includes three globally innovative drugs already on the market—Cosela®, Envita®, and Endostar®—while also laying out strategic initiatives in protein engineering, T-cell engagers, NK-cell engagers, AI-assisted molecular design, protein degraders, and antibody-drug conjugates (ADCs).

Top 10 Domestic Biopharmaceutical Financing Deals in H1 2024 Data Source: VCBeat Database

In addition to Midu Bio, Lanacheng, another company on the Top 10 list, is also engaged in radiopharmaceutical-related businesses. As a subsidiary of Dongcheng Pharmaceutical, its 177Lu-LNC1011 injection has received FDA approval and is poised to initiate Phase I clinical trials.

Relatively Dispersed Financing Scale; Nearly Half of Projects Are in Early to Mid-Stages; Medical Robotics and Synthetic Biomaterials Projects Are in High Demand

In the first half of 2024, the largest single investment in the global medical device sector was completed by Biosensors International, a subsidiary of Blue Sail Medical, which raised $900 million in January 2024. Biosensors International is the cardiovascular and cerebrovascular division of Blue Sail Medical. Backed by its parent company, Blue Sail Medical ranks fourth globally in market share for coronary stents, trailing only Abbott, Medtronic, and Boston Scientific, and holds the second-largest market share in China.

Top 10 Global Medical Device Financings in H1 2024 Data Source: VCBeat Orange Database

In the Top 10 list, Accumed Medical raised $200 million in its Series A+ financing round, making it the company at the earliest funding stage. Accumed Medical independently developed pulsed field ablation technology in November 2020 and is a leading platform-based innovative technology company in the field of cardiac electrophysiology in China. In addition, Ruilong Nuofu, Tuge Medical, and WaterThane Electronics are all Series B companies.

Leading Innovation in Minimally Invasive Surgical Devices, Focusing on Series A+/B Projects

In China, the largest single financing round for medical device companies in the first half of 2024 also went to Blue Sail-Biosensors. Suzhou Elite Analytical Instruments, which completed its Series A+ financing in April 2024, is another company on the list at a relatively early stage of funding. Established in 1993, Suzhou Elite Analytical Instruments specializes in the field of liquid chromatography. Its products are 100% designed in China, with over 95% of components domestically sourced. The company has cumulatively sold more than 17,000 liquid chromatography instruments, while column sales have surpassed the 200,000-unit mark, securing a leading market share in China.

Top 10 Medical Device Financings in China (H1 2024) Data Source: VCBeat Orange Database

Boya New Materials, which completed its Pre-IPO financing round in March 2024 and is engaged in the R&D, production, processing, and sales of intraocular lens materials, disclosed its filing report for IPO tutoring in early July.

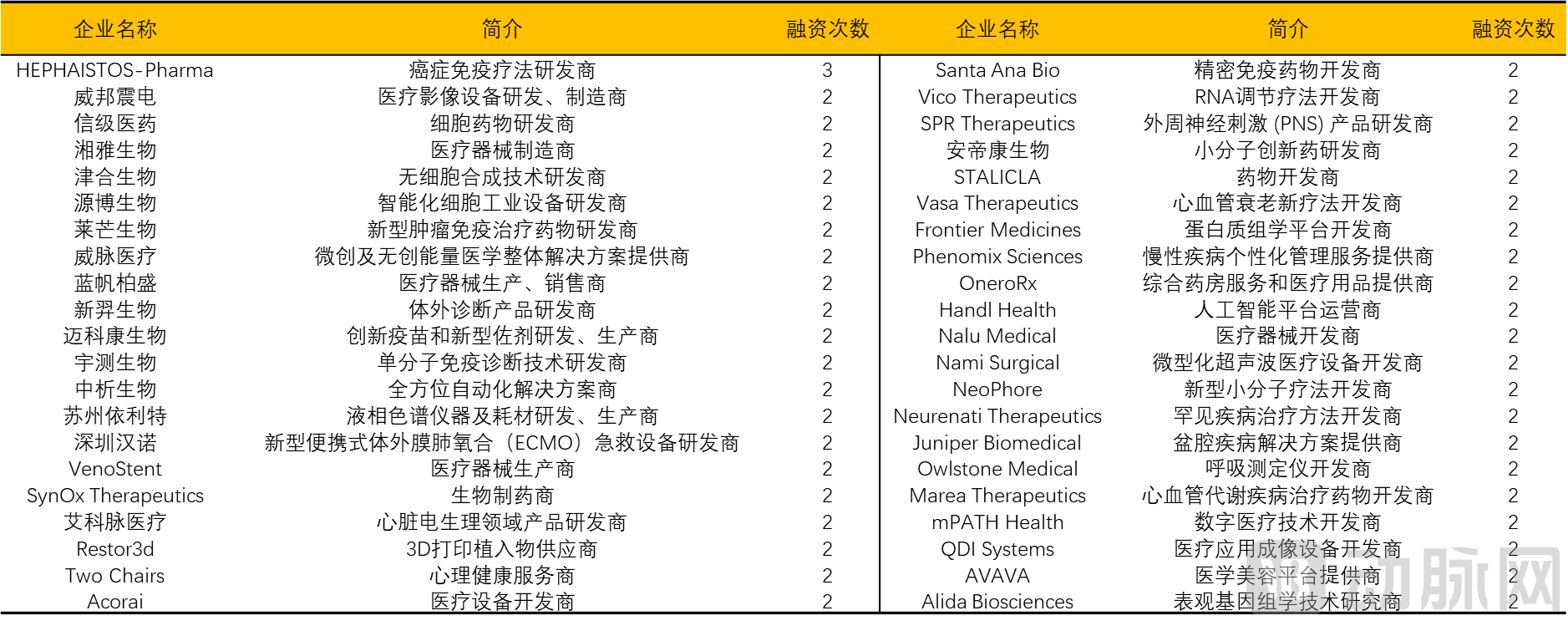

42 Global Companies Complete Two or More Funding Rounds; Concentration of Capital Inflows Slows

Analysis of Global Healthcare Investment and Financing Trends in H1 2024 | Data Source: VCBeat Orange Database

Analysis of Global Healthcare Investment and Financing Trends in H1 2024 | Data Source: VCBeat Orange Database

In H1 2024, 42 global companies completed two or more rounds of financing, accounting for 3.6% of the total, a significant decrease from 8.6% in the same period of 2023. This indicates that healthcare primary market funds are beginning to seek new project investment opportunities. Among them, France-based HEPHAISTOS-Pharma, a biotech company engaged in the development of innovative oncology therapies, was the only enterprise to complete three rounds of financing in the past six months.

III. Review of Healthcare IPOs Listed in H1 2024

IPO Pace Slows Further as U.S.-Listed Biopharmaceutical Companies Become the Mainstay of IPOs

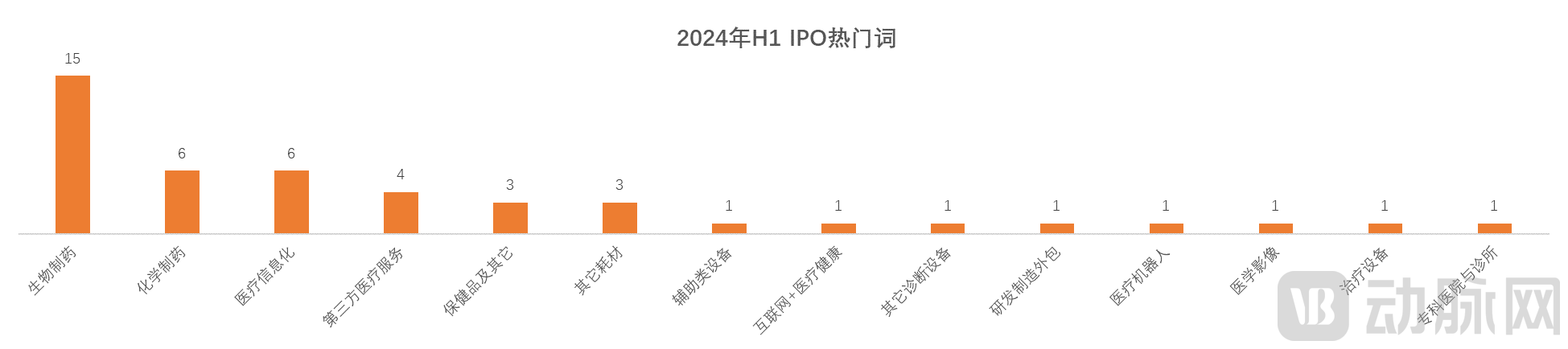

In H1 2024, nearly 47 companies completed initial public offerings (IPOs) in the global healthcare market. Among them, 15 biopharmaceutical companies went public, making biopharmaceuticals the hottest segment for IPOs globally.

In the United States, in H1 2024, a total of 32 companies went public, including 12 biopharmaceutical firms, 5 chemical pharmaceutical firms, and 5 healthcare IT companies, accounting for 68% of the global total, making it the capital market with the highest IPO activity worldwide.

Global Healthcare IPO Distribution in H1 2024 Data Source: Arterial Orange Database

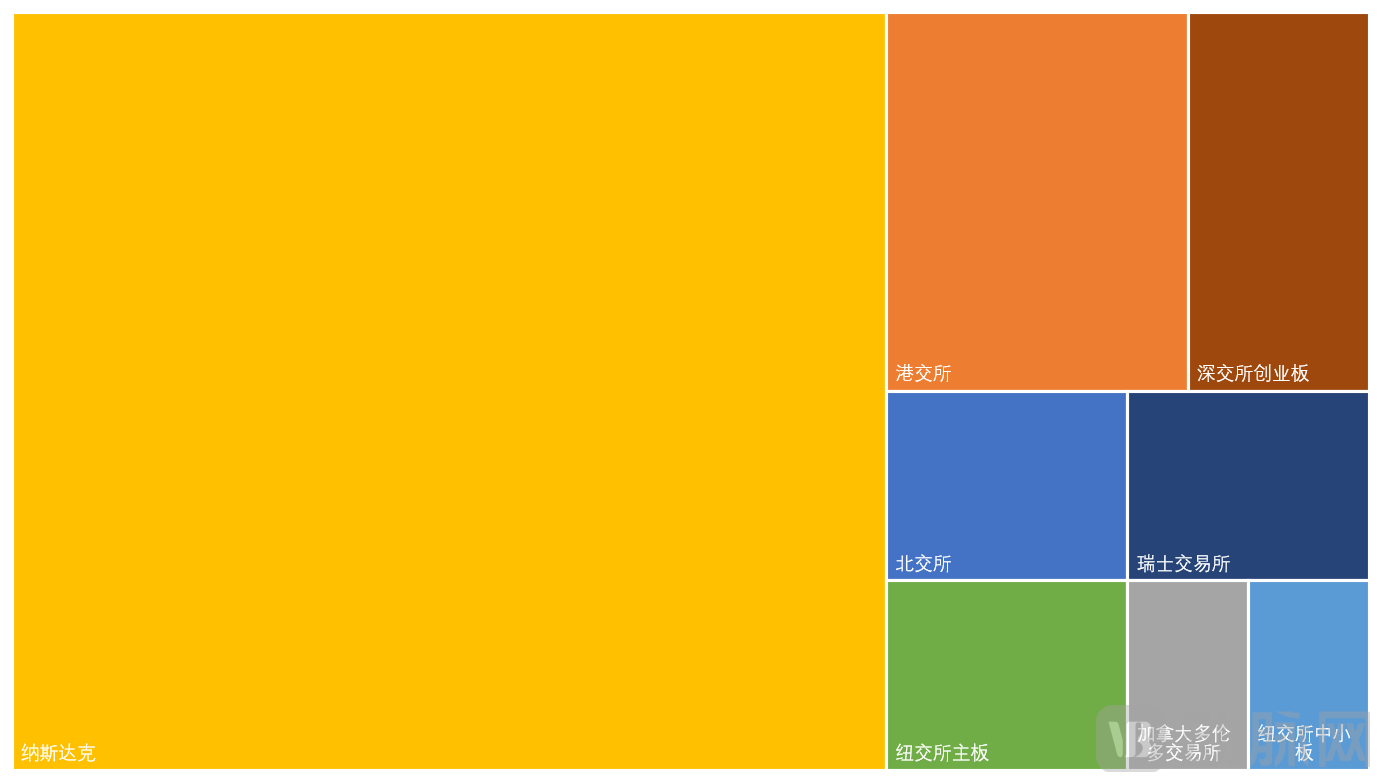

Nasdaq Holds Half the Market; Hong Kong Stock Exchange Shows Clear Recovery; STAR Market Adds No New Listings

In H1 2024, the Nasdaq market completed 31 IPOs, making it the hottest capital market for IPOs with a share of 65.9%; followed by the Hong Kong Stock Exchange, which completed 5 IPOs in H1 2024. Meanwhile, the STAR Market of the Shanghai Stock Exchange, previously a popular destination for domestic biotech IPOs, saw no new healthcare-related IPOs in the past six months.

Capital Market Choices for Global Healthcare IPOs in H1 2024 Data Source: VCBeat Database

Notably, the five HKEX listings in H1 2024 were from XtalPi, Yimai Yangguang, Shenghe Biopharmaceuticals, Quanxin Biotech, and Meizhong Jiahe, all of which are mainland Chinese companies listing in Hong Kong.

In recent years, the traditional hotspots for initial public offerings (IPOs) of domestic healthcare and medical enterprises have been undergoing adjustments to their listing rules. The listing requirements for the STAR Market and the ChiNext Board have become increasingly stringent after multiple rounds of revisions. In contrast, the Beijing Stock Exchange and the Hong Kong Stock Exchange have continuously adjusted their standards, bringing more medical innovation companies closer to the prospect of an IPO.

IPO Fundraising Amounts Shrink Significantly, Domestic Biotech Firms Become Regulars Again

In H1 2024, the largest IPO in the global healthcare market was completed by Waystar. In June 2024, Waystar listed on the Nasdaq, raising $967.5 million through its IPO. Waystar is a company that provides cloud-based payment software systems for healthcare providers (such as large hospitals, health systems, physician groups, clinics, surgical centers, and laboratories). It was formed in 2017 through the merger of Navicure and ZirMed.

Top 10 Global Healthcare IPOs by Financing Amount in H1 2024 Data Source: Artery Orange Database

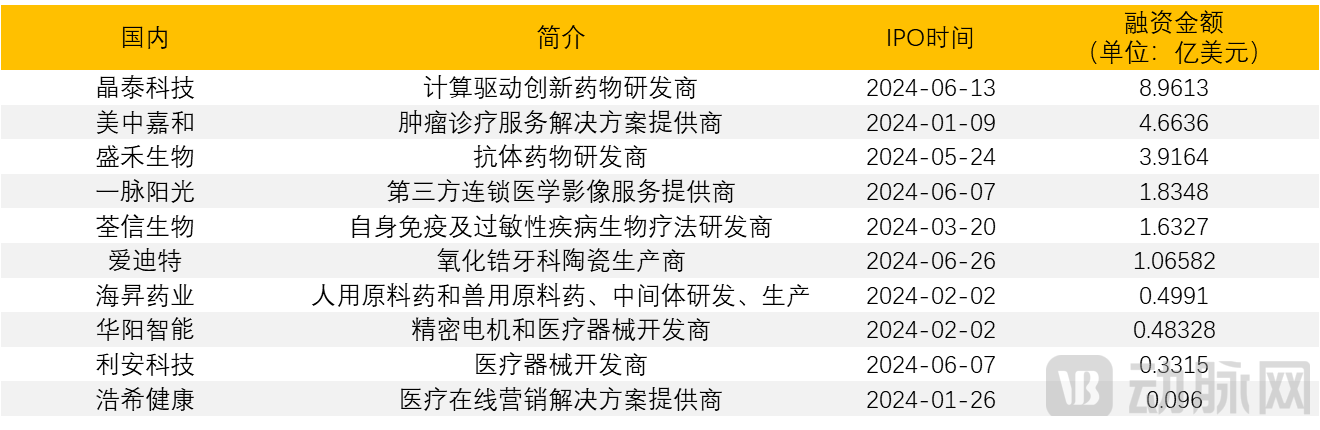

In China, XtalPi’s IPO completed in June 2024 ranked first in terms of funds raised. XtalPi is the first company to successfully list under the Hong Kong Stock Exchange’s new listing rules for specialized and sophisticated technology companies (Chapter 18C), and it is also the first publicly traded AI-driven drug discovery company.

Furthermore, Meizhong Jiahe, Shenghe Biotechnology, and Quanxin Biotechnology—among the top 10 domestic healthcare IPOs in China during the first half of 2024—are all biotech companies, signaling a promising recovery in the IPO market for Chinese innovative drugs.

Top 10 IPO Financings in China’s Healthcare Industry in H1 2024 Data Source: VCBeat Orange Database

IV. Analysis of Active Healthcare Investment Institutions in H1 2024

RA Capital Made 33 Investments in Total, Becoming a Phenomenally Active Investment Firm in the First Half of the Year

In H1 2024, RA Capital was the most active institution in the global healthcare sector, with a cumulative total of 33 investments in the first half of the year. This figure approached its full-year investment count in 2023 (over 40 deals), demonstrating a clear preference for the innovative drug sector. Notably, RA Capital made 13 more investments than Perceptive Advisors, which ranked second in terms of deal volume, underscoring RA Capital’s phenomenal level of activity. Meanwhile, consistent with its strategy in 2023, RA Capital continued to focus on antibody drugs and anti-tumor medications in the first half of 2024.

Top 10 Most Active Investors in Global Healthcare Financing and Investment in H1 2024 Data Source: VCBeat Orange Database

Moreover, the trend of “investing early and in small ventures” over the past two years has not garnered strong resonance among active global investment institutions. These firms have shown a greater preference for companies in the growth or even mature stages, and some have continued to increase their stakes in publicly listed companies, adopting a risk-averse investment strategy.

Preferences are more concentrated and convergent, with risk aversion becoming the primary strategy

In H1 2024, Qiming Venture Partners was the most active investor in China’s healthcare and medical sector, making a total of 12 investments, primarily focused on medical devices. Similar to 2023, Qiming Venture Partners continued to increase its stakes in previously invested companies during the first half of 2024, such as making its third follow-on investment in a gene-editing drug platform. Meanwhile, early-stage high-value consumable projects with high potential remained a key focus for Qiming Venture Partners.

Top 10 Most Active Investors in China’s Healthcare Industry in H1 2024 Data Source: VCBeat Database

Despite industry trends and guidance from local government policies suggesting that domestic investment institutions should prioritize early-stage investments and deepen their engagement in the early stages of healthcare, the growing uncertainty across the entire healthcare sector in the first half of 2024 has made doubling down on companies in the growth or even mature stages a risk-averse strategy. Furthermore, compared with the more diversified area preferences of active global investment firms in the first half of 2024, leading Chinese institutions have concentrated more heavily on the biopharmaceuticals and medical devices sectors.

V. Regional Distribution of Global Healthcare Investment and Financing Hotspots in H1 2024

U.S. Total Financing Rises Month-on-Month; Swiss Capital Market Shows Significant Momentum

In H1 2024, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, Switzerland, and France.

Hotspots for Global Healthcare Primary Market Financing and Investment in H1 2024 Data Source: VCBeat Orange Database

The United States led globally with 536 financing deals totaling $21.677 billion; although the number of deals fell short of the previous year, the total financing amount increased by approximately 16% compared to the first half of 2023 (approximately $18.654 billion), reflecting heightened capital concentration.

The European countries ranked among the top five globally all face a similar situation: life sciences investors began 2024 with an optimistic outlook; meanwhile, the proportion of total healthcare expenditure to GDP has been rising year by year, inversely driving capital inflows into healthcare companies with the potential to reduce costs and improve efficiency.

Among them, Switzerland has actively built a policy framework with global competitiveness, established a collaborative innovation and technology transfer network, and provided diverse financing channels. Owing to its high level of integration with international markets, it has gradually become a preferred destination for the headquarters of global life sciences R&D and innovative enterprises in recent years.

Jiangsu and Shanghai Show Clear Capital Concentration Trends, with Large Strategic Investments Gradually Rebounding

In the first half of 2024, the five regions in China with the highest concentration of healthcare and medical investment and financing activities were, in order, Jiangsu, Shanghai, Beijing, Guangdong, and Zhejiang.

Hotspots for Primary Market Investment and Financing in China’s Healthcare Sector in 2024 Data Source: VCBeat Database

Jiangsu recorded a cumulative total of 81 financing events, raising $899 million (approximately RMB 6.5 billion), making it the city with the highest number of financing deals in the first half of the year. Shanghai ranked second with 75 financing events; however, it led all five major regions in total capital raised, amounting to $939 million (approximately RMB 6.8 billion).

It is worth noting that although the number of financing events in Jiangsu and Shanghai nearly halved, the total financing amount increased quarter-on-quarter compared to the first half of 2023 (1H 2023), with large-scale strategic investments showing a trend of recovery.

Please scan the QR code to add the assistant and obtain the full report. If you have already added the assistant, please proactively request the report: